[ad_1]

JHVEPhoto

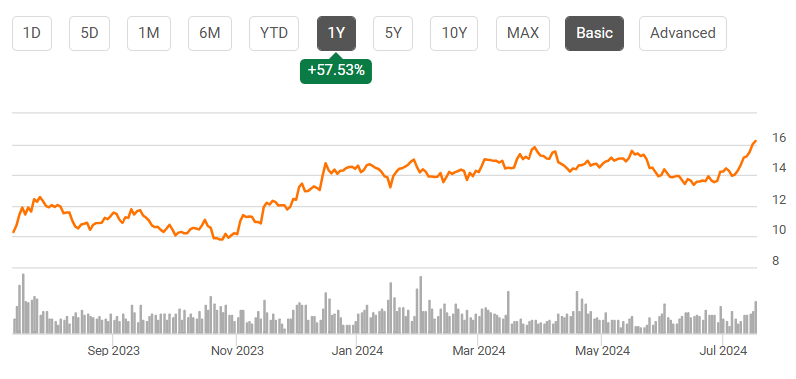

Shares of KeyCorp (NYSE:KEY) have been a robust performer over the previous 12 months, rising almost 58%, because the financial institution has recovered solidly from the regional banking disaster. On Thursday morning, Key reported a strong set of Q2 earnings, inflicting shares to drag again modestly from a 52-week-high. I final coated KEY in March, score shares a “purchase” given steadiness sheet optimization efforts, and since that advice, Secret’s up 10% vs the market’s 9% achieve. Given its massive run, I perceive the impulse to take some income; nevertheless, I see additional upside.

In search of Alpha

Within the firm’s second quarter, KeyCorp earned $0.25, a penny forward of consensus. Whereas funding prices have pressured most financial institution outcomes relative to a 12 months in the past, Key has executed a robust job managing spending with $1.08 billion in bills, flat from a 12 months in the past. The corporate can also be benefiting from improved capital market exercise. It generated $627 million in non-interest earnings, up 3% from final 12 months. Belief and funding providers had been up 10% given larger markets and web new asset progress—these tailwinds ought to additional increase leads to Q3.

Nonetheless, web curiosity earnings is essentially the most essential driver of the financial institution’s outcomes. Internet curiosity earnings of $899 million was up 1.5% sequentially and down 8.8% from final 12 months. As I wrote in March, I believed Key was at a turning level in NII with momentum set to collect later this 12 months and thru 2025. With this sequential rise, I really feel more and more assured that’s the case. General, Key’s web curiosity margin (‘NIM’) was 2.04%, up 2bps sequentially, due to a 8bps profit from rolling off fixed-rate securities and swaps and reinvesting at larger charges.

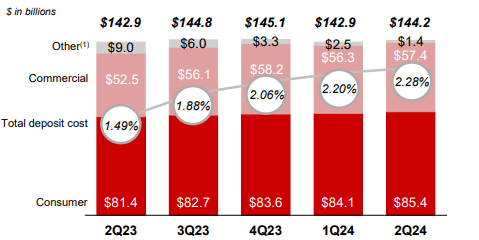

First, as I’ve written about throughout my protection of the regional banks, I view steady deposits as an important requirement to spend money on the sector. Key passes this check with relative ease. As you’ll be able to see under, Key reported $1.3 billion in deposit progress throughout Q2. Over the previous 12 months, client balances have risen a wholesome 5%.

KeyCorp

Now, deposit prices did rise by 8bps to 2.28%. That is the slowest improve in over a 12 months, and we’re doubtless nearing an inflection level right here. Destructive combine shift has contributed to larger prices, however this seems to be close to its finish. Non-interest-bearing deposits had been down simply 1% to $15 billion within the quarter. With over a 12 months to reposition NIB deposits in a 5+% fee world, remaining balances are doubtless close to operational minimums for purchasers, and I don’t count on materials additional bleed.

Moreover, I’m presently anticipating the Federal Reserve to start decreasing charges in September and interact in a average fee slicing cycle. Given its ongoing deposit progress, this positions Key to be comparatively aggressive in passing these fee cuts by means of to purchasers. Given a reduce is probably in September, that will likely be extra of a profit to This autumn outcomes, and Q3 ought to symbolize the height in Key’s deposit prices for my part.

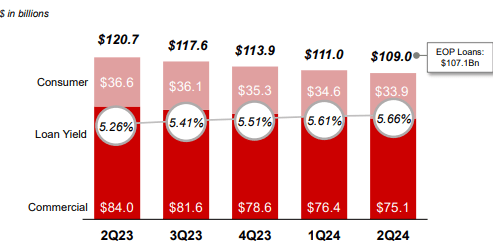

On the mortgage aspect, Key continues to see tepid demand, with some progress anticipated within the second half. Some potential debtors are doubtless anticipating decrease rates of interest in a number of months, and so they could also be deferring borrowing exercise till these charges materialize. Within the meantime, Secret’s sustaining robust credit score requirements and permitting loans to say no. As you’ll be able to see under, loans are down about $2 billion sequentially. ($1.3 billion attributable to industrial loans and $730 million in client). Its common client FICO rating is 766, a wholesome stage.

KeyCorp

Notably, loans are down almost 10% from a 12 months in the past, at the same time as deposits are larger. This has left Key with a really robust liquidity place, and it has only a 74% loan-to-deposit ratio. There may be vital room to develop loans as calls for get well, which might be a fabric web curiosity earnings tailwind.

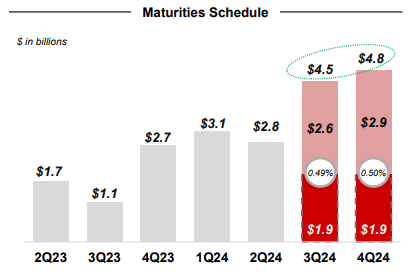

Moreover, Key, like many banks, has been weighed down by a big portfolio of fixed-income securities purchased when rates of interest had been a lot decrease. As these bonds mature and roll off, it will probably reinvest them at as we speak’s larger market yields, boosting NII. Even because the Fed begins decreasing charges, legacy bonds had been purchased at such decrease yields that there will likely be ongoing accretion. For now, KEY has basically been holding its securities portfolio flat at about $45.4 billion, merely rolling maturities.

There’s a significant stage of maturing bonds and fixed-rate swaps over the steadiness of the 12 months. As famous above, maturities added 8bps to NIM in Q2. I count on ongoing accretion, and KEY ought to be capable of broaden web curiosity earnings towards $1 billion by This autumn, up $100 million from Q2 ranges given this, an $0.08 profit to quarterly EPS.

KeyCorp

Except for rate of interest traits, Key’s credit score high quality stays strong. Importantly, simply 13% of loans are within the industrial actual property sector, which is the world the place I’ve the best concern. This comparatively modest publicity positions Key effectively relative to rivals for a possible downturn. In the course of the quarter, Key took $100 million in provisions for credit score losses, down $1 million sequentially and $67 million from final 12 months. This reserving replenished $91 million of web charge-offs and added $10 million of incremental provisions.

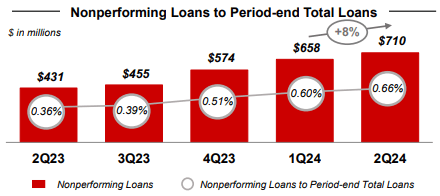

As you’ll be able to see under, Key has seen a modest deterioration in nonperforming loans, because the financial cycle continues to age. Importantly, KEY has already reserved for some additional deterioration. It has $1.83 billion of allowances, protecting 1.71% of loans. That is 257% of protection, above my wholesome 250% stage. As such, I don’t count on provisions to rise a lot past the $100 million/quarter tempo, absent a recession. Certainly, if the Fed lowers borrowing prices later this 12 months, that will assist to restrict mortgage losses.

KeyCorp

Key can also be effectively capitalized with a ten.5% widespread fairness tier 1 (CET1) capital ratio, up 23bps sequentially and 122bps from final 12 months, above the ~9.5% space it must run its enterprise safely. One cause KEY is holding extra capital is due to its unrealized losses on its mounted earnings portfolio. It will have a 7.3% CET1 ratio adjusted for its AOCI loss. Importantly, its AOCI loss will shrink by about $900 million by the tip of subsequent 12 months, decreasing the capital headwind by almost 80bps. Moreover, its AOCI loss will be phased in progressively beginning subsequent 12 months. As such, whereas I count on Key to retain additional capital, it’s effectively positioned to maintain CET1 above goal.

KeyCorp

Alongside outcomes, Key up to date steering. It has raised its deposit steering barely whereas decreasing its mortgage progress forecast. In any other case, there have been no materials adjustments. Finally, its larger deposit base will enable it to speed up mortgage progress when demand does get well. For now, it’s prudent to keep away from loosening credit score requirements an excessive amount of to power progress and threat credit score losses ought to the financial system flip down.

KeyCorp

General, Key reported strong outcomes. Importantly, it has a transparent runway to earnings progress, as it’s set to profit from maturing bonds being reinvested at prevailing yields. The first threat to this outlook could be a surge in credit score losses, which seems unlikely given restricted CRE publicity, strong reserves, and an financial system I count on to develop.

KEY is effectively positioned to develop EPS in the direction of $0.35 by This autumn and proceed to develop earnings in 2025 in the direction of $1.80 given this dynamic. With shares simply 9x 2025 earnings and a steadiness sheet with vital extra liquidity, I see shares as enticing. I proceed to count on them to rally towards $18, making a 15+% whole return alternative given its 5% dividend yield. As such, I proceed to view Key as a purchase.

[ad_2]

2024-07-18 17:41:18

Source :https://seekingalpha.com/article/4704887-keycorp-q2-points-to-ongoing-net-interest-income-gains?source=feed_all_articles

{kind=link}

Discussion about this post