[ad_1]

D-Keine/iStock by way of Getty Pictures

Since my first promote score on Amplify Excessive Revenue ETF (NYSEARCA:YYY) in February 2021, its share value is down -27% and its whole return is +9% (earlier than tax on distributions), whereas the S&P 500 index has gained 42%. Though YYY has carried out decently within the final 10 months, this text renews my long-term destructive opinion within the gentle of up to date knowledge.

YYY technique

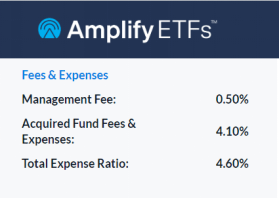

Amplify Excessive Revenue ETF (YYY) is a high-yield fund that launched on 6/21/2013 monitoring the ISE Excessive Revenue Index. It has a portfolio of 60 closed-end funds (CEFs), a distribution fee of 11.85% and a 30-day SEC yield of 10.45%. The expense ratio is extraordinarily excessive, even in contrast with different funds of funds: 0.50% in administration charges plus 4.10% in held fund bills, totaling 4.60%! You will need to see it to imagine it:

YYY charges on 9/6/24 (Amplify ETFs web site)

As described by Amplify ETFs, the underlying index:

selects CEFs ranked highest general by ISE within the following components: Yield, Low cost to Web Asset Worth (NAV), and Liquidity. This funding strategy ends in a portfolio which accommodates quite a lot of asset lessons, funding methods and asset managers.

Eligible funds should be listed within the U.S., have a capitalization of not less than $500 million and a median day by day buying and selling quantity of not less than $1 million. They’re ranked based mostly on a rating together with 3 components: yield, low cost to NAV and liquidity. Constituents are chosen and weighted based mostly on their rating, with some changes. The index is reconstituted twice a yr, in January and July.

The fund modified names in 2019, holding the identical ticker and methodology. The methodology modified in July 2021: the variety of holdings elevated from 30 to 45, the constituent weight was capped at 3%, and the reconstitution turned semi-annual (beforehand annual). It appears there was one other modification in 2024, leading to an inconsistency on Amplify ETFs web site as of 9/6/2024: it stories a listing of 60 holdings, whereas the index methodology doc nonetheless claims that “the Index seeks to have 45 parts, that quantity must be thought-about a most restrict”. I do not like funds that change their methodologies: it could be a clue of failing technique.

Portfolio

BlackRock is the heaviest fund sponsor within the portfolio (23% of asset worth), adopted by abrdn (15%) and Nuveen (14%). As of writing, YYY is diversified throughout asset lessons: 59% of asset worth is in bonds and 41% in shares. These numbers might change over time. The heaviest subclass is senior loans, with 16% of property. The highest 10 holdings, listed within the subsequent desk, signify 32.2% of asset worth, and the heaviest place weighs 3.92%. Subsequently, the portfolio is well-diversified and dangers associated to particular person funds are low to average.

|

TICKER |

NAME |

WEIGHT |

|

CBRE World Actual Property Revenue Fund |

3.92% |

|

|

Nuveen Credit score Methods Revenue Fund |

3.28% |

|

|

Western Asset Diversified Revenue Fund |

3.27% |

|

|

NYLI CBRE World Infrastructure Megatrends Time period Fund |

3.23% |

|

|

Nuveen Floating Price Revenue Fund/Closed-end Fund |

3.17% |

|

|

Aberdeen Asia-Pacific Revenue Fund Inc |

3.14% |

|

|

abrdn Healthcare Traders |

3.10% |

|

|

BlackRock Capital Allocation Time period Belief |

3.06% |

|

|

BlackRock ESG Capital Allocation Time period Belief |

3.03% |

|

|

BlackRock Well being Sciences Time period Belief |

2.97% |

Closed-end funds are sometimes chosen by buyers for his or her excessive yields. Additionally they have a couple of metrics that aren’t relevant to shares and ETFs. Two of them are extra necessary than the yield:

- Low cost to NAV (increased is best);

- Relative low cost = Low cost to NAV minus its 12-month common (increased is best).

The latter is significant as a result of the low cost typically reveals a mean-reversion sample. The subsequent desk compares these metrics within the full CEF universe and a pattern of 37 holdings of YYY (excluding these for which my knowledge supplier doesn’t have all the knowledge).

|

Mixture low cost % |

Mixture relative low cost % |

|

|

YYY Holdings (37) |

5.30 |

-2.77 |

|

CEF universe |

6.18 |

-2.39 |

Calculation with Portfolio123

This pattern of holdings is a bit inferior to the CEF universe concerning these valuation metrics, so YYY valuation is probably going barely below-par.

Previous efficiency

Since 7/1/2013, YYY has underperformed its largest competitor, Invesco CEF Revenue Composite ETF (PCEF). The subsequent desk additionally features a benchmark of mine: a simulated portfolio of the 100 CEFs with increased yields amongst these with a median day by day buying and selling quantity above $100,000 and a optimistic low cost. It’s reconstituted twice a yr in equal weight to make it akin to the underlying index.

|

Since 7/1/2013 |

Complete Return |

Annual Return |

Drawdown |

Sharpe ratio |

Volatility |

|

YYY |

58.58% |

4.21% |

-42.52% |

0.26 |

13.92% |

|

PCEF |

90.08% |

5.91% |

-38.64% |

0.42 |

12.51% |

|

My Benchmark |

123.91% |

7.47% |

-42.88% |

0.46 |

15.03% |

Knowledge calculated with Portfolio123

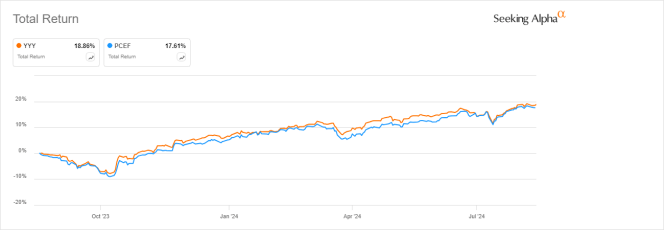

YYY underperforms in whole return, and in addition in risk-adjusted efficiency (Sharpe ratio). Nevertheless, it’s marginally forward of PCEF during the last 12 months:

YYY vs PCEF, 12-month whole return (In search of Alpha)

The annualized return, together with distributions, is beneath the distribution fee’s historic common (which is over 8%). It means YYY paid excessive yields whereas it was struggling a decay in worth. The subsequent chart confirms it: the share value has misplaced 46% since 7/1/2013. Including to the ache, the cumulative inflation in the identical time was over 30%, based mostly on CPI knowledge. PCEF was a bit higher at preserving capital, though a 20% loss isn’t fairly both.

YYY share value historical past (In search of Alpha)

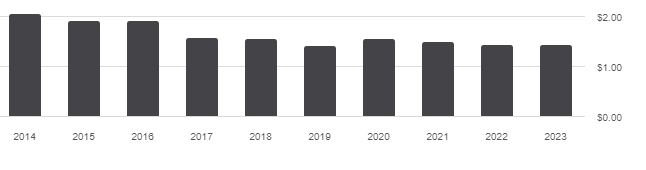

The distribution historical past isn’t extra engaging. The annual sum of distributions decreased from $2.06 per share in 2014 to $1.44 in 2023. For shareholders, it’s a 30% lack of revenue stream in 9 years, whereas the cumulative inflation was about 30%.

YYY distribution historical past (In search of Alpha)

Takeaway

Amplify Excessive Revenue ETF could also be utilized in short-term trades to revenue by some market anomalies. Nevertheless, it has been a nasty long-term funding since its inception in 2013, exhibiting a big decay in worth and distribution. It’s unlikely to immediately develop into a winner. Anyway, its ridiculous expense ratio of 4.60% is adequate purpose to keep away from it.

[ad_2]

2024-09-06 21:42:32

Source :https://seekingalpha.com/article/4719634-yyy-long-term-decay-and-excessive-expense-ratio?source=feed_all_articles

{kind=link}

Discussion about this post