[ad_1]

loveguli

Yum China Holdings, Inc. (NYSE:YUMC) gives a lovely shopping for alternative after good Q2 2024 outcomes, and a major cluster of insider shopping for exercise within the days following the incomes launch.

On this article, I’ll stroll you thru the totally different elements of my funding thesis, and I’ll attempt to convey in probably the most direct means potential the totally different occasions that motivated my Sturdy Purchase ranking.

Moreover, I’ll undergo among the headwinds in Q2 2024, particularly their strategic transfer with Pizza Hut WOW, which I consider poses a threat to my Sturdy Purchase ranking within the occasion of an financial downturn.

Nevertheless, contemplating that my timeframe is comparatively quick (three to 24 months) I consider this inventory has an uneven alternative within the quick to mid-term.

As at all times, I’ll start with an organization overview part for these readers new to this inventory.

Firm Overview

Yum China is a Shanghai primarily based firm that operates numerous eating places in China, specializing in quick meals and informal eating.

They’ve unique rights to function and sublicense the KFC, Pizza Hut, and Taco Bell manufacturers in China.

Moreover, they personal the mental property of two manufacturers, Little Sheep and Huang Ji Huang. You may not be acquainted with these two names until you’ve got just lately frolicked in China.

They make most of their income by way of their KFC and Pizza Hut eating places. To present you an thought in regards to the relative weight of every phase, I’ve included beneath a breakdown of their annual income in 2023.

| Section | 2023 Income (in tens of millions) |

|---|---|

| KFC | $8,240 |

| Pizza Hut | $2,246 |

| All Different Segments | $779 |

| Company and Unallocated | $293 |

Writer’s compilation from the newest 10-Okay.

As a aspect be aware, all different segments embrace income from manufacturers like Lavazza, Huang Ji Huang, Little Sheep, Taco Bell, their supply working phase, and their e-commerce enterprise.

Regarding the helpful possession (as of April 11, 2024) of the corporate, I’ve to confess that I’m disenchanted by the truth that the combination possession throughout all administrators and government officers within the firm is lower than 1%.

SEC 14A SEC – 14F

Nevertheless, my funding type leans extra on insider shopping for exercise (particularly after a latest selloff) reasonably than complete frequent inventory possession within the firm.

In case you are questioning why, is as a result of my timeframe is comparatively quick, between three and 24 months, most of the time, involving extremely illiquid name choices. Subsequently, once I see cluster insider shopping for exercise after a decline within the share worth, I’ve a excessive conviction that administration believes that the present share worth is affordable (emphasis on present). In any other case, if insiders personal 40% of the corporate however do not buy after a selloff, I can’t infer the identical reasoning.

Latest Efficiency

I like to begin my dinner with the cake, so I’ll cowl the headwinds first, regardless of their respectable Q2 2024 outcomes.

My funding type favors corporations with excessive margins and low volumes, primarily throughout their flexibility throughout financial downturns. Taken as a right that fast-food eating places are extra targeted on volumes than rising their margins, I thought of going by way of their strategic initiatives, one among which, the Pizza Hut WOW idea, raised my eyebrow.

This idea was designed to cater to a broader viewers, notably solo diners and worth aware clients. The primary thought is that by providing smaller portion sizes and cheaper meals, Pizza Hut WOW would meet the wants of a broad viewers who prefers eating alone, or are searching for a fast meal at an inexpensive worth.

Look, I will be trustworthy with you, nothing dangerous with this. I used to be born in a socialist nation, so from an moral standpoint, I prefer it. Extra folks eat extra, at extra affordable costs, resulting in extra staff required to satisfy the elevated demand.

Nevertheless, from a purely financial standpoint of view, I do not consider that is good for his or her web earnings, in the long term, particularly within the occasion of an financial downturn.

Contemplating that the working bills for his or her Pizza Hut phase have been $460 million, I see the 13.2% margin in danger within the occasion of a slowdown within the QSR business.

Simply to make clear, I’m not saying that there shall be a slowdown in QSR, but when there’s, the margins for Pizza Hut are in danger, for my part.

Transferring on to extra optimistic outcomes, I’ve to say that, revenue-wise, this was a record-breaking Q2. Their complete income was $2.68 billion, up by 1% YoY.

Working revenue was up by 4% YoY, with a complete working margin of 9.9%, additionally up in comparison with the identical quarter final 12 months, though solely by 20 foundation factors.

I’m additionally inspired by the 11% YoY supply gross sales. As a aspect be aware, near 90% of their complete gross sales got here from digital gross sales, by way of digital apps to order quick meals.

Outlook

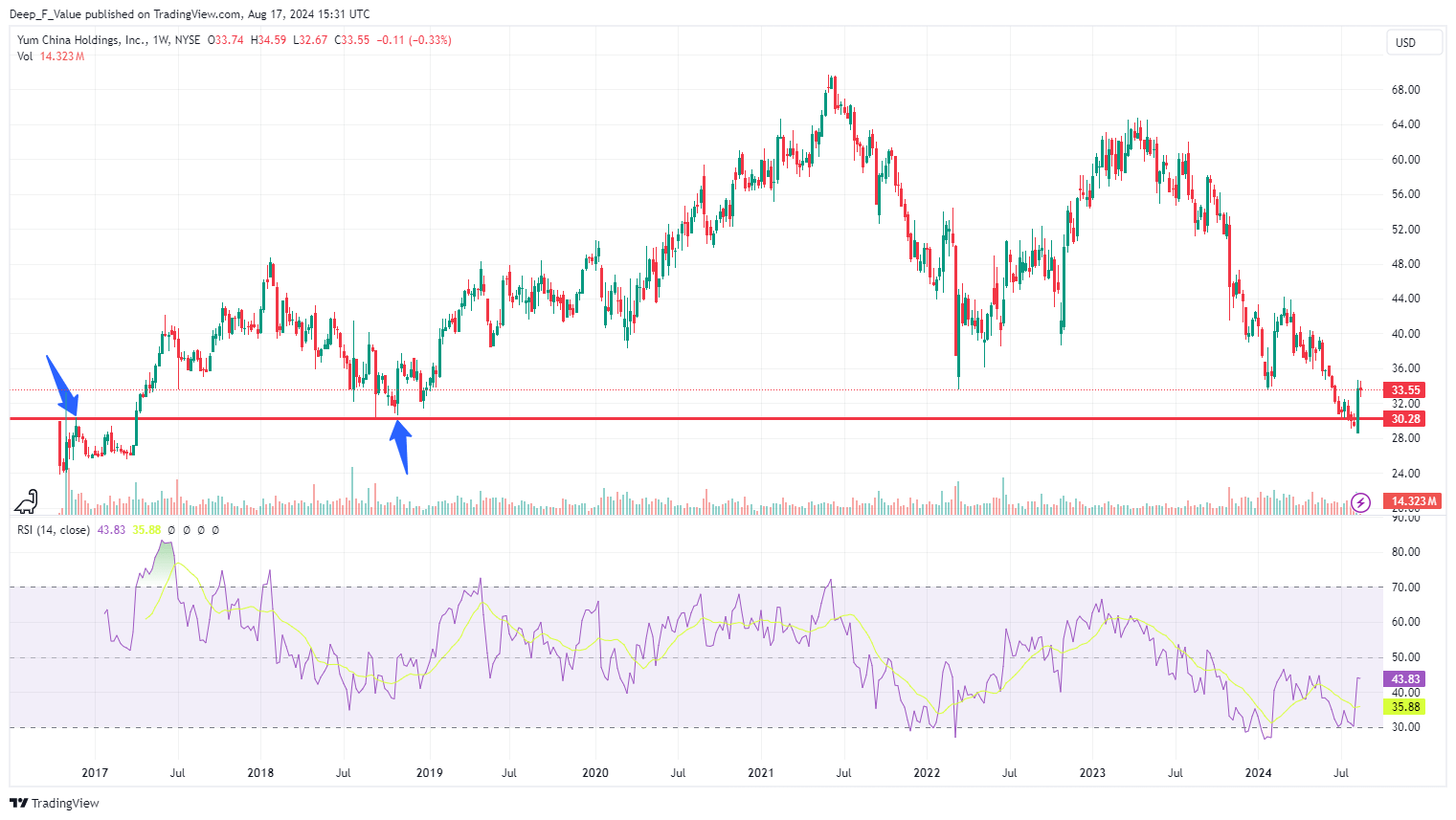

Let’s have a fast have a look at the share worth on a weekly chart.

Buying and selling View

As a contrarian deep worth investor, I really like this chart for the next causes:

- YTD decline (previous to Q2 2023 earnings launch) of 33%.

- If we glance additional again, since April 2023 the share worth declined by over 50%.

- The worth bounced on a validated (for my part) help degree from 2019.

Alright, the chart appears good, however that is simply the tip of the iceberg.

Let’s proceed to the financials.

Working earnings is up, which is sweet.

Buying and selling View

I’m additionally inspired by the elevated working and web earnings margins since 2022.

Buying and selling View

Fast and present ratios above 1, and debt to belongings beneath 0.5, which is an effective indicator that they will handle each their quick and long-term debt, for my part.

Quarterly dividend in place, with a low dividend yield beneath 2%, TTM. This can be a good indication, as they do not have to surrender a major quantity of their free money circulation to pay dividends.

Talking of cashflows, each working and free money circulation are up.

Buying and selling View

Valuation-wise I really like the truth that a lot of the valuation metrics are beneath the corporate’s five-year common. Provided that they function within the Chinese language market, I do not look an excessive amount of on the comparability with the broader shopper discretionary sector.

So, the weekly chart reveals a selloff, the monetary statements look respectable, and the valuation ratios are beneath the five-year common (nice!). Now I’ll deal with insider shopping for exercise.

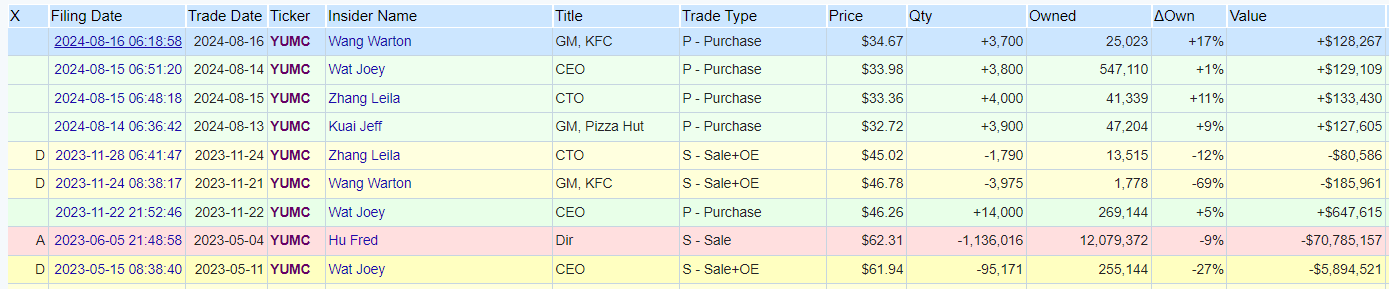

I thought of together with a screenshot exhibiting the appreciable cluster insider shopping for exercise, after the 20% bounce within the share worth following Q2 earnings outcomes (emphasis on after).

OpenInsider

Earnings have been launched on August 5, after market shut. Insiders began shopping for between August 13 and 16.

I’m extremely inspired by the truth that the 5 shopping for transactions have been accomplished by 5 totally different insiders, together with the CEO, CFO, and the GM of their two largest segments.

That is the proper state of affairs for my funding type. All of the elements that I take note of are optimistic. Subsequently, I made a decision to take a daring step and buy name choices expiring in January 2025.

If my Sturdy Purchase ranking would not pan out, my portfolio goes to take a success.

Conclusion

Wrapping up, I consider Yum China presents a compelling shopping for alternative, particularly for high-risk, contrarian traders, like myself.

Regardless of seeing a excessive threat to Pizza Hut’s margins in case of an financial downturn, the general monetary well being of the corporate is powerful with a rise in income and working margins, and powerful money flows.

When in comparison with their very own five-year common, their valuation ratios look fairly respectable to me, indicating that they could possibly be undervalued.

The insider shopping for exercise, notably by prime executives, and following a 33% decline within the share worth YTD, additional reinforces my confidence within the present share worth.

Subsequently, I preserve a Sturdy Purchase ranking, holding name choices expiring in January 2025.

[ad_2]

2024-08-18 17:39:54

Source :https://seekingalpha.com/article/4715486-yum-china-insider-buying-good-valuation-ratios-q2-results-make-stock-strong-buy?source=feed_all_articles

{kind=link}

Discussion about this post