[ad_1]

Thomas Barwick/DigitalVision through Getty Photographs

Abstract

Following my protection of Wyndham Resorts (NYSE:WH) in Aug’23, which I really helpful a purchase score given the wholesome growth pipeline and capital return insurance policies, this submit is to supply an replace on my ideas on the enterprise and inventory. I persist with my purchase advice for WH as I anticipate adj. EBITDA to develop at 7% CAGR over the medium time period. The rising growth pipeline helps optimistic room progress, and secular tailwinds assist RevPAR progress, which ought to simply bridge to this degree of progress.

Funding thesis

On 24-07-2024, WH launched its 2Q24 earnings, which noticed a robust EBITDA efficiency of $178 million (~13% y/y progress) ($8 million above the road estimate of $170 million). Income progress of three.7% and 130 bps of EBITDA margin growth, from 43.6% in 2Q23 to 48.5% in 2Q24, drove this beat. Income progress was pushed by optimistic efficiency in internet unit progress [NUG], RevPAR, and home occupancy charges. NUG grew 3.9% in 2Q24 (0.9% within the US and eight.2% abroad), whereas RevPAR grew 2% on a relentless foreign money foundation (US RevPAR y/y progress was flat; worldwide RevPAR was up 7%; Larger China fell 17%; the remainder of APAC grew 3%; EMEA grew 15%; Canada grew 3%; and LATAM grew 37%). As for occupancy charges, home occupancy charges improved by ~100 bps in 2Q24.

2Q24 was little doubt a robust quarter, and one that ought to instill confidence available in the market and persuade the market that WH is on observe to proceed compounding EBITDA at 6 to eight% for the foreseeable future.

Beginning with NUG progress, the outlook stays strong. On the event entrance, WH’s pipeline grew to 245,000 rooms, a rise of two,000 rooms, which represents 7.5% y/y progress. This additionally marks the 16th consecutive 12 months of sequential progress for the corporate. Notably, WH signed 180 new growth contracts, up 33% vs. 2Q23 and in addition a sequential enchancment vs. 1Q24 (signed 171). This, to me, signifies no indicators of demand deteriorating. WH pipeline progress can also be in step with different giant lodge gamers, which means that your entire {industry} is benefiting from this demand tailwind.

By rising our scale, community of franchisee relationships, and buyer attain, we now have considerably elevated our future progress alternatives, leading to a document world pipeline of over 115,000 rooms at quarter finish, which is a ten% enhance quarter-over-quarter. Selection Resorts Worldwide 1Q24

I believe the developments on the pipeline are actually encouraging. And the factor that was actually encouraging to me, in case you take a look at the pipeline and simply examine Q1 ’24 to Q1 ’23 as a result of it is a first rate apples-to-apples comparability as a result of neither of these would have had MGM, had been up 9% year-over-year on the pipeline. Marriott Worldwide 1Q24

Turning to signings, we added practically 18,000 rooms into our pipeline within the quarter which was a rise of seven% on the same-period final 12 months. InterContinental Resorts Group 1Q24

On account of our sturdy pipeline and all the nice progress we have seen so far, for the complete 12 months, we anticipate internet unit progress of 6% to six.5%, excluding the deliberate addition of Graduate. Hilton Worldwide Holdings 1Q24

My view is that this demand tailwind ought to final for the medium to long-term as youthful generations worth expertise greater than the earlier generations. As extra of those youthful generations enter the work pressure, their disposable earnings will develop considerably, which implies the general “client pockets” obtainable for motels to seize goes up (which additionally means extra provide of motels is required). Additionally, there may be the long-term secular tailwind of extra air journey – which implies extra vacation events – that bodes nicely for lodge demand as nicely.

WH

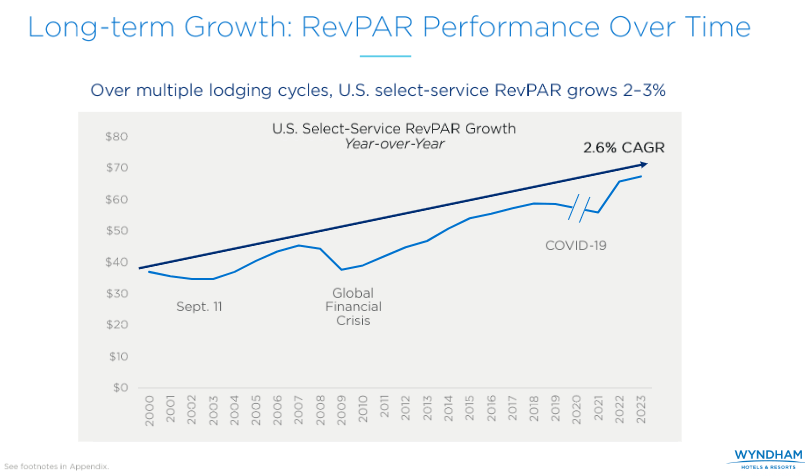

Traditionally, RevPAR has usually grown at 2 to three%, and encouragingly, 2Q24 outcomes proved that this pattern line continues to be intact as RevPAR progress grew 2% within the quarter after a stoop over the previous 2 quarters (-1% in 4Q23 and 1% in 1Q24).

There are two foremost attributes that drive RevPAR progress: common each day charges [ADR] and occupancy. As I indicated above, the demand for motels may be very favorable over the long run, and that ought to assist industry-wide ADR progress (for reference, ADR is anticipated to develop at ~2%, regardless of the present macro weak point, which implies in good instances, ADR progress might be even higher). As for occupancy, my opinion is that demand goes to return again on-line a lot quicker than the provision of motels (i.e., new motels being constructed), as building takes time. This dynamic ends in demand exceeding provide, which implies the occupancy price has to extend. WH 2Q24 outcomes have proven that home occupancy continues to enhance, and the worldwide occupancy price nonetheless has enormous room to additional recuperate to pre-COVID ranges. All in all, I believe it isn’t very tough to imagine RevPAR can proceed to develop at ~2 to three% given these dynamics.

Occupancy internationally stays a tailwind for the rest of the 12 months and is now 13% behind the place it was in 2019. EMEA and Latin-America RevPAR had been each particularly sturdy this quarter, rising year-over-year by 15% and by 37% respectively, pushed by energy in Greece, Spain, Turkiye, the Center East and throughout the Caribbean and the beginning of what seems to be to be a really sturdy summer season throughout the European continent. 2Q24 earnings outcomes name

WH

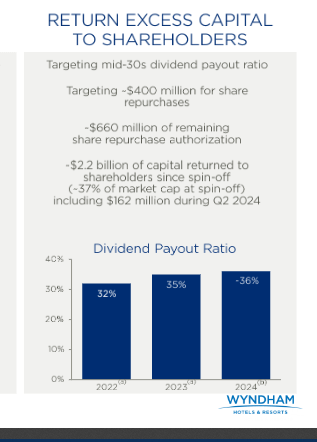

One final level to spotlight is that WH has stepped up its capital return coverage. Buyback exercise has elevated in 2Q24 from $57 million in 1Q24 to $131 million, exhibiting that administration may be very keen to return capital in good instances. With my optimistic EBITDA outlook for WH (i.e., optimistic money move progress), WH’s sturdy steadiness sheet (whole liquidity of $820 million), and a manageable leverage ratio of three.5x (in step with the administration goal vary of three–4x), WH should not have any points persevering with to buy $400 million of shares per 12 months (it nonetheless has $660 million remaining within the present share repurchase authorization).

Valuation

Personal calculation

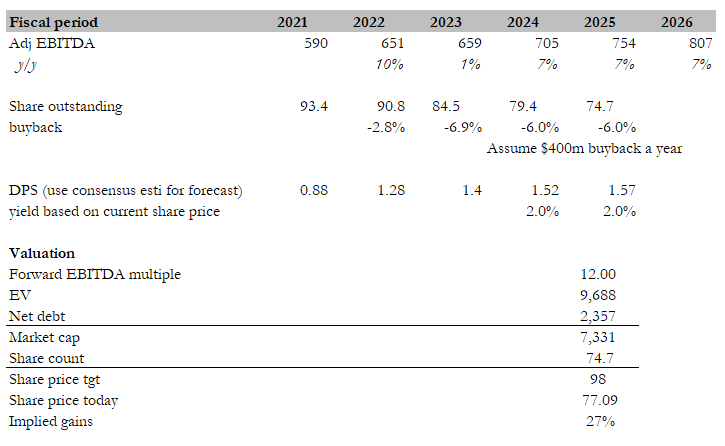

My goal worth for WH primarily based on my mannequin is $98. Since administration steerage is predicated on adj. EBITDA progress, I’ve rewired my mannequin to be primarily based on adj. EBITDA (for simpler reference). I consider there are adequate progress tailwinds to consider that 7% annual EBITDA progress is well achievable. My bridge to 7% adj. EBITDA progress is as follows: (1) high-single-digit pipeline progress interprets to mid-single-digit NUG progress + (2) 2 to three% RevPAR progress + (3) margin growth from improved occupancy charges + (4) potential upside from ancillary price streams (guided for 7% in FY24).

I’m not assuming a rise in multiples, as I consider WH is buying and selling at the place it must be. Whereas it looks as if WH is buying and selling under the historic common of 13x ahead EBTIDA, eradicating the COVID interval would present that 12x is the precise common. At 12x, my worth goal for WH is $98, assuming a $400 million buyback per 12 months. Add on the dividend yield, and the full return is near ~30%.

Threat

Growing macroeconomic and world geopolitical dangers might negatively influence leisure and enterprise journey demand and pricing, in addition to developer curiosity in motels. If charges proceed to go up, it would end in greater financing prices, which might meaningfully erode developer curiosity in new lodge building.

Conclusion

In conclusion, my score for WH is a purchase score. WH continues to point out sturdy operational efficiency, and I anticipate this degree of efficiency to proceed. Whereas near-term macroeconomic uncertainties persist, I consider the long-term fundamentals for the lodge {industry} stay intact, with favorable demographic developments and rising journey demand supporting WH’s progress.

[ad_2]

2024-07-30 13:24:44

Source :https://seekingalpha.com/article/4707957-wyndham-hotels-and-resorts-positive-adj-ebitda-growth-outlook?source=feed_all_articles

{kind=link}

Discussion about this post