[ad_1]

BING-JHEN HONG

TSMC (NYSE:TSM) not too long ago reported its 2Q24 outcomes and I joined in for the earnings name.

Earlier than I soar in on the earnings outcomes, I assumed I might first touch upon the earnings name.

In my view, the temper on the earnings name was rather more jovial in comparison with prior earnings name and CEO Wei additionally sounded extra energetic than he did earlier than.

In reality, TSMC CEO Wei even tried to be humorous by saying Nvidia (NVDA) CEO Jensen’s tagline and altering it for TSMC: “The extra TSMC wafers you purchase, the extra you save.”

Whereas the temper within the earnings name is probably not quantitative proof, it does present qualitative proof that TSMC’s enterprise may, in reality, be booming and that good occasions are forward.

I’ve written extensively about TSMC inventory on In search of Alpha, which could be discovered right here.

2Q24 outcomes

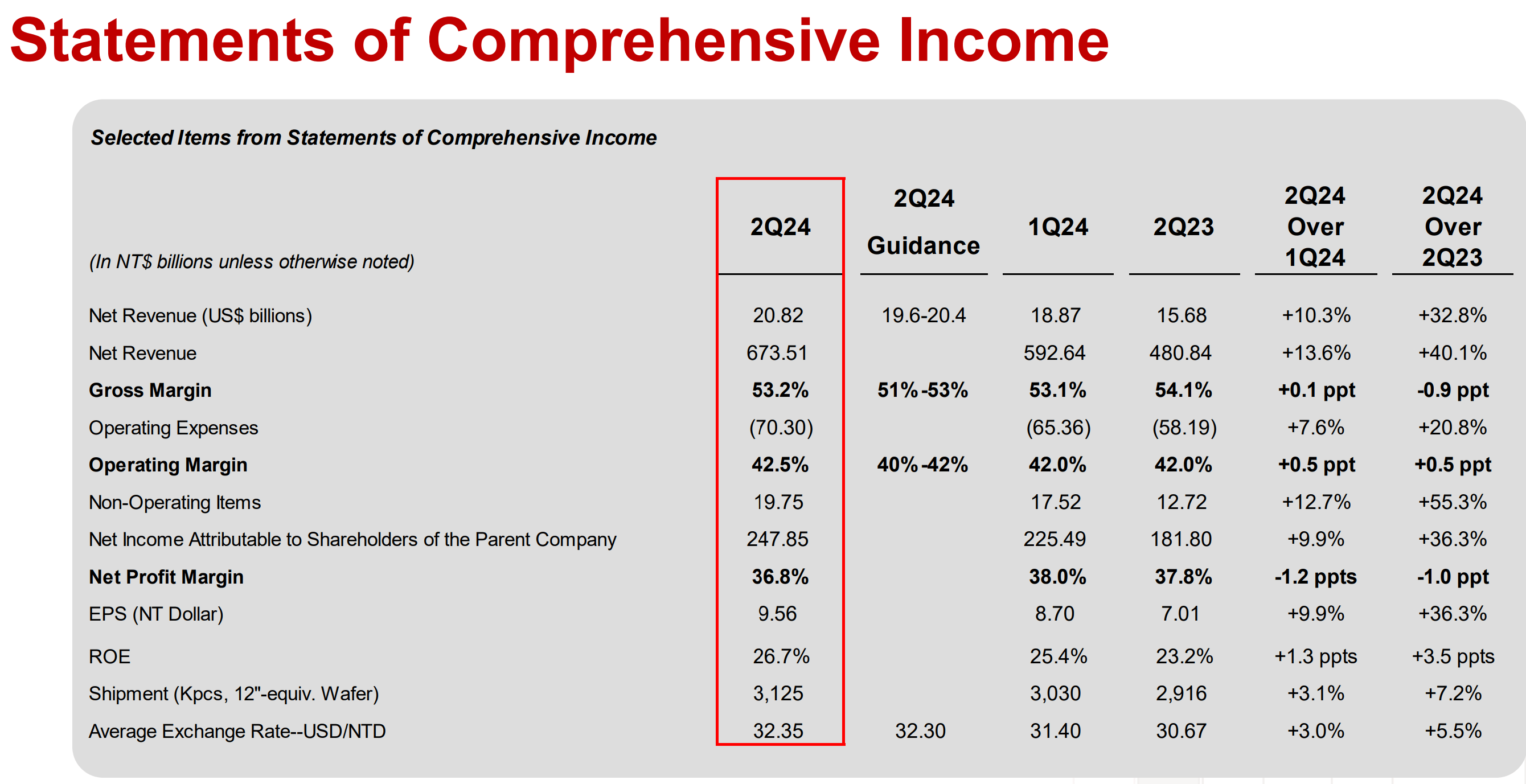

TSMC revealed 2Q24 outcomes that exceeded the highest finish of its steerage.

Here’s a abstract of the 2Q24 outcomes.

TSMC 2Q24 outcomes (TSMC)

Earlier in July, TSMC reported 2Q24 revenues of NT$673.5 billion, which was up 40% from the prior yr and up 14% sequentially. This beat the excessive finish of its personal steerage and consensus expectations by 2% to three%.

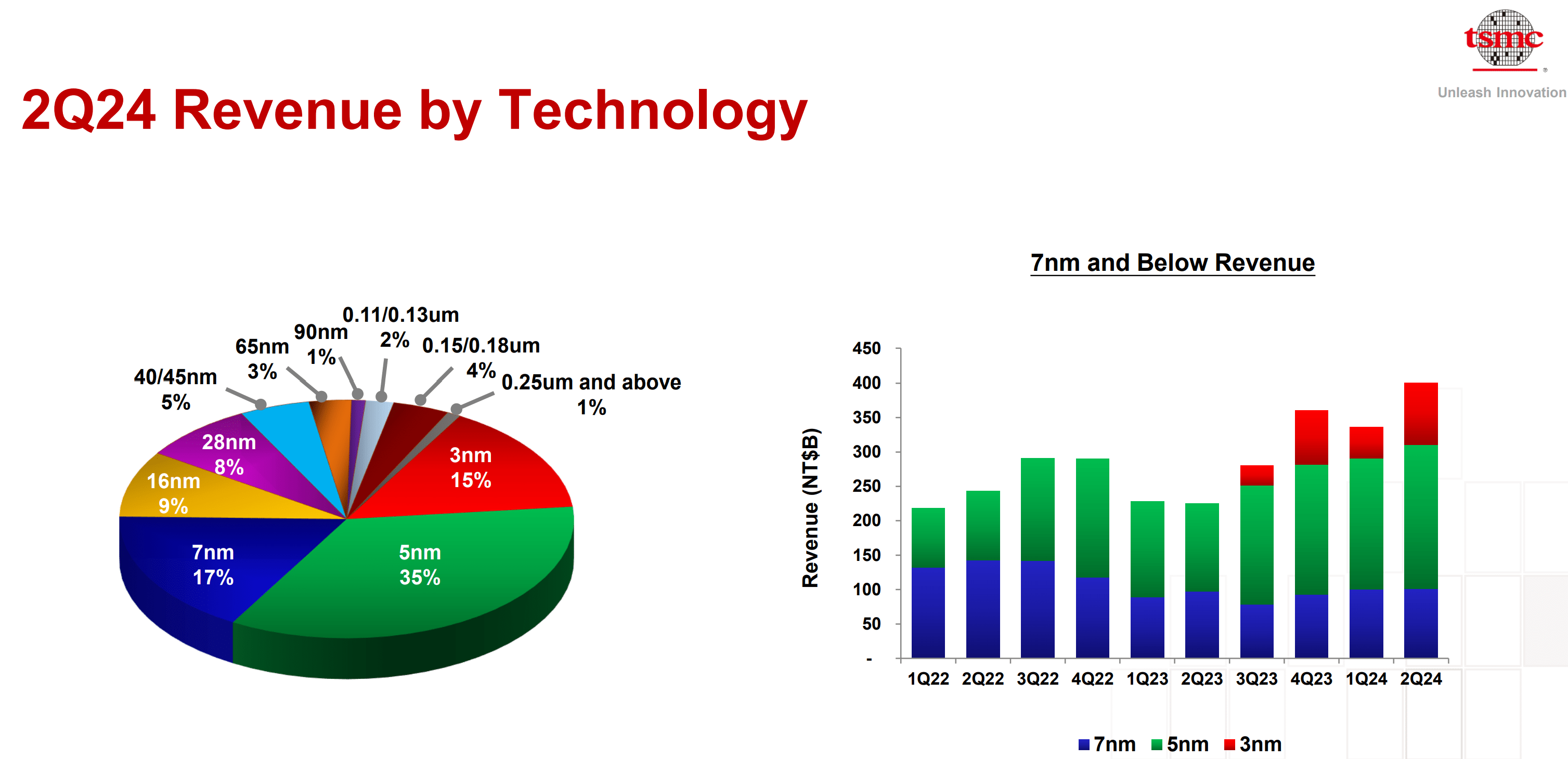

By expertise, TSMC’s N3 course of contributed 15% of wafer income, and that is probably the most superior in manufacturing at the moment.

In reality, revenues from TSMC’s N3 nearly doubled from the earlier 3-month interval.

The N3 prospects are literally not Nvidia.

These vital N3 prospects are Apple, Qualcomm and AMD.

TSMC income by expertise (TSMC)

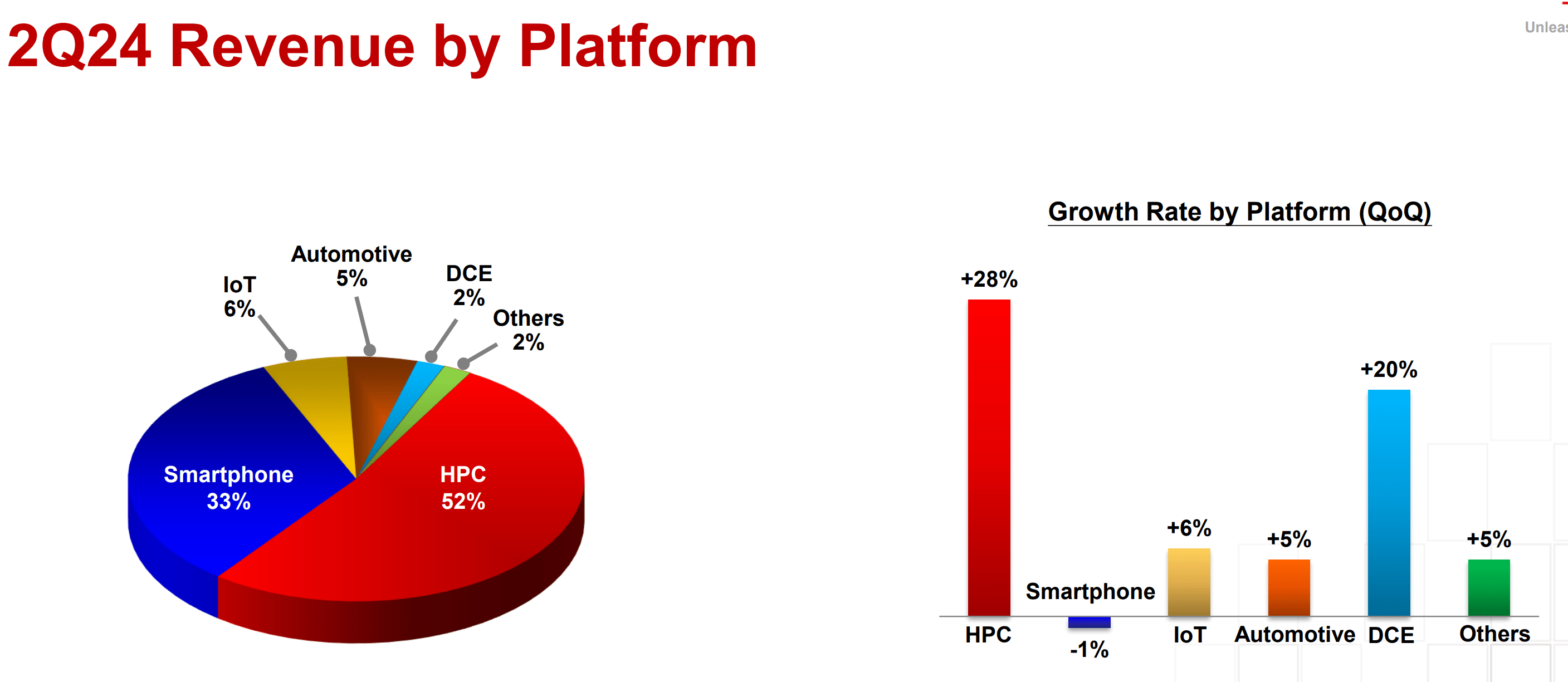

The excessive efficiency computing (“HPC”) phase is crucial phase for TSMC at the moment. That is basically the AI phase for TSMC.

It makes up 52% of TSMC’s internet revenues.

The HPC phase grew very robust, which was up 28% sequentially.

One other vital phase for TSMC is the smartphone phase.

Smartphones make up 33% of revenues, however within the 2Q24 quarter, was down 1% sequentially.

TSMC income by platform (TSMC)

From the margins and profitability aspect of issues, TSMC additionally managed to beat expectations.

TSMC’s 2Q24 gross margin got here in at 53.2%, beating consensus estimates of 52.6% and got here in above the long-term purpose of a constant 53%.

TSMC’s 2Q24 working margin got here in at 42.5%, beating consensus estimates of 41.6%.

TSMC’s 2Q24 internet revenue got here in at NT $247.8 billion, in comparison with consensus expectations of NT $235 billion, beating consensus by nearly 6%.

Capital expenditures for the primary half of 2024 got here in at $12.13 billion.

This means that it might want to ramp up capital expenditures within the second half of 2024 to satisfy its capital expenditure steerage.

Outlook

TSMC’s outlook for its enterprise was additionally robust.

TSMC expects 3Q24 revenues to be between $22.4 billion and $23.2 billion, rising +32% from the prior yr on the midpoint.

TSMC expects 3Q gross sales to be pushed by structural demand from AI and cyclical upturn demand from smartphones.

3Q24 gross margin is predicted to be between 53.5% to 55.5%, and 3Q24 working margin is predicted to be between 42.5% to 44.5%, which beat consensus expectations of 52.5% gross margin and 42.1% working margin respectively.

TSMC raised the 2024 steerage above mid 20% in USD phrases.

The capital expenditure steerage vary for 2024 was elevated.

The preliminary vary of between $28 billion and $30 billion was elevated to the brand new vary of between $30 and $32 billion.

70% to 80% of this capital expenditure can be used for superior applied sciences.

Smartphones

TSMC supplied strong commentary about smartphone demand.

TSMC CEO Wei mentioned: “We count on our enterprise to be supported by robust smartphone and AI-related demand for our modern course of applied sciences.”

He expects smartphone-related demand to be one of many development drivers for TSMC within the second half of the yr.

Inside smartphones, with AI requiring extra silicon content material, with 5% to 10% die measurement improve typically, AI will present structural development alternative for TSMC.

TSMC can be seeing extra smartphone shoppers are transferring to superior packaging like InFO packaging.

Pricing

TSMC has lengthy maintained that pricing is strategic, and by no means opportunistic.

TSMC acknowledged that pricing is an ongoing and steady course of.

The corporate is probably going in negotiations with key prospects to extend costs in some key merchandise.

TSMC CEO Wei mentioned that: “My prospects are doing very properly, and we must always do as properly”.

Aside from the truth that its prospects like Nvidia are doing properly, and that there’s very robust demand that the provision can not catch as much as, TSMC additionally talked about some price causes that will assist with its value hikes.

Particularly, TSMC talked about that their prices are rising resulting from worldwide enlargement and high-power costs in Taiwan.

Whereas there may be rising concern over geopolitical stress given the upcoming US presidential election, TSMC talked about that it might proceed its abroad enlargement to mitigate the dangers. This contains the brand new fabs ramp within the US and Japan the following yr and diversifying manufacturing areas. TSMC additionally reported authorities subsidies within the money circulate assertion and stability sheet. If there may be any tariff and commerce insurance policies, that can be paid by their prospects, based on TSMC.

That is undoubtedly excellent news for TSMC on condition that any tariffs imposed may result in prospects paying the additional and given that almost all of TSMC’s prospects are based mostly within the US, US firms find yourself paying the tariffs on behalf of TSMC.

I believe this quarter’s report exhibits that with a robust market place, TSMC is in a good place when it comes to pricing energy, which helps with the long-term gross margins.

With robust pricing energy, TSMC expects that its long-term gross margin is predicted to be 53% and better.

In reality, TSMC CEO Wei even emphasised on the “and better” and he acknowledged: When I’ve discussions with my prospects, I’ll give the “and better portion”.

Regardless of potential challenges from geological tensions or larger working prices resulting from inflation, rising electrical energy prices and abroad capability ramp-up, TSMC stays optimistic that it will possibly obtain gross margin of 53% and better.

This can be a results of TSMC’s superior efficiency and effectivity of its merchandise, which helps justify a premium pricing and this may even assist with its long-term profitability.

In brief, TSMC wants to make sure it maintains this superior efficiency and effectivity, if not this margin and profitability profile may deteriorate.

Rising its management and capability

As talked about within the prior part, TSMC wants to keep up a superior efficiency and effectivity degree to have the ability to preserve its profitability.

With that, TSMC is rising its management inside foundry, and including to the a lot wanted CoWoS capability that’s present in wanting provide.

TSMC acknowledged that for its N2 fabrication course of, which is for its 2nm expertise, the preliminary ramp up can be stronger than earlier nodes like 3nm.

When requested in regards to the progress about TSMC’s subsequent two fabrication nodes N2 and A16, CEO Wei mentioned that “nearly all of the AI innovators are working with TSMC.”

“He expects to have extra N2 prospects than for N3 and N5 and all the things goes forward of schedule with A16 growth.”

On account of higher efficiency of scale, this has a optimistic impression on margin dilution, which can be lower than what we noticed with N2.

One other factor TSMC has been targeted on is rising the provision for CoWoS superior packaging, which is crucial to AI accelerators like Nvidia.

TSMC states that demand could be very robust and that the corporate is working arduous to satisfy this robust demand.

The purpose right here is to proceed to extend provide, though TSMC expects provide to proceed to be “very, very tight” all the best way into 2025.

That mentioned, TSMC is aiming to achieve a stability someday in 2025 or 2026 for the CoWoS provide and demand scenario.

TSMC expects CoWoS capability to be greater than double from the prior yr in 2024.

In flip, administration expects rising AI demand to help its accelerated CoWoS enlargement into the following one to 2 years.

TSMC highlighted within the earnings name the position of AI in driving demand and sees AI as a long-term development development, not only for TSMC, however for the semiconductor business.

Valuation

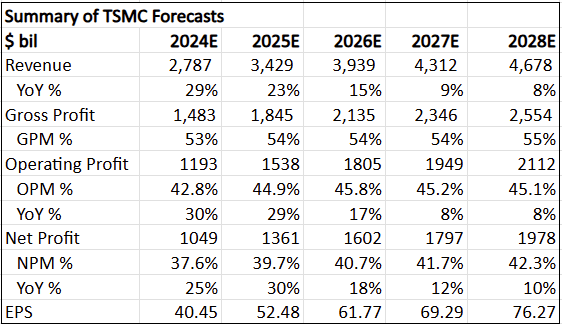

Under, I share my 5-year monetary forecasts for TSMC. The income CAGR over the following 5-year interval is 17% whereas EPS CAGR is barely larger at 19%.

I take advantage of the free money circulate to fairness derived from the monetary forecasts for the intrinsic worth calculation.

Abstract of 5-year monetary forecasts (Writer generated)

My intrinsic worth for TSMC is $184. That is based mostly on the belief of 21x terminal a number of and 12% price of fairness. TSMC’s 5-year common a number of is 23x, so I believe giving a 20x terminal a number of is cheap given the slower development profile within the outer years.

I might purchase TSMC at $147, or at a 20% low cost to its intrinsic worth.

My 1-year and 3-year value targets for TSMC are $228 and $302 respectively, which suggests 25x 2025 and 25x 2027 P/E respectively.

Conclusion

At a time when the theme is rotation out of expertise shares and when AI has been likened to a bubble, TSMC’s enterprise proceed to shine and exceed expectations.

Sturdy demand for top efficiency computing, or AI, drove the majority of the expansion we noticed in revenues for 2Q24, which is pushed by robust structural demand from AI.

Within the second half of 2024, aside from this structural AI demand, we may even see cyclical demand from smartphones because of an upcycle.

Whereas income development is nice, when mixed with rising margins, this cocktail of income development and increasing margins is a really robust inventory value mover.

Margins for TSMC are anticipated to be robust because of its dominant market place, superior efficiency and effectivity, which is driving pricing energy and the power to lift costs.

As well as, TSMC is just not stopping there. The corporate continues to increase its lead over rivals to make sure that its margin and profitability profile could be maintained.

[ad_2]

2024-07-31 12:02:54

Source :https://seekingalpha.com/article/4708414-tsmc-multiple-growth-drivers-ahead?source=feed_all_articles

{kind=link}

Discussion about this post