[ad_1]

pabst_ell

Word:

I’ve coated Transocean Ltd. or “Transocean” (NYSE:RIG) beforehand, so buyers ought to view this as an replace to my earlier articles on the corporate.

Three weeks in the past, main offshore driller Transocean reported weaker than anticipated Q2/2024 outcomes with revenues once more impacted by contract graduation delays and profitability hit by non-cash tax accounting necessities.

Nevertheless, adjusted for $156 million in GAAP earnings tax expense, the corporate would have reported a worthwhile quarter.

Firm Press Releases/Regulatory Filings

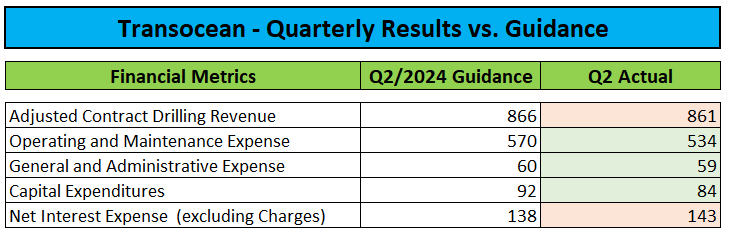

Adjusted EBITDA of $284 million got here in considerably forward of expectations offered by administration on the Q1/2024 convention name as slight income underperformance was greater than offset by decrease working and upkeep expense. On the convention name, administration attributed this to “the delay of in-service upkeep within the energetic fleet and the favorable decision of previous contingencies“.

Q1 Convention Name Transcript / Firm Press Launch

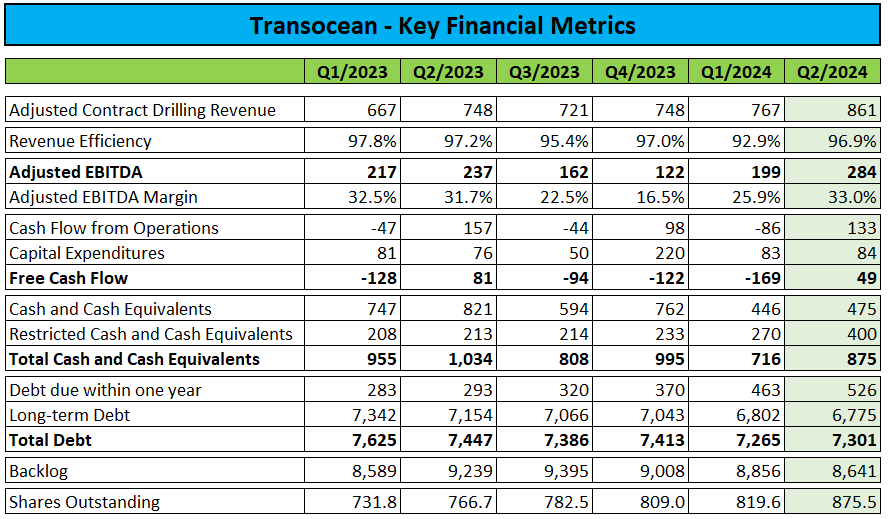

Adjusted EBITDA margin of 33% represented the best stage in current quarters and Transocean generated $133 million of money move from operations. Capital expenditures amounted to $84 million thus leading to free money move of $49 million.

The corporate completed the quarter with unrestricted money and money equivalents of $475 million, restricted money of $400 million and roughly $7.3 billion in debt. Transocean retains entry to its undrawn $576 million secured credit score facility for a complete liquidity of $1.05 billion.

Please notice that Transocean consists of restricted money in its liquidity calculations and projections:

Our projected liquidity at year-end 2024 is unchanged from final quarter at roughly $1.4 billion which incorporates the complete $576 million capability of our undrawn revolving credit score facility in addition to restricted money of roughly $390 million, most of which is reserved for debt service. This liquidity forecast consists of 2024 CapEx expectations of $250 million of which roughly $115 million is said to the Deepwater Aquila, about $15 million of CapEx related to the Aquila stays.

Backlog of $8.64 billion as of July 24 was down 2.4% on a sequential foundation, however on July 31, the corporate introduced a brand new $531 million contract for the high-specification drillship Deepwater Invictus within the U.S. Gulf of Mexico.

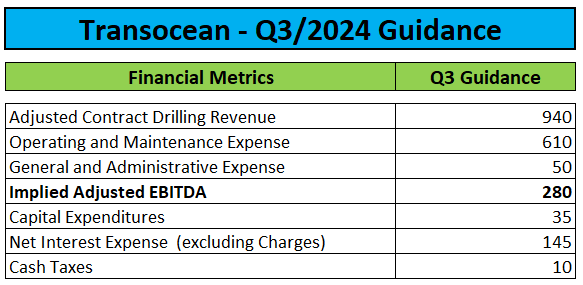

On the convention name, administration guided Q3/2024 largely according to expectations:

Q2/2024 Convention Name Transcript

With each revenues and working bills anticipated to be up considerably, Adjusted EBITDA is more likely to be roughly unchanged from Q2.

Nevertheless, with capital expenditures projected to be down roughly $50 million quarter-over-quarter, free money move ought to get a lift, albeit the timing of curiosity funds stays an essential issue.

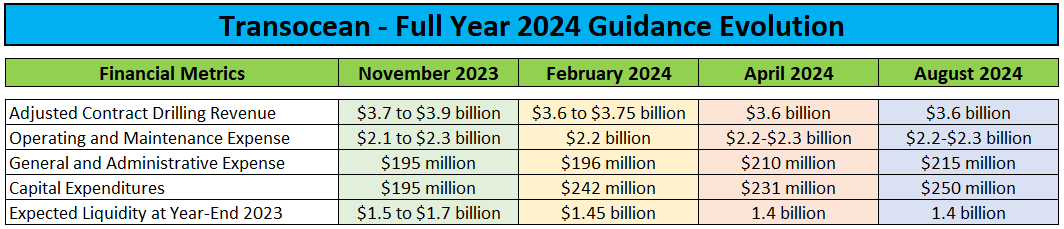

Following two consecutive downward revisions, the corporate reiterated its full-year outlook:

Convention Name Transcripts

On the convention name, administration was enthusiastic concerning the firm’s prospects:

In closing, we proceed to consider the underlying fundamentals help a multiyear development cycle for our belongings and providers.

Given our backlog and the visibility it offers to future money flows, together with a future discount in CapEx necessities as our newbuilds are actually all out of yards and on contract, we count on our unlevered free money move to proceed incrementally growing every quarter for the following a number of quarters, which might allow us to delever our stability sheet and in the end place us to design, talk and implement a sustainable technique to make distributions or in any other case return worth to our shareholders.

CEO Jeremy Thigpen even talked about the potential want for purchasers to finance the reactivation of Transocean’s cold-stacked rigs:

(…) our working fleet is greater than 90% dedicated by way of the top of 2025. And based mostly upon superior discussions with our clients and reflecting LOIs and robust verbal commitments, we consider that other than some small exercise gaps, which might come up in our buyer drilling packages, our fleet that’s presently working might quickly be utterly booked properly into 2026. As such, our clients could quickly want to contemplate financing the reactivation of cold-stacked belongings to fulfill their future program necessities.

Please notice that Transocean administration’s views are considerably in distinction to its primary opponents Noble Company plc (NE), Valaris Restricted (VAL), and Seadrill Restricted (SDRL) which all pointed to the present interval of subdued floater contracting exercise probably extending properly into 2025 with demand for lower-specification belongings being significantly weak.

That is additionally evidenced by Transocean’s most up-to-date fleet standing report which exhibits two sixth technology floaters (Deepwater Inspiration and Growth Driller III) sitting idle for greater than a 12 months already.

On the convention name, administration acknowledged that these rigs should not anticipated to be awarded new work within the close to future and in consequence, the corporate has began to cut back working bills for these belongings.

Whereas the outlook for high-specification belongings is healthier, there isn’t any want for purchasers to pay for the reactivation of Transocean’s cold-stacked belongings, significantly not given the truth that these drillships have been sitting idle for nearly a decade now.

Please notice that there aren’t any examples of rigs being reactivated after having been mothballed for such an extended time period which provides appreciable uncertainty concerning the corporate’s means to efficiently full reactivations in time and on finances. In distinction to competitor Valaris, Transocean has by no means reactivated a cold-stacked drillship up to now.

As well as, there are many high-specification belongings out there available in the market in the present day with various newbuild drillships presently marketed for employment by opponents.

Proper now, Noble Company has a sizzling (able to work) seventh technology drillship (Noble Voyager) sitting idle in Curacao whereas Seadrill must discover work for 3 high-specification drillships scheduled to roll off contract by mid-2025.

Consequently, I’d be stunned to see any near- and even medium-term reactivations of Transocean’s cold-stacked rigs.

Nevertheless, even with the presently energetic fleet, the corporate ought to see an honest leap in profitability subsequent 12 months with free money move more likely to exceed $700 million with further rigs transitioning to higher-margin contracts and not too long ago transitioned items contributing for a full 12 months.

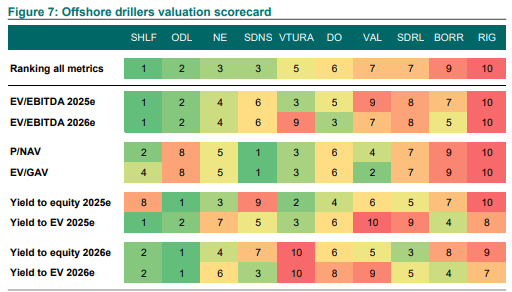

Sadly, Transocean’s share value already displays expectations for a lot increased profitability and money technology going ahead because the inventory continues to commerce at a big premium to friends based mostly on mainly all key monetary metrics tracked by analysts:

DNB Markets

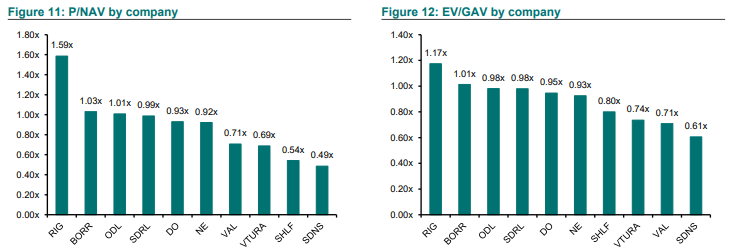

From a web asset worth perspective, the corporate is valued at a greater than 100% premium to competitor Valaris:

DNB Markets

As well as, Transocean’s current choice to purchase the remaining 67% stake within the harsh surroundings floater Transocean Norge in change for 55.5 million newly issued shares and $130 million in 8% senior notes has resulted in additional dilution for frequent fairness holders and better total debt ranges.

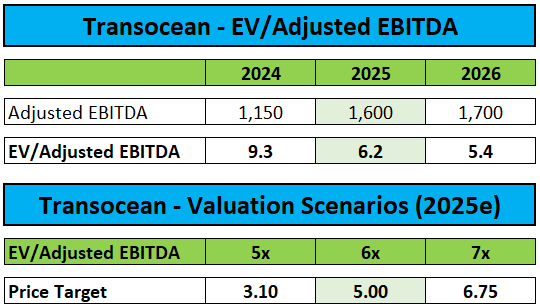

Whereas full possession of Transocean Norge will positively impression money move and Adjusted EBITDA, the elevated contribution is totally offset by decrease expectations for the Deepwater Inspiration and Growth Driller III which I now assume to stay idle till at the least H2/2025. In consequence, my ahead Adjusted EBITDA estimates stay unchanged:

Writer’s Estimates

With a further 55.5 million shares now included within the mannequin, I’m reducing my value goal from $5.50 to $5.00 whereas reiterating my “Maintain” score on the shares.

Buyers searching for publicity to the trade ought to slightly think about friends like Noble Company, Valaris, and Seadrill that are all buying and selling at considerably decrease ahead valuations regardless of vastly superior stability sheets and robust commitments to shareholder capital returns.

Writer’s Estimates

Backside Line

Adjusted for a big non-cash tax cost, Transocean reported worthwhile second quarter outcomes and reiterated full-year expectations.

Whereas profitability and money technology ought to enhance very considerably going into 2025, these expectations seem very a lot mirrored within the firm’s premium valuation relative to friends.

With the inventory value near my revised $5.00 goal, I’m reiterating my “Maintain” score on the shares.

[ad_2]

2024-08-19 19:34:45

Source :https://seekingalpha.com/article/4715695-transocean-positive-outlook-well-reflected-in-premium-valuation-hold?source=feed_all_articles

{kind=link}

Discussion about this post