[ad_1]

Trevor Williams

Overview

There are such a lot of completely different healthcare investments within the sector that I desire to get my publicity from a fund that may present on the spot diversification and supply a gentle distribution alongside the best way. abrdn World Healthcare Fund (NYSE:THW) has been certainly one of my choices to reaching this and I’ve beforehand lined what I’ve appreciated about it prior to now. Nevertheless, I’m beginning to see some indicators of weak spot, notably with the distribution protection. What makes THW such a horny selection is that the fund is diversified and gives a better than common dividend yield of about 10.7% and distributions are paid out to shareholders on a month-to-month foundation.

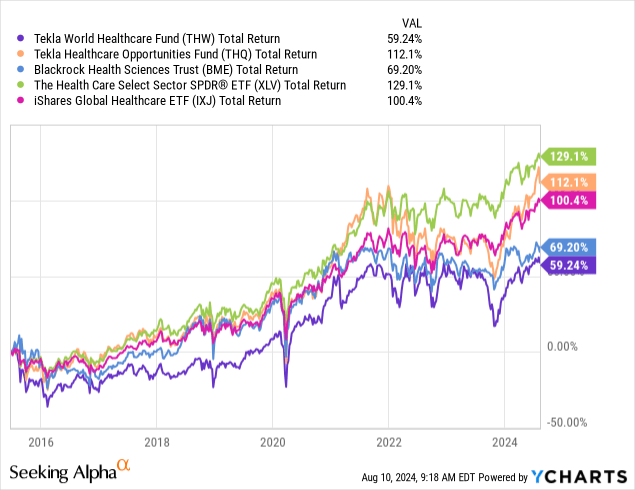

When trying on the efficiency of THW, we are able to see that it has underperformed most friends within the healthcare sector. This has led me to query whether or not or not the earnings side of THW is well worth the tradeoff of underperformance. Whereas I’d sometimes be okay with a few of a tradeoff, I consider that there’s a lot of future progress to be captured from the healthcare sector over the subsequent decade and I’m beginning to shift my goal in direction of acquiring the very best complete return potential.

Only for some temporary context, THW operates as a closed finish fund that gives world publicity to the healthcare sector all through various sub sectors corresponding to prescription drugs, biotech, and even healthcare associated actual property funding trusts. The fund has a public inception relationship again to 2015 and sports activities a administration payment of 1.25%. THW maintains each equities publicity in addition to mounted earnings investments to assist enhance the general yield that may be generated.

Distribution Threat

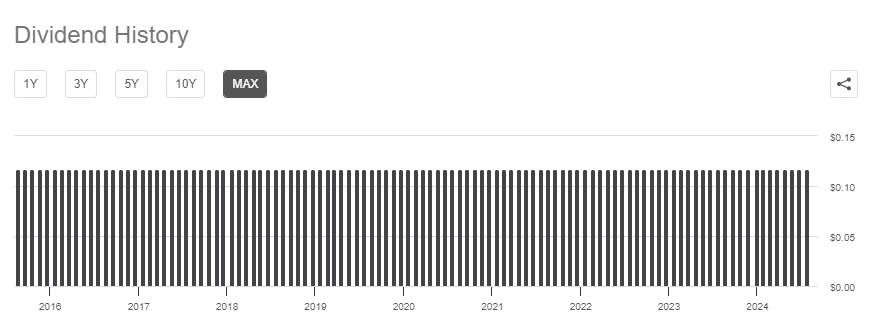

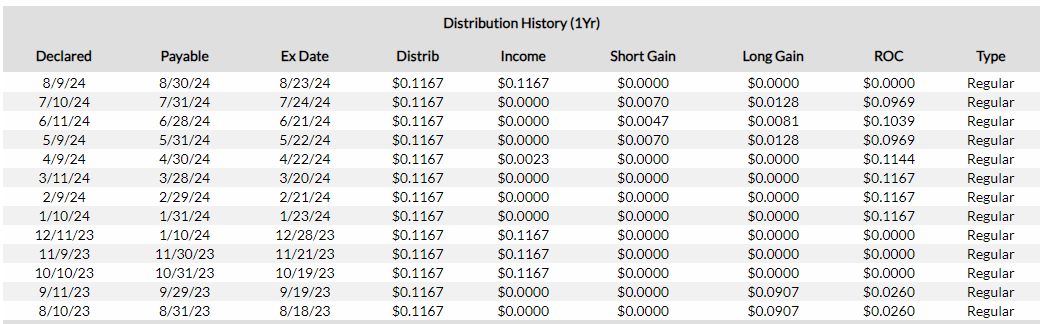

As of probably the most not too long ago declared month-to-month distribution of $0.1167 per share, the present dividend yield sits at 10.7%. For the reason that distributions are issued on a month-to-month foundation, THW might be a horny selection for buyers that will rely upon the earnings generated from their portfolio to fund their way of life bills. One thing that THW has on its aspect is that the distribution has by no means been minimize for the reason that fund’s inception. Due to this fact, the fund has traditionally provided buyers a spot to seize a dependable source of earnings whereas sustaining a various publicity to the healthcare sector.

Looking for Alpha

This sense of stability has additionally enabled long run buyers to repeatedly progress their earnings yr over yr. Regardless of the shortage of raises, the soundness may have been taken benefit of by reinvesting these distributions again into THW. By doing this, you’d successfully be compounding your distributions and making a snowball impact of rising earnings. This course of may additional be amplified by reinvesting new capital in order that the distributions develop at a faster charge.

Nevertheless, the issue I’ve with the distribution is that it has traditionally been funded by largely return of capital. Return of capital in itself is not all the time a unfavorable factor however the extreme use of it may be dangerous to the fund’s NAV and future progress. It may well additionally point out a concern with the underlying technique and the way it ma be failing to generated adequate returns to totally cowl the distribution. Return of capital distribution get taken immediately out of the fund’s web belongings and in consequence, stunts the skilled value progress.

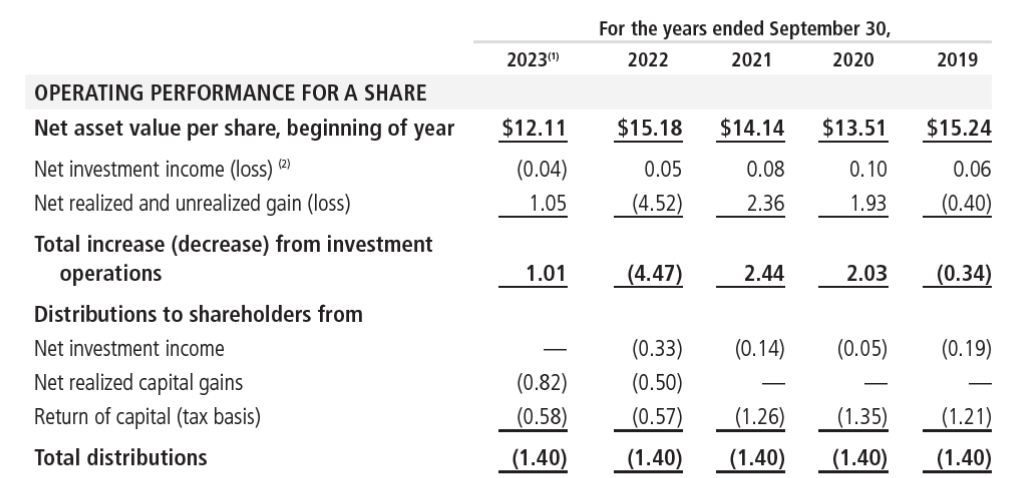

The newest annual report reveals that the fund’s NAV sat at $15.18 per share by the yr finish of 2021. Nevertheless, this steadily decreased all the way down to $11.73 per share by the top of 2023. Having a look on the distribution historical past over the past yr, I assume that that the continued use of return of capital is a contributing issue the the NAV decline. We are able to see that a lot of the distributions over the past yr consisted of primarily ROC, quite than utilizing the web funding earnings generated from the underlying belongings or web realized positive factors.

CEF Knowledge

The annual stories over the past 5 years present that web funding earnings has by no means surpassed $0.10 per share. Internet funding earnings can embrace the dividends, curiosity, and earnings acquired from possibility writing. Since these totals have by no means confirmed any impactful progress, it may well point out an underlying concern with the fund’s technique. The massive majority of THW’s progress comes from web realized positive factors from shopping for and promoting of the underlying securities inside.

THW 2023 Annual Report

I consider that if the distribution was decreased a bit, it could permit the fund to seize extra upside progress by retaining a bigger portion of earnings. I do know {that a} distribution minimize would not be best due to the already established sense of reliability, however continued efficiency down this path will result in additional NAV deterioration.

Underlying Portfolio Technique

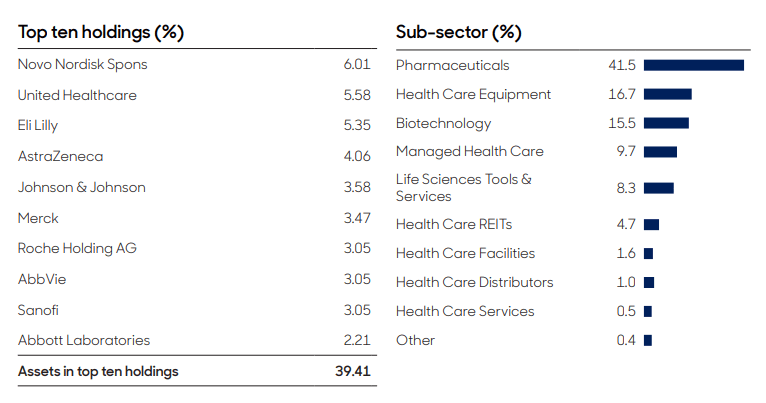

What differentiates THW from its sister fund, abrdn Healthcare Alternatives Fund (THQ), is that THW has an emphasis on sustaining world publicity. In keeping with the fund’s newest truth sheet, publicity to the USA solely accounts for 45.9% of the investments inside. The breakdown consists of US-based firms which have substantial quantities of income coming from worldwide sources, making up 20.9%. That is adopted by various weights of publicity to completely different international locations corresponding to the UK, Denmark, Switzerland, France, Netherlands, and Eire.

One other factor that makes THW completely different is that it maintains publicity to different asset courses apart from simply equities. As an example, THW has some publicity to mounted earnings, REITs, and Enterprise Capital investments. These different asset courses appear to be earnings centric and may very well be a contributing issue on why the value efficiency has been underwhelming all through THW’s historical past. We are able to additionally see that THW has publicity to rate of interest delicate sub sectors corresponding to well being care REITs.

Prescribed drugs make up the biggest space of funding, accounting for 41.5% of the overall portfolio make-up. That is adopted by publicity to sectors corresponding to well being care gear and biotech, accounting for 16.7% and 15.5% respectively. Due to this fact, most areas of the healthcare sector are lined with an funding in THW. By way of prime positions, Novo Nordisk (NVO) is the biggest place sitting at 6.01%. That is adopted by a 5.58% publicity to United Healthcare (UNH) and a 5.35% publicity to Eli Lilly (LLY). The highest holdings have shifted a bit from the final time I lined THW. At the moment, Eli Lilly was the biggest place, adopted by United Healthcare. The breakdown of the sub sectors have additionally shifted a bit as pharma solely accounted for 39% of their portfolio and biotech was the second largest sector.

THW Reality Sheet

THW additionally has the inclusion of an possibility writing technique to assist generated larger ranges of earnings inside the fund. Nevertheless, I beforehand shared the web funding earnings outcomes and it does not appear to be the choice technique right here has actually helped amplify the returns over the previous few years. As well as, possibility methods can often be carried out as a method for funds to make the most of cycles of upper market volatility by gathering larger premiums on the choices. THW fails to do that with web funding earnings by no means displaying any significant progress, even throughout excessive volatility instances like we have skilled for the reason that pandemic in 2020.

THW can write name choices towards the underlying equities inside however the typical portion measurement of those choices are solely 20% of the fund’s web belongings. The added draw back right here is that the choice technique successfully caps the upside value appreciation that may be skilled right here. It’s because positive factors from value will increase are capped at regardless of the strike value is on the underlying asset. I am prepared to wager that if the choice technique was utterly eradicated from THW, the distribution must be decreased by the general NAV and value progress skilled right here could be much more enticing. Due to this fact, whereas the inclusion of choices have a optimistic intent, the precise execution has confirmed to be flawed over time.

Valuation

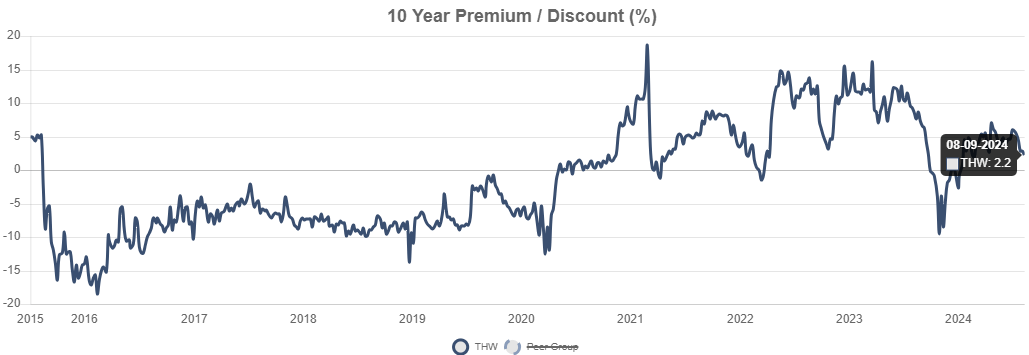

Since THW operates as a closed finish fund, the value can range from the precise worth of the underlying belongings. In consequence, we are able to see when the value has traditionally traded at a premium of low cost to NAV. Trying on the chart under, we are able to see that previous to 2020, the fund has incessantly traded within the low cost to NAVV territory. THW at present trades at a slight premium to NAV of two.2%. For reference, the value traded at a median premium to NAV of 6.8% over the past three years however I don’t see any causes to justify this premium.

CEF Knowledge

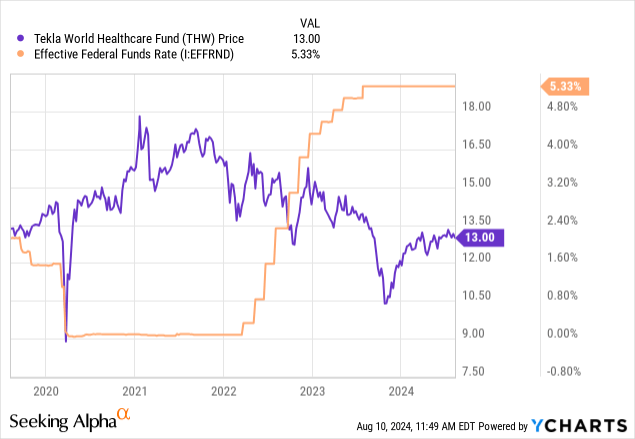

When taking a look at THW from a value perspective, it has did not seize an identical progress skilled from the healthcare sector. This is not too shocking nonetheless for the reason that principal focus of THW is on earnings technology. Due to this fact, THW will likely be at a horny worth as soon as the premium comes down and the value trades within the low cost territory. Ahead trying, I consider that future rate of interest cuts could also be a optimistic value catalyst. Trying on the latest historical past, we are able to see that THW has shared a novel relationship with the federal funds charge.

When rates of interest have been minimize to close zero ranges following the pandemic, the value of THW quickly appreciated. Conversely, when rates of interest have been aggressively hiked all through 2022 and 2023, the value regularly retracted to the draw back. Greater charges put extra monetary stress on firms that held numerous floating charge debt on their stability sheet. Greater charges have the facility to shrink profitability metrics as extra earnings should be dished out in direction of curiosity funds and debt discount, quite than being reinvested again into firms.

The unemployment charge has steadily climbed over the past 12 months and now sits on the 4.3% whereas the inflation charge concurrently developments downward over the past couple of months. Moreover, US Presidential elections are upcoming and will trigger larger ranges of volatility and uncertainty within the markets. The mixture of those elements might incentivize the Fed to start slicing rates of interest as early as September. I consider that decrease rates of interest could be a optimistic catalyst for progress going ahead as a result of decrease charges would allow healthcare firms to allocate extra capital in direction of varied progress initiatives.

Since rates of interest would immediately translate to cheaper entry to debt capital, healthcare firms may use this capital to fund the analysis and growth of latest medication or merchandise, fund acquisitions, or develop operations with new development initiatives or developments. Due to this fact, I plan to stay very observant at how the fund’s efficiency will enhance one rates of interest begin to get minimize. I at present maintain a place in THW however will not be reinvesting the distribution or including new capital for now.

Takeaway

In conclusion, THW’s excessive yield might be enticing for earnings buyers for the reason that distribution is paid out on a month-to-month foundation and the dividend has by no means been minimize. Nevertheless, the historic efficiency of the fund is a bit underwhelming and has prompted some concern for the sustainability of the distribution. Over the past twelve months, the vast majority of the distribution has been funded from return of capital. Whereas I’ve no points with this type of distribution, I do consider that extra use and reliance on it’s finally dangerous for NAV and can proceed to contribute to the value decline.

The choice technique hasn’t confirmed to be very helpful in producing larger ranges of earnings. Due to this fact, the choices has solely restricted the upside progress potential skilled. THW trades at a slight premium to NAV however latest efficiency does not justify this premium. As well as, THW has underperformed peer healthcare targeted funds in complete return over the past decade. Whereas the the does have a pleasant degree of variety and the month-to-month distribution is enticing, I’m downgrading my score to a maintain. I plan to take care of my place however won’t proceed reinvesting these distributions or add any further capital for now. I plan to look at how the fund’s efficiency modifications or improves when rates of interest are minimize.

[ad_2]

2024-08-11 20:38:54

Source :https://seekingalpha.com/article/4713579-thw-deteriorating-distribution-coverage-downgrade?source=feed_all_articles

{kind=link}

Discussion about this post