[ad_1]

J Studios

There are some wonderful alternatives amongst excessive yield preferreds with the potential to seize secure double-digit yields. We’re additionally seeing capital beneficial properties potential with some buying and selling at steep reductions to par worth regardless of a excessive likelihood of redemption at par within the subsequent few years. In response to this chance, we now have been posting our analysis comparable to our current piece on Chimera Funding Company preferreds (CIM).

There are, nevertheless, fairly just a few traps within the space as nicely so I wish to shed equal gentle on the dangers. One should tread rigorously and totally analysis every firm to distinguish the nice from the dangerous. This text will talk about the ideas behind the methods through which excessive yield preferreds will be harmful in addition to level out some particular points which can be harmful immediately.

Mechanics of getting paid by preferreds and what can go incorrect

There are 3 ways through which an investor in a most popular will get paid:

- Dividends.

- Liquidation desire.

- Redemption.

Like some other fastened revenue instrument, preferreds pay a contractually obligated sum designated by the coupon. Additionally just like bonds, preferreds are entitled to their liquidation desire (face worth) within the occasion the corporate is offered or liquidated.

There are two points that make preferreds as an asset class barely riskier than bonds:

- Preferreds sit beneath debt however above the widespread within the capital stack so within the occasion of liquidation, debt will get paid earlier than the preferreds.

- Failure to pay a most popular dividend doesn’t set off an occasion of default as failure to pay curiosity would with a bond. This makes it a decrease precedence for the corporate.

As a tradeoff for these weaknesses, preferreds normally provide increased yields than bonds. The unfold between the yield of a most popular and that of a bond must be proportional to how a lot incremental danger most popular holders are taking over. In idea, the popular of a well-managed firm with a robust stability sheet ought to commerce at a really small unfold to bonds whereas the popular of an organization with weak cashflows, too excessive of leverage, or different substantial danger ought to commerce at a big unfold.

The market normally understands that there must be a ramification between preferreds and debt, however it’s usually incorrect to ascribe the magnitude of that unfold. Herein lies each the hazard and the chance.

By analyzing the basics of the underlying firm, its capital stack, and its administration, we will get a way of what yield a most popular ought to commerce at relative to the place it’s really buying and selling. Amongst different issues, key items of knowledge for a most popular are:

- Fairness cushion.

- Enterprise volatility.

- Premium to par.

- Unhealthy actor danger.

Under we are going to discover particular preferreds that we consider are harmful.

Not sufficient cushion

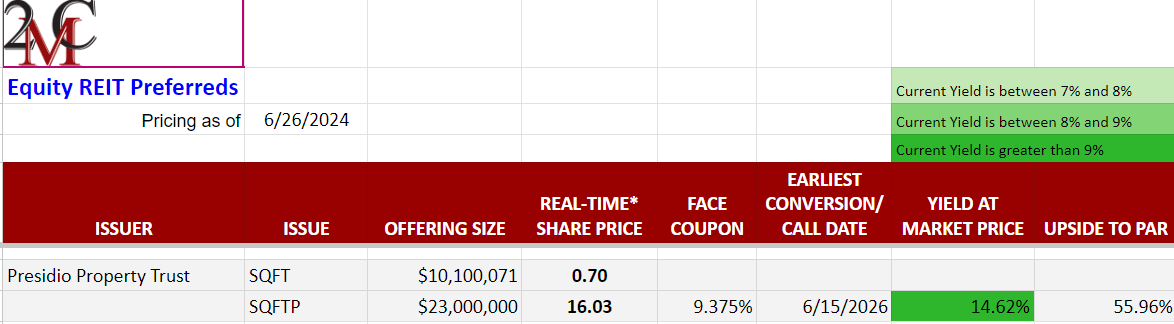

Presidio Property Belief, Inc. (SQFT) has a most popular, SQFTP that appears fairly engaging at first look with a present yield of 14.62% and a whopping 56% upside to par.

Portfolio Revenue Options

This most popular may be a entice, nevertheless, because it has little or no fairness beneath. The market cap of the widespread is simply $10 million towards $23 million of most popular and $98.5 million mortgage debt as of three/31/24.

Given these ratios, it might solely take just a few share factors of decline in asset worth to wipe out the widespread solely after which the popular begins to really feel the burden of declines.

It’s potential that there’s some form of turnaround play right here, however that will require a differentiated thesis with particular explanation why one believes SQFT will enhance. Shopping for SQFTP for its revenue looks as if a extremely dangerous endeavor to me.

It’s simple to see {that a} microcap like SQFT is just too small to offer a cushion of security for the popular, however it might probably occur in bigger corporations as nicely. The bottom line is the ratio between widespread, most popular, and debt.

This ratio also needs to be thought-about within the context of the enterprise. Maybe a excessive ratio of most popular to widespread is okay if the underlying enterprise is kind of secure, however we might desire a a lot greater fairness cushion for unstable companies.

Enterprise volatility danger

The volatility of a enterprise shouldn’t be essentially dangerous for widespread fairness traders as they profit from upswings simply as a lot as they may very well be damage by downswings.

As fastened revenue investments, preferreds are capped of their upside on account of being redeemable at par worth both presently or within the not-too-distant future. Volatility retains the danger aspect with out the upside making it a transparent total destructive. Thus, preferreds of corporations in inherently unstable sectors ought to commerce at increased yields.

Motels are one such unstable sector. They’ll make nice sums of cash throughout event-driven surges or durations of financial power inducing extra journey, however in addition they have stretches of working losses.

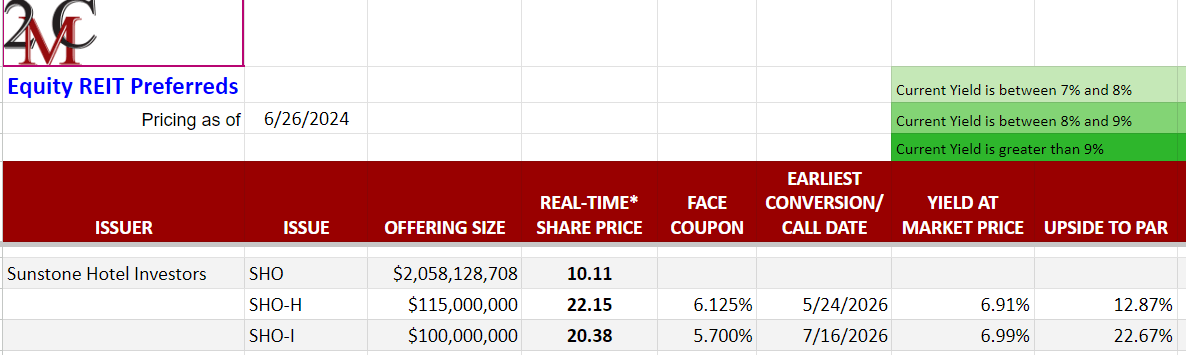

I feel the market usually misunderstands the idea that preferreds do not take part in excessive upside and as such tends to overvalue preferreds of robust but extremely cyclical corporations. Sunstone Resort Buyers, Inc. (SHO) is a well-managed and comparatively profitable lodge REIT however the preferreds will not be enticing at present pricing.

Portfolio Revenue Options

A 6.9% yield can be applicable for a non-cyclical firm of comparable measurement and earnings energy. At that yield, it merely is not correctly compensating traders for the additional cyclical danger they’re taking over.

Recall that throughout the pandemic resorts had a protracted interval of losses with many billions of {dollars} misplaced. Related, though much less extreme losses occurred after the 9/11 terrorist assaults, the Nice Monetary Disaster, and even the dot-com bust to a lesser extent.

Horrible occasions occur to lodge profitability seemingly a number of instances every decade. If you will tackle that danger, not less than get compensated for it.

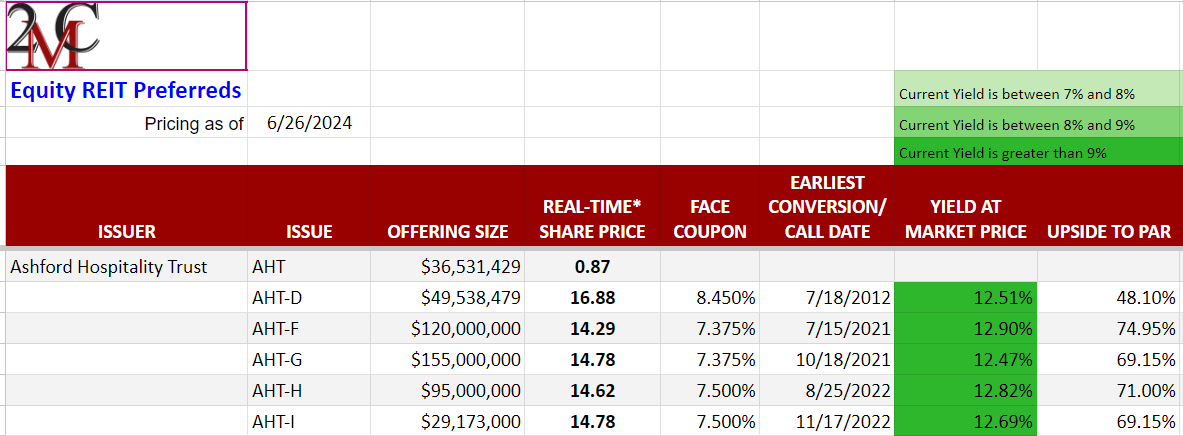

Ashford Hospitality Belief, Inc. (AHT) preferreds seem to compensate for further danger with yields within the 12% vary, however along with the cyclical danger of the trade, they’ve too small of an fairness cushion as nicely.

Portfolio Revenue Options

With the $36 million market cap widespread dwarfed in measurement by the excellent most popular points, the corporate is only a sneeze away from the liquidation desire of the preferreds turning into impaired.

All the time be cautious when reaching for yield, however notably in excessive leverage conditions in unstable sectors.

Unhealthy actor danger

One of the vital troublesome dangers to keep away from is that related to dangerous actors. It will not be discernible in monetary statements or evaluation of the underlying enterprise.

Administration groups are people and generally people make dangerous selections that may hurt traders. It’s troublesome to warn about future dangerous actor danger as a result of I do not know which firm will attempt to pull a quick one, however we will look at historic circumstances to see what kind of issues can occur.

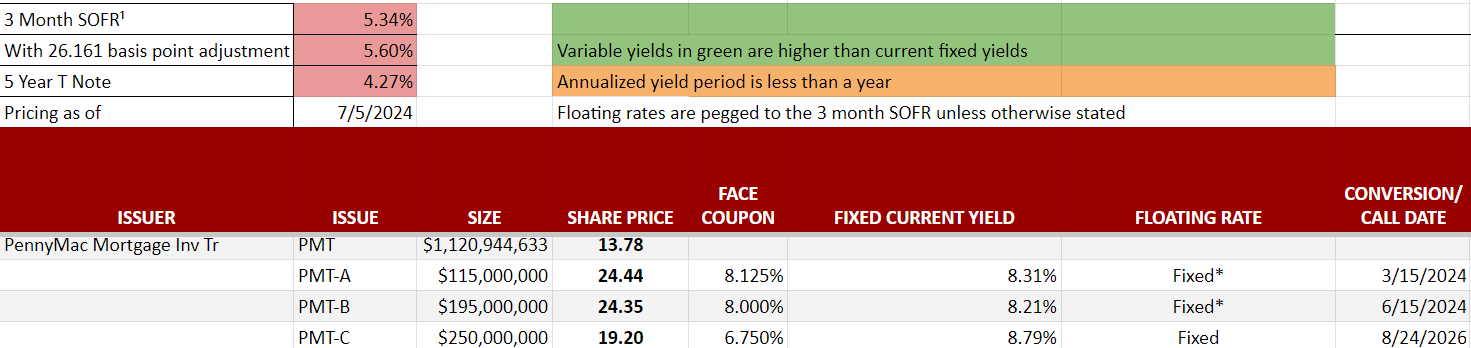

PennyMac Mortgage Funding Belief (PMT) has fastened to floating preferreds that had been alleged to convert to floating on the dates listed beneath.

Portfolio Revenue Options

On the time of conversion to floating fee, PMT introduced that they weren’t going to honor the floating fee and as an alternative maintain it on the authentic fastened fee.

The costs of those preferreds dropped materially. They’ve since recovered as many consider there can be authorized or different actions that would power the corporate to pay the correct floating fee.

If floating as initially supposed, the yields can be considerably increased.

One other manner administration can hurt the worth of a most popular is to take away property from beneath them.

Cedar Most well-liked C and B had been pretty well-protected preferreds essentially, as Cedar had a pleasant portfolio of procuring facilities with a worth that was clearly a lot bigger than the debt plus preferreds.

In structuring the sale of Cedar to Wheeler Actual Property Funding Belief, Inc. (WHLR), nevertheless, the preferreds had been transferred to WHLR in such a manner that they’re now tied to a a lot smaller pool of property. As such, they grew to become essentially riskier and have traded down materially to mirror the upper danger. We wrote extra in-depth about what occurred right here.

There isn’t a strategy to totally defend one’s portfolio towards dangerous actors. It might occur to widespread, preferreds, and even debt. I discover the perfect mitigation methods to be understanding the administration groups of corporations and diversification.

Hazard in preferreds of secure and extremely worthwhile corporations

Even when a most popular is related to an amazing firm that has low debt, excessive cashflows, and a secure enterprise, the market worth will be its personal hazard.

It’s troublesome to discover a firm that’s extra able to supporting its preferreds than Prologis, Inc. (PLD). With $103B of widespread fairness cushion and a robust rising enterprise, Prologis, Inc. 8.54% PFD SR Q (OTCQB:PLDGP) is at minimal danger of going unpaid. Given the underlying power, it ought to commerce at a really small unfold over debt.

Its present yield is 7.56% which, on a nominal foundation, is definitely excessive sufficient.

Portfolio Revenue Options

pricing as of 6/26/24.

Nevertheless, the market appears to be targeted solely on the present yield and has forgotten about redemption danger.

Prologis has entry to cheaper capital than its 8.54% coupon most popular so it’ll virtually actually redeem the popular as quickly as potential which is 11/13/26. With a par worth of $50, traders are prone to get redeemed at $50 in 2.38 years which might incur a capital lack of $6.50 from immediately’s worth.

This capital loss would eat up a big quantity of the dividend acquired over that time-frame taking complete return till redemption to about 6.5%. Over the course of two.38 years that’s an annual yield of about 2.7%

PLD is a superb firm, however there isn’t a manner its most popular ought to commerce at a yield to maturity nicely beneath that of treasuries.

Placing it collectively

REIT preferreds have traditionally had pretty low default charges and have usually been a strong supply of secure excessive yield. In immediately’s setting, excessive rates of interest are inflicting many of those points to commerce at notably excessive yields and good reductions to par making it broadly opportunistic.

As at all times, we advocate for sensible single-issue choice, even when an space is broadly robust. There are each wonderful alternatives and a few traps. Hopefully, this text helps shed some gentle on differentiate between the 2.

Editor’s Notice: This text discusses a number of securities that don’t commerce on a serious U.S. alternate. Please pay attention to the dangers related to these shares.

[ad_2]

{kind=link}

Discussion about this post