[ad_1]

wellesenterprises

Article Thesis

Tesla, Inc. (NASDAQ:TSLA) reported its second-quarter earnings outcomes on Tuesday afternoon. The corporate missed estimates on the underside line, which resulted in a share value decline. I consider that these outcomes don’t assist the present share value and really elevated valuation.

Previous Protection

I final coated Tesla round three months in the past, when the corporate introduced its first-quarter earnings outcomes. Since then, shares have risen quickly, though that was largely the results of future robotaxi bulletins, whereas the underlying enterprise efficiency was not very thrilling. Actually, not too way back, Tesla needed to announce that its deliveries throughout the second quarter had been down in comparison with final 12 months’s second quarter — though Tesla nonetheless marginally beat analyst estimates with its Q2 supply quantity. In as we speak’s article, I will give attention to Tesla’s Q2 outcomes and what they inform us in regards to the firm.

What Occurred?

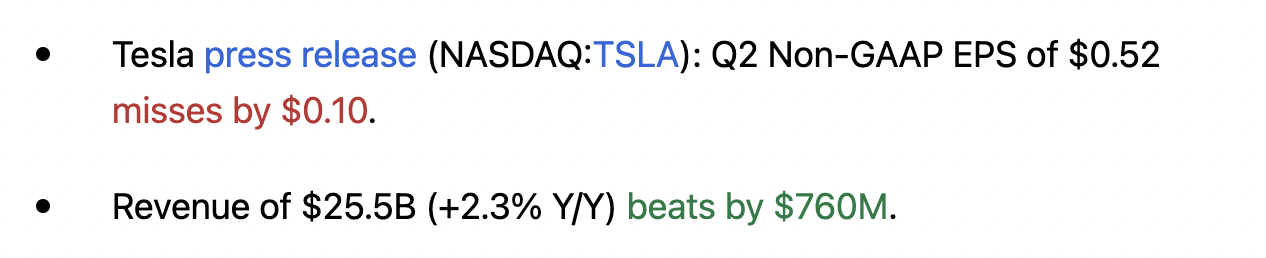

The world’s main car firm by market capitalization introduced its most up-to-date quarterly earnings outcomes, for its fiscal second quarter, on Tuesday afternoon, following the market’s shut. The headline numbers may be seen within the following screencap:

Tesla outcomes (Searching for Alpha)

Tesla was in a position to generate revenues that had been considerably larger than anticipated. The latest development implied that revenues can be down on a year-over-year foundation, as this had been the case throughout the first quarter of the present 12 months, when Tesla reported a 9% income decline. Analysts had been anticipating a small income decline for the second quarter as properly. Outcomes throughout the second quarter had been higher than anticipated, nonetheless, with Tesla managing to ship a small income improve in nominal phrases.

These outcomes had been nonetheless removed from nice, I consider, contemplating the truth that EV firms are oftentimes thought-about development investments. Moreover, Tesla’s valuation of round 100x ahead web earnings implies that the corporate will develop at a large tempo sooner or later. Nonetheless, a minimum of proper now, that’s clearly not occurring, as income development was barely under the latest inflation price of three% in June, the final month of the second quarter. Relying on whether or not one appears at nominal or actual revenues, there’s thus gradual to no development.

The truth that the corporate’s income efficiency was higher in Q2 in comparison with Q1 may be partially defined by the truth that there was no disruption within the Berlin Gigafactory throughout the second quarter, in contrast to throughout the first quarter.

Relating to earnings, Tesla hit earnings per share of $0.42 on a GAAP foundation. That’s down from $0.78 throughout the second quarter of 2023. Thus, profitability clearly stays underneath strain. The market reacted negatively to those outcomes, sending Tesla’s shares decrease by a bit greater than 3% on the time of writing. Let’s delve into the outcomes.

Tesla: Progress Has Stalled

For years, the marketplace for electrical autos grew properly, and Tesla and plenty of of its friends noticed substantial development in deliveries. This former development has floor to a halt at Tesla, with car volumes being down barely throughout the newest quarter. Actually, the mixture of weak costs for Tesla’s autos and sluggish gross sales numbers made Tesla’s automotive income decline by 7% year-over-year. In different phrases, Tesla’s foremost enterprise, which contributes round 80% of the corporate’s complete income, is declining, a minimum of for now. To some extent, this is because of market weaknesses — in some European nations, for instance, decrease subsidies have resulted in decrease EV gross sales. However not each EV firm is experiencing the declines that Tesla is experiencing; thus there are company-specific elements at play as properly. BYD Firm (OTCPK:BYDDY, OTCPK:BYDDF), Tesla’s greatest competitor, is seeing ongoing gross sales development, for instance, whereas NIO (NIO) had a powerful second quarter as properly. Even legacy car firms comparable to BMW (OTCPK:BMWYY) are profitable within the present atmosphere — BMW noticed its EV gross sales rise by 34% throughout the first half of the present 12 months.

So whereas development at Tesla has stalled (or is unfavorable), some opponents are nonetheless seeing their gross sales numbers develop. A weaker market development price alone does thus not clarify Tesla’s points. As an alternative, it appears like shoppers are more and more discovering Tesla’s choices much less interesting in comparison with what its friends are providing. This could possibly be as a consequence of a considerably stale and somewhat restricted mannequin line-up, whereas the corporate’s CEO Elon Musk has additionally been a considerably controversial determine within the eyes of some shoppers. In the end, it seems Tesla can not seize the minds of the EV client the way in which it did previously, which is why it’s struggling to generate gross sales development whereas opponents comparable to BYD or BMW are gaining market share.

Tesla additionally has its non-auto companies, such because the vitality enterprise. Right here, revenues have been lumpy, which is why there are vital quarter-to-quarter swings. Q2 was a powerful quarter for the vitality enterprise, with a relative development price of 100%, albeit from a a lot decrease degree in comparison with the auto enterprise. Nonetheless, that was a powerful consequence and helped Tesla to beat the analyst consensus income estimate. If Tesla can preserve the momentum intact within the vitality enterprise, that may be nice. Nonetheless, historical past means that revenues will stay lumpy and that there’s a good probability that income development will likely be weaker sooner or later. Between Q2 of 2023 and Q1 of 2024, for instance, general income development for the vitality enterprise was simply a few proportion factors, so I consider that it’s unlikely that we’ll be seeing constant 100% development charges going ahead.

The companies enterprise carried out properly as properly, with a development price of round 20%. Sadly, that is the smallest enterprise unit by far, which is why company-wide income development remained fairly weak regardless of the interesting efficiency of each the vitality enterprise and the companies enterprise.

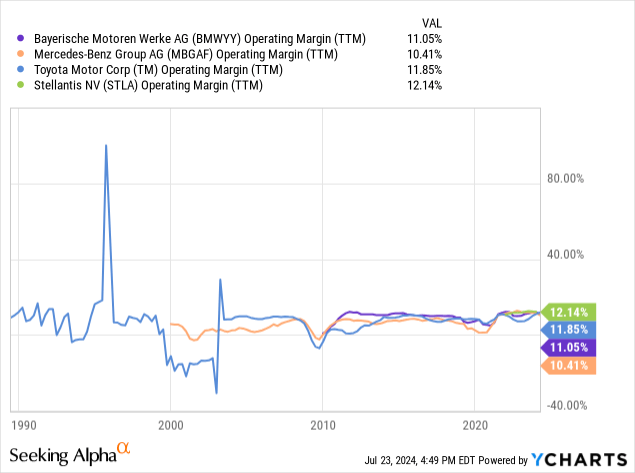

In fact, earnings are finally much more vital than revenues, as earnings permit for reinvestment, shareholder returns, M&A, and so forth. Right here, the development is clearly towards Tesla. Regardless of having the ability to eke out a small income improve, earnings continued to break down. Tesla’s working margin declined by round one-third year-over-year, from a strong (though removed from nice) degree of 9.6% to only 6.3% — the next chart reveals that this isn’t as much as par in comparison with what Tesla’s friends can obtain:

Each legacy premium car firms comparable to BMW or Mercedes (OTCPK:MBGYY) and legacy mass-market gamers comparable to Toyota (TM) or Stellantis (STLA) are producing margins which can be means larger than these of Tesla. Lengthy gone are the times when Tesla was in a position to generate robust margins because of quite a lot of pricing energy.

Earnings per share got here in additional than 40% decrease in comparison with the earlier 12 months’s quarter, each on a GAAP and a non-GAAP foundation, which brings up the query of why this firm needs to be valued at 100x web earnings. Alphabet/Google (GOOG, GOOGL) additionally introduced outcomes as we speak, delivering an debatable far stronger report with a lot of income development and earnings per share development of greater than 30%. And but, Alphabet trades at round one-quarter of Tesla’s valuation.

It’s, after all, potential that Tesla finally solves self-driving and enjoys robust earnings within the robotaxi enterprise. However to date, all of Elon Musk’s guarantees have did not materialize — there aren’t one million robotaxis on the highway as we speak, and no coast-to-coast summoning is on the market. The extremely anticipated occasion that was initially deliberate for August has been pushed down the highway, and we do not know but when (or if) one thing large will likely be introduced.

Those that need to purchase Tesla as a consequence of its potential in robotaxis can achieve this, after all, however once we take a look at the prevailing companies as we speak, the present valuation appears unjustified. The core enterprise is declining each when it comes to items and revenues, and whereas the vitality enterprise had a powerful quarter, it stays to be seen whether or not that development is sustainable or not. For now, margins proceed to compress, with earnings falling quickly — and but, Tesla is buying and selling at one of many highest valuations within the inventory market. Nvidia (NVDA) trades at lower than half Tesla’s earnings a number of and has explosive enterprise and revenue development, a wonderful market place, and ultra-strong (and rising) margins.

Takeaway

I believe that Tesla’s outcomes showcase that the corporate is overvalued proper right here. The core auto enterprise is struggling, margins and earnings are shifting within the mistaken path, and free money flows stay weak, at simply $1.6 billion over the past 4 quarters. That makes for an especially excessive free money stream a number of of round 500, for a free money stream yield of 0.2% (none of which is paid out to shareholders).

With higher-quality development firms being out there at a lot decrease valuations, I do not see a motive to personal Tesla, Inc. inventory. Those that belief in Elon Musk’s capacity to ship robotaxis could disagree, however I do not like shopping for overvalued shares as a consequence of administration’s guarantees.

Editor’s Notice: This text discusses a number of securities that don’t commerce on a significant U.S. alternate. Please concentrate on the dangers related to these shares.

[ad_2]

2024-07-23 22:51:14

Source :https://seekingalpha.com/article/4705961-tesla-these-results-are-way-too-weak?source=feed_all_articles

![Chase Freedom Flex℠ vs. Uncover it® Money Again [2024]](https://fitfinancespot.com/wp-content/uploads/2024/09/couple-using-cash-back-credit-card-120x86.jpeg)

{kind=link}

Discussion about this post