[ad_1]

Robert Manner

Shares of Tencent Holdings Restricted (OTCPK:TCEHY) preserve buying and selling at an undeservedly low price-to-earnings ratio regardless of the Chinese language expertise firm reporting respectable Q1’24 outcomes. Tencent represents good worth, in my view, as a result of the communications agency is rising, particularly in internet advertising. The firm’s give attention to controlling prices is paying off within the type of surging gross income and Tencent continues to generate a ton of free money circulation. For my part, an funding in Tencent displays a excessive security margin and U.S traders are too hesitant to purchase into promising Chinese language large-cap!

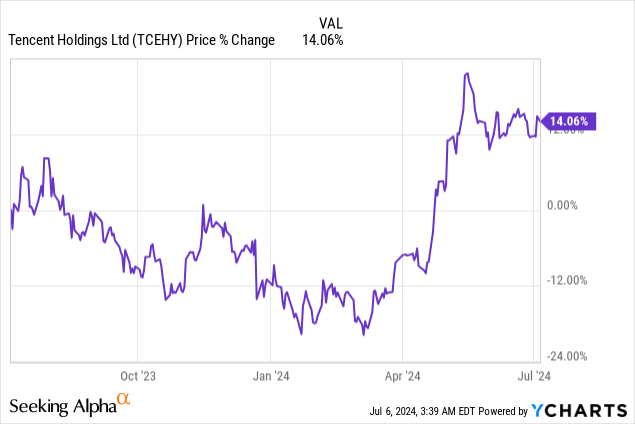

Earlier ranking

I rated Tencent a sturdy purchase in April 2024 as a consequence of a fast-growing internet advertising enterprise in addition to sturdy core enterprise profitability. Whereas I additionally referenced Tencent’s low valuation on the time, shares of the tech agency are nonetheless extensively undervalued given the corporate’s favorable enterprise developments. With Tencent additionally seeing sturdy free money circulation within the final quarter and posting free money circulation margins in extra of 30%, I consider Tencent is engaging as a capital return play going ahead.

Stable progress in Q1’24, surging gross income

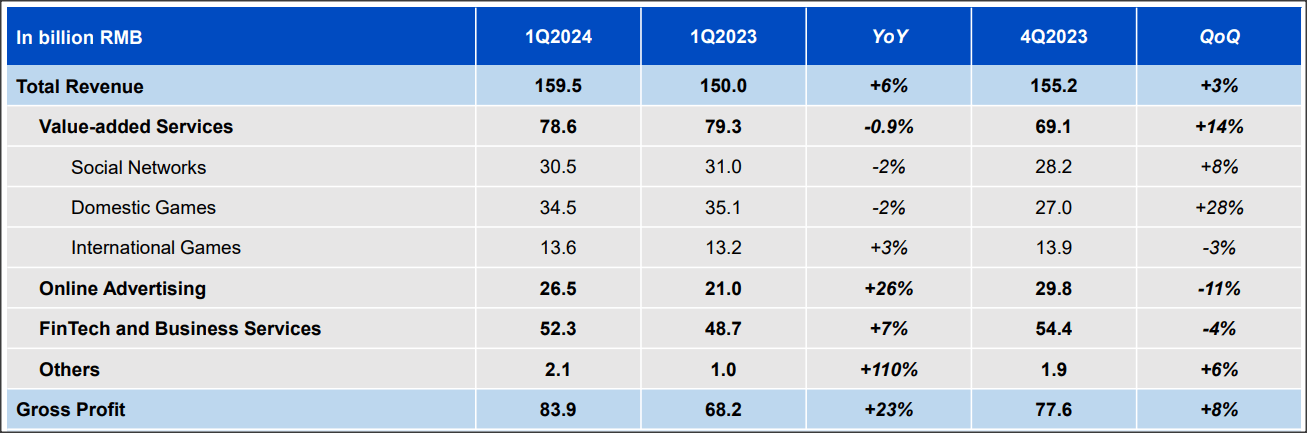

Within the first fiscal quarter, Tencent noticed a 6% improve within the high line and quarterly revenues of 159.5B Chinese language Yuan ($22.5B). Tencent is without doubt one of the high three Chinese language massive caps and owns various on-line and social media companies. Tencent is doing particularly properly in internet advertising proper now, with the Q1’24 earnings card exhibiting a 26% 12 months over 12 months progress price on this important enterprise. Whereas Tencent’s high line progress has moderated within the final couple of years as a consequence of slowing progress in China’s financial system, partly as a consequence of COVID-19, the trajectory in gross income appears to be like promising.

Tencent

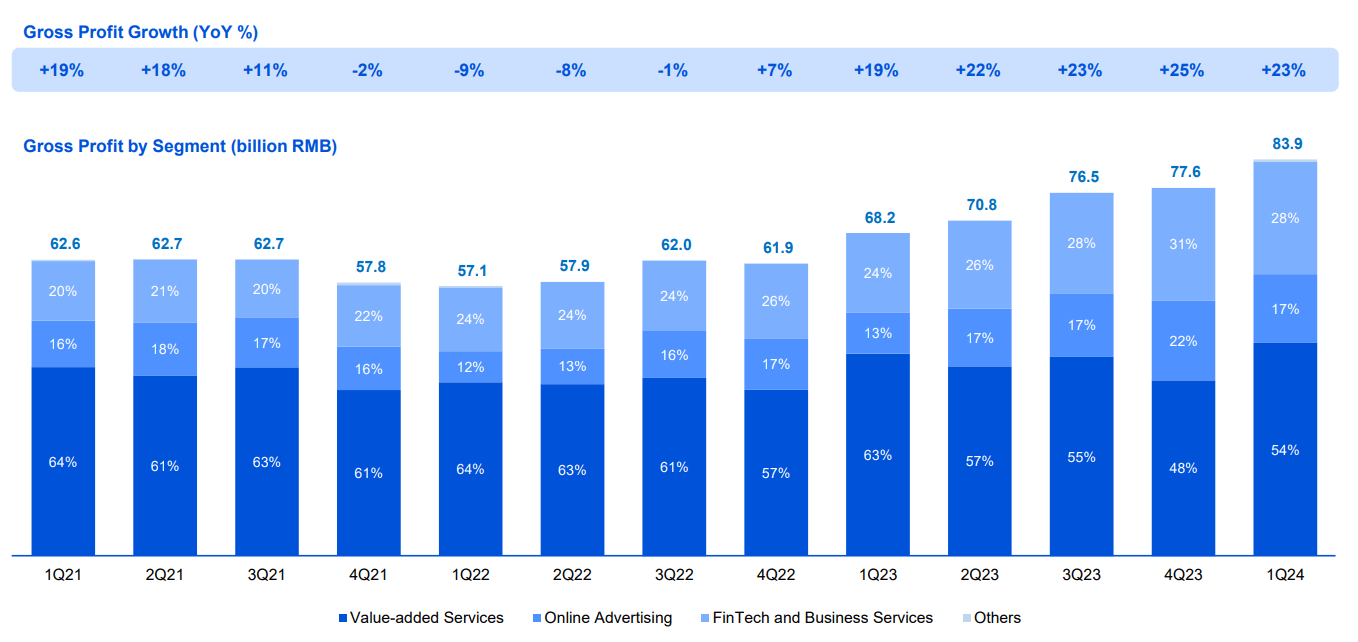

Tencent’s gross income are in an upsurge (+23% Y/Y) and hit 83.9B Chinese language Yuan ($11.8B) within the March quarter. Driving this progress is a stricter give attention to prices and a revisit of strategic priorities. For instance, to focus extra on profitability, Tencent simply determined to close down its on-line schooling platform which has about 400M customers.

The choice to close down the web schooling enterprise is pushed by a need to refocus consideration on the corporate’s core companies, similar to communications. Tencent, which is commonly known as China’s FaceBook, is the proprietor of Weixin, often known as WeChat, which is the biggest communications app in China with 1.4B month-to-month energetic customers.

Tencent’s ‘Worth-Added Providers’ which incorporates the agency’s social networking enterprise is accountable for greater than half (54%) of the corporate’s gross income… with one other 17% contributed by internet advertising. The internet advertising enterprise, which I discussed in April as underpinning my bullish outlook for Tencent, is by far the fastest-growing core enterprise for the Chinese language firm.

Tencent

Capital return potential

In addition to gross revenue momentum, a refocus on core enterprise actions, similar to social media and internet advertising, Tencent might probably grow to be engaging as a capital return play for traders.

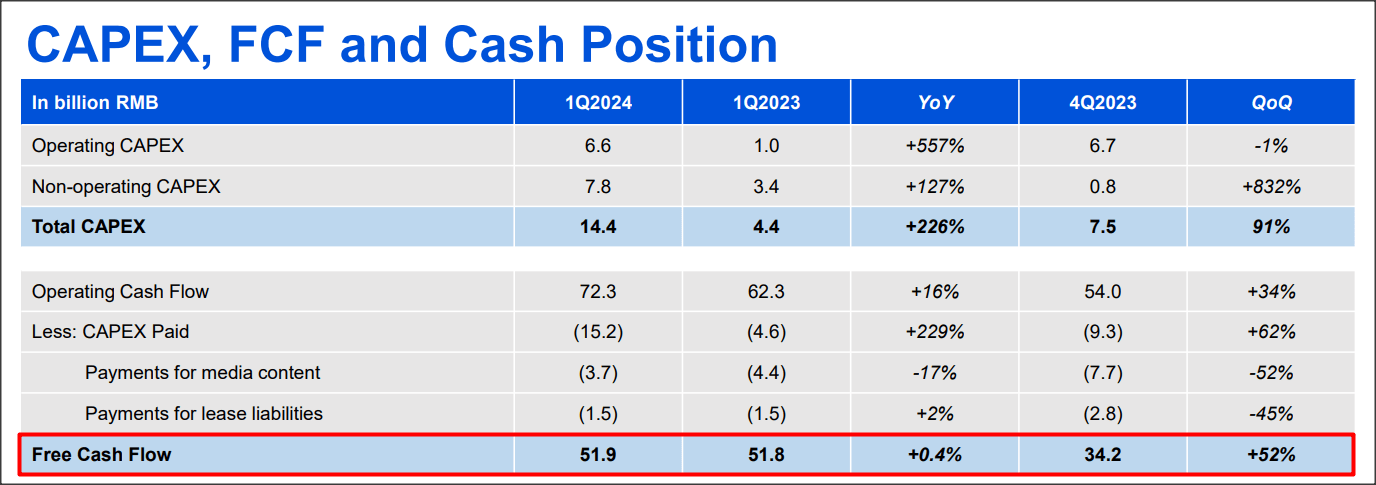

The explanation behind that is that Tencent is producing fairly a bit in free money circulation and the rebounding internet advertising enterprise paired with strategic price cuts has led to vital free money circulation tailwinds within the final quarter. In the latest quarter, Tencent generated 51.9B Chinese language Yuan ($7.3B), exhibiting 52% quarter over quarter progress.

The free money circulation margin expanded as properly and was a powerful 33% in Q1’24 in comparison with 22% in This autumn’23. A big a part of this free money circulation might get returned to shareholders sooner or later and Tencent might due to this fact grow to be far more engaging for traders from a inventory buyback perspective. For the present fiscal 12 months, Tencent has introduced plans to purchase again 100B Hong Kong Greenback ($12.8B) price of its shares. In Q1, Tencent repurchased 51M shares in Hong Kong for a complete consideration of 14.8B Hong Kong Greenback ($1.9B).

Tencent

Tencent’s valuation

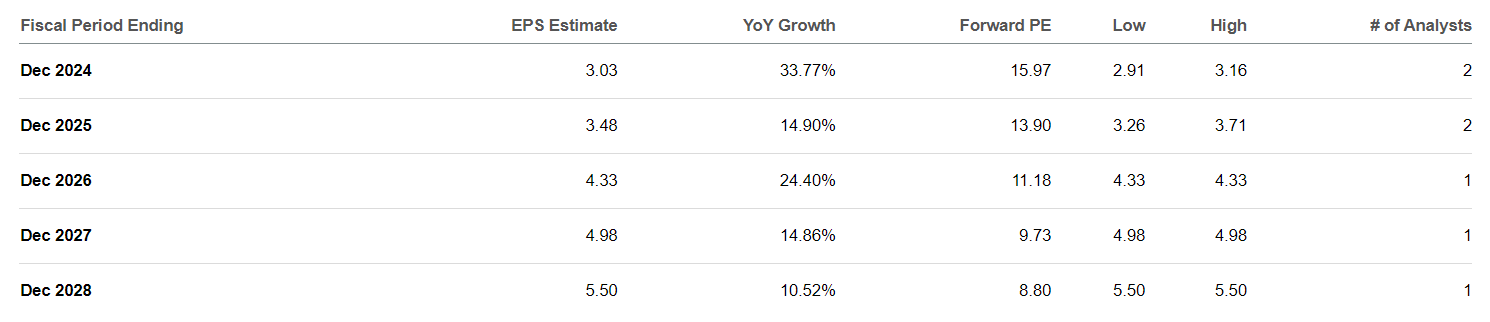

Like Alibaba (BABA) and Baidu (BIDU), Tencent is buying and selling for an unreasonably low price-to-earnings ratio. Tencent is valued at a 13.9X P/E ratio, primarily based off of FY 2025 earnings estimates, in comparison with 8.1X for Alibaba and seven.6X for Baidu. All three Chinese language large-caps are low-cost primarily based off of earnings, in my view, and Alibaba and Baidu clearly characterize even deeper earnings worth than Tencent does. Particularly Alibaba will be thought of a capital return play in addition to the e-Commerce agency lately introduced a particular dividend and is ready to purchase again extra shares going ahead.

Tencent has deep earnings worth as a result of its earnings per-share are rising quicker, nonetheless: each Alibaba and Baidu are anticipated to generate destructive EPS progress this 12 months whereas Tencent is projected to see 34% earnings per-share progress, as a consequence of a complete price restructuring and continuous momentum in internet advertising.

Given the power of Tencent’s free money circulation and gross income, stronger EPS progress and momentum in internet advertising, I’m elevating my honest worth P/E ratio from 15X to 15-16X which suggests a good worth vary of $52-56. This can be a dynamic quantity and will lower or improve primarily based off of Tencent’s core enterprise momentum, free money circulation margins and progress by way of shopping for again discounted shares out there.

Searching for Alpha

Dangers with Tencent

The largest danger for Tencent is that the corporate might see slowing progress in its on-line advertisements enterprise… which is the place all of the motion is true now for the corporate. As I mentioned previously, a possible Taiwan invasion could possibly be a danger issue for Chinese language equities generally. What would change my thoughts concerning the tech firm is that if it noticed moderating high line progress in its social media companies or a deterioration of its free money circulation (margins).

Closing ideas

Tencent has rather a lot to supply and presumably far more than traders are keen to confess. Whereas Tencent has been extensively out of favor with U.S. traders — as have Alibaba and Baidu — the corporate is rising its gross income shortly, seeing sturdy underlying free money circulation and shares are low-cost. Alibaba additionally lately stepped up its inventory buybacks and paid a particular dividend… strategic choices that had been at the very least partially directed at making shares extra engaging to traders outdoors of China. Tencent’s core enterprise is doing properly, particularly internet advertising which along with a extra critical give attention to price controls has led to improved profitability. Shares are nonetheless low-cost and the valuation, in my view, displays a excessive security margin!

Editor’s Word: This text discusses a number of securities that don’t commerce on a significant U.S. change. Please concentrate on the dangers related to these shares.

[ad_2]

{kind=link}

Discussion about this post