[ad_1]

Adriana Duduleanu

Co-Authored by Analyst Antonio Mello

Thesis

All through the final yr, there was a whole lot of motion via the industrials sector, with gold costs driving upward and copper volatility particularly. The sector offers for a singular funding alternative, particularly amongst two opponents, because the panorama of the trade gathers hypothesis. We consider there’s a window of alternative to capitalize on upside potential from the market discounting Newmont Company (NYSE:NEM) and potential underperformance of Teck Sources (NYSE:TECK). We suggest 130% lengthy publicity to Newmont Company and 50% brief publicity in Teck Sources as gold value forecasts counsel vital high line upside for Newmont Company, whereas sustaining greater progress potential via publicity in copper and the corporate is liquid, offering for extra funding alternative to scale operations or enhance complete manufacturing.

Firm Backgrounds

Teck Sources is Canada’s largest built-in pure sources group. Teck Sources has a Twin-class share construction, with the Keevil household holding vital voting management. The corporate is headquartered in Vancouver, Canada, however has widespread operations amongst. Particularly, Teck sources produces copper out of its 4 mines in Canada, Chile, and Peru. Teck Sources additionally produces zinc out of its Alaska working mine and produces coal out of its mines in British Columbia. The vast majority of Teck Sources’ income has come from their coal manufacturing, as it’s the largest producer in North America. The income breakdown as of the final fiscal yr, follows with 56.86% of income coming from coal, 22.82% of income coming from copper, and 20.33% of income coming from zinc.

Newmont Company is likely one of the world’s largest gold miners and is a publicly traded firm. The corporate is headquartered in Denver, Colorado and has publicity everywhere in the world, with operations in North America, South America, Australia, and Africa. In North America, their giant operations lay in Nevada, Colorado, and Mexico. In South America, their presence is critical in Peru and Suriname. Their operations run throughout all of Australia and penetrate Ghana inside Africa. Newmont Company produces and mines primarily for gold, however has giant secondary publicity to copper and a few publicity to silver, zinc, and lead. As talked about, they focus closely on gold manufacturing and have positioned themselves because the world’s largest gold mining firm by manufacturing and market capitalization.

Given the pattern of sure commodity costs and the growing shortage of pure sources, Newmont Company and Teck Sources discover themselves in a fascinating trade that might see elevated penetration, looking for an increasing number of manufacturing to produce surging tendencies. Among the many two corporations, they share opponents together with miners similar to Hudbay Minerals Inc. (HBM), First Quantum Minerals Ltd. (OTCPK:FQVLF), Lundin Mining Company (OTCPK:LUNMF), Agnico Eagle Mines Restricted (AEM), and Freeport-McMoRan Inc (FCX).

Qualitative Evaluation

The largest driver of worth for Newmont Company shall be tailwinds on gold and copper costs. Newmont Company solely operates in mining for gold and copper, apart from one mine that additionally produces silver, lead, and zinc. Teck Sources has produced primarily coal previously, in addition to copper and zinc. Consequently, we’ll primarily dig into gold, copper, coal and zinc tailwinds, as they make up most of every portfolio.

Gold is a pivotal side of this lengthy/brief funding, as Newmont Company has giant publicity in gold manufacturing and Teck Sources has no publicity in gold. As of just lately, gold costs have risen, and we maintain that they are going to proceed to rise into the foreseeable future, however have maintained a conservative long-term estimate. Gold costs have risen largely because of inflation ranges sustaining greater than goal ranges and traditionally observe this pattern as traders flip to gold when buying energy decreases and the U.S. greenback is weaker. We maintain that if gold can keep greater for longer, as inflation might keep greater for longer sooner or later, it suggests greater upside for the lengthy leg and no danger on the brief leg, as Teck Sources at the moment has no gold publicity or manufacturing.

What the market has advised us during the last yr is that buyers have change into extra comfy with elevated costs and an inflationary surroundings, as CPI has not budged considerably regardless of the hawkishness of the FED. This bodes effectively for future funding in gold and will drive gold costs up because of this.

Whereas gold costs have excessive potential to rise, we remained conservative with our estimates suggesting long-term gold costs will taper off to $1,970 per ounce. Compared to different gold projections, that is extraordinarily conservative.

Copper is uniquely vital relating to its place, as each corporations have related manufacturing ranges proper now and have indicated elevated curiosity in. As a result of each corporations share related quantity in copper and pursuits in ramping up quantity, how a lot every firm will increase manufacturing will largely decide how this place responds to motion inside the copper market. Relating to our projections, we assumed honest, leveled off will increase in copper costs per pound for a few causes. The primary driver in copper costs would be the push for inexperienced power transition. Particularly, the expansion in demand for electrical autos and the factitious intelligence sector will push costs upwards. Copper costs might also profit from sustaining greater inflation ranges, with the U.S. greenback remaining weaker. Teck Sources will greater than seemingly, profit extra from copper value tendencies, as they’re aiming to take a position extra into this phase and accomplished a big sale of a majority portion of their greatest income phase permitting for this.

Coal is one other pivotal side of this funding, because it has been Teck Sources’ greatest income phase by far. With the sale of 77% of its unit, this shall be considerably lowered, however will nonetheless keep a notable chunk of its income phase. Coal costs will greater than seemingly see a decline, and it could be vital. Coal is prone to undergo from an growing shift in direction of renewable power sources, stricter environmental laws, and improved power effectivity.

Moreover, Teck Sources has shifted its focus away from coal manufacturing regardless of its present quantity. Administration has already indicated curiosity in investing extra into copper, which can draw away from coal manufacturing, as indicated by the sale that occurred in November of 2023. This is sensible with regard to the demand tendencies for copper and coal. In our projections, we left manufacturing to be 23% of final yr’s manufacturing (present possession of its coal enterprise) and a constant $285 per tonne of coal.

Lastly, zinc is the final notable commodity to research. Teck Sources has seen declines in zinc manufacturing over the previous few years and will observe this pattern, as they shift focus into different segments, primarily copper. Our assumptions adopted that zinc manufacturing declines at an acceptable price, consistent with historic numbers and administration’s fiscal yr expectations, and zinc costs enhance steadily inside its vary of costs over the previous few years.

Foremost Factors

Newmont Company presents a compelling purchase alternative for quite a lot of causes spanning throughout progress runways, in addition to a reduced value through a Ahead EV/EBITDA imply a number of.

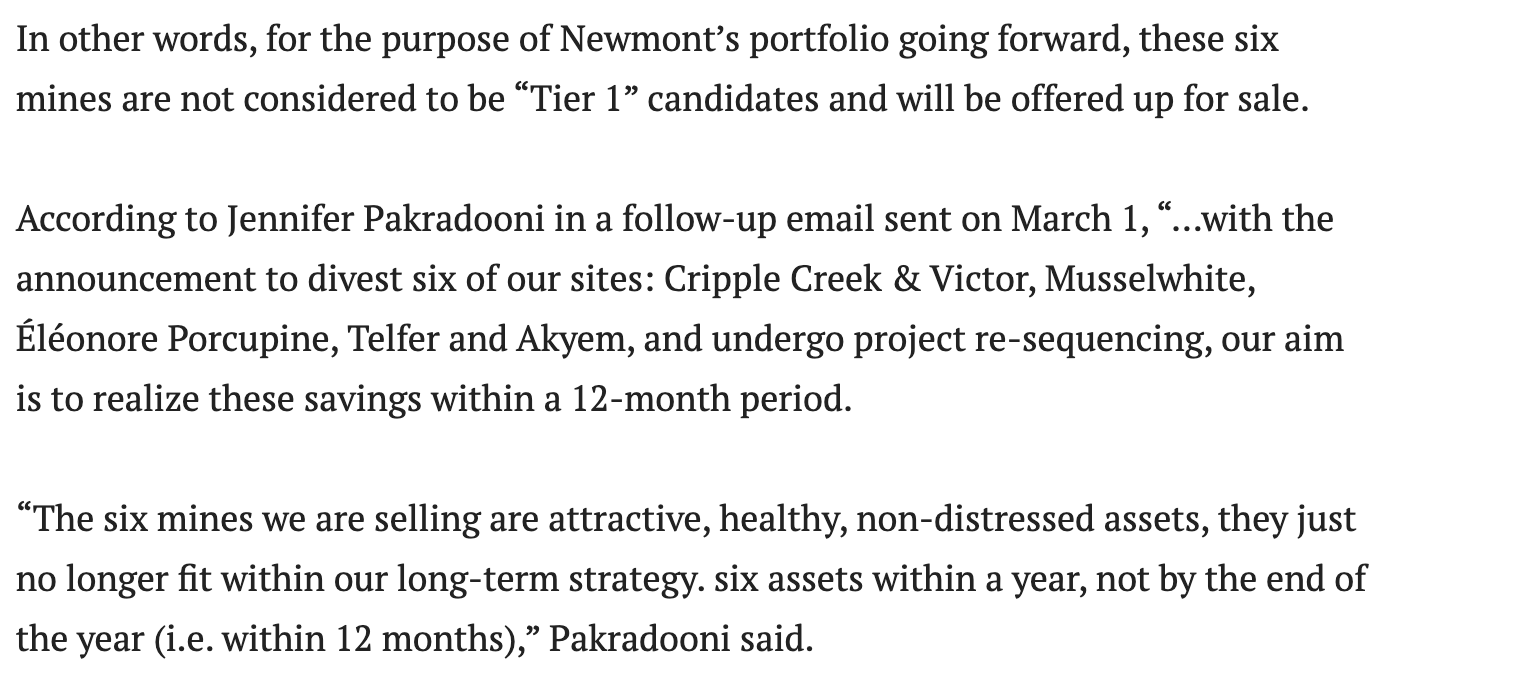

First, the administration staff has confirmed to be succesful and centered on delivering shareholder worth. The corporate operates primarily in tier 1 mines, the place it maximizes manufacturing. Administration can be proactive in adjusting the corporate’s positioning by promoting off belongings which are not tier 1 as just lately supplied. Newmont CEO Tom Palmer indicated their plans to divest eight non-core belongings, in addition to to trim the workforce to chop debt following their $17.14 billion acquisition of Newcrest. Management has additionally acknowledged that their shares are undervalued and introduced an aggressive $1 billion inventory buyback.

Pikes Peak Courier

Secondly, Newmont Company’s operations are set to proceed delivering worth in surging segments. All of their mines produce gold, with a number of moreover producing copper, just one nonetheless produces cheaper metals as effectively. Amongst all the firm’s mines, they keep top quality or will greater than seemingly be divested to chop down debt or reinvest into excessive worth operations. Newmont Company additionally boasts spectacular margins from operations, with a 34.90% gross margin compared to a comparables evaluation imply of 21.08%. Not solely are their present operations set to proceed growing manufacturing in present mines, which accumulates worth via rising costs, however the firm can be liquid, offering for extra funding alternatives into the enterprise to scale operations or enhance complete manufacturing even additional.

Lastly, as talked about earlier, the spot costs of the metals that Newmont Company produces are set to develop and enhance in demand, which can accumulate worth of their reserves and new manufacturing. The metals themselves will change into pricier and the gross sales yield of the metals which are produced will seemingly enhance, as will their place out there as they’re the biggest producer.

On the opposite aspect, Teck Sources appears to be buying and selling close to honest worth, and its progress outlook is minimized by its portfolio of operations.

Specifically, the biggest draw for Teck Sources would be the increase within the copper market. Contemplating this, you will need to take a look at how the income streams have shifted and can observe value tendencies. Contemplating the big manufacturing will increase in copper as administration indicated, this income phase will see substantial progress.

Nevertheless, trying on a cumulative scale, the expansion shall be restricted as they see vital declines to income from their greatest phase in coal making, the place it’ll offset the big progress they might see in copper costs. Thus, their progress in copper income will have to be extraordinarily vital and aggressive to offer the returns essential to counsel upside and by comparables evaluation imply multiples, Teck Sources trades at a good worth value.

A big advantage of the lengthy/brief place right here, is that markets have been highly regarded currently, so within the occasion of a market huge correction, our place presents safety whereas nonetheless incomes upside, as we consider Newmont Company will outperform Teck Sources throughout any timeframe.

Valuation

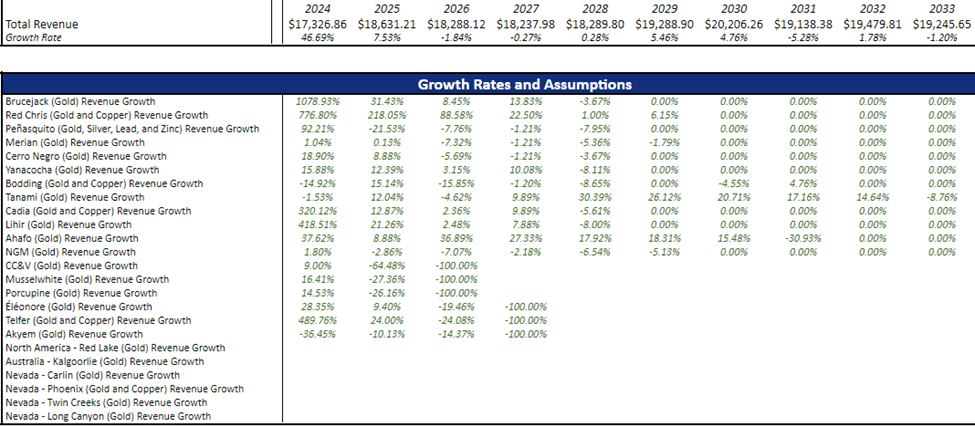

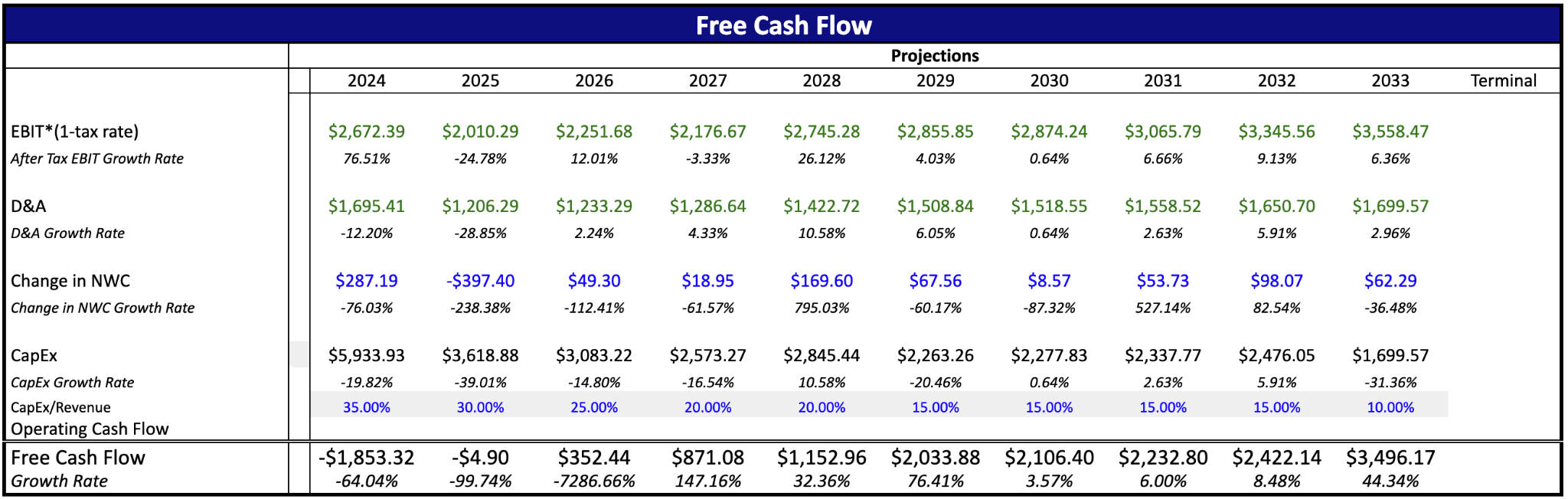

First, we’ll look via the Newmont Company Valuation. Income was projected through every mine, the place six of the mines have been offered off consistent with administration statements, that may accumulate a complete of round $2 billion. Moreover, newer mines skilled bigger progress spurts and 2024 values have been used from administration expectations for full yr manufacturing.

QOE Capital

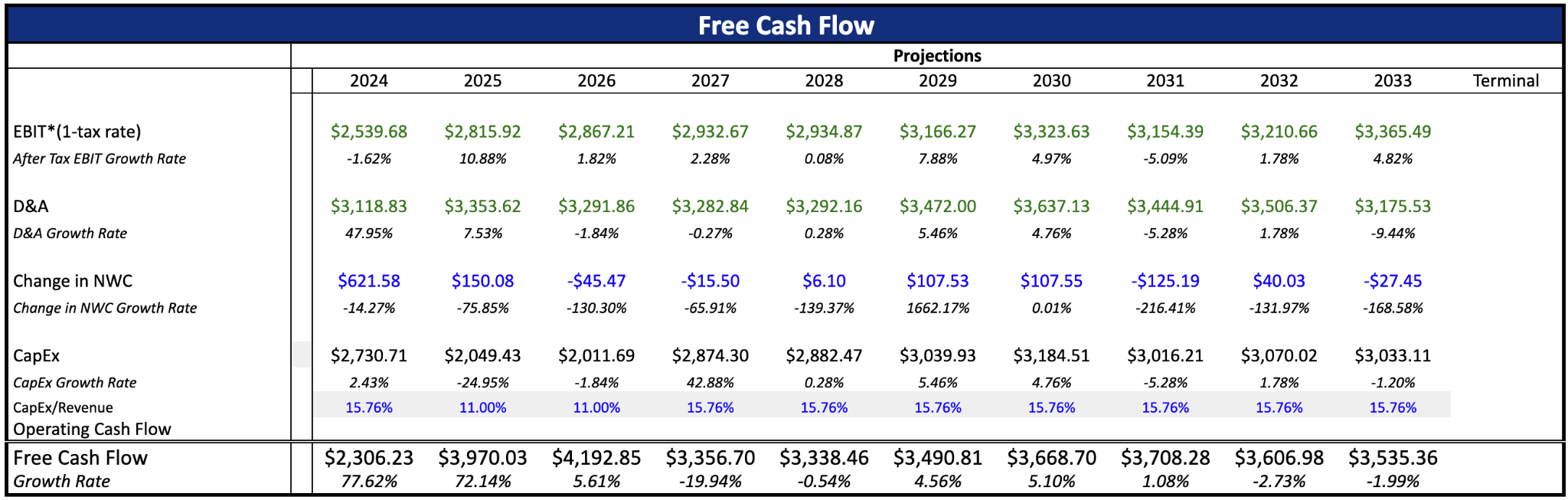

To undertaking web earnings and web earnings progress, we used the above income numbers and projected the working bills as a proportion of income, and utilized historic tendencies for the opposite assumptions.

QOE Capital

Change in Internet Working Capital was calculated by rising accounts receivables by the income progress price and stock and accounts payables by the price of items offered progress price.

QOE Capital

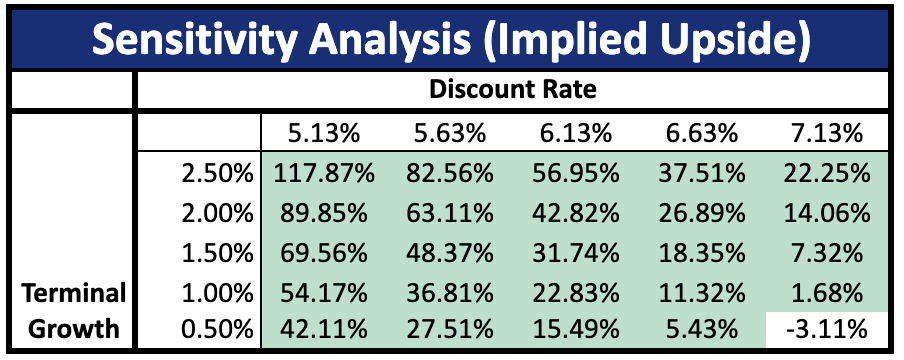

There’s vital upside and minimal draw back relating to the change within the WACC and terminal progress.

QOE Capital

Along with our DCF mannequin, we calculated an EV/EBITDA valuation with a imply ahead EV/EBITDA a number of from our comparables evaluation.

QOE Capital

Weighting the DCF $55.81 implied share value at 80% and the EV/EBITDA $55.34 implied share value at 20%, we reached an implied share value of $55.71 indicating an upside of 31.52%.

Teck’s Valuation

Now we’ll take a look at the Teck Sources valuation. Income was projected by every useful resource phase. The corporate indicated a shift in direction of curiosity in copper, following the sale of its coal enterprise, which is mirrored within the income projections.

QOE Capital

We utilized the identical course of as earlier than to undertaking web earnings progress and free money move progress.

QOE Capital QOE Capital

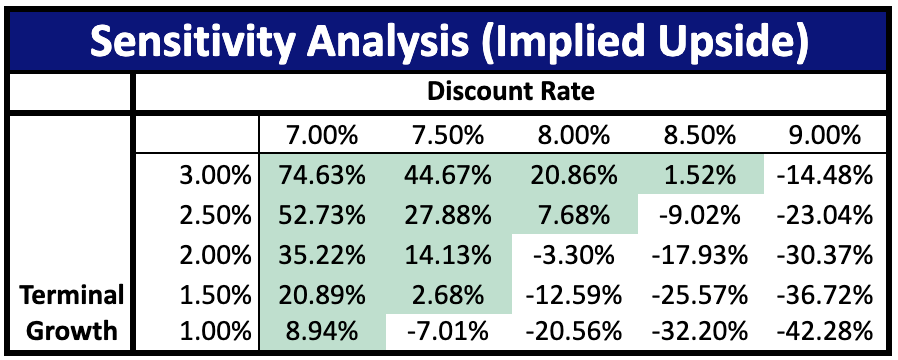

Teck Sources presents a lot much less wiggle room than Newmont in its valuation relating to adjustments to its WACC or terminal progress.

QOE Capital

We used the identical set of opponents for the comparables evaluation with Newmont Company.

Weighting the DCF, $45.70 implied share value at 80% and the EV/EBITDA $58.97 implied share value at 20%, we reached an implied share value of $48.35 indicating an upside of two.32%.

Dangers

With this place, the extreme danger that may be endured is the state of affairs the place gold costs decline and copper and zinc costs increase. We aimed to mitigate this danger in our evaluation by placing a haircut on our Gold Forecast when projecting income. Our common per ounce gold value schedule is as under:

| 2024 | 2025 | 2026 | 2027 | Lengthy-run |

| $2,155 | $2,195 | $2,070 | $2,045 | $1,970 |

The decrease expectation in 2024 is to mirror provide offered at pre-run-up costs in Q1.

The course of every firm has been outlined by each administration groups and follows that Newmont Company will proceed to provide gold, whereas additionally growing manufacturing progress of copper in gentle of demand tendencies. As for Teck Sources, they’re aiming to transition primarily into copper whereas sustaining lowered stakes in zinc and coal.

Relating to this, the biggest draw back comes from the state of affairs that gold costs will decline and copper and zinc costs soar. On this state of affairs, given Newmont Company additionally produces and sells copper, the danger is considerably minimized however not with out potential for losses, as Teck Sources appears to be extra aggressively aimed toward increasing their copper enterprise phase forward of the push for inexperienced power.

Teck Sources appears to be extra poised to reinvest into its copper phase from the sale of 77% of its coal enterprise, which can enable it to achieve extra from the expansion of the copper trade, than that of Newmont Company. Given our recommended brief place in Teck Sources, an increase in copper costs and decline in gold costs may very well be vital sufficient the place this place results in adverse returns.

One other notable danger that might result in vital draw back could be extra aggressive funding into the copper enterprise by Teck Sources than projected. If Teck Sources is ready to enhance manufacturing considerably above estimates forward of value tendencies, then they might have the ability to profit absolutely from a increase in copper value progress, exposing our place to adverse returns in a flourishing copper market.

Conclusion

We consider there may be a sexy alternative to learn from upside potential on Newmont Company’s operations portfolio and potential underperformance of Teck Sources. We once more suggest 130% lengthy publicity in Newmont Company and 50% brief publicity in Teck Sources, as commodity value forecasts counsel vital high line upside for Newmont Company whereas minimizing draw back via a hedged overlap in Teck Sources’ greatest potential income stream within the foreseeable future. The 130/50 lengthy/brief place will depart the place beta optimistic with a web lengthy publicity of 80%, which is justified within the portrayed upside for Newmont Company.

We’re bullish on Newmont Company and if Teck Sources loses worth, as we assume it’ll in gentle of their adjusting into the copper enterprise and buying and selling at honest worth even in a highly regarded market, the place ought to be rebalanced right into a 130% lengthy publicity in Newmont Company and a 30% brief publicity in Teck Sources.

[ad_2]

2024-07-08 22:18:59

Supply :https://seekingalpha.com/article/4703026-teck-resources-newmont-corp-golden-long-short-in-mining-space?supply=feed_all_articles

{kind=link}

Discussion about this post