[ad_1]

jsnover

One firm that I’ve been constantly bullish about over the previous few years is homebuilder Taylor Morrison Residence Company (NYSE:TMHC). With a market capitalization as of this writing of about $7.1 billion, the corporate is moderately sizable. Nevertheless it hasn’t at all times been this massive. Since I final wrote a bullish article in regards to the firm in Might of this yr, the inventory has risen by 15.9% whereas the S&P 500 is up solely 5.8%. And since I first rated it a ‘purchase’ again in January of 2022, shares have skyrocketed 125.9% whereas the S&P 500 has risen solely 28.4%.

The efficiency achieved by the corporate is an actual demonstration of profitable worth investing. You’d suppose that the corporate would have been exhibiting super development throughout this time. However the truth of the matter is that monetary efficiency has been considerably mediocre. There are some shiny spots, similar to rising backlog and year-over-year will increase in new orders for houses. These counsel that good instances lie forward. However income, income, and money flows have been shrinking for some time. The rationale why the market has largely ignored it’s because shares have been tremendously undervalued. And even right this moment, the inventory is reasonable in comparison with most related enterprises. Given this and contemplating what doubtless lies across the nook with rates of interest, I do suppose that conserving the corporate rated a ‘purchase’ is sensible for now.

Nice upside regardless of some weaknesses

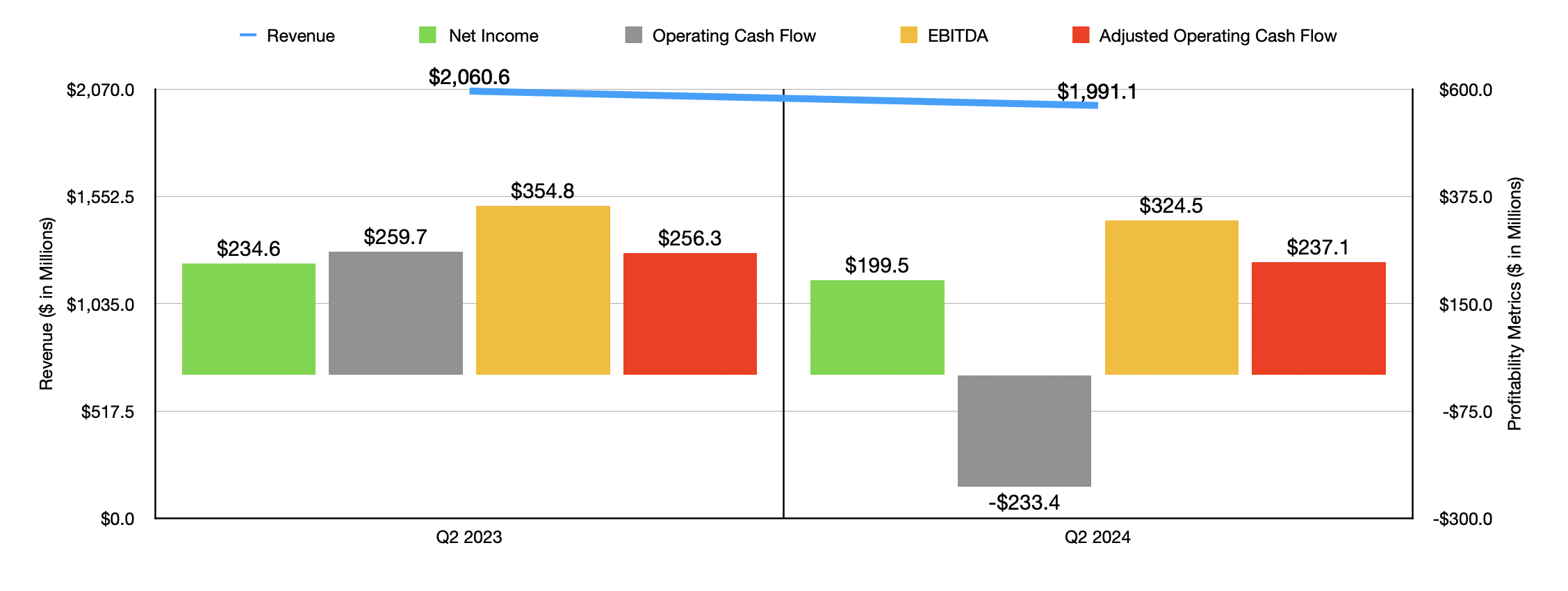

In my most up-to-date article overlaying Taylor Morrison Residence Company, I detailed monetary efficiency from 2022 to 2023. My purpose is to not rehash these particulars now. The necessary factor to bear in mind is that, yr over yr, income, income, and money flows, all took successful. The most up-to-date information that I’ve concerning the enterprise covers the second quarter of 2024. In order that could be an important place to begin. Throughout that point, income for the corporate got here in at $1.99 billion. This represents a drop of three.4% in comparison with the $2.06 billion the enterprise reported only one yr earlier.

Creator – SEC EDGAR Knowledge

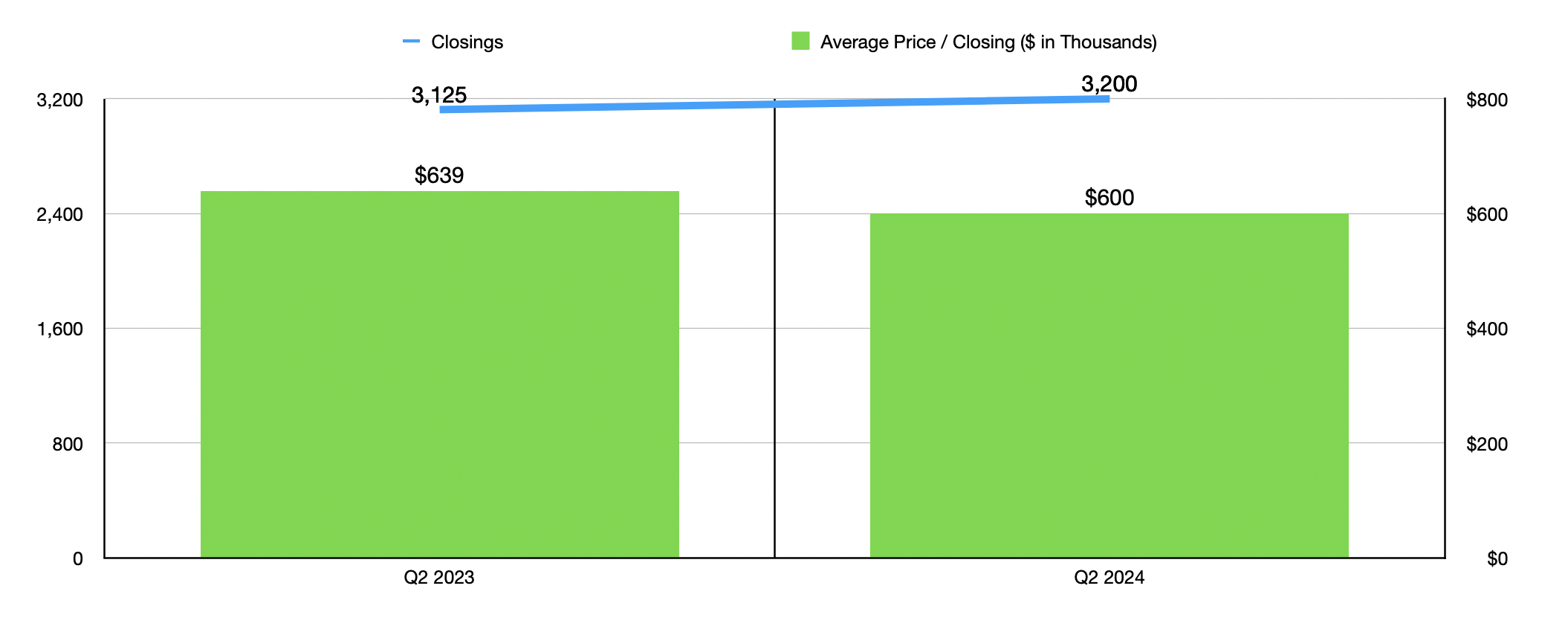

With an organization within the homebuilding area, income is basically decided by two major elements. The primary could be the variety of houses closed on, and the second could be the value at which these houses have been closed on. Whole closings within the second quarter got here in sturdy at 3,200. That is a modest uptick from the three,125 reported the identical time final yr. You’d suppose that this might trigger income to rise. Nonetheless, the typical worth of a closing dropped a yr over a yr, falling from $639,000 to $600,000. The actual fact of the matter is that prime rates of interest have a damaging impression on residence costs. And proper now, rates of interest are the best they’ve been in a long time. Or not less than that’s what the info reveals when it comes particularly to the charges set by the Federal Reserve.

Creator – SEC EDGAR Knowledge

With income falling, income have additionally taken successful. Web revenue dropped from $234.6 million within the second quarter of 2023 to $199.5 million the identical time this yr. The drop in gross sales definitely contributed to this. Nevertheless it was additionally the truth that the drop was pushed by worth adjustments versus quantity adjustments that actually negatively impacted margins. Different money move metrics adopted an analogous trajectory. Working money move went from $259.7 million to damaging $233.4 million. If we alter for adjustments in working capital, we get a smaller drop from $256.3 million to $237.1 million. And at last, EBITDA for the corporate managed to fall from $354.8 million to $324.5 million.

Creator – SEC EDGAR Knowledge

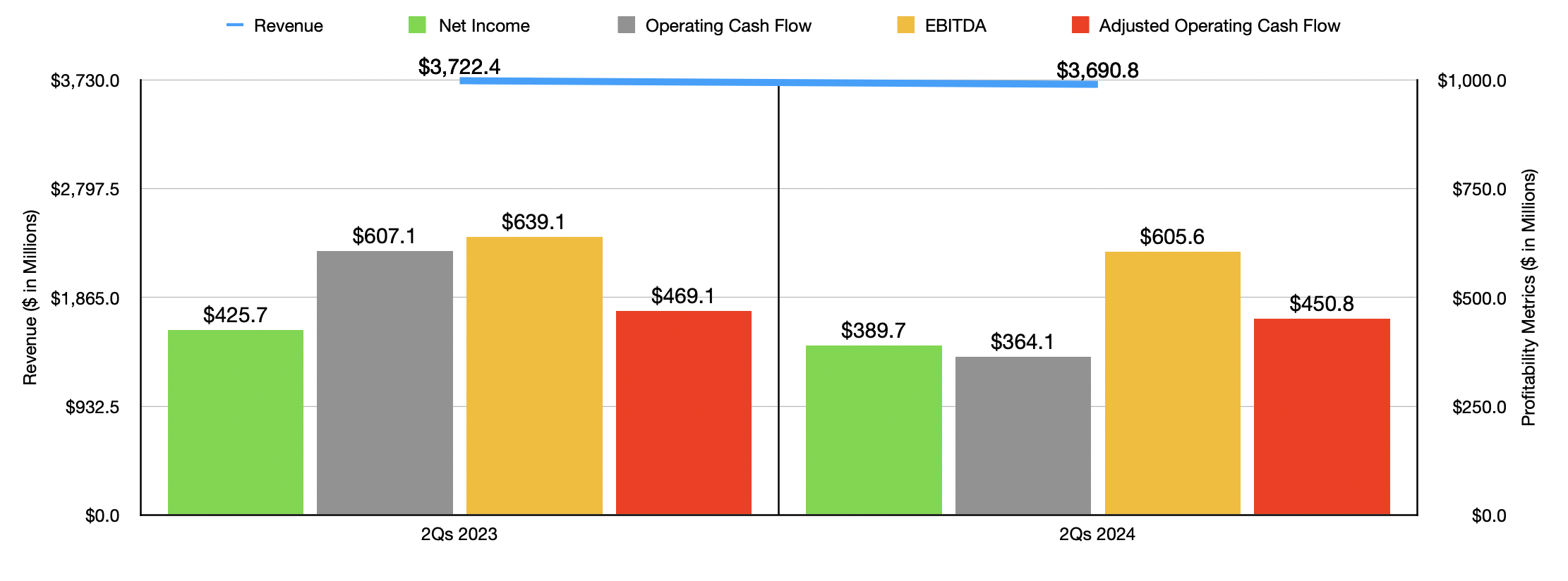

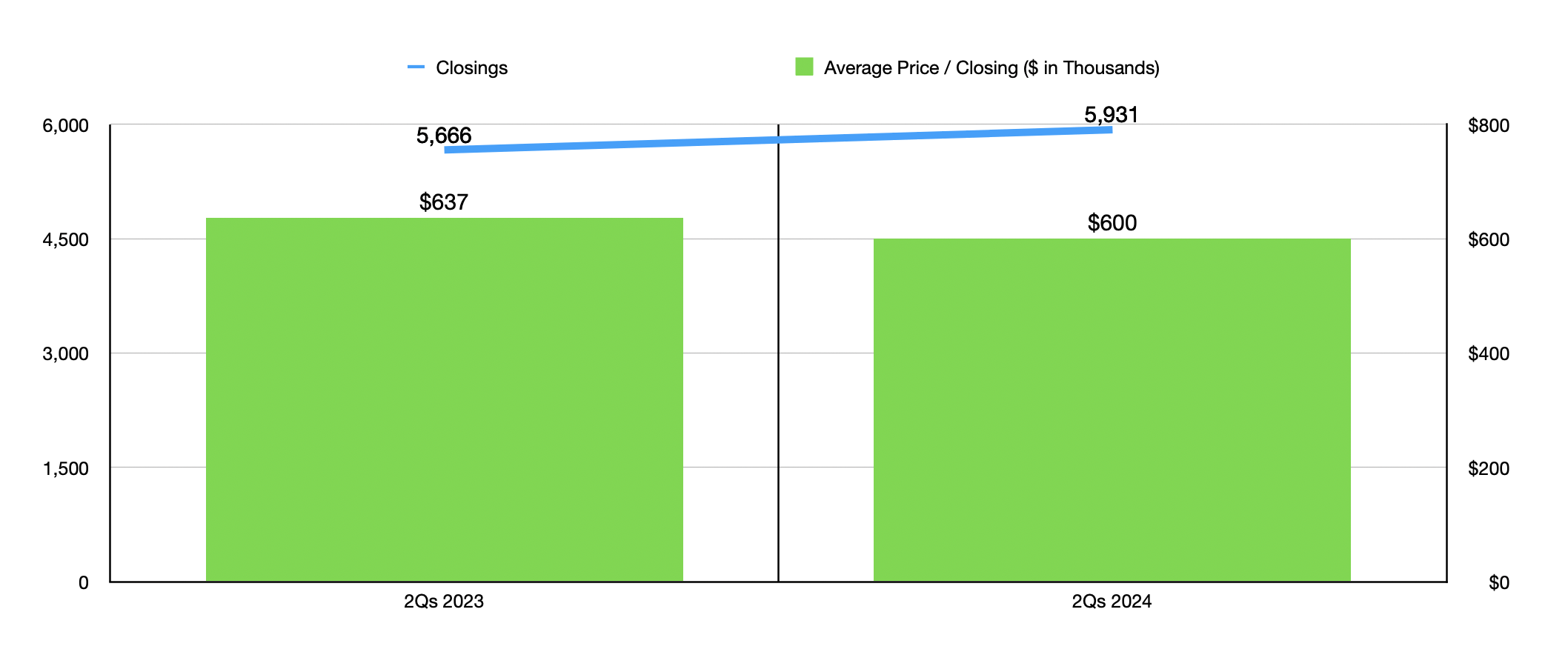

Within the chart above, you may see monetary outcomes for the primary half of 2024 in comparison with the identical time in 2023. As was the case within the second quarter alone, income, income, and money flows, all took successful on a year-over-year foundation. This was despite the truth that the variety of residence closings jumped properly from 5,666 to five,931. Not surprisingly, the ache for the corporate got here from a decline within the common worth of a house closed from $637,000 to $600,000.

Creator – SEC EDGAR Knowledge

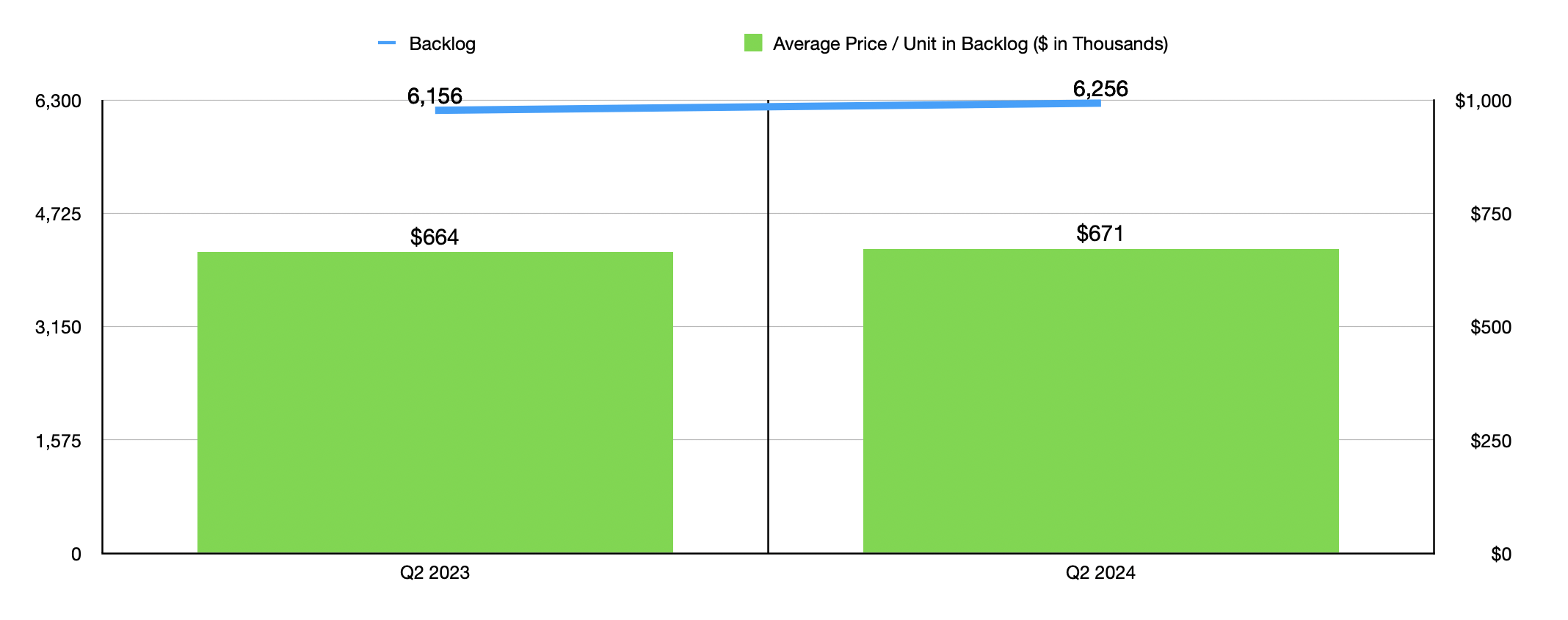

Typically, an increase in closings can translate to a decline in backlog. This happens when new contract orders are available weaker than what closings have been. However that isn’t what we have now seen. By the top of the latest quarter, Taylor Morrison Residence Company boasted 6,256 houses in its backlog. This represented a rise over the 6,156 houses in its backlog the identical time final yr. And although the typical worth of a house closed dropped, the typical worth of 1 in backlog grew from $664,000 to $671,000.

Creator – SEC EDGAR Knowledge

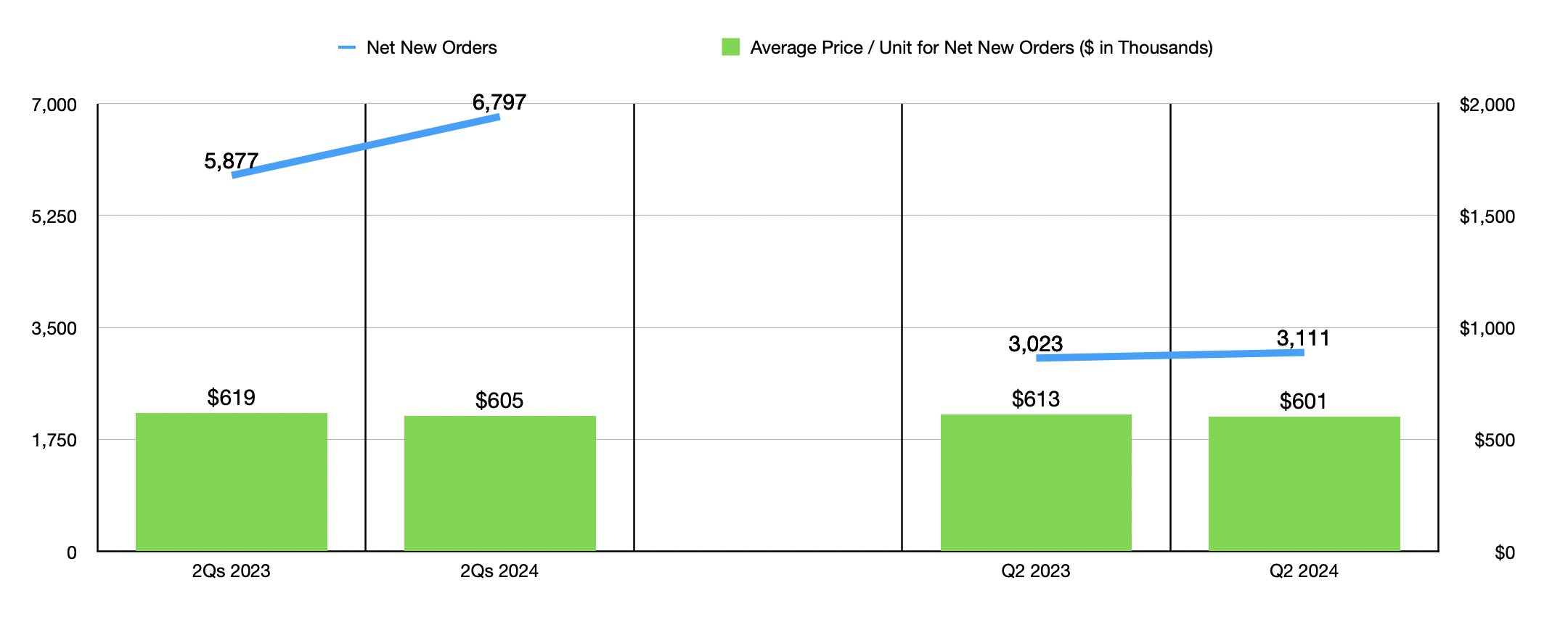

This enchancment in backlog was made doable by web new orders in the latest quarter of three,111 houses. That’s increased than the three,023 houses ordered the identical time final yr. Yr thus far, the advance was even higher, with 6,797 houses ordered on a web foundation far outpacing the 5,877 houses ordered the identical time final yr. Sadly, the brand new contracts coming to the corporate contain decrease priced houses. For the latest quarter, these houses have been valued at $601,000 apiece. That is down from $613,000 reported the identical time final yr. And for the primary six months of this yr, the worth is $605,000 in comparison with $619,000 reported for the primary half of 2023.

Creator – SEC EDGAR Knowledge

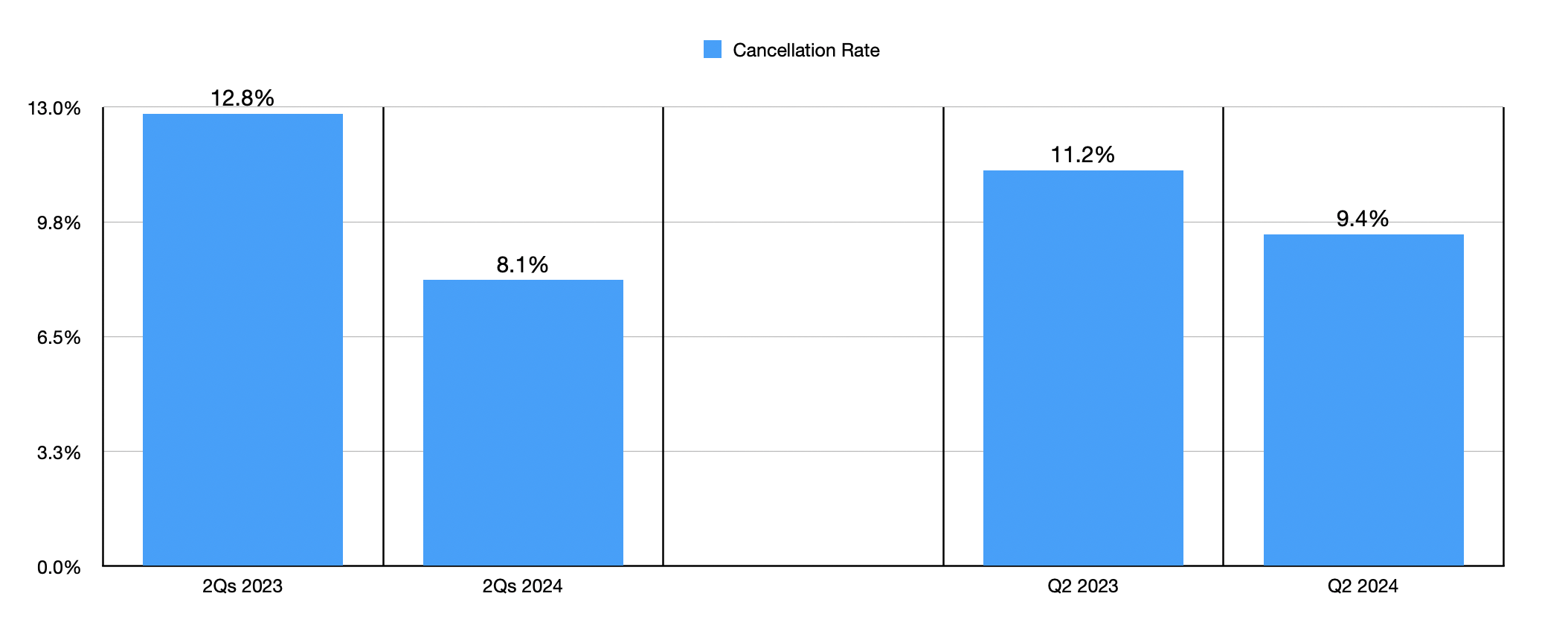

One other factor that has benefited the corporate has been a significant enchancment in cancellation fee. Simply because a house is ordered doesn’t imply that the client will comply with by way of on it. Over the previous couple of years, the surge in inflation and the excessive rates of interest aimed toward combating that inflation resulted in cancellation charges skyrocketing. Companywide, cancellation charges spiked to 13.5% in 2022. Although in some elements of the nation the place it operates, this quantity was increased at 18.5%. And I’ve seen different homebuilders with charges far in extra of 20%. The excellent news is that, in the latest quarter, the cancellation fee was solely 9.4%. That is down from 11.2% one yr earlier. And for the primary six months of this yr, the 8.1% reported by administration was materially under the 12.8% achieved within the first half of 2023.

Creator – SEC EDGAR Knowledge

We do not actually have a lot in the best way of steering relating to 2024 in its entirety. Or to be extra exact, we do not have what I want to have. Nonetheless, administration did say that traders ought to anticipate between 12,600 and 12,800 residence closings this yr. That may really be, on the midpoint, the second highest within the firm’s historical past, second solely to the 13,699 closed in 2021. These houses ought to are available at a median worth of between $600,000 and $610,000. So the costs we have now been seeing to date this yr are unlikely to enhance materially, if in any respect, within the second-half of the yr.

Creator – SEC EDGAR Knowledge

That is not the top of the world. If we annualize the outcomes seen to date for this yr, we might anticipate a web revenue of $703.9 million, adjusted working money move of $821.5 million, and EBITDA of $1.19 billion. Utilizing these estimates, in addition to historic outcomes from 2023, we are able to see within the chart above how shares of the enterprise are priced. On a ahead foundation, they’re costlier than utilizing the historic outcomes. However they are not considerably costlier, they usually do look attractively priced on an absolute foundation. Within the desk under, I then in contrast the corporate to 5 related companies. On a worth to earnings foundation, two of the 5 ended up being cheaper than our candidate. This quantity drops to one of many 5 on an EV to EBITDA foundation. And if we use the value to working money move method, Taylor Morrison Residence Company finally ends up being the most cost effective of the group.

| Firm | Worth / Earnings | Worth / Working Money Movement | EV / EBITDA |

| Taylor Morrison Residence Company | 10.0 | 8.6 | 7.5 |

| Legacy Housing Company (LEGH) | 12.3 | 81.2 | 9.3 |

| Meritage Houses (MTH) | 8.7 | 19.3 | 6.9 |

| Century Communities (CCS) | 10.2 | 74.7 | 9.7 |

| Beazer Houses USA (BZH) | 6.8 | 25.8 | 12.4 |

| KB Residence (KBH) | 11.1 | 11.9 | 9.7 |

Just lately, there have been some considerations in regards to the state of the economic system. Primarily, there was the event that jobs created within the personal sector have been overstated to the tune of 818,000 within the mixture within the 12 months ending in March of this yr. Whereas broader financial weak spot might trigger an issue for housing demand, it is also true that the Federal Reserve will virtually definitely reduce rates of interest for the primary time since they started elevating them. That reduce is predicted for September. Generally, decrease rates of interest make the financing of homes extra interesting as a result of, all else being equal, it lowers the general pricing of stated homes. And in keeping with most sources on the matter, there appears to be a scarcity of homes on this nation. Again in December of final yr, it was estimated that the nation was quick on housing by 3.2 million items. Extra current estimates have instructed that this quantity could be nearer to 4.5 million. This pent-up demand will doubtless end in increased orders and doubtlessly increased residence costs as soon as charges begin falling constantly. So, absent a major financial downturn, I do not see any purpose to grow to be bearish on the enterprise simply but.

Takeaway

Basically talking, issues may not have been the most effective for Taylor Morrison Residence Company lately. However on the entire, the corporate is doing fairly effective. Sure, income, income, and money flows are all dropping yr over yr. However shares are low-cost and backlog is rising. Cancellation charges are declining, and an eventual reduce in rates of interest ought to show bullish for it and corporations prefer it. Add all of this collectively, and I’ve no drawback conserving the corporate rated a ‘purchase’ for now.

[ad_2]

2024-09-01 05:44:12

Source :https://seekingalpha.com/article/4718367-taylor-morrison-home-corporation-despite-weaknesses-picture-for-the-business-is-bullish?source=feed_all_articles

{kind=link}

Discussion about this post