[ad_1]

Sundry Pictures

Again in late March of this 12 months, one firm that I had determined to downgrade was residence enchancment big The Residence Depot, Inc. (NYSE:HD). Since October 2022, I had been bullish on the agency. And the returns throughout that window of time had been constructive. The inventory was up 44.1% whereas the S&P 500 (SP500) was up 39.6%. However between how the inventory had develop into priced, and due to the agency’s determination to accumulate SRS Distribution in alternate for $18.25 billion, I felt as if a downgrade to a “maintain” from a “purchase.” Since then, the inventory is definitely down 0.7% whereas the S&P 500 is up 6.4%.

Since that point, information overlaying two extra quarters has come out. The agency has additionally accomplished its acquisition of SRS Distribution. This provides us extra readability concerning the general well being and trajectory of the enterprise. However between how shares are nonetheless priced and due to key market weaknesses, I believe it will be a mistake to improve it right now. In consequence, I’ve determined to maintain the agency rated a “maintain” for now.

A take a look at current outcomes

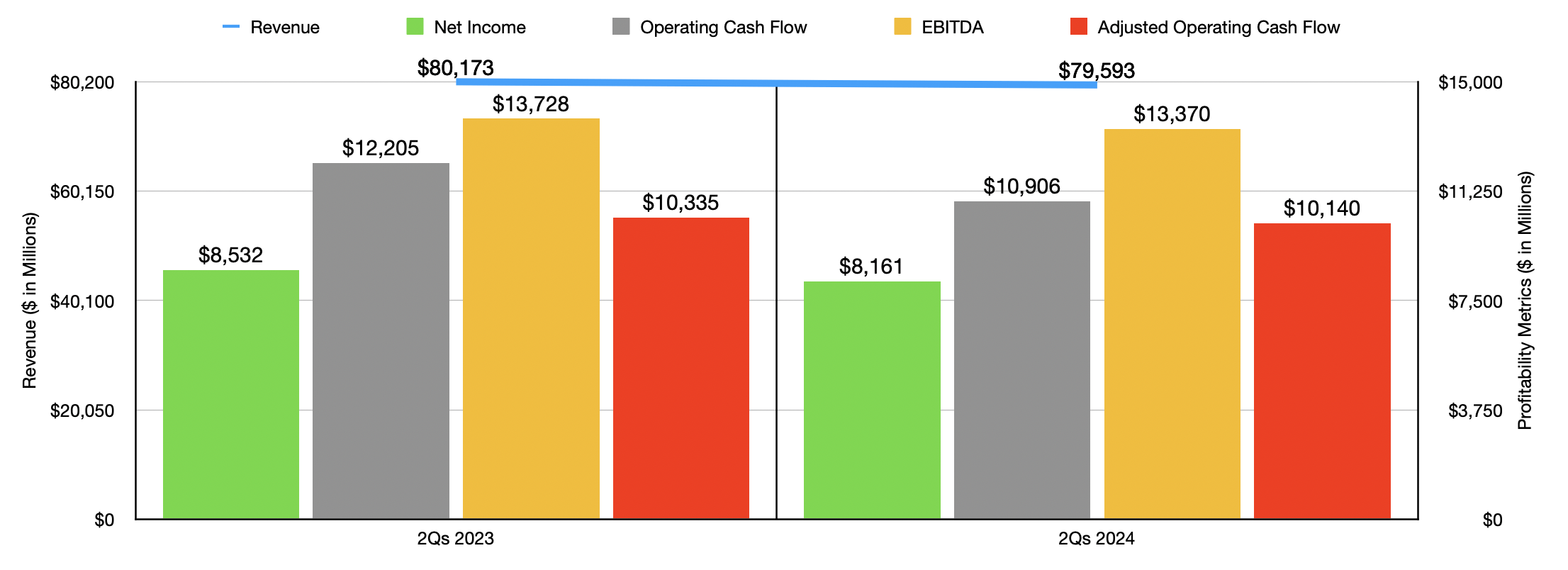

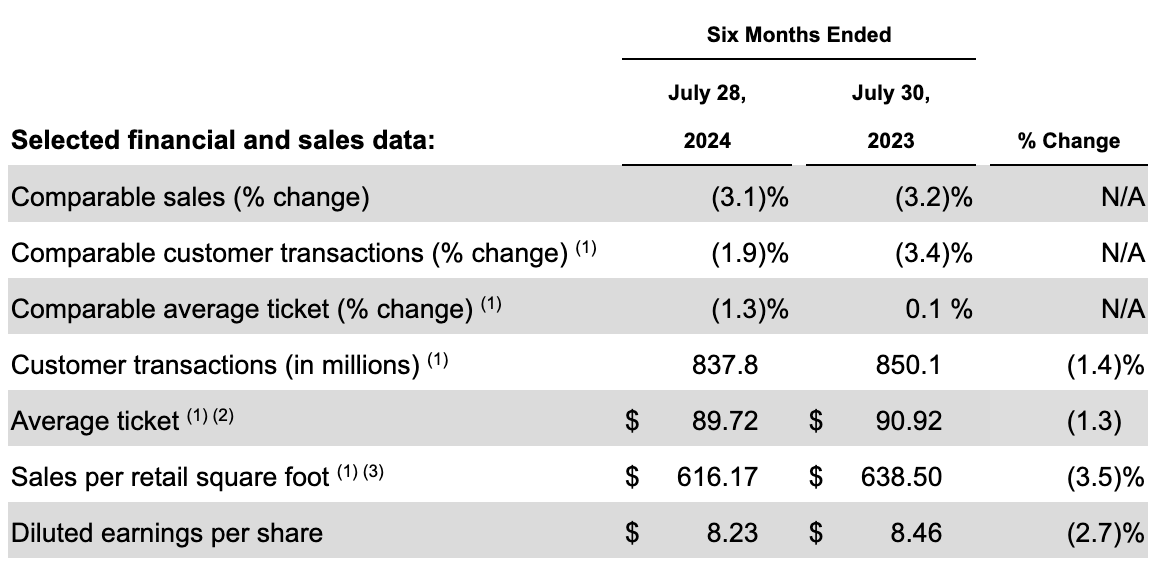

Essentially talking, current information offered by administration has been combined, however principally unfavourable. For the first half of 2024, income for the corporate got here in at $79.59 billion. That represents a lower of 0.7% in comparison with the $80.17 billion the corporate reported one 12 months earlier. This decline was pushed by weak spot throughout the board. For starters, comparable gross sales declined by 3.1% throughout this time period. This was due to a 1.9% drop in comparable transactions and a 1.3% drop within the comparable common ticket. The overall variety of transactions for the corporate fell from 850.1 million to 837.8 million, whereas the common ticket throughout this time dropped from $90.92 to $89.72.

Writer – SEC EDGAR Information

The image for the corporate would have been worse had it not been for its acquisition of SRS Distribution. That buy closed in June of this 12 months. And in line with administration, that new entity contributed $1.3 billion to the agency’s high line. Administration attributed the comparable gross sales decline to macroeconomic situations that resulted in fewer purchases at its shops. As well as, there was worth stabilization that may solely be interpreted as worth cuts that had been carried out following worth will increase the prior 12 months that the corporate pushed by way of due to inflationary pressures.

The Residence Depot

With income dropping, earnings for the corporate additionally took a success. Web revenue fell from $8.53 billion to $8.16 billion. This was despite the fact that the agency’s gross revenue margin expanded from 33.3% to 33.7% due to decrease transportation bills and decrease shrinkage. Different prices, nonetheless, did enhance 12 months over 12 months. Particularly, promoting, common, and administrative prices, grew from 16.6% of income to 17.4%. A discount in legal-related advantages, a rise in payroll prices, and deleveraging related to the decline in comparable retailer gross sales, had been all accountable for this. Different profitability metrics for the corporate additionally took a dive. Working money circulation fell from $12.21 billion to $10.91 billion.

If we regulate for modifications in working capital, the decline was extra modest, from $10.34 billion to $10.14 billion. In the meantime, EBITDA for the corporate dropped from $13.73 billion to $13.37 billion.

Writer – SEC EDGAR Information

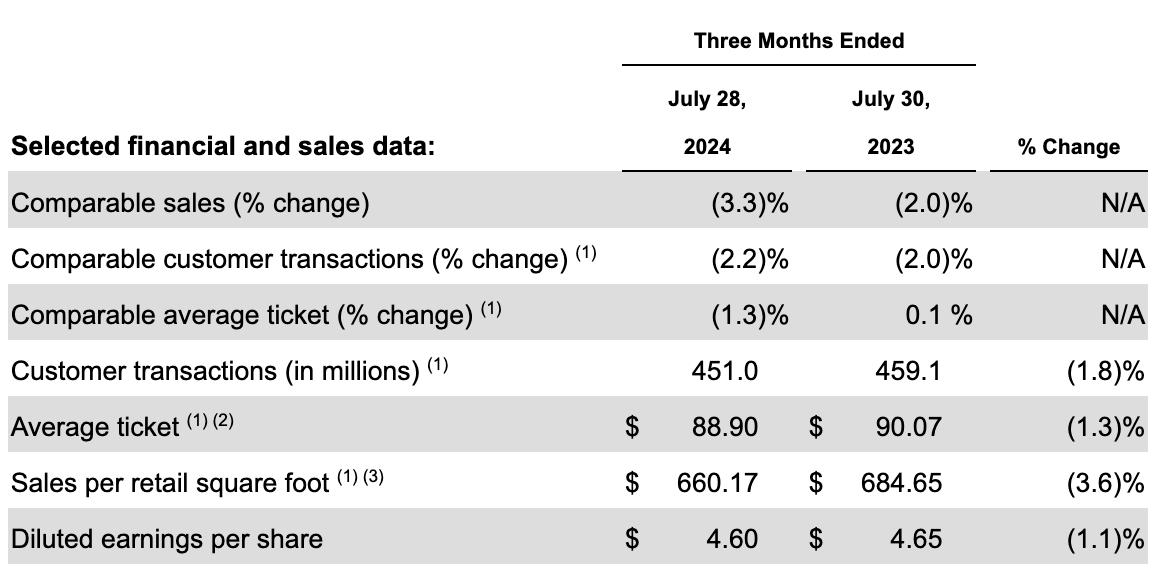

Within the chart above, you may see outcomes for simply the latest quarter by itself. As was the case for the primary half of the 12 months in its entirety, earnings had been down. Nevertheless, income and a few money circulation gadgets got here in stronger 12 months over 12 months. The rise in income for the corporate got here from the $1.3 billion from the corporate’s acquisition of SRS Distribution. Comparable gross sales, nonetheless, dropped a somewhat painful 3.3% as buyer transactions dropped 2.2% on a comparable foundation and because the comparable common ticket of consumers fell by 1.3%. The identical pressures that impacted the corporate for the primary half of the 12 months as a complete impacted outcomes for the second quarter.

The Residence Depot

Relating to the 2024 fiscal 12 months in its entirety, administration expects whole income to return in between 2.5% and three.5% above what it was final 12 months. Nevertheless, comparable gross sales are anticipated to say no by between 3% and 4%. This disparity might be attributed to issues. First, administration expects that SRS Distribution will add $6.4 billion in income for the 12 months. And second, an additional working week will add about $2.3 billion to the corporate’s high line. Adjusted earnings per share ought to fall by between 1% and three%. However this consists of $0.30 per share related to the additional working week and a few unknown quantity related to SRS Distribution.

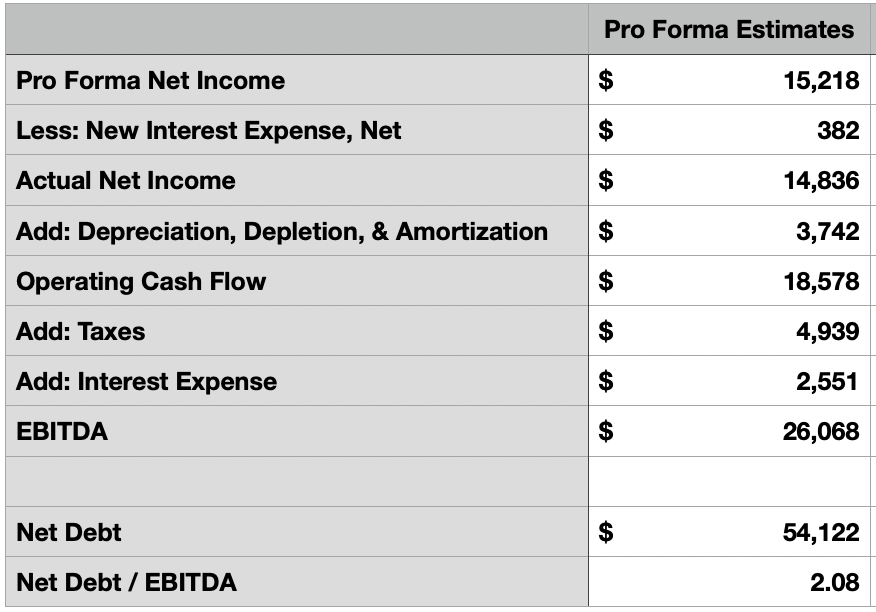

Relating to valuing the corporate, we’re confronted with sure challenges due to the aforementioned buy of SRS Distribution. In my prior article on The Residence Depot, we got some estimates concerning that enterprise on a standalone foundation. And we additionally had trailing 12-month information for The Residence Depot as nicely. I’d argue that due to the small decline in comparable gross sales anticipated, the general monetary efficiency achieved by The Residence Depot is not going to be radically completely different on a standalone foundation than it was in 2023. If we make this assumption, and we use the info offered by administration concerning SRS Distribution, we will get some perception into a professional forma image for the mixed enterprise.

Writer – SEC EDGAR Information

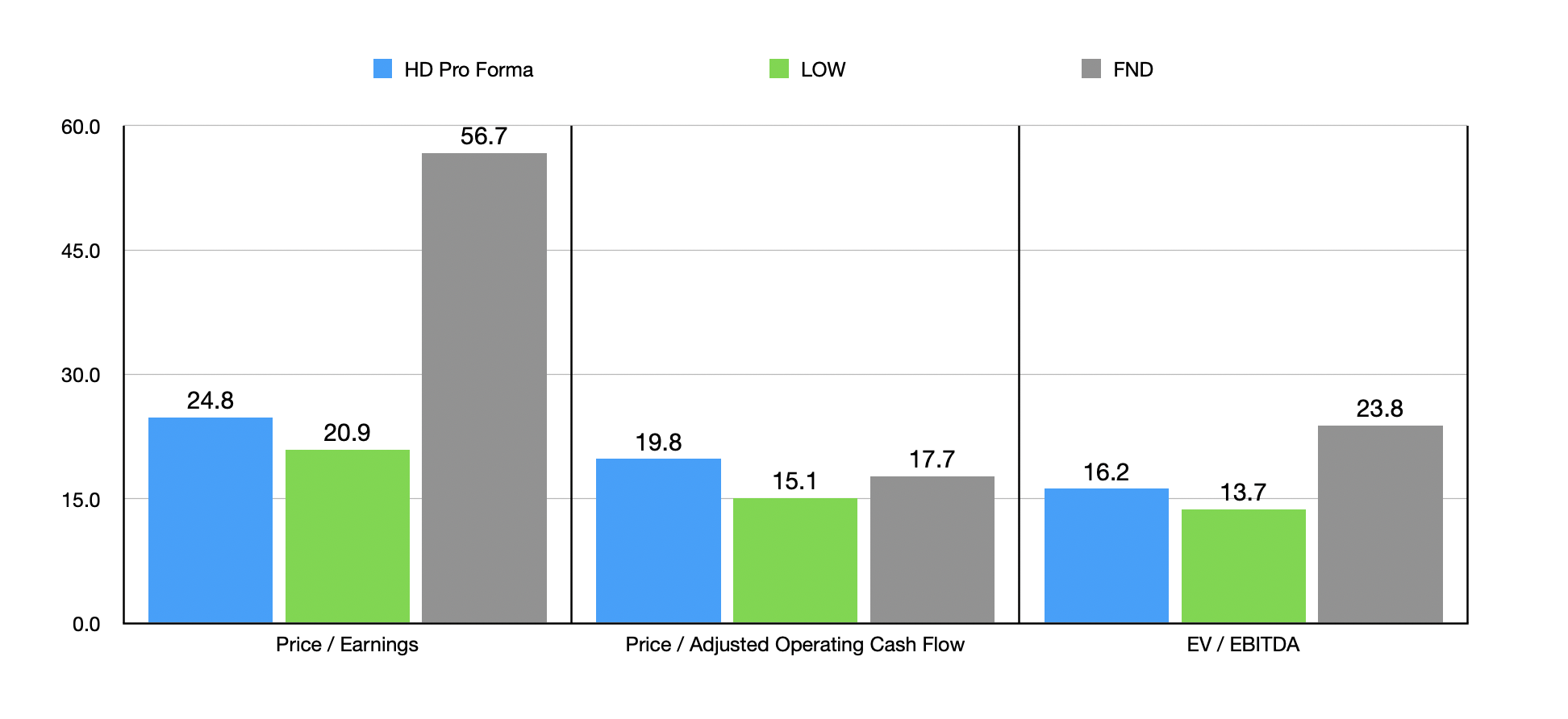

I truly did this sort of evaluation in my prior article. However now, we have now extra information. This consists of rates of interest incurred on the debt that The Residence Depot issued to make the acquisition. It additionally elements in money flows that The Residence Depot has generated up so far. Within the desk above, you may see what my calculations are for professional forma internet revenue, working money circulation, and EBITDA. You may also see the online leverage ratio of the corporate primarily based on present internet debt of $54.12 billion. Administration used a distinct measure for leverage that included an add-back for working leases and likewise added eight years’ price of these rents to the agency’s debt. In addition they checked out gross debt somewhat than internet debt.

Writer – SEC EDGAR Information

Utilizing these calculations, we will see within the chart above how The Residence Depot is valued on a professional forma foundation. That chart additionally compares The Residence Depot to 2 comparable companies, Lowe’s Firms (LOW) and Ground & Décor Holdings (FND). In every case, The Residence Depot is valued between the 2 firms. If you talk about the valuation on a standalone foundation, I’d argue that shares are a bit expensive. However once more, we’re coping with an trade chief with an ideal observe file. So I would not go as far as to say that the inventory is overvalued. Nevertheless, I’d argue that we’re getting fairly near that.

U.S. Census Bureau

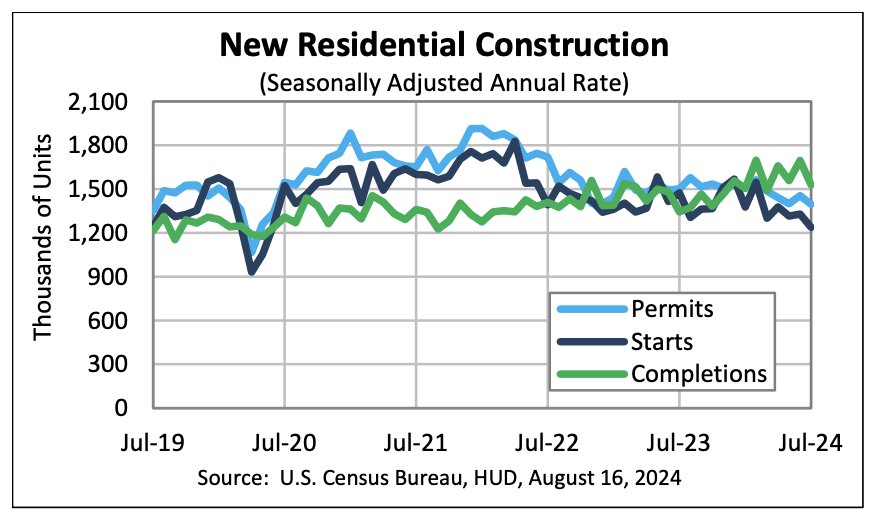

There are a few different elements that performed a job in my determination to be impartial to barely unfavourable in the case of The Residence Depot. For starters, financial situations will not be precisely constructive for the corporate. This 12 months, in line with one source, spending on enhancements, repairs, and reworking actions, ought to whole about $450 billion within the US. That is down from $481 billion spent in 2023. A unique source estimated the decline from $489 billion to $452 billion. However that is not all, the corporate does generate income from different actions as nicely. The residential housing house is one such instance. Although housing completions are up 12 months over 12 months, climbing 13.8% in July in comparison with the identical time final 12 months, housing begins and constructing permits are down. For the most recent month out there, which might be July, housing begins are down 16% in comparison with the identical time final 12 months. Constructing permits, in the meantime, are down 7%.

U.S. Census Bureau

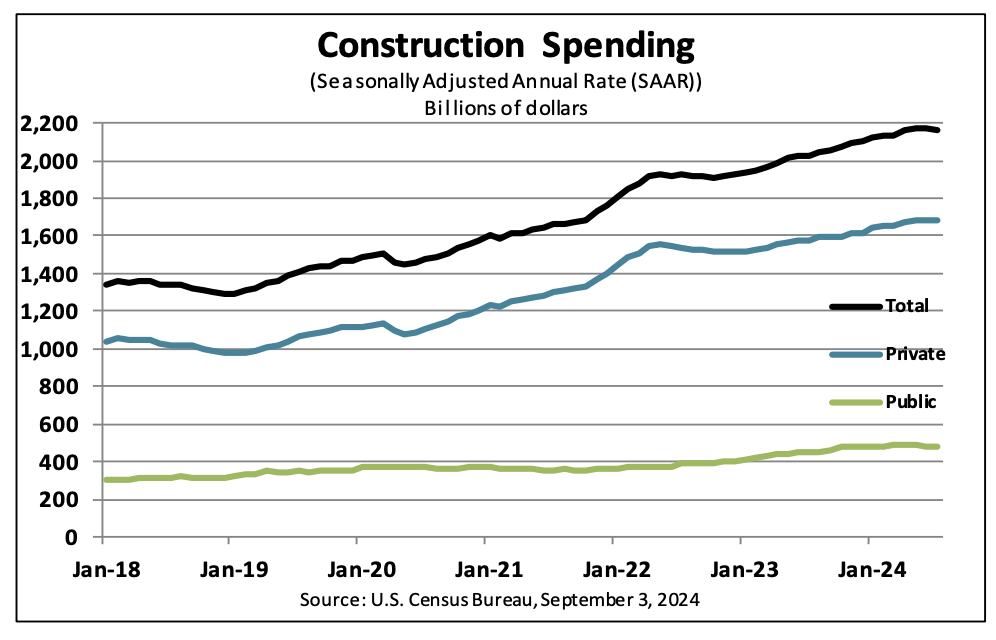

This isn’t to indicate that every part is dangerous. When speaking in regards to the building trade extra broadly, there may be some constructive information to contemplate. In July, whole building spending within the US was up 6.7% 12 months over 12 months. And for the primary seven months of 2024, it was up 8.8% in comparison with what it was on the identical time in 2023. On the entire, this can be a internet constructive. However with the opposite market information that I coated already, I’d say that the image for The Residence Depot is barely unfavourable on the entire.

Takeaway

Based mostly on the info offered, I nonetheless suppose that The Residence Depot is a high quality enterprise. However I do not suppose it is an ideal alternative to purchase into right now. The excellent news is that rate of interest cuts ought to ultimately end in an enchancment in its markets. Nevertheless, with uncertainty whether or not there will likely be a smooth touchdown, and with market situations pointing to extra weakening because the delayed impact related to begins and permits ultimately take a toll on completions within the housing market, I believe the corporate deserves a extra cautious strategy. That is very true contemplating how shares are priced, notably on an absolute foundation. Due to this, I’ve determined to maintain the agency rated a “maintain” for now.

[ad_2]

2024-09-13 13:29:10

Source :https://seekingalpha.com/article/4720953-staying-the-course-with-the-home-depot?source=feed_all_articles

{kind=link}

Discussion about this post