[ad_1]

Tetiana Soares/iStock by way of Getty Pictures

I first reviewed Sew Repair (NASDAQ:SFIX) again in February of this yr. For the reason that time of that article, the inventory is up 12%, however it’s nonetheless underperforming the S&P 500.

Regardless of the rise within the worth of the inventory since that preliminary article, I’m nonetheless bearish on the corporate and am not offered on the corporate’s turnaround story.

Let’s dig into the corporate’s newest quarter and focus on latest occasions.

Funding Thesis

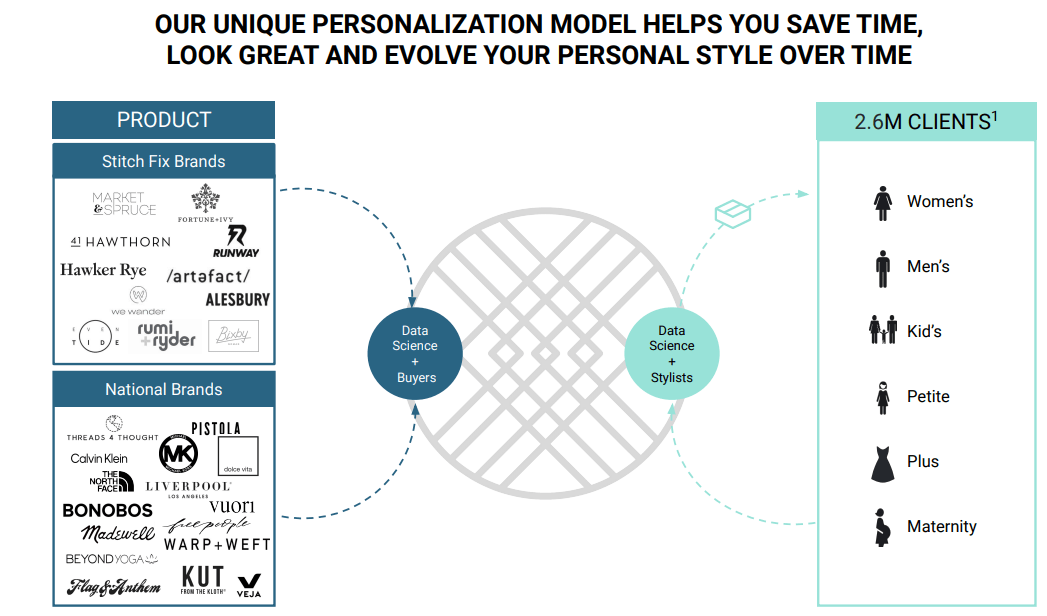

As beforehand famous, Sew Repair is a retail firm that gives personalised “fixes” to males, ladies, and kids. The corporate’s inventory rose to almost $100 a share throughout the COVID-19 pandemic earlier than cratering. The corporate has since modified CEOs a number of instances (together with dropping the corporate’s founder Katrina Lake) and have let go of quite a few staff.

At the moment, Sew Repair has roughly 2.6 million lively shoppers and offers clothes choices from widespread manufacturers together with Vuori, Calvin Klein, and a number of other others as you’ll be able to see beneath:

Sew Repair Investor Relations

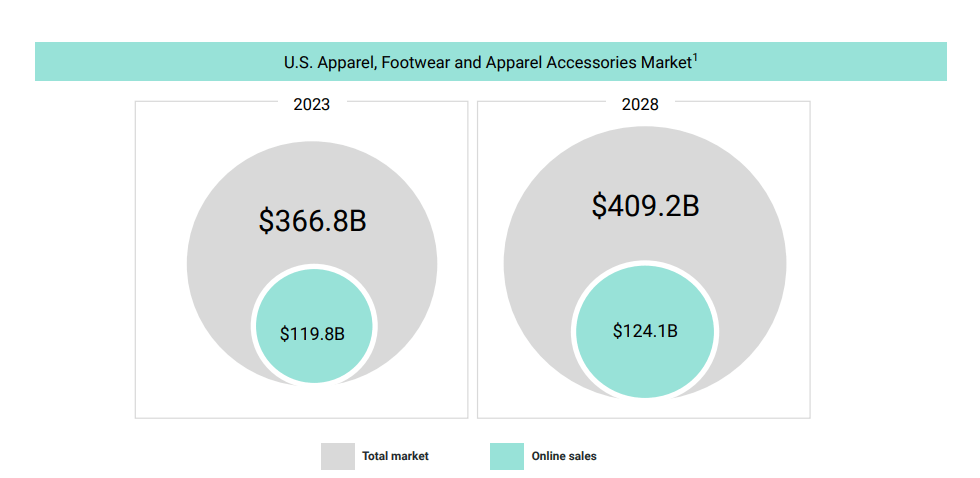

Sew Repair believes they’ve an addressable market of $124 billion associated to on-line retail as you’ll be able to see beneath which is a part of the general addressable attire market of roughly $409 billion:

Sew Repair Investor Relations

Nonetheless, Sew Repair’s consumer rely has been steadily declining leading to much less income era, which I’ll focus on subsequent.

Financials

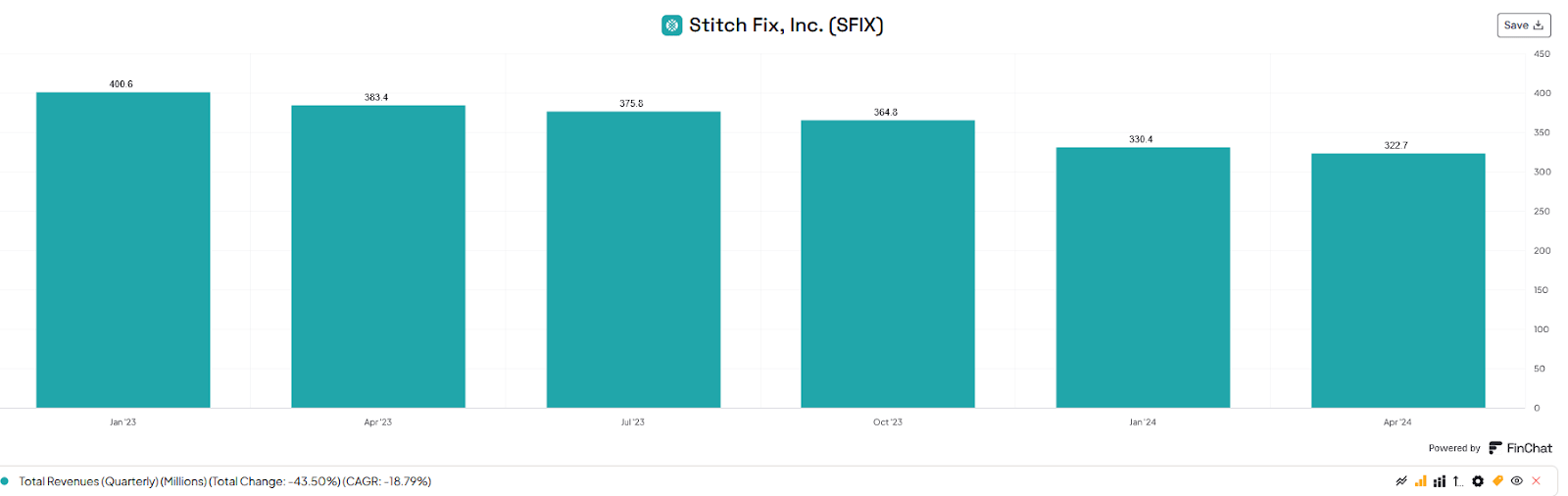

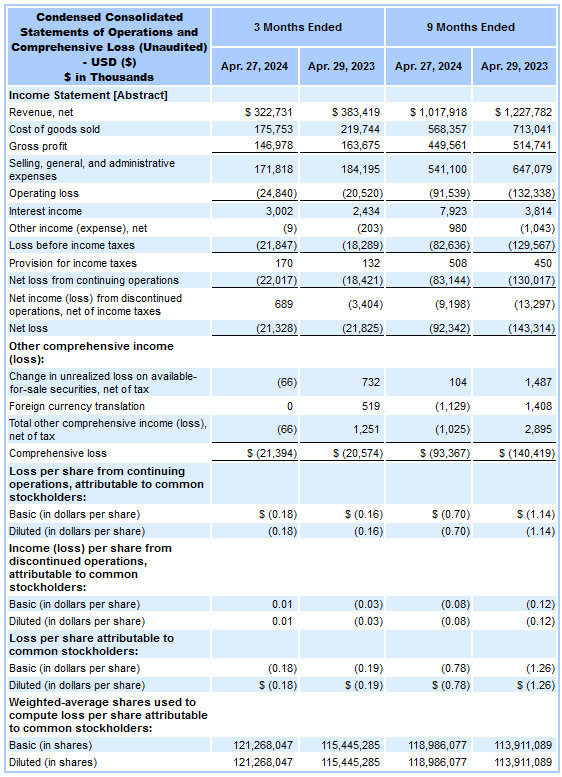

Income for Q3 of Sew Repair’s fiscal yr 2024 got here in at roughly $322 million, which is a lower of 16% in comparison with the identical quarter within the prior yr. The corporate’s income has continued to say no every of the final a number of quarters, as you’ll be able to see beneath:

Finchat.io

Sew repair now estimates they’ll earn between $312 to $322 million for the fourth quarter and revenues of $1.33 to $1.34 billion for the complete 2024 fiscal yr. This implies the corporate could have continued declines, as Sew Repair has seen full-year income figures repeatedly decline since 2021.

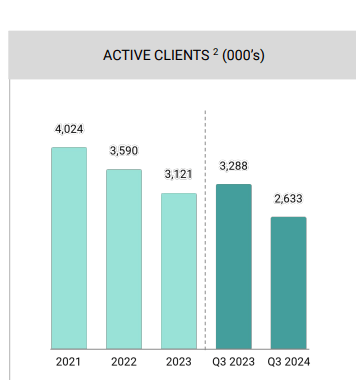

The corporate had 2,633,000 lively shoppers in Q3 2024 which is a 6% lower quarter-over-quarter and a 20% decline in comparison with the prior yr. Sew Repair continues to lose shoppers, as this graphic beneath illustrates:

Sew Repair Investor Relations

As you’ll be able to see beneath, the firm posted a web loss this quarter which could be very practically the quantity posted within the prior yr third quarter:

SEC.gov

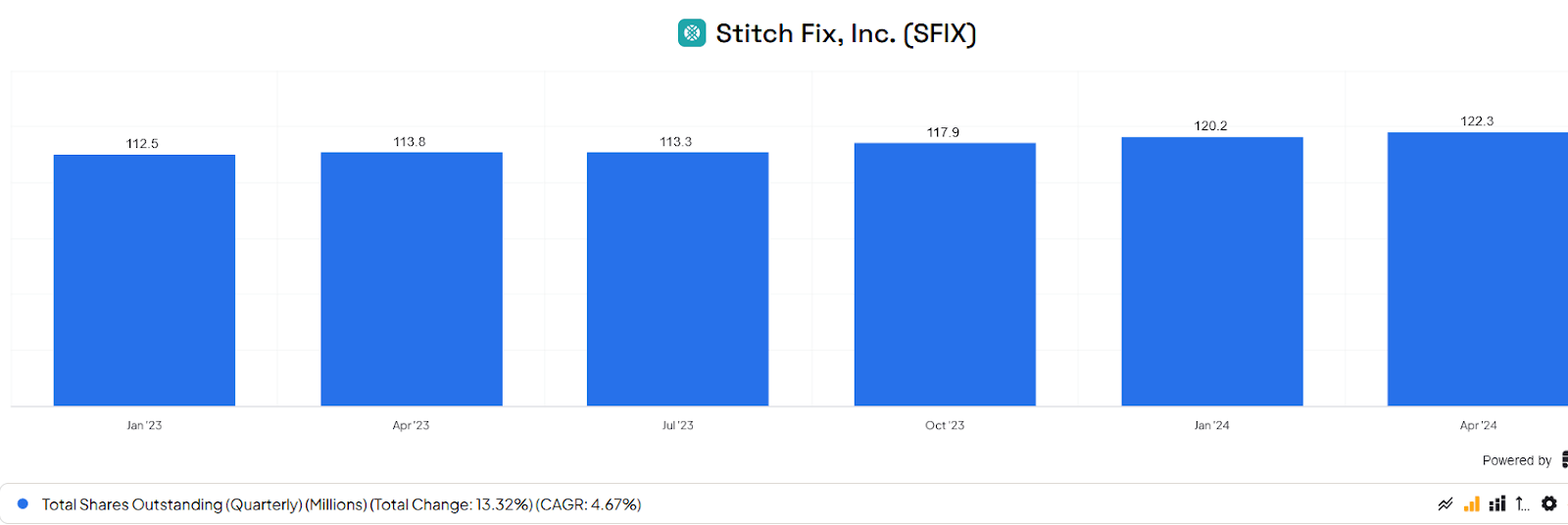

Nonetheless, the web loss YTD is smaller this yr because of a discount in SG&A bills. The corporate does proceed to dilute shareholders as you’ll be able to see the variety of shares excellent continues to rise:

Finchat.io

The corporate’s gross margins have been 45.5% for the quarter which is healthier than the prior yr and web income per lively consumer did enhance 2% which is a constructive signal.

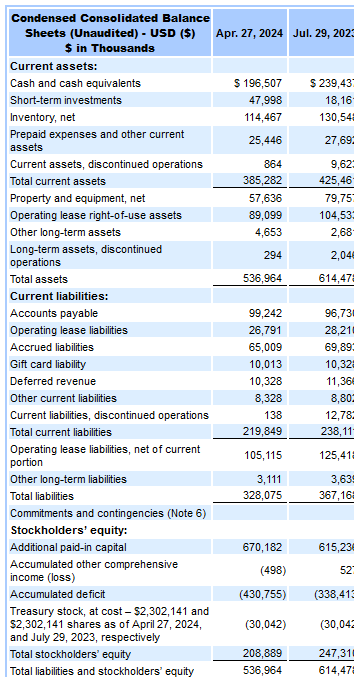

Sew Repair nonetheless maintains a superb stability sheet as you’ll be able to see beneath:

SEC.gov

The corporate has no long-term debt and sufficient present belongings to cowl all of their present liabilities.

AI Efficiencies and Stylist Focus

On Sew Repair’s most up-to-date earnings name, the corporate’s CEO, Matt Baer, famous quite a few operational enhancements to the enterprise. Utilizing AI and improved inner analytics, Sew Repair is discovering methods to get prospects to buy extra when a “repair” is ordered. On the decision, Baer went on to say, “Using our proprietary demand algorithms, we enhance the efficiency of Fast Repair’s by solely providing them to shoppers after we know the brand new fixes have a excessive probability of success. Inside three weeks of this variation, Fast Repair common order worth improved by 25%.”

Moreover, via using AI, the corporate is making higher purchase choices as Baer went on to state, “… We proceed to scale our AI stock shopping for software to tell a bigger set of shopping for choices. This software sifts via our proprietary transactional and consumer knowledge to foretell demand on the particular person fashion and consumer degree, empowering our merchandising crew to make shopping for choices which are simpler and environment friendly.”

It’s actually promising to see the organizational efficiencies gained via using AI, particularly if AI might help enhance the corporate’s possibilities to get shoppers to order extra per repair.

One other attention-grabbing merchandise on the earnings name was the dialogue concerning having stylists come extra into focus. When I’ve ordered fixes up to now, I’ve seen some stylists appear to have higher concepts than others. I believe it could be attention-grabbing if people might maybe collaborate with their stylist and even request a stylist in case you are actually having fun with the choices of a specific particular person. On the Q3 earnings name, Baer had this to say about stylists, “… Our stylists proceed to play a important half in our price proposition, and one thing that our shoppers have instructed us is that they need to get to know the stylist behind their fixes.”

I actually assume it is a good concept and consider this might assist Sew Repair retain prospects if patrons have been capable of develop some rapport with their stylists.

Valuation

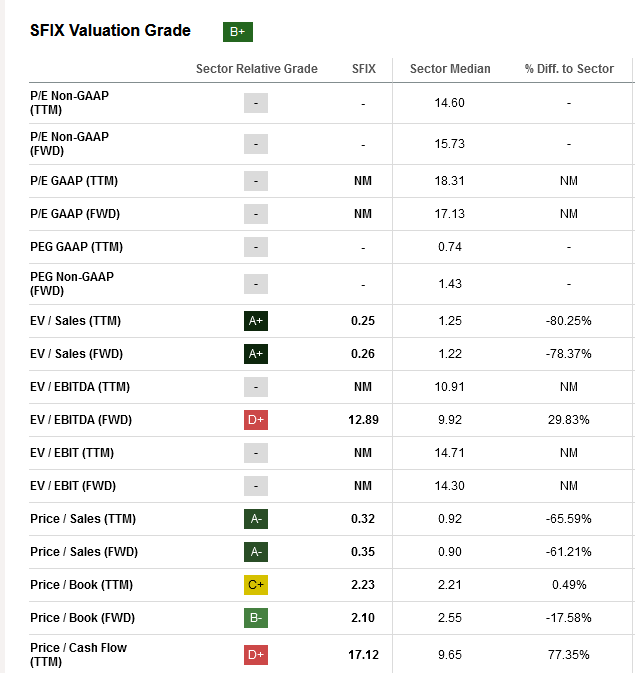

Sew Repair has a valuation grade of a “B+” at In search of Alpha:

In search of Alpha

Given Sew Repair is unprofitable, I believe worth to gross sales is the most effective metric valuation. Sew Repair does have a ahead worth ratio which is healthier than the sector median. Additionally, Sew Repair has a greater worth to gross sales in comparison with The RealReal, which has a comparatively shut market cap.

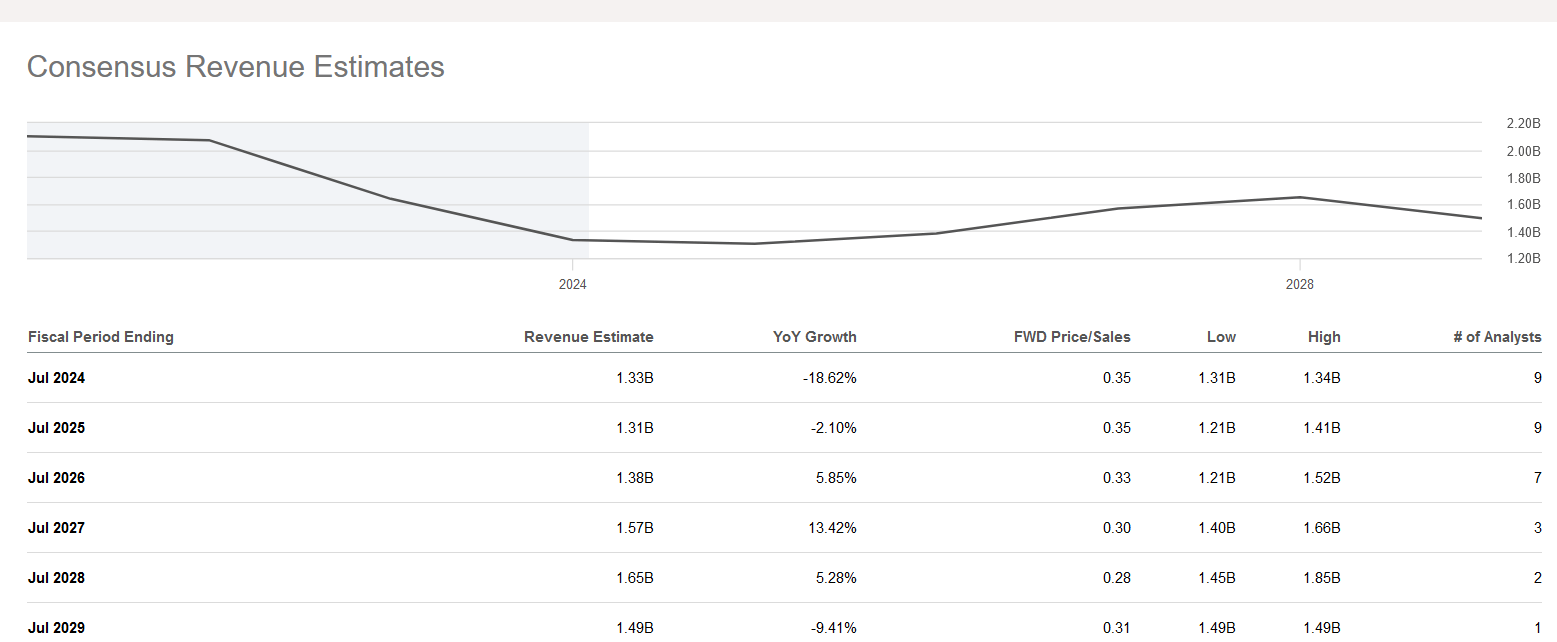

Though The RealReal (REAL) is projected to have income development within the coming yr (albeit minor development). As you see beneath, Sew Repair remains to be anticipated to battle over the following a number of years:

In search of Alpha

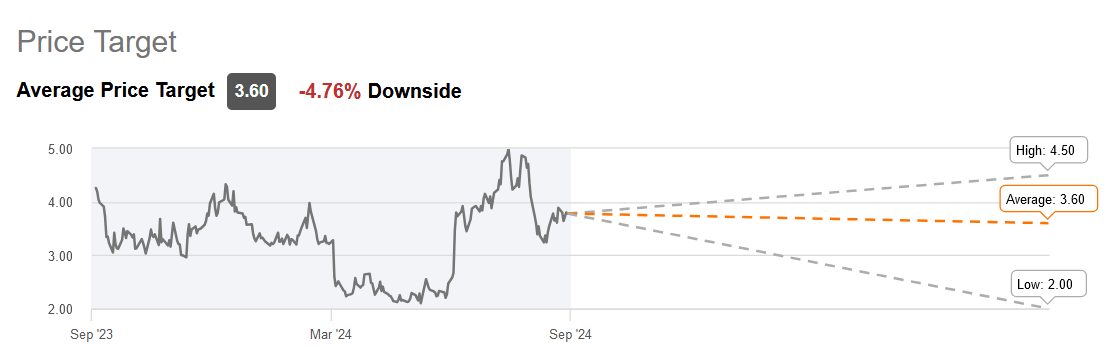

Moreover, Wall Avenue analysts see draw back for Sew Repair as the corporate has a median worth goal of $3.60:

In search of Alpha

I believe it is tough to say it is a worth inventory given the continual income decline and meager forward-looking estimates.

Conclusion

Sew Repair has some noteworthy positives, because the AI and analytic-related operational efficiencies appear to be serving to enhance consumer spend, and the corporate was capable of enhance gross margins for the quarter. Additionally, Sew Repair nonetheless maintains a superb stability sheet with no long-term debt.

Nonetheless, Sew Repair continues to see consumer losses, which is in flip resulting in continued income declines as the corporate is nowhere close to near attaining profitability. Additionally for buyers, Sew Repair continues to dilute shareholders as shares excellent have continued to rise for the previous couple of quarters.

Though the valuation is perhaps affordable, given the continued anticipated income losses, coupled with the damaging projections, I’m inclined to facet with Wall Avenue’s worth goal as I believe the corporate’s inventory worth will decline in the previous couple of months of this yr.

I’m not offered on the comeback story, as I nonetheless foresee a really lengthy highway to profitability for this firm.

[ad_2]

2024-09-03 09:41:21

Source :https://seekingalpha.com/article/4718613-stitch-fix-operational-efficiencies-not-enough-to-stop-revenue-decline?source=feed_all_articles

{kind=link}

Discussion about this post