[ad_1]

Richard Drury

In March this yr, I issued a relatively pessimistic article on the Schwab U.S. Dividend Fairness ETF (NYSEARCA:SCHD), recommending buyers keep away from going lengthy with this ETF.

The explanation was easy – the chance price was simply too large relative to the opposite excessive yielding funding performs on the market. In different phrases, by investing in SCHD, buyers must lock in an unattractive entry yield, the place even after contemplating the dividend development potential, there would nonetheless be a significant hole between whole present earnings streams between SCHD and a few defensive excessive yielders.

For the reason that dividend earnings profile of SCHD was not that attractive, going lengthy right here simply didn’t make sense, particularly contemplating that one of many key goals of this ETF is to fulfill yield-seeking buyers. As an illustration, SCHD is definitely not a capital development (value appreciation) automobile, because it doesn’t carry excessive development names that usually distribute no or very minimal dividends.

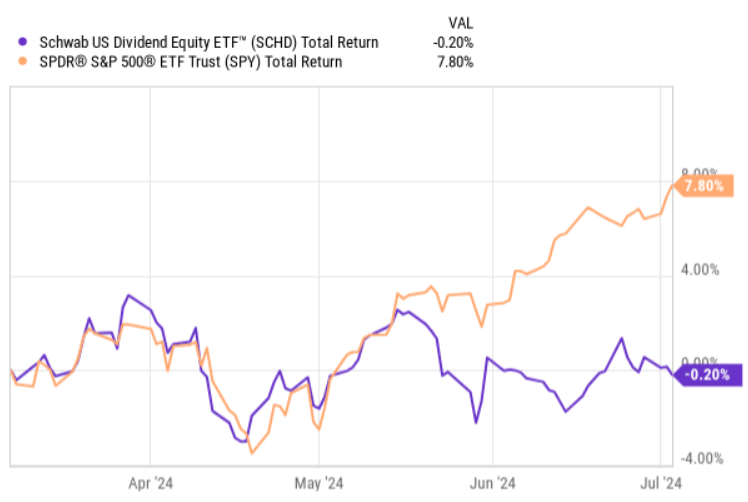

Trying on the chart under, we will see that after the publication of my article, SCHD has lagged behind the S&P 500 (measured on a complete return foundation). This has to do with the purpose that SCHD doesn’t put an enormous emphasis on the really high-flying shares, which don’t have any significant dividend insurance policies in place, and thus they fall out of the funding choice course of.

YCharts

Nonetheless, there are actually two basic elements which have led me to revise the thesis and kind a extra bullish view of SCHD.

Thesis evaluation

The first side is said to the improved attractiveness of SCHD’s dividend yield, which as illustrated within the chart under has gone up by ~ 30 foundation factors. But, I’d argue that the precise yield is greater than this if we shift the calculus from a TTM strategy to an annualized FWD yield primarily based on the collected distribution stage in the latest quarter.

In search of Alpha

By making use of this sort of strategy, we arrive at an implied / FWD dividend yield of ~ 4.2%, which is already an attractive stage from an absolute stage perspective. If we evaluate this yield with the U.S. 10-year YTM ranges we are going to now not see any significant distinction between these two yields.

Right here one may theoretically argue that it doesn’t make sense to base the dividend estimate on the current quarter, since over the subsequent couple of quarters the distribution ranges may sink. Whereas it’s true that the quarterly distribution ranges are unstable (i.e., not rising in a linear trend), we won’t discover any occasion the place SCHD has paid out a decrease dividend in This autumn than in Q2, and it isn’t that usually when the Q3 dividend quantity is available in at a decrease stage than within the prior quarter.

All in all, the yield element of SCHD has certainly develop into engaging even when we don’t bear in mind the ingredient of development, which is basically the important thing essence of this ETF. So, what buyers now successfully get is an ETF which supplies an honest yield from the beginning with a ~ 10% dividend development potential on a go-forward foundation, the place the underlying money flows are underpinned by strong and large-cap companies.

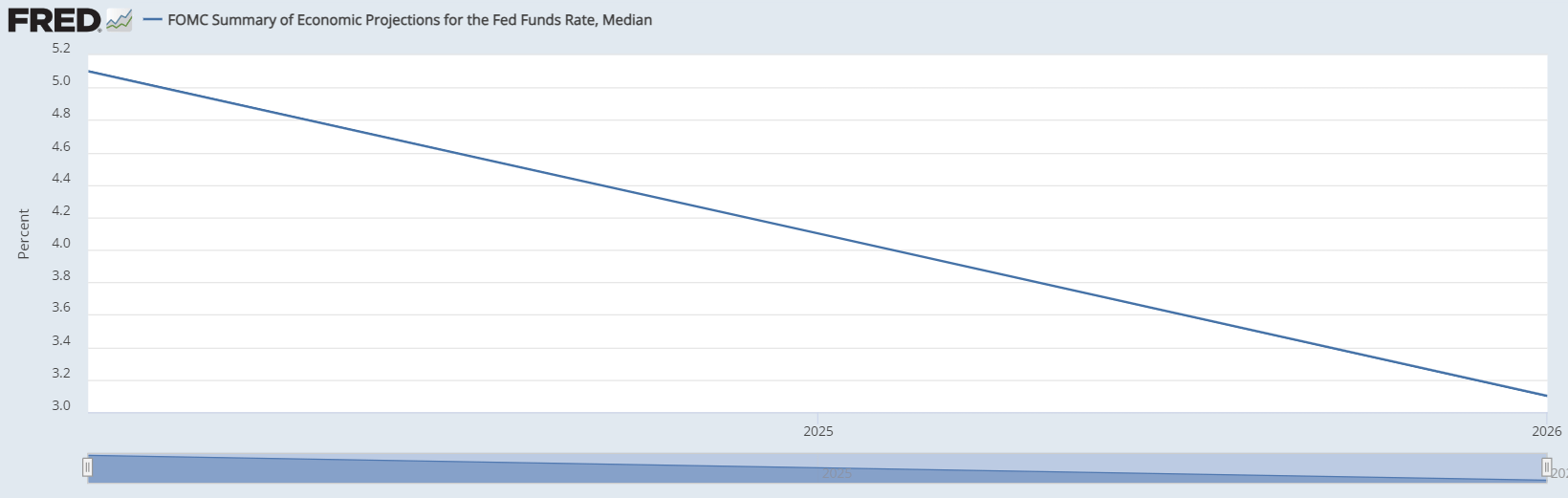

The second side, which renders SCHD an attention-grabbing ETF to think about, is the long run trajectory of the rate of interest ranges. Within the chart under we will observe two issues: (1) the Fed Funds fee is about to go down from right here and (2) the extent of rates of interest will nonetheless stay greater than the place they have been through the accommodative financial coverage part.

FOMC; St. Louis Fed

This suggests a few issues for SCHD. An important one is that I consider lowering rates of interest will inevitably influence development names in a extra favorable means than high-yielding belongings (or companies). This has to do with the length issue that’s extra pronounced for firms which have a back-end loaded money circulate profile. For SCHD’s investments, that is the case, as many of the investments might be deemed large-cap development names which have sturdy sufficient development prospects to accommodate double-digit dividend development.

Conversely, the devices that supply irregular yield ranges now are usually those which do not likely have stable prospects to extend their money era ranges sooner or later, thereby rendering the length issue comparatively smaller than for the extra growth-oriented names.

Which means as soon as the rates of interest begin to drop, the possible results on the asset costs will likely be extra favorable to SCHD’s holdings than, say, for standard high-yielding segments corresponding to BDCs and MLPs.

In the meantime, the FOMC dot plot additionally signifies that it’s unlikely that the SOFR will converge again to zero or extraordinarily accommodative ranges, which, in flip, ought to put a flooring on how low the dividend yield of SCHD may drop. On account of this, we may assume that the danger of buyers dealing with a reinvestment danger (from the angle of low incremental yield ranges on the reinvested capital) is relatively distant.

The underside line

As lots of my followers have most likely observed, I’m an enormous fan of high-yielding devices (with common yields of seven – 10%), which explains circa 90% of my portfolio.

Whereas a while in the past I used to be comparatively skeptical of SCHD – principally from the chance price perspective – the rise in SCHD’s yield coupled with a extra pronounced ingredient of capital appreciation potential that may be related to lowering rates of interest makes me change my stance.

For my part, at this specific second, the Schwab U.S. Dividend Fairness ETF presents a compelling entry level even for high-yielding buyers who’re keen to think about including some investments that supply a little bit of a decrease yield from the beginning, but additionally have a stronger dividend development potential that might comparatively rapidly offset the foregone earnings potential.

[ad_2]

{kind=link}

Discussion about this post