[ad_1]

heckmannoleg/iStock through Getty Photographs

Introduction

Sally Magnificence Holdings (NYSE:SBH) is a small-cap inventory, famous for offering magnificence merchandise throughout the globe to each DIY clients in addition to skilled stylists/salons (in North America, they function the biggest distributors {of professional} hair coloration and care); the majority of those magnificence merchandise embrace hair coloration and hair care-related merchandise, with each classes accounting for properly over 80% of group gross sales (in addition to hair-related materials, SBH additionally offers styling instruments and nail merchandise).

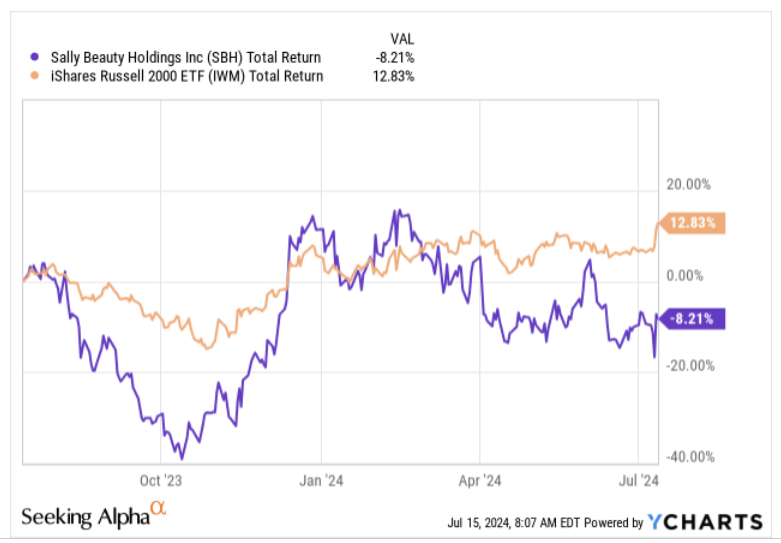

Over the previous 12 months, the market hasn’t fairly taken a flowery to this small-cap discretionary inventory, and it has ended up dropping 8% of its worth, at the same time as different small-caps have delivered constructive returns throughout the early teenagers.

YCharts

Trying forward, we really feel there could possibly be a change within the narrative, on account of the next causes.

Monetary Outlook Seems Higher And Ahead Valuations Look Low-cost

During the last 4 quarters, SBH has continued to face dwindling topline progress on a YoY foundation, and by the appears of it they may shut the present fiscal barely decrease (by – 0.5% YoY). But contemplating the H1 efficiency, the place the topline was down by -2% on common, the FY anticipated progress decline would recommend constructive YoY progress of 1% in H2.

SBH’s BSG (Magnificence Programs Group) section which offers omnichannel distribution companies for hair salon professionals throughout North America, has already began seeing constructive momentum for 2 quarters (in Q2, comparable transaction gross sales had been up by 2%), and may gain advantage from simpler comps because the hair care headwinds from the earlier years received’t be current in H2.

Then, SBH’s Sally Magnificence Section [SBS], which accounts for 56% of group income, 64% of working earnings, and has a greater margin profile ( 16.8% working margin vs BSG’s margin of 11.4%) has been going through some challenges on account of the macro setting. Basically this section caters extra to the DIY low-income buyer, and right here, on account of inflationary pressures, these clients have been leaning extra in direction of promotions, thus impacting the common unit costs. SBS too has been contributing much less to the gross sales combine in H1 and this has ended up impacting the general group margin.

Nonetheless final week’s inflation report was very encouraging, with the CPI seeing its first drop since Might 2020, following an unchanged stance within the following month. Additionally within the 12 months by way of June, the CPI witnessed its smallest achieve since June 2023; broadly the important thing takeaway right here is that inflation pressures are properly and really abating, and we may additionally see some rate of interest cuts in September, which might enhance family budgets, and immediate a number of the low-income section to interact in additional discretionary gross sales.

Even when topline dynamics could possibly be gradual to select up (SBH follows a September year-ending calendar), notice that administration has put in place a “ Gas for Development” program to generate value financial savings in distribution and delivery, which can lead to $20m value of advantages within the present fiscal and even an excellent larger run price of $50m p.a. throughout FY25 and FY26, taking the mixture whole to $120m.

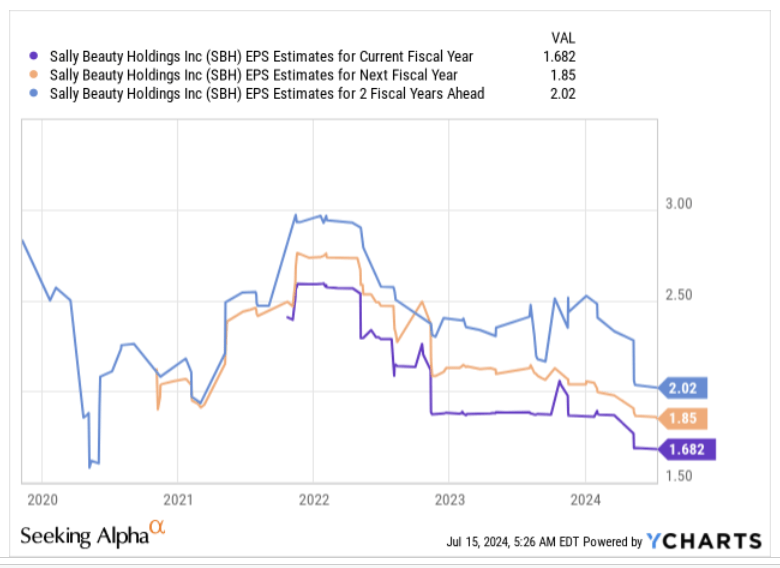

YCharts

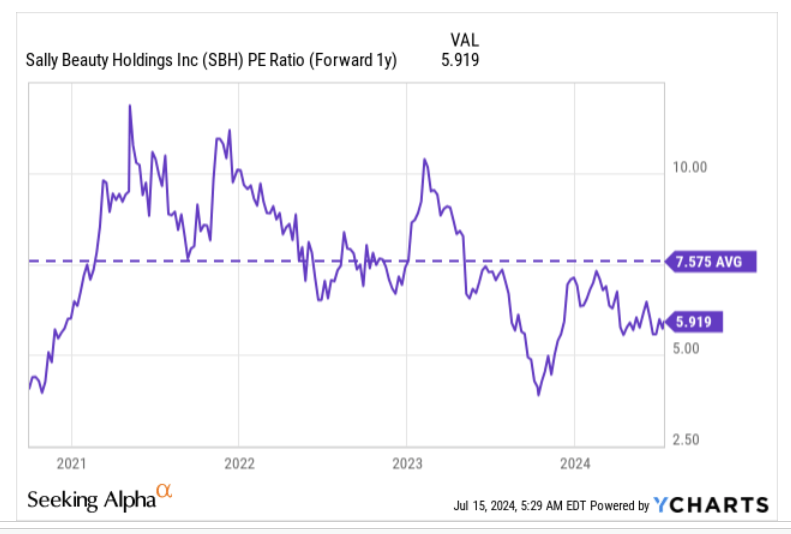

All these components may lead to very strong bottom-line progress of double-digit CAGR for the subsequent two years (primarily based on consensus estimates above). Provided that it is a enterprise that might generate double-digit earnings progress, we really feel the present ahead P/E a number of of lower than 6x appears very alluring.

YCharts

Be aware additionally that the present P/E a number of interprets to a 22% low cost to its rolling 5-year common of seven.57x

Enhancing Money-Technology Prospects Bode Nicely For Leverage Decline And A Potential Choose Up in Buybacks

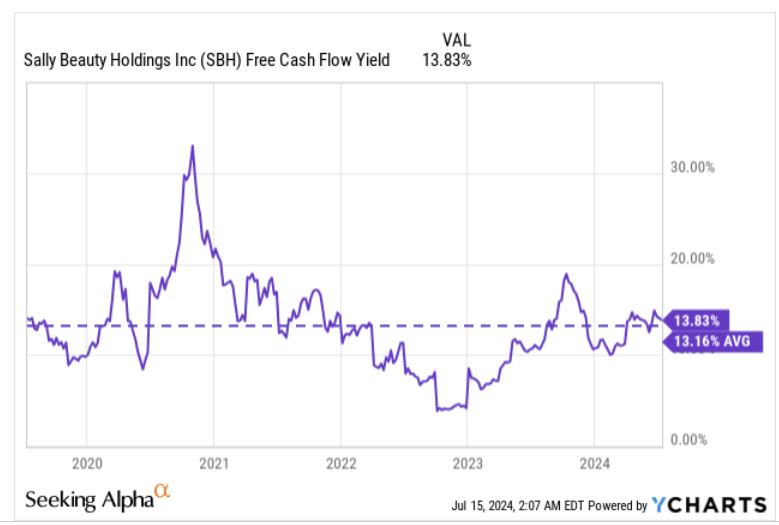

One of many extra commendable traits of the SBH working mannequin is that it has been capable of constantly facilitate constructive free money move yearly (though the EBITDA to FCF conversion has dipped in recent times from a earlier 6-year common of 48% to 23% over the past couple of years).

On the present market-cap, notice that the SBH inventory already yields fairly a compelling FCF yield of practically 14%, which can also be marginally higher than its 5-year common a number of. With two extra quarters of outcomes to go earlier than SBH wraps up its fiscal, we imagine upside dangers to the FCF are wanting much more possible.

YCharts

As inflationary situations dip and buying momentum choose up, that is anticipated to go away a good impression on the stock buildup within the retail channels, which may immediate SBH’s personal stock place to begin making southbound strikes.

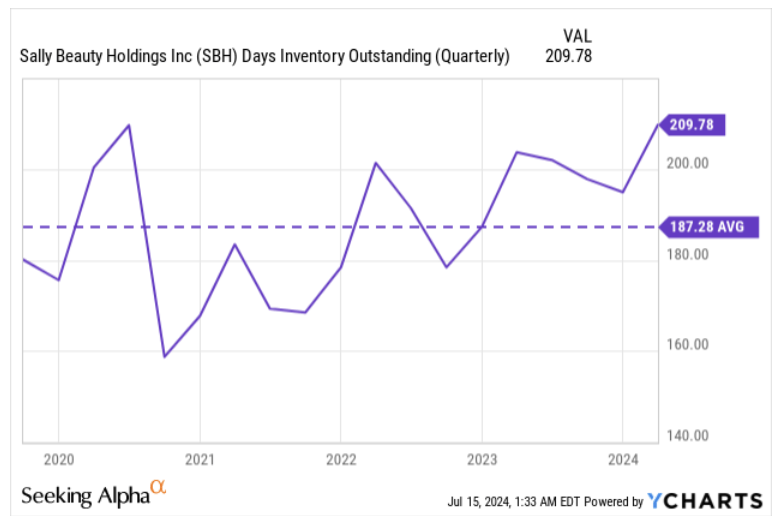

Be aware that SBH’s stock takes up an enormous chunk of its property at 36%, and a few of that is pushed by the excessive stock it must constantly preserve, to cater to the BSG section. Purchasers right here primarily include salon professionals throughout North America who should cope with capital constraints and restricted warehouse and shelf area, thus prompting them to comply with a JIT (Simply-In-Time) stock coverage.

But nonetheless, we really feel there’s loads of scope for SBH to rightsize its stock place, notably with the SBS facet of the enterprise, as the general present days in stock excellent is at 5-year highs and round 12% greater than its 5-year common.

YCharts

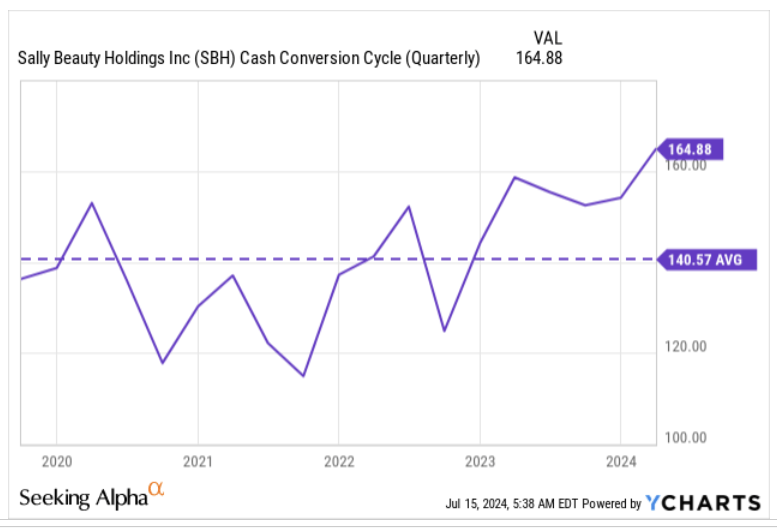

It isn’t simply the stock facet of issues that gives the potential for enchancment; SBH’s total money conversion cycle, which measures the variety of days that money is tied up with working capital, at present stands at nearly 165 days, and at 5-year highs. Even this might imply revert as it’s at present 17% greater than its long-term common.

YCharts

All in all, notice that regardless of solely averaging lower than $45 of working money move (OCF) per quarter in H1-24, SBH administration believes they’ll nonetheless ship $240m of OCF for the entire 12 months; this could suggest a sizeable uplift within the OCF run price per quarter to properly over $75m, giving a helpful fillip to free money move prospects.

With $100m of CAPEX budgeted for the 12 months, SBH could possibly be on the right track to generate $140m of constructive FCF for this 12 months, implying an enormous step up in FCF technology for H2 to the tune of $97m (which is greater than double the run price seen in H1 of $43.2m). What this implies is that SBH’s present FCF yield which is already above common may see a significant uplift.

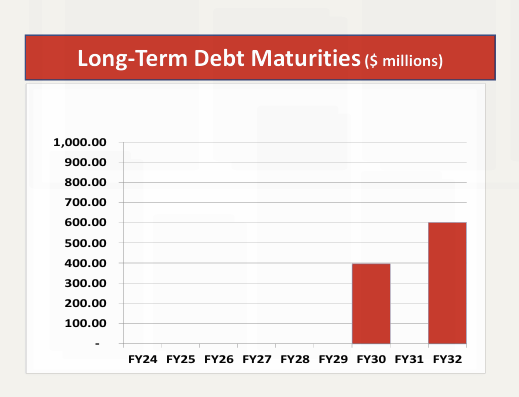

With wholesome FCF technology on the playing cards, SBH is well-positioned to convey down its leverage ranges to its goal vary of 1.5x-2x. On the finish of H1 it stood at 2.2x; even, in any other case, SBH just isn’t below any urgent want to take action because it not too long ago re-financed it debt and stretched the general maturity profile of its debt ($680m of senior unsecured notes with a coupon of 5.58%, which had been due in 2025, had been changed by 6.75% senior notes due solely in 2032). Because of this, SBH doesn’t have any main debt maturities for the subsequent 6 years.

March 24 Presentation

So even when FCF just isn’t meaningfully used to scale back the extent of gearing, SBH can even step up the tempo of its share repurchases, because it nonetheless has round $540m of share repurchase authorization remaining, which primarily represents round 5% of the present market-cap.

Closing Ideas- Good Danger-Reward On The Charts

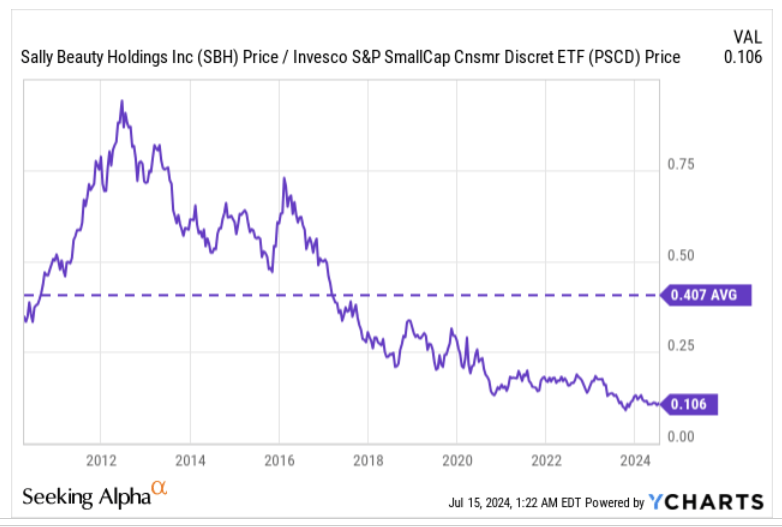

We have talked about earlier, how SBH’s valuations look grime low-cost, and this could pique the curiosity of bargain-hunters, notably those that imagine within the idea of mean-reversion within the markets. The picture beneath measures SBH’s relative energy (RS) versus its friends from the small-cap discretionary area, and proper now, the RS ratio is at inordinately low ranges, or solely about one-fifth its long-term common. Given SBH’s favorable valuation quotient, we might count on funds from some over overbought counters of small-cap discretionary to move into SBH going ahead.

YCharts

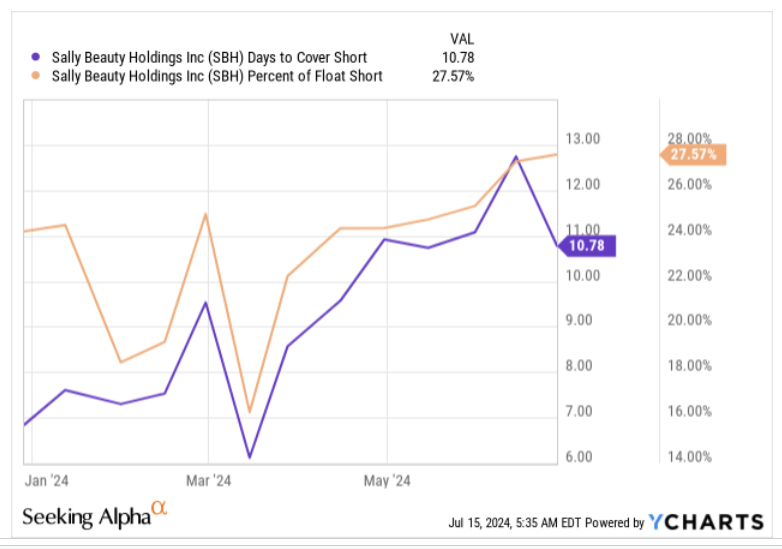

SBH can also be a kind of names that might profit from a powerful quick squeeze, as not solely is the share of float fairly heightened at 27%, however you even have a really excessive days-to-cover ratio throughout the double-digit threshold, which received’t make the exit of short-sellers simple to facilitate.

YCharts Investing

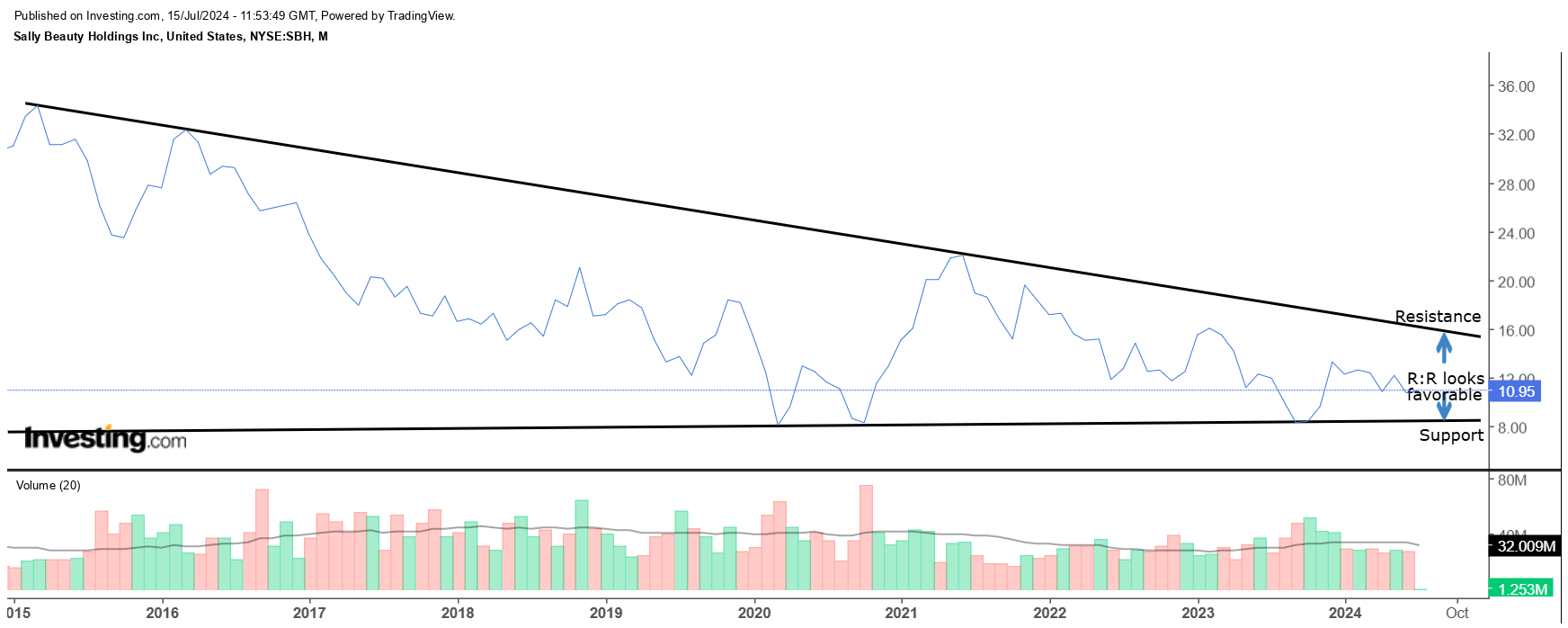

Lastly, if we take a look at SBH’s month-to-month actions over the past decade or so, notice that it may be encapsulated throughout the two black traces; primarily a downward sloping resistance which is at present at across the $15.5 ranges, and a flattish help at across the $8.4 ranges. Given the place the value is at present perched ($11 ranges), the risk-reward for a protracted place appears slightly engaging at over 1.7x.

[ad_2]

2024-07-16 02:21:17

Source :https://seekingalpha.com/article/4704192-sally-beauty-3-reasons-to-buy-this-small-cap-discretionary-stock?source=feed_all_articles

{kind=link}

Discussion about this post