[ad_1]

Matteo Colombo

Funding replace

Since my June publication on RadNet, Inc. (NASDAQ:RDNT) reiterating it a purchase the inventory is +10% and we noticed one other set of sturdy quarterly numbers in its Q2 FY’24 earnings. Right here I am going to run by my evaluation of the quarter, up to date modelling, and reinstated my subsequent value goal to $72 per share, nonetheless eyeing long-term aims of $95 per share within the base case.

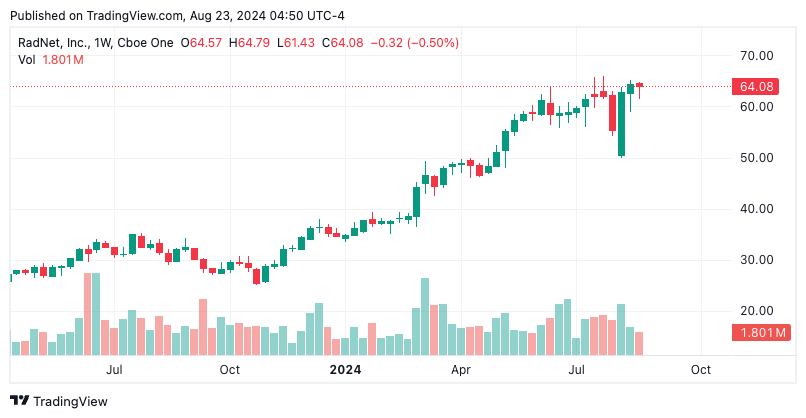

Determine 1.

Tradingview

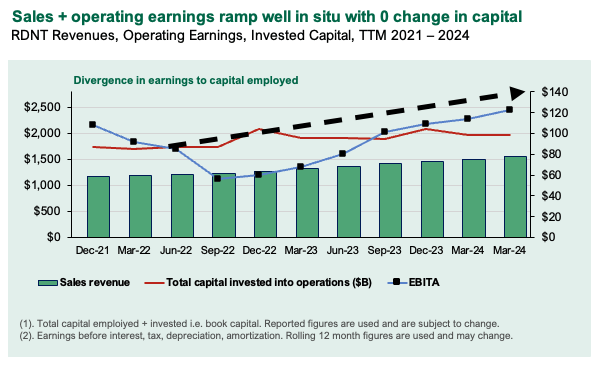

RDNT is evident proof that the market pays very shut consideration to how companies make the most of capital by taking money flows produced by their operations and redeploying them again into the enterprise to supply extra earnings energy (outlined right here merely as extra income in greenback phrases).

What this reveals is how an organization is creating financial worth for its shareholders – not simply the day-to-day or 12 months two 12 months machinations within the inventory market. Precise financial worth. The query is how a agency creates financial worth – it does so by investing cash and producing income on these investments at greater charges of return than what buyers can usually obtain elsewhere. Furthermore, it’s when a enterprise can develop gross sales + working earnings with out the necessity to commit piles of money to engender this progress.

Such is the case for RDNT, the place post-tax earnings are +$0.81/share since Q1 FY’23, however the enterprise runs on ~$5.33/share much less working capital it did again then. As such, you’ll be able to see the ‘cross’ in working earnings to invested capital in Determine 2, illustrating how the enterprise is producing considerably greater earnings off the identical stage of investments as 2yrs in the past.

Internet-net, I reiterate RDNT a purchase.

It is a identify I do know tremendously effectively, having coated it extensively right here on Searching for Alpha. See earlier analyses right here:

Determine 2.

Firm filings

Q2 FY’24 earnings breakdown

RDNT put up $460mm of gross sales in Q2 FY ‘24 (+14% YoY). It pulled this to adjusted EBITDA of $72mm, +20% YoY. Development was underscore by upsides in its imaging heart and digital well being segments.

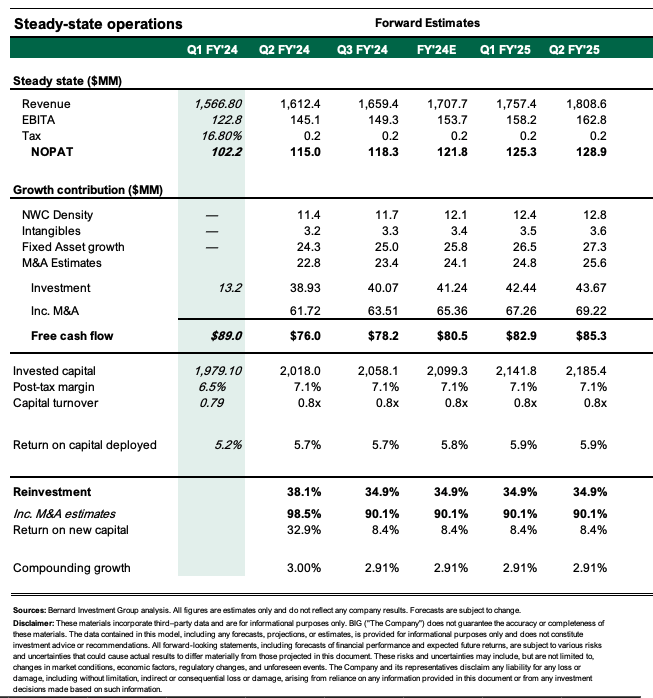

Administration revised FY 24 steering to the upside and now expects revenues of $1.7 billion on the prime finish, pulling to working earnings of $267mm. It appears to be like to speculate $145mm in capital expenditures, up from $135mm beforehand. My numbers name for the corporate to supply $1.7 billion in gross sales this 12 months, and $121mm in post-tax earnings. I see this stretching up past $1.8 billion by FY’25 (see Appendix 1).

Because the divisional highlights, my takeouts had been the next:

-

Imaging heart revenues had been $444mm, +13% YoY. Administration mentioned that utilization of its diagnostic imaging property was greater, reflecting progress in ambulatory websites, and it is a development I’ve been seeing by many healthcare service suppliers of late. What is occurring is there’s a shift away from hospital-based alternate options to area of interest operators reminiscent of RDNT. It is a tailwind in my view and it’s a aggressive benefit that can widen financial situations tighten. Individuals nonetheless search for worth of their imaging companies, and that is mirrored by referring accounts as effectively. Critically, superior imaging revenues had been +150bps YoY reflecting this.

-

The digital well being enterprise grew 36% over the 12 months and put up $16mm in income. Earnings had been +135% to $3mm for the quarter. Development was underlined by the AI-powered breast most cancers initiative, which noticed progress of 137% over the 12 months. Administration additionally mentioned the improved breast most cancers diagnostic and mammography (“EBCD”) providing is nearly full. It reported that adoption charges are excessive, per the earnings name: “Adoption charges proceed to rise and now exceed over 40% on the East Coast and are averaging near 30% on the West Coast, the place we now have extra lately carried out this system.”

-

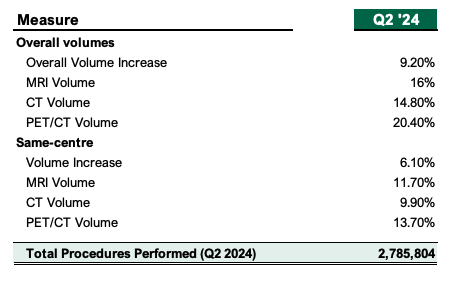

Total process volumes elevated 9.2% YoY, with imaging procedures exhibiting upsides throughout all classes, MRI, CT, and PET/CT respectively. MRI volumes expanded 16%, while the opposite two segments had been up 15% and 20% YoY respectively. In the meantime, same-center quantity will increase had been +600bps, with same-center MRI, CT, and PET volumes up 12%, 10%, and 14% respectively (Determine 3). Total, it carried out 2.78mm procedures in the course of the quarter.

Determine 3.

Firm filings, Writer

Yr to this point it has opened 5 new services, and has one other 6 scheduled for opening by FY ‘24. It has 15 initiatives in improvement, a lot of which can be opened in FY’25. There’s a 50-50 break up between joint-venture/wholly-owned facilities on this pipeline. It had 398 facilities below its books by the top of Q2, and 37% of those are inside well being system partnerships giving them a structural aggressive benefit in my opinion.

Valuation upsides stay firmly in view

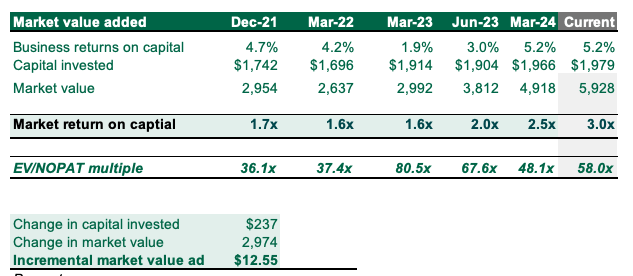

RDNT is now a 3x EV/IC enterprise after persevering with the economics mentioned earlier on this report. This has stretched up considerably from ranges of ~1.7 X in FY 21. Administration has plowed again $237mm again into the working base of the enterprise, and this has been valued at $2.9 billion in further market worth.

As such, each $1 administration has put again to work within the firm since FY’21 is valued at $12.55 available in the market. That is tremendously engaging to the funding debate, as my funding thesis hinges on this firm opening as many services as potential – in different phrases, reinvesting as a lot of its income again into the enterprise to broaden its working asset base and working earnings. At a 3x a number of, that is extremely engaging.

Determine 4.

Writer

Valuation insights

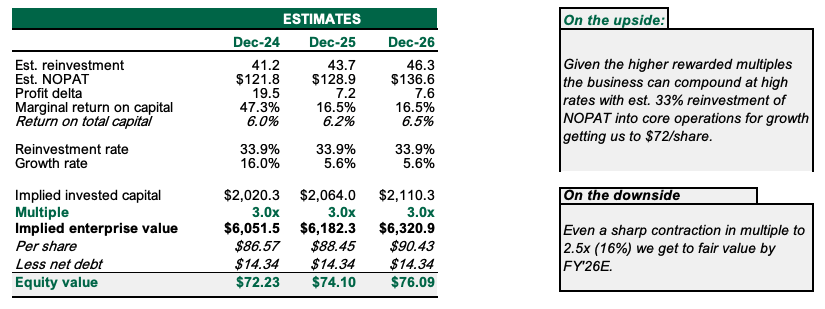

- Given the upper rewarded multiples, the enterprise can compound at excessive charges with est. 33% reinvestment of NOPAT into core operations for progress, getting us to $72/share. On the draw back, even with a pointy contraction in a number of to 2.5x (16%), we get to honest worth by FY’26E.

Determine 5.

Writer

- The compounding capacity at this stage of valuation a number of is very engaging. Beneath my estimates for FY’26E (see: Appendix 1) my view is there’s a excessive propensity to compound our earnings energy in proudly owning this enterprise over that point.

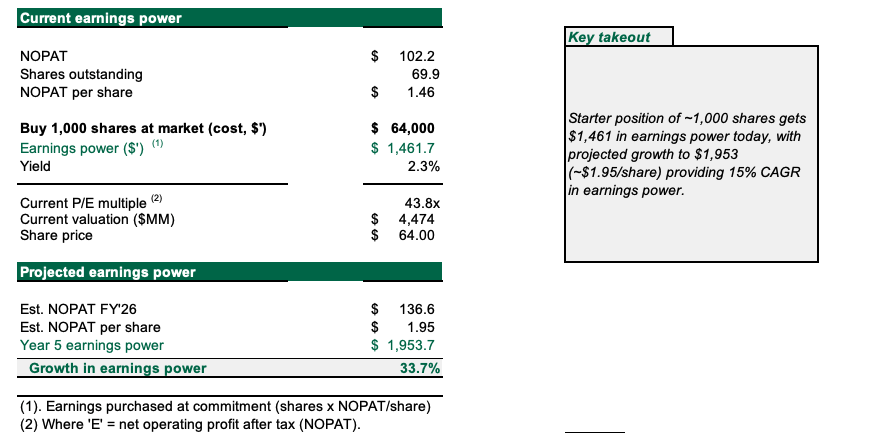

- A starter place of 1,000 RDNT shares will get us $1461 in earnings energy at this time at a value of $64,000 (Determine 6). My estimates venture this to compound by 15% per 12 months out to 2026, growing cumulative incomes energy by 33.7% to $1.95 per share. This helps a purchase ranking – it outpaces our hurdle price of 12% – the place we assign a hypothetical funding that may reinvest 100% of its earnings at this 12% determine. My assumptions – which don’t hyperlink the corporate to market worth, solely display earnings energy – corroborate that RDNT can surpass this threshold. This helps a reiterated purchase ranking.

Determine 6.

Writer’s calculations

Dangers to thesis

Draw back dangers to the thesis embody 1) gross sales progress lower than 10%, as this reduces the valuation, 2) administration slowing the tempo of recent retailer openings such that earnings don’t compound at an analogous price, 3) new retailer openings not pulling their financial weight and underperforming the legacy base, and 4) the broader set of macroeconomic dangers that have to be factored in proper now, together with inflation, charges and geopolitical dangers.

Buyers should acknowledge these dangers in full earlier than continuing any additional.

In brief

RDNT stays a purchase in my opinion given the elemental economics on show. Administration continues to plow our funds again into new services, rising working earnings with little or no change in incremental capital employed. My view is the enterprise is value ~$72 a share at this time, with compounding capacity as much as $95 per share, my beforehand said estimates of the intrinsic value of this enterprise. Internet-net, reiterate purchase.

Appendix 1.

Writer

[ad_2]

2024-08-24 02:23:00

Source :https://seekingalpha.com/article/4716835-radnet-growth-in-operating-earnings-off-very-little-incremental-capital?source=feed_all_articles

{kind=link}

Discussion about this post