[ad_1]

bjdlzx

Permian Sources (NYSE:PR) has been quickly rising. This administration has been a bit extra formidable with its acquisitions than another managements that I comply with. Not solely has administration discovered accretive acquisitions. But it surely has discovered acquisitions that it may materially enhance (typically large time) after the acquisition. The outcome has been a hovering inventory value that is still a discount even after a substantial quantity of appreciation.

The final article famous but one other discount coming onboard:

Permian Sources Acquisition From Occidental Petroleum (Permian Sources Second Quarter 2024, Earnings Convention Name Slides)

The factor that continues to amaze me concerning the bargains this administration finds is proven within the slide above. The acquisition will mix a number of disparate holdings into one giant, contiguous place that will likely be much more environment friendly and sure far more worthwhile than all of the components have been earlier than this deal got here alongside. Not solely is the deal “bolt-on” it’s extra like “BOLT-ON” with a variety of gusto. This needs to be the most effective offers of its sort within the present fiscal yr.

Often, comparatively giant offers like this mix a number of disparates and usually small components. Clearly, this one goes to do much more than that.

Earnings

The earnings have been simply launched. The issue is that the reasonably vital Earthstone Power acquisition remains to be being digested whereas, one more acquisition is underway. This makes any comparisons or evaluation very difficult.

Clearly, the debt scores companies are happy sufficient to boost the debt score of the corporate’s money owed. However that’s hardly reassuring to shareholders.

Most likely some-time is required for the Earthstone Power acquisition to be optimized earlier than worrying an excessive amount of concerning the quarterly comparisons. They’re price studying “simply in case” and to search out main points. However that’s about it, actually.

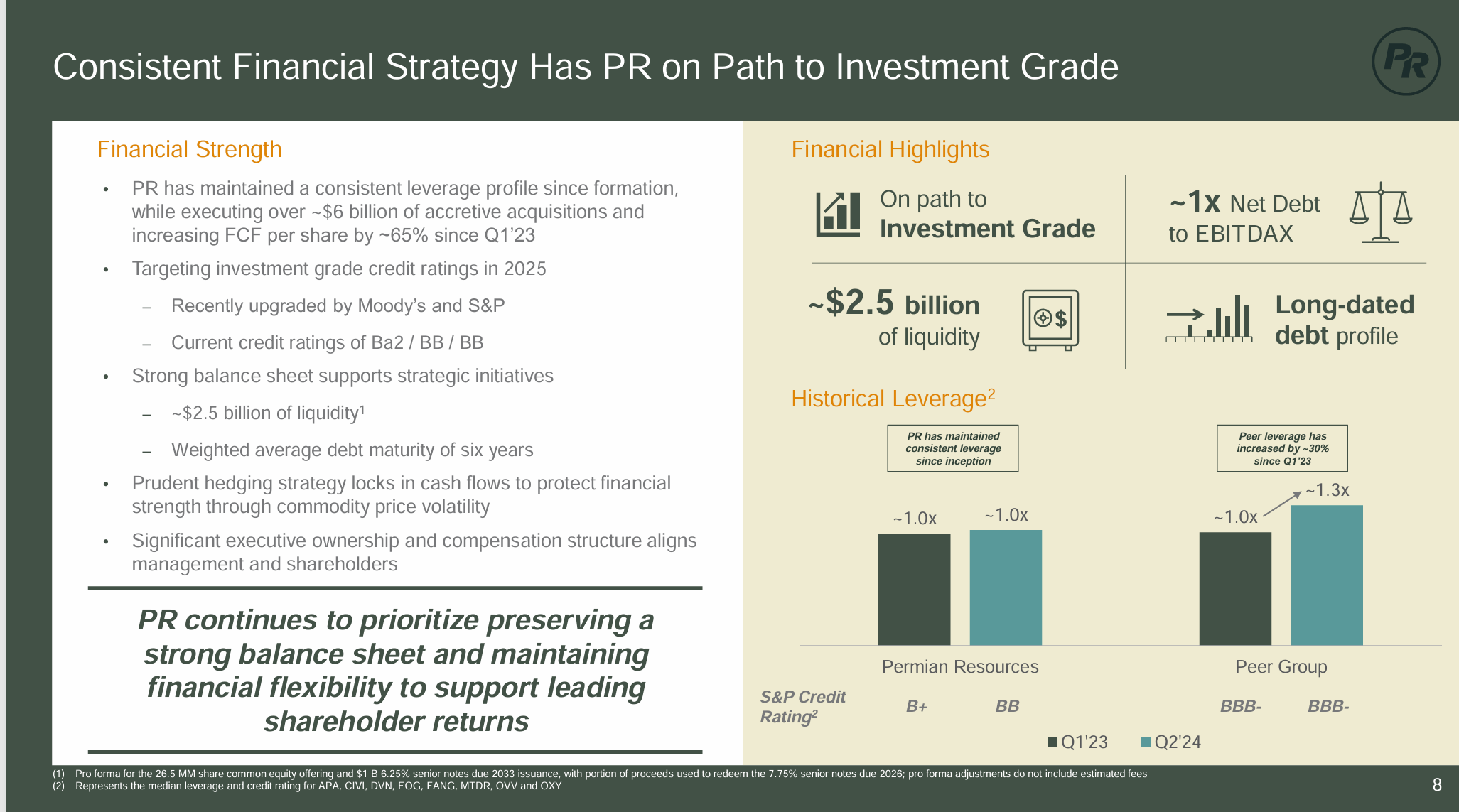

Funds

The scores corporations have seen as nicely.

Permian Sources Debt Rankings Progress (Permian Sources Second Quarter 2024, Earnings Convention Name Slides)

I’ve lengthy heard from traders that they consider that one of the simplest ways to have a “homerun” funding is to have a variety of leverage. But here’s a administration that has constructed and offered corporations efficiently conserving that debt ratio at roughly 1.0 whereas nonetheless benefitting the inventory value long-term.

In reality, the debt score goes up. Administration does have a aim to make funding grade by subsequent yr. Clearly, with the most recent debt score improve, the corporate is nicely on its method to assembly that aim.

There may be clearly a large disjoint between what many traders assume is required for fulfillment in comparison with what profitable managements like this one do for these giant returns.

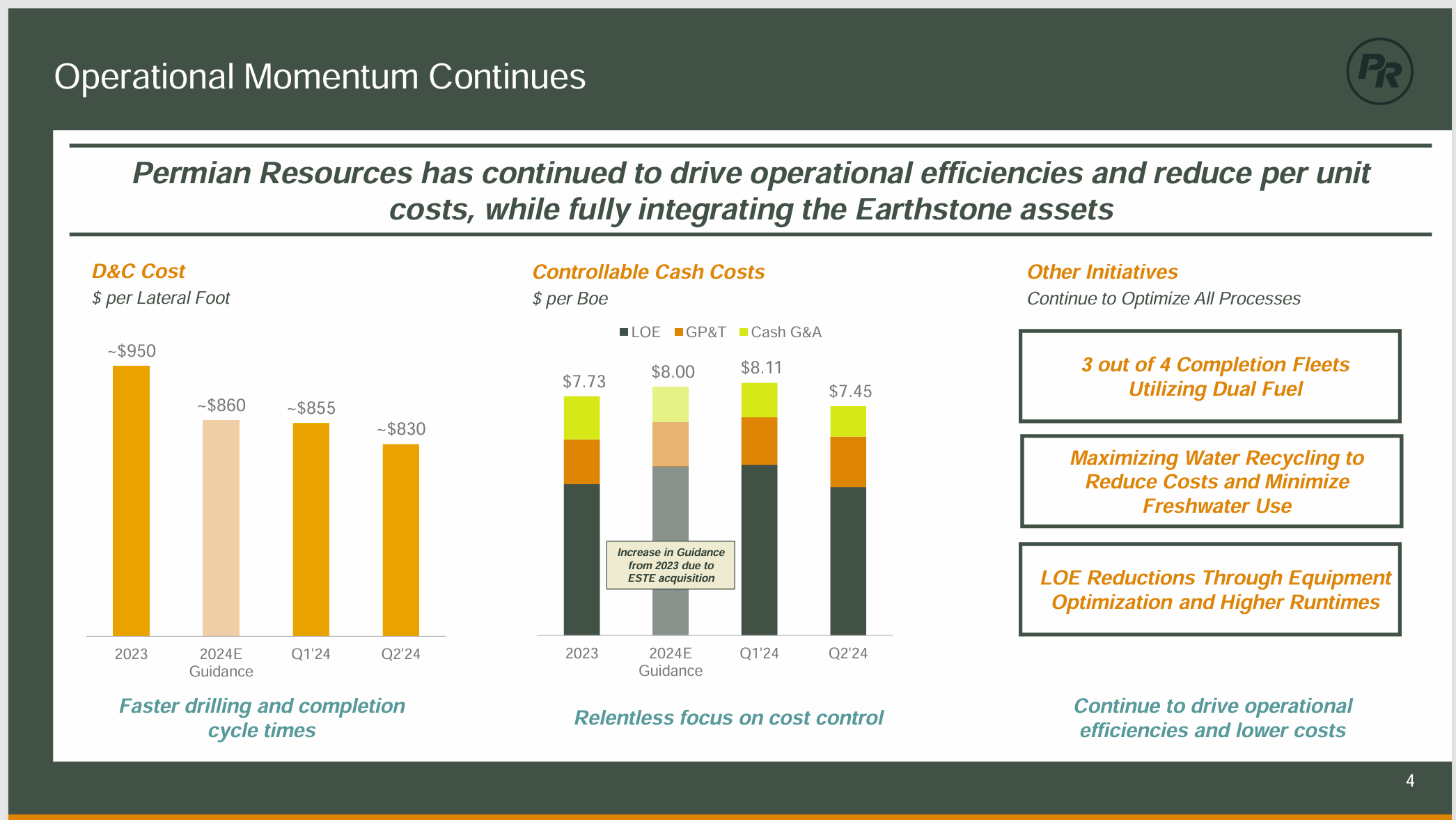

Price Reductions

The most important acquisition by far was the Earthstone acquisition. That firm itself was on a purchasing spree when the provide to be acquired by Permian Sources was negotiated. There was no approach that the Earthstone administration may have optimized operations earlier than the merger with Permian Sources. Due to this fact, there was seemingly appreciable upside potential simply by persevering with the optimization course of that Earthstone started.

Permian Sources Price Discount Progress (Permian Sources Second Quarter 2024, Earnings Convention Name Slides)

The very first thing that occurs after a big acquisition like this can be a quarterly report that actually reveals the vendor’s prices mixed with current operations. It takes a while to optimize operations, and doubtless nonetheless extra time for some high-cost manufacturing to say no in significance over time.

Within the meantime, it likewise takes a while for brand new decrease price wells to have an effect on company outcomes. Nonetheless, administration seems to be making good progress on this entrance.

The place this firm is positioned, the economies of scale ought to ultimately enable these prices proven above to strategy the price of pure fuel corporations whereas producing much more oil. The outcome must be one very worthwhile firm.

Steerage Adjustment

The persevering with progress has allowed steerage adjustment within the present fiscal yr.

Permian Sources Manufacturing Quantity Will increase (Permian Sources Second Quarter 2024, Earnings Convention Name Slides)

The factor about small changes like that is that a variety of prices don’t improve when the adjustment is small. Because of this, a disproportionate quantity of the money worth of the adjustment heads to the underside line to considerably improve profitability.

Since web earnings is a small share of revenues, small changes like this will materially change the earnings outlook within the close to future.

There may be seemingly extra upside potential as know-how advances preserve including intervals that have been beforehand not industrial to the manufacturing prospects. Due to this fact, there may very well be extra acreage added to Tier 1 over time.

Location

This firm has a location benefit that few corporations of its measurement can match.

Permian Sources Abstract Of Operations (Permian Sources Second Quarter 2024, Earnings Convention Name Slides)

The difficulty with the Delaware acreage was the flexibility to get permits to drill. The present administration has straightened that subject out to the purpose the place it’s not the difficulty it was earlier than 2020. Nevertheless, as soon as one thing like that occurs, then the worth of the acreage “takes a success” till it is clear a monitor file has been established that allows will likely be given out on a well timed foundation. This subject principally affected the New Mexico acreage the place there was federal land.

The Reeves County acreage might be a few of the finest positioned acreage within the business. Seldom does a smaller firm get to determine an acreage place in such a prestigious county.

The problems on Federal land have allowed a number of acquisitions at discount costs from managements (like Earthstone) who used to state that they now had years of permits. So long as that allow subject continues to fade into the previous, then these acquisitions are solely going to extend in worth.

Abstract

This inventory has been doing exceptionally nicely for the reason that administration took over the operations of a public firm to basically carry their operations public. Since my unique article on the merger that created this firm, the inventory value has completed reasonably nicely.

The inventory value ought to proceed to do nicely as it seems that the acquisition program is continuing efficiently. It is a firm that manages to largely develop via acquisitions whereas additionally paying a dividend.

It’s an instance of a administration keen to go that further mile to discover a method to develop whereas assembly the market calls for for shareholder returns together with a low debt ratio. That takes a pushed, detail-oriented administration to perform all of that.

The inventory stays a robust purchase as this administration had appreciable personal expertise in constructing and promoting corporations. That lessens the danger of failure significantly.

The corporate remains to be comparatively low cost on this market as a result of there actually is not any monitor file after the massive merger with Earthstone Power. However that seems to be about to vary for the higher as administration continues to lower prices whereas rising manufacturing efficiency. The hot button is that administration doesn’t should do something extraordinary. They simply should preserve doing what they at all times have been doing to proceed to return above-average returns for this business.

I might subsequently think about holding this firm till administration decides to promote the corporate. This administration has completed nicely for its traders prior to now. Whereas that’s no assure of future outcomes. The diminished danger of failure by going with skilled administration might be going to provide outsized risk-adjusted returns.

Danger

Any firm that has a historical past of profitable acquisitions can have an acquisition that fails to satisfy expectations. Clearly, the danger is diminished right here as a result of the previous monitor file has been fairly good. Nonetheless, once in a while, a handsome acquisition could be disappointing.

Any upstream firm is topic to the volatility and low visibility of future commodity costs. The hedging program in place can cut back these dangers. Nevertheless, a extreme and sustained commodity value downturn can change the longer term outlook of the corporate.

A lack of key personnel can materially change the outlook of the corporate.

[ad_2]

2024-08-09 01:38:25

Source :https://seekingalpha.com/article/4712462-permian-resources-stock-q2-the-building-process-continues?source=feed_all_articles

{kind=link}

Discussion about this post