[ad_1]

Paul Wallén/iStock through Getty Pictures

PYPL inventory: what’s treasury inventory?

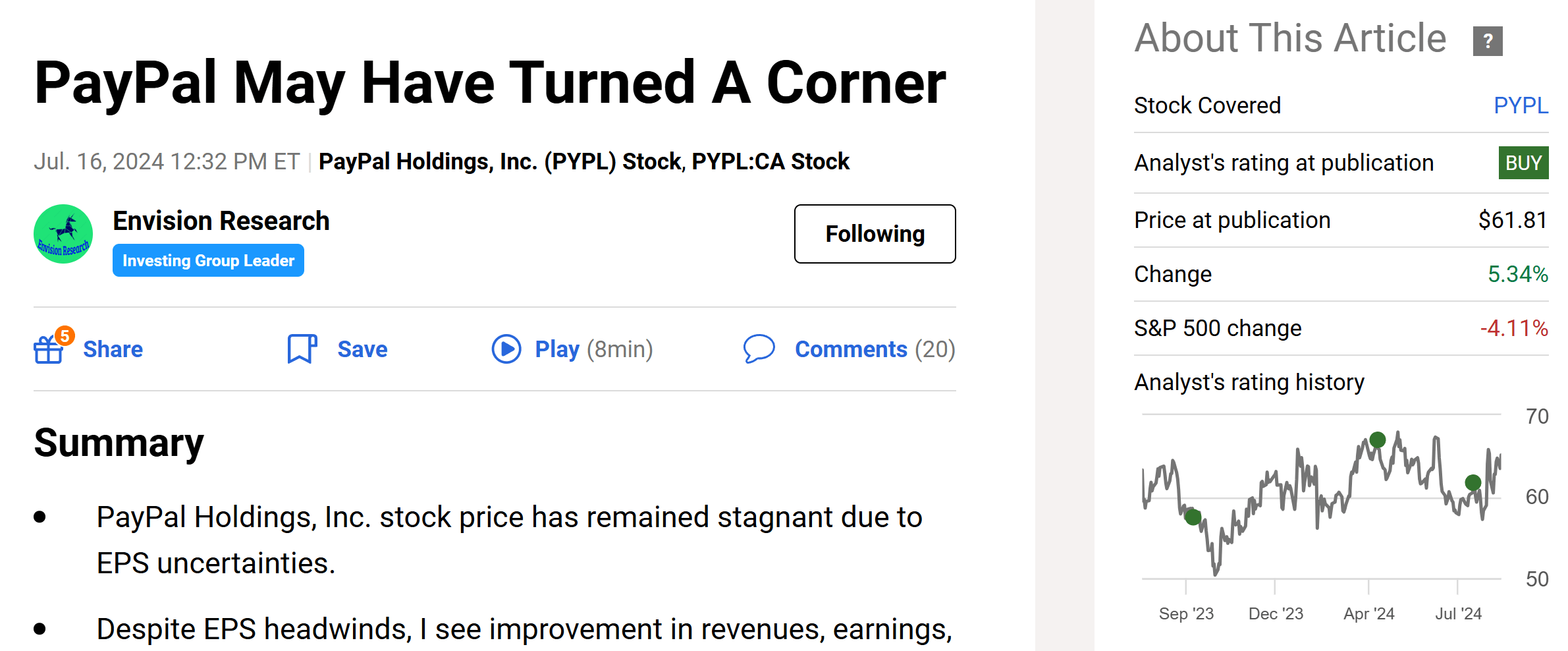

I final wrote about PayPal Holdings, Inc. (NASDAQ:PYPL) a couple of month in the past. As illustrated by the screenshot under, the article was titled “PayPal Could Have Turned A Nook” and was printed by Searching for Alpha on July 16, 2024. Within the article, I argued for a “purchase” ranking primarily based on the next concerns:

PayPal Holdings, Inc. inventory worth has remained stagnant resulting from EPS uncertainties. Regardless of EPS headwinds, I see enchancment in revenues, earnings, and working margins. Additional positives embrace its main market share, loyal consumer base, sturdy steadiness sheet, and low cost valuation ratios.

Searching for Alpha

Since that writing, the corporate has launched its 2024 Q2 earnings report (ER) and its worth additionally diverged by about 10% from the broader market as seen within the chart above. Thus, I assumed it will be useful to put in writing this follow-up article to include these new developments. By this time, a number of different SA authors had already reviewed the Q2 ER (which was launched on July 30) and dissected the numbers in numerous methods. Therefore, right here I’ll focus solely on one issue that has not been mentioned in any respect so far: its sizable treasury inventory. Within the the rest of this text, I’ll clarify why this issues and the way its valuation (already fairly low cost) is much more enticing than on the floor as soon as the treasury inventory is taken into account.

I assume many buyers most likely by no means paid consideration to treasury inventory (or treasury shares). So let me begin with a quick introduction to higher prime the extra in-depth dialogue. Treasury inventory, also called treasury shares, is inventory that an organization buys again from its shareholders. The corporate then holds the inventory for future use (extra on this later). For PYPL, its treasury inventory has grown to a file $24.06B as of Q2 2024. Extra particularly, the chart under reveals the treasury inventory and its YOY progress for PYPL inventory. As seen, PayPal’s treasury inventory has been constantly growing at a fast tempo just lately. The year-over-year progress price has been above 20% prior to now 5 years, yearly.

Subsequent, I’ll clarify the place the treasury inventory comes from and what it means for PYPL’s return potential.

Searching for Alpha

PYPL treasury shares: the place do they arrive from?

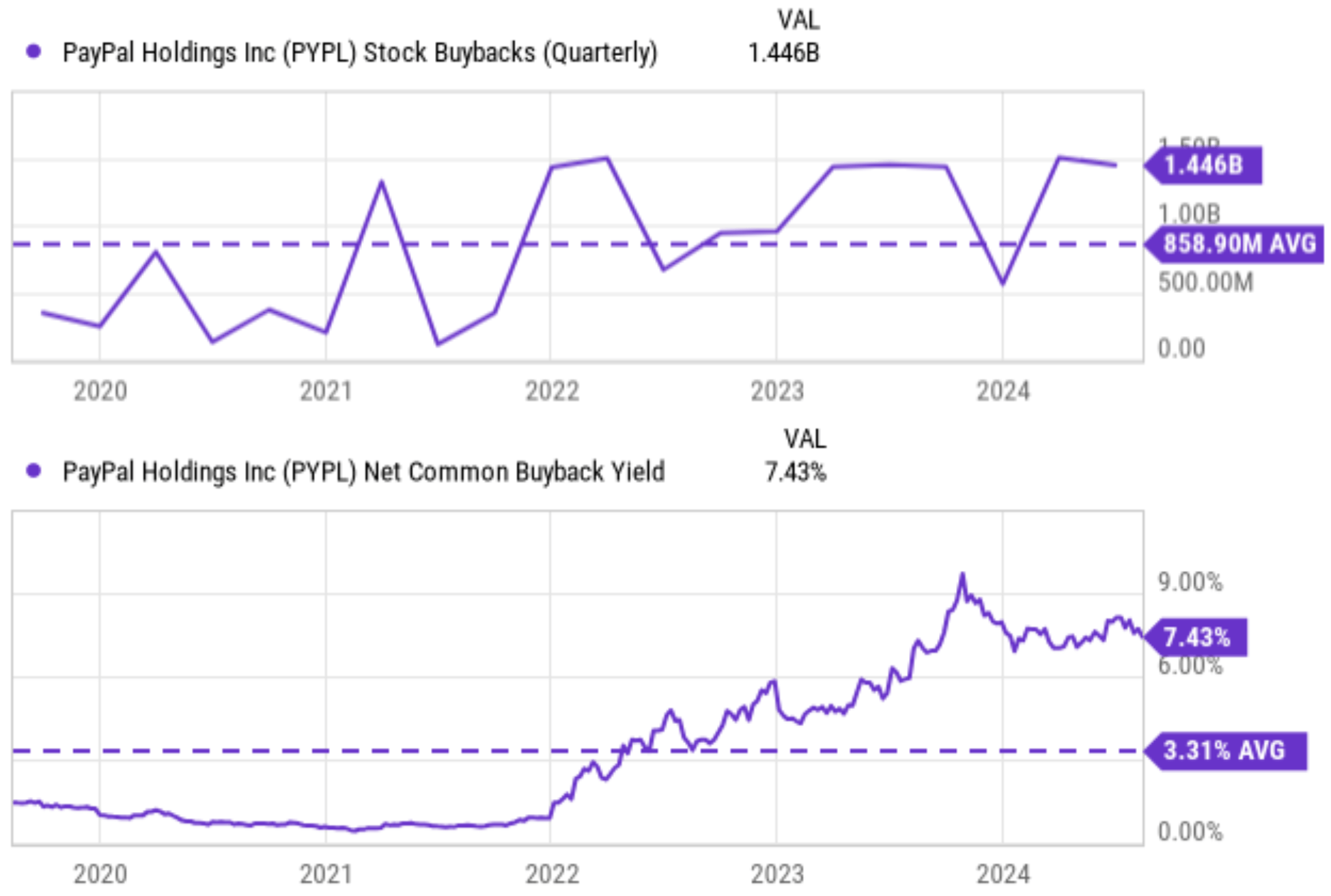

As aforementioned, treasury shares come from shares repurchased from shareholders. The corporate has been aggressively shopping for again its personal shares just lately – a powerful signal of its wholesome money move and a sign of the enticing valuation of its shares. Extra particularly, the following chart reveals PayPal’s quarterly inventory buybacks and web widespread buyback yield prior to now 5 years from 2020 to 2024. As seen, buybacks peaked at roughly $1.5 billion per quarter for a number of quarters. The typical buyback worth is round $858.9 million throughout this era, translating right into a web widespread buyback yield of three.31% on common. The present buyback yield of seven.43% is much above the historic common.

After an organization repurchases its personal shares, the corporate can select to take away the inventory completely from circulation (aka, retire the shares). Alternatively, the corporate can file it as a contra-equity account on its steadiness sheet, which then turns into the treasury inventory we’re speaking about right here.

Subsequent, we’ll take a better have a look at it and I’ll clarify why the massive treasury inventory creates extra worth for shareholders than on the floor.

Searching for Alpha

PYPL inventory: treasury inventory is hidden treasury

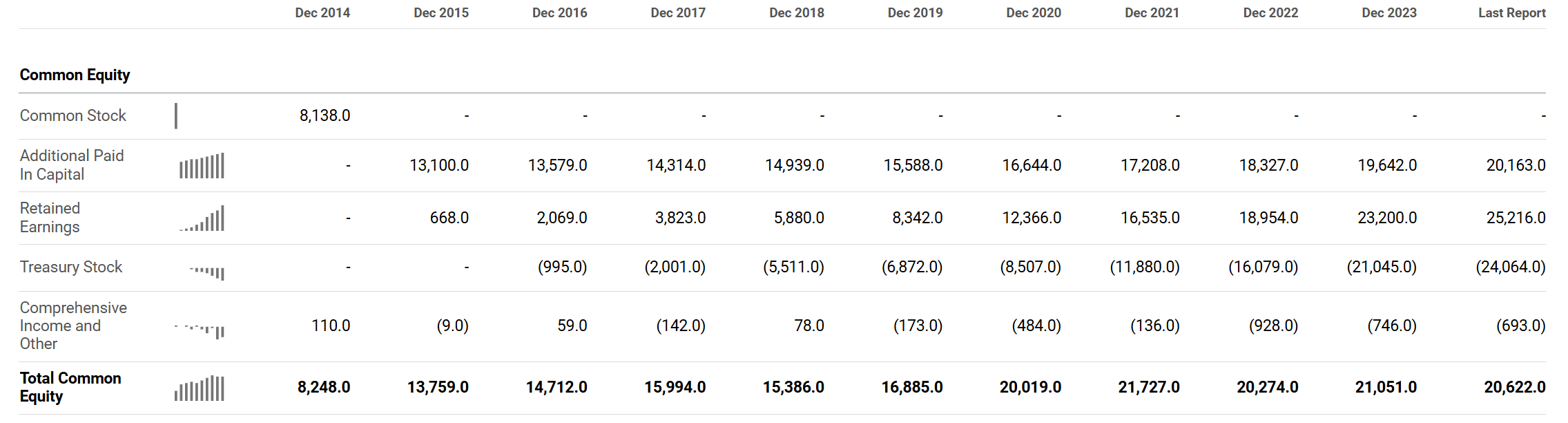

As simply talked about, treasury inventory is recorded as a contra-equity account within the steadiness sheet. Particularly for PYPL, the chart under reveals its treasury inventory prior to now 10 years. As seen, it began at a negligible quantity of $995 million in 2014 and quickly grew to the present file quantity of $24.06 billion. After all, many corporations maintain treasury inventory. It’s simply within the case of PYPL, its holdings are too massive to disregard both compared to its complete widespread fairness (as seen within the chart under) or its market cap (about $66B as of this writing). The sheer magnitude, mixed with its present valuation, makes it a big upside catalyst for shareholder returns in additional view.

Searching for Alpha

First, a big share buyback (to create treasury inventory within the first place) can probably create extra worth for PYPL shareholders than holding money or paying money dividends for a lot of causes. Low-cost valuation (extra on this later) and tax benefit are the highest two on my checklist.

Second, in comparison with retiring the repurchased shares, there are additionally some key benefits for an organization to carry treasury inventory. The benefits can are available numerous varieties and shapes, however the essence may be summarized in a single phrase: flexibility. By holding treasury inventory relatively than retiring it, an organization maintains the choice to make use of these shares because it sees match. For instance, PYPL can re-issue these shares sooner or later to boost capital when it wants. PYPL may additionally use the treasury inventory to satisfy inventory choices they’ve provided to executives as a part of their compensation bundle. Such flexibility is stronger than on the floor (though a $20B+ place is already fairly potent on the floor) as defined subsequent.

Different dangers and closing ideas

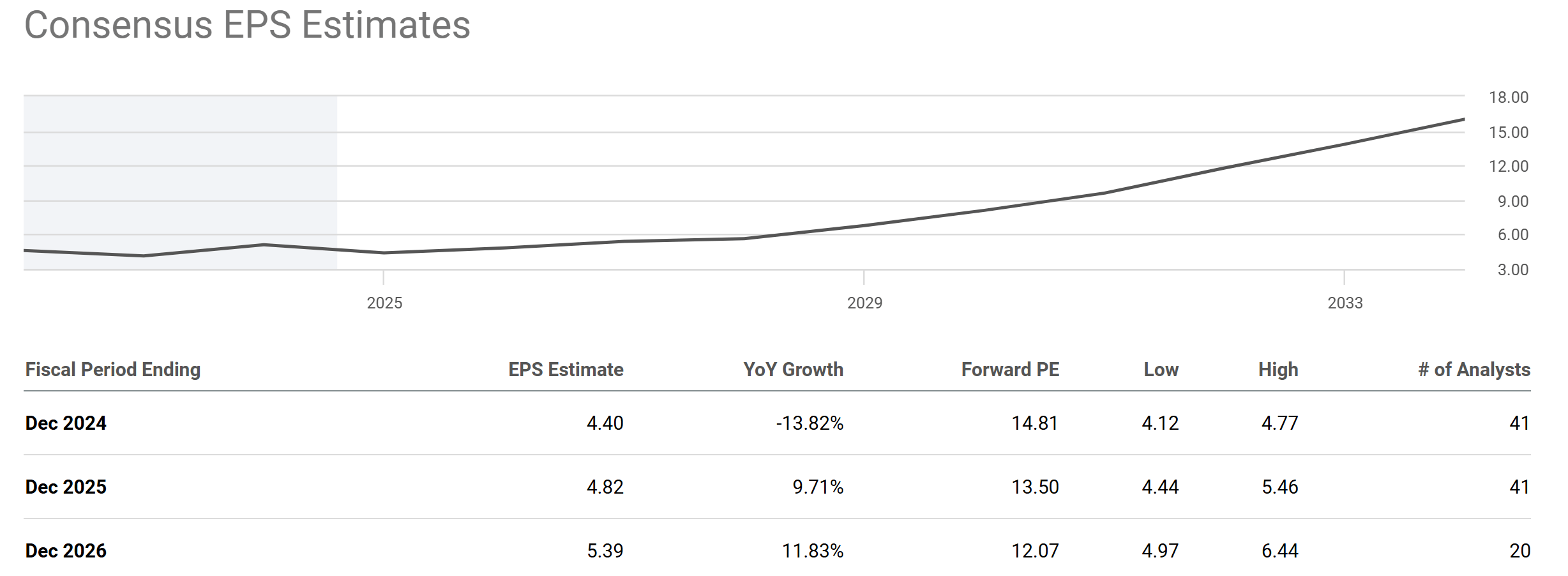

An element many PYPL bulls quote is a budget valuation. Certainly, the inventory’s present P/E may be very enticing each in absolute phrases and relative phrases. The chart under summarizes PYPL inventory’s valuation grade. As seen, its shares are buying and selling at solely 12.89x P/E on a TTM and non-GAAP foundation. That is greater than 62% decrease than its 5-year common of 33.95. The valuation low cost is even deeper than on the floor when the above massive treasury inventory (and rising widespread fairness) is taken into account. Even when the corporate’s incomes energy doesn’t enhance, the corporate needs to be price extra by merely hoarding money. In PYPL’s case, the earnings energy is projected to develop at strong charges (see the second chart) and thus I count on the efficiency of its treasury inventory to rise in tandem.

Searching for Alpha Searching for Alpha

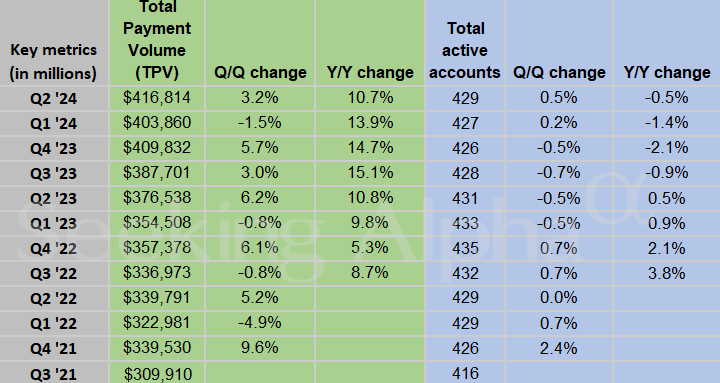

By way of draw back dangers, the variety of energetic accounts has been stagnating currently. The chart under reveals the whole energetic accounts of PYPL inventory in latest quarters. As seen, the quantity peaked at 435 million accounts in This fall 2022. The expansion price then began fluctuating since then. On a year-over-year foundation, the quantity has declined by 0.5% in Q2 2024 to 429 million. Judging by its Q2 numbers, it appears to me that some elevated exercise among the many current buyer base helped to offset the affect to a point. Wanting additional out, it is unclear to me how/whether or not the quantity can resume its earlier progress charges given the present utilization price of the platform by retailers and in addition the general macroeconomic surroundings.

All advised, my verdict is that the inventory gives a skewed return/danger profile below its present situations. At its present P/E of round 15x with double-digit EPS progress projection, PayPal Holdings, Inc. inventory gives an interesting GARP alternative (Development at an affordable worth). Its valuation is much more enticing than on the floor, contemplating the sizable treasury inventory. As a thought experiment for illustrative functions, retiring all its current treasury shares at the moment would immediately cut back its share counts by about one-third (at at the moment’s share costs), thus boosting its EPS and reducing its P/E by the corresponding quantity.

Searching for Alpha

[ad_2]

2024-08-14 17:28:07

Source :https://seekingalpha.com/article/4714527-paypal-treasury-stock-what-it-is-why-it-matters?source=feed_all_articles

{kind=link}

Discussion about this post