[ad_1]

Lighthouse Movies/DigitalVision through Getty Photos

Following a transition interval for Nike, on the finish of December 2023, our workforce determined to improve On Holding AG (NYSE:ONON) to a purchase score. This optimistic view was primarily influenced by the corporate’s very important product innovation, favorable demand traits, and supportive outcomes. On Holding AG was additionally assured in its ambitions for the FY 2026 targets, with plans for increased top-line gross sales, new retailer openings, and a key benefit on working leverage to help its earnings development story. Since then, the corporate’s inventory worth has appreciated by nearly 65% (Fig 1), making On Holding top-of-the-line 2024 funding concepts.

Mare Previous Evaluation Ranking Replace

Fig 1

Q2 Outcomes and Our Constructive Take

Very briefly, the corporate reported stable Q2 gross sales and adjusted EBITDA beats. In numbers, internet gross sales elevated by 27.8% to CHF 567.7 million, with a 140-basis-point overperformance in comparison with the Avenue’s development forecast. The unfavorable forex developments have been a 160-basis-point headwind within the quarter. Excluding that, ON’s wholesale and DTC channels elevated by 28.8% and 30.4%, respectively.

Wanting on the geographical footprint, On’s APAC gross sales have been up 84.7%. That mentioned, EME and Americas (excluding FX) have been up by 22.2% and 25.8%. By class, On reported stable gross sales in footwear, however attire rose by 66.6%. Happening to the P&L, gross margin expanded to 59.9%, and OpEx as a proportion of gross sales reached 48.6% and was down by 5 foundation factors in comparison with final 12 months. For that reason, the corporate’s adj. EBITDA elevated to CHF 90.8 million with a 16% margin. This was additionally above consensus estimates. On a optimistic notice, stock was down 8% on a year-to-year comparability.

Other than a robust print of outcomes, On technique is progressing nicely. Certainly, we see a number of drivers to our supportive fairness story:

- Firstly, the corporate continues to innovate. There may be supportive new footwear innovation. For example, the corporate has launched LightSpray™ expertise. This new product is ESG-friendly however, extra importantly, offers excessive efficiency in racing;

- The corporate is transferring on to new sports activities, equivalent to tennis, mountaineering & out of doors, and coaching & health club;

- Apart from new sports activities, the corporate is efficiently increasing into new product classes, primarily attire and equipment. This reinforces the corporate’s concentrate on its EU enterprise. The corporate efficiently leveraged the Olympic Video games to consolidate its model momentum with native EU customers. For the event, On opened its Paris retailer, which is its largest retail location. These initiatives will doubtless improve model loyalty and consciousness, growing its whole addressable market;

- Lastly, there’s a supportive enlargement into new geographies, significantly in APAC. Asia’s turnover is lower than 10% of the overall firm’s gross sales (Fig 2), so there’s room for development.

On Holding APAC gross sales

Source: On Holding Q2 press launch – Fig 2

Whereas Nike careworn client weak point and macroeconomic pressures, right here on the Lab, we consider the worldwide athletic put on business would possibly obtain a high-single-digit development for a multi-year interval. The most recent Athletic Attire market report additionally helps this. Earlier than the COVID-19 outbreak, the business’s common improve was within the single-digit space; nonetheless, we consider the pandemic has amplified client traits towards wellness, well being, and informal gown. For that reason, we consider On will doubtless improve its market share penetration.

By class, On footwear division has already proven it could actually deal with a big market share. Right here on the Lab, we consider it’s uncommon to see a model with international traits. We are actually pricing a multi-sport & class model just like Puma, Adidas, and Nike. On Holding, international recognition additionally stays low; this would possibly point out room for development as shoppers uncover the brand new model.

Earnings Adjustments and Valuation

Following the Q2 outcomes, we anticipate Q3 gross sales to develop by 28% to CHF 620 million. For the Fiscal 12 months 2024, our whole turnover reached CHF 2.26 billion. On the outlook offered, the corporate guides for “not less than” 30% gross sales development, excluding FX in 2024. Our reported gross sales come down for FX headwinds; we would anticipate 350 foundation factors of unfavorable impression with the present spot charges.

As well as, contemplating increased freight value expectations, we decrease The gross margin estimate by 20 foundation factors. On a optimistic notice, we forecast a gross margin profit from increased DTC share, and taking place to the P&L assumption, we forecast increased advertising and marketing bills as a result of Paris Olympic video games.

Combining these unfavorable results, our internet earnings projection goes down by 7% to CHF 260 million, with an EPS of CHF 0.8. That mentioned, our goal worth is derived from our long-term assumption. Intimately, we consider the corporate would possibly obtain 2% of the sports activities market with a high-teens EBIT margin. This is because of its premium worth and DTC enterprise. Due to this fact, we consider increased market penetration will probably be accretive to On’s margins in the long term.

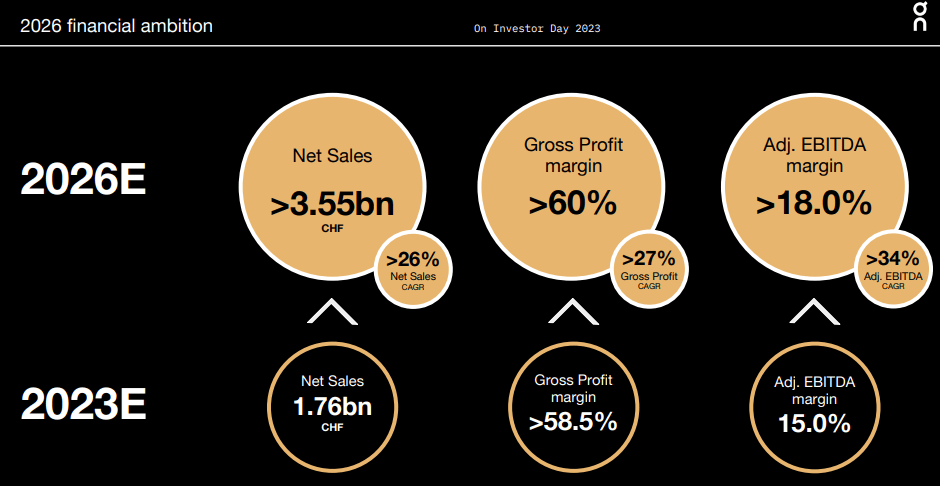

Our workforce forecasts a 25% gross sales development within the subsequent 5 years, with a optimistic and 45% appreciation of the corporate’s EPS. This elements an achievable 16.5% EBIT margin in 2028. With this consideration and the corporate’s visibility (Fig 3), in 2026, based mostly on a 40x P/E goal and an EPS of CHF 1.4, we elevated our goal worth to $55 per share. This obese worth takes into consideration an FX of 1.10 $/CHF.

On Holding 2026 goal

Source: On Holding Investor Day presentation – Fig 3

Dangers

From our standpoint, draw back dangers embody disruptions in international commerce, which could impression the corporate’s provide chain. Moreover, the corporate’s merchandise are primarily manufactured by third-party companions. Any disruption in On’s logistic operation can be a danger for the shares. In comparison with Nike, On Holding has a direct-to-consumer enterprise. Due to this fact, On Holding’s merchandise should not primarily offered by means of third-party retailers, which could affect end-market gross sales. That is supportive of our goal worth. The corporate nonetheless shares many dangers inside the sector, and we report 1) tariff modifications, which may have an antagonistic impression on earnings and operations, 2) FX fluctuations, 3) an incapacity to take care of a speedy tempo of recent product innovation to market, 4) slowing development in China, and 5) increased competitors. As well as, sporting items are delicate to style danger and financial cycles.

Conclusion

Our workforce continues to consider in On’s concentrate on innovation, direct-to-consumer promoting, and premium costs. The corporate is without doubt one of the world’s fastest-growing athletic put on manufacturers, and after stable Q2 outcomes, our purchase score goal is confirmed.

[ad_2]

2024-09-05 03:51:12

Source :https://seekingalpha.com/article/4719127-on-holding-growth-stock-to-buy?source=feed_all_articles

{kind=link}

Discussion about this post