[ad_1]

Michael Vi

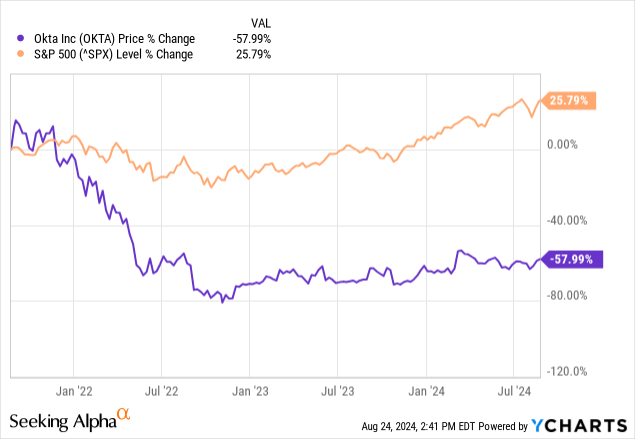

Okta (NASDAQ: OKTA) is a pacesetter within the Id and Entry Administration (“IAM”) market, each for workers and clients. I final wrote concerning the firm on March 15, 2021, earlier than macroeconomic headwinds hit the IT (Info Know-how) business. The corporate was in the course of buying Auth0, and traders have been anxious concerning the $6.5 billion price ticket, which some thought was an enormous overpay. The market additionally anxious concerning the firm’s excessive valuation within the face of rising bond rates of interest in response to excessive inflation. The best way issues turned out, the market was proper to fret. Since my purchase suggestion, the inventory value is down 57%, in comparison with the S&P 500’s (SPX) 42% rise.

Though issues look bleak as we speak, a stable secular tailwind drives progress within the IAM market, which has turn into important to an group’s safety posture. A stable id resolution is important as companies and authorities businesses digitally remodel. Regardless of a down financial system, non-public and public organizations will not be capable of keep away from the results of not having a high id resolution endlessly. As soon as the financial system improves, Okta’s difficulties in producing gross sales ought to reduce, and the corporate ought to begin delivering the basics traders need to see. Contemplating the corporate’s high quality, it at present sells at an inexpensive valuation.

This text will discover the financial headwinds behind the corporate’s decline, evaluate some issues traders ought to search for earlier than it reviews its upcoming second-quarter fiscal yr (“FY”) 2025 earnings on August 28, and talk about three actions the corporate has taken to reignite income progress. It can additionally study Okta’s valuation, a number of dangers, and why I fee the inventory as a purchase.

Macroeconomic headwinds

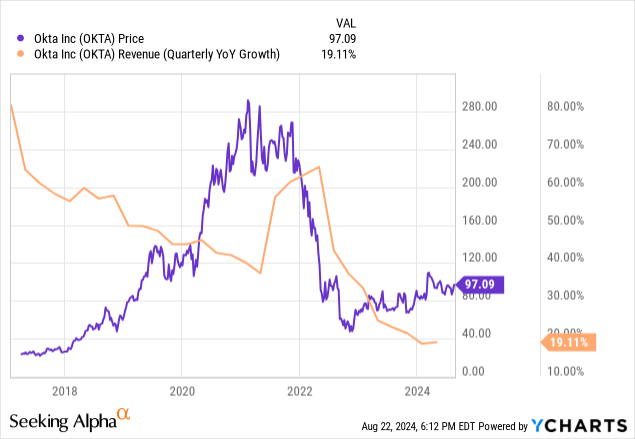

Okta’s all-time closing value was $291.78 on February 12, 2021. It closed out 2021 at $224.18. Because the Federal Reserve raised rates of interest throughout 2022, the specter of an financial downturn rose, and in response, enterprises reduce on spending on IT infrastructure, software program, and providers. The next chart exhibits that the corporate’s income fell drastically for the reason that starting of 2022. Income progress was above 60% year-over-year on the finish of the calendar yr 2021 and the start of 2022. Okta’s year-over-year quarterly income is now right down to 19.11% as of the tip of the primary quarter of FY 2025.

Okta Chief Monetary Officer (“CFO”) Brett Tighe mentioned on the June 11, 2024, NASDAQ Investor Convention (emphasis added):

So macro is certainly a headwind to us. We have talked about it for a number of quarters now. We do not see it getting worse or getting higher at this level. Whenever you take a look at our steering for the stability of the yr, we’re assuming actually the macro as it’s as we speak, which is a headwind and it is a headwind in a wide range of methods, however the primary one which we see it as a brand new emblem acquisition, it’s more durable to do enterprise with new clients at this level. In case you take a look at the final a number of quarters, for us, many of the enterprise or many of the internet new ACV [Annual Contract Value] is coming from an upsell facet of the home. Upsell being both seats or from cross-sell. And while you dial-in and also you dive deeper into that, it is actually extra cross-sell than it’s extra seats. Individuals are way more considerate about their budgets at this level and their contractual spend.

My translation: The Okta CFO thinks that the specter of recession has made firms reluctant to buy new cloud providers, making it tough for Okta to achieve new clients.

Essentially the most in depth deterioration of Okta’s enterprise within the IT downturn has come from small and medium-sized companies (“SMB”). Enterprise from bigger enterprises, with extra stable stability sheets, has been way more secure. Enterprise from authorities businesses has additionally held up nicely. Nevertheless, till the financial system recovers sufficient for SMBs to open their wallets once more, the corporate’s income and earnings-per-share (“EPS”) progress might look lackluster.

Firm Fundamentals

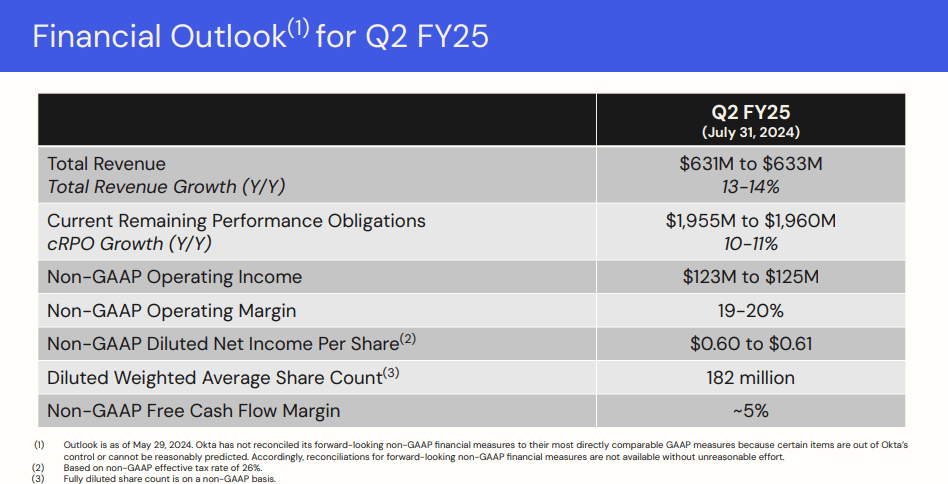

The next exhibits administration’s steering for Okta’s second quarter FY 2025 earnings. As you possibly can see, the corporate forecasts a 13-14% year-over-year enhance in quarterly income. If it hits that mark, it would proceed a downward quarterly year-over-year income progress pattern.

Okta First Quarter FY 2025 Investor Presentation

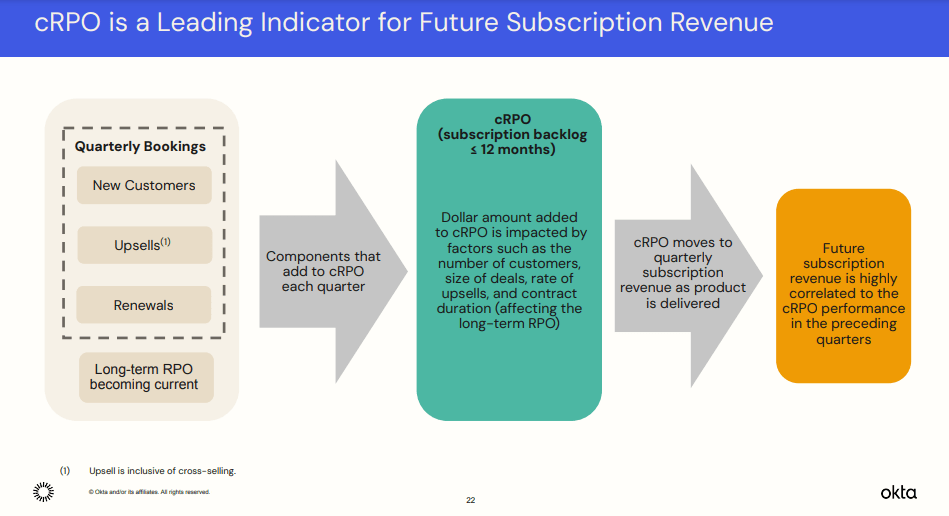

Buyers must also contemplate the present remaining efficiency obligations (cRPO) within the upcoming Okta earnings report. This quantity represents the income an organization expects to acknowledge from contractual obligations it would full inside the forthcoming yr. The next picture exhibits how cRPO turns into future quarterly subscription income. The corporate has recognized cRPO as a forerunner of subscription income within the subsequent a number of quarters.

Okta First Quarter FY 2025 Investor Presentation.

Okta’s first quarter FY 2025 cRPO grew 15% year-over-year, and the corporate forecasts a second-quarter cRPO of 10-11%. If that steering seems to be correct, the downtrend in cRPO might imply that quarterly income progress might proceed to drop in future quarters. Though Wall Road and In search of Alpha analysts advocate a purchase, and In search of Alpha Quant recommends a robust purchase, traders have but to purchase the inventory enthusiastically. The chart beneath exhibits that the 30-day common each day inventory quantity has decreased for the reason that center of 2022.

In case you determine to take a position on this inventory, perceive that the market might stay unexcited concerning the firm till it ends its downward income progress pattern and reaccelerates income progress.

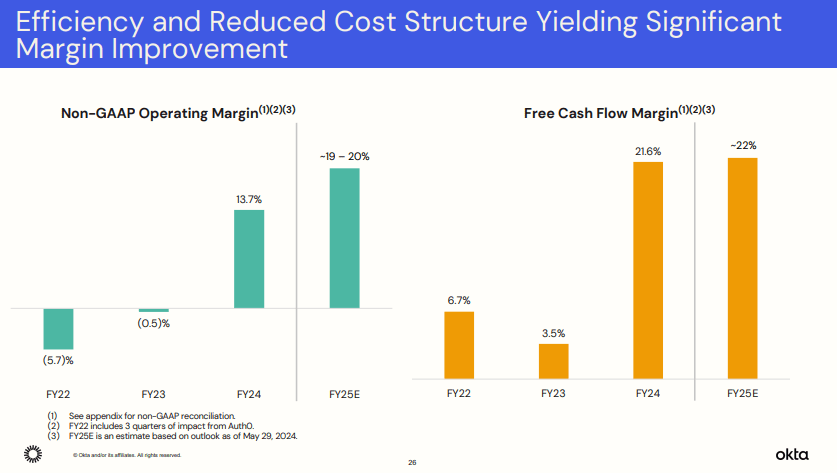

Like different SaaS firms, when topline progress began to pattern down in 2022, Okta targeted on decreasing prices and growing effectivity. The market desires to see that elevated focus present up in elevated profitability and improved free money circulate (“FCF”). The next charts present the corporate’s annual non-GAAP (Usually Accepted Accounting Rules) working margin and FCF margin trending up—proof that its technique is working.

Okta First Quarter FY 2025 Investor Presentation

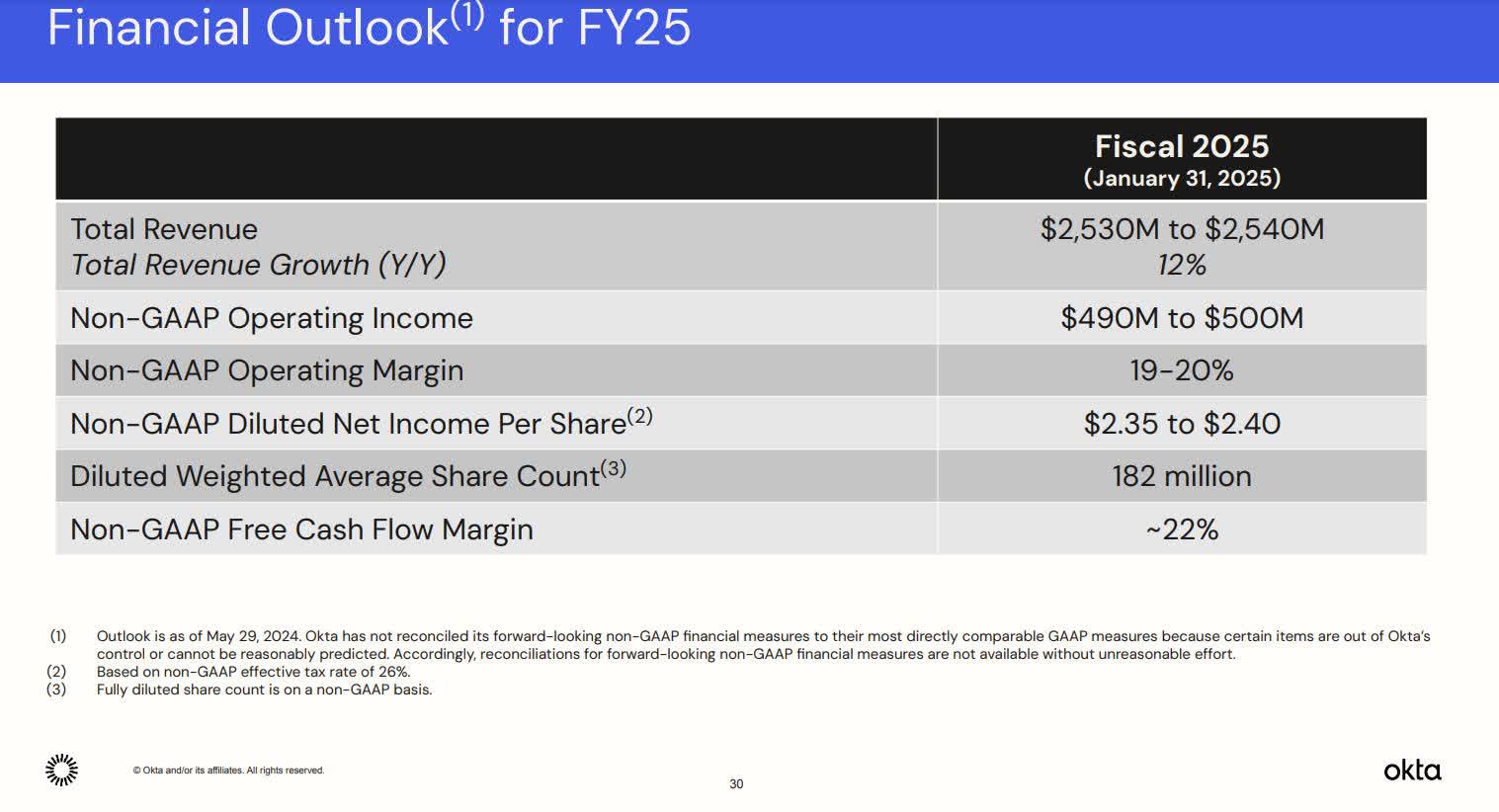

When the corporate reviews its second quarter FY 2025 earnings and FY 2025, traders ought to pay shut consideration as to if Okta can meet or beat steering for non-GAAP working revenue, working margin, diluted internet revenue per share, and FCF margin. All of these gadgets have implications for a way traders worth the inventory.

Okta First Quarter FY 2025 Investor Presentation

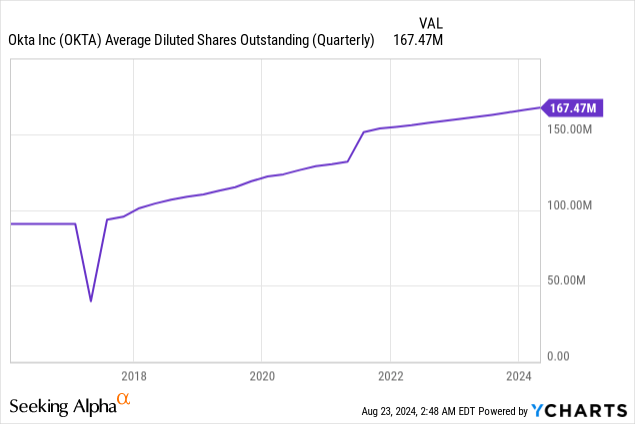

Additionally, administration forecasts a diluted weighted common share depend of 182 million for FY 2025. The next chart exhibits Okta’s common excellent diluted shares have constantly risen since 2018.

The corporate’s stock-based compensation (“SBC”) as a share of income is 24.47%, which is comparatively excessive. SBC dilutes present traders by elevating the share depend, negatively impacting GAAP internet revenue per share. Consequently, traders must also take note of GAAP numbers regardless of the corporate emphasizing non-GAAP metrics (non-GAAP removes the impression of SBC).

The corporate at present has a primary quarter FY 2025 Rule of 40 of 43.47 (Quarterly income progress fee of 19% + free money circulate margin of 24.47%). The Rule of 40 is a SaaS metric that states {that a} wholesome SaaS firm at scale ought to have a income progress fee + revenue margin of 40% or extra. Some analysts use the EBITDA (Earnings Earlier than Curiosity, Taxes, Depreciation, and Amortization) margin. Others use internet revenue margin. On this case, I exploit the trailing 12-month (“TTM”) FCF margin. If Okta’s income progress decreases to 13%-14%, as forecasted for the second quarter, the corporate should enhance its TTM FCF margin to proceed assembly the Rule of 40.

Reigniting Okta’s progress

Presently, investor sentiment about IT infrastructure firms is dismal. Lots of the cloud firms that thrived in 2020 have struggled from 2022 to 2024. Nevertheless, the macro financial system will finally enhance, and enterprises will begin spending on important providers that allow digital transformation. One glorious query is what providers Okta will supply the market to assist the corporate reignite progress as soon as the macro financial system turns into a tailwind.

On the NASDAQ Investor convention, Jeffries analyst Joseph Gallo requested Okta CFO Brett Tighe, “What are the three or 4 issues that may possibly finally reaccelerate progress?” CFO Tighe mentioned:

So, we expect that these three areas, the brand new merchandise, the associate ecosystem, and a hunter-farmer ought to assist us reignite progress over the medium-term. I am not saying it is over the near-term.I imply, in a SaaS income mannequin, it is exhausting to speed up that in such a brief timeframe. So, it will take us a while.

1. New merchandise

CFO Tighe named three new merchandise: one associated to governance, Privileged Entry Administration (“PAM”), and High-quality-Grained Authorization (“FGA”).

The corporate launched its Okta Id Governance product in August 2022. Id Governance defines the roles of every job and the permissions allowed. This service assigns every consumer a job throughout onboarding. It additionally continually opinions whether or not customers nonetheless require the entry they’ve and ensures that nobody consumer has extra entry than they want. Final, it removes an individual’s entry once they go away the corporate.

PAM focuses solely on managing entry to privileged accounts and delicate information. A privileged account can change system settings, set up software program, make configuration modifications, and management community entry. System directors and anybody who can view, modify, or delete delicate information have privileged accounts.

FGA is one in all Okta’s latest merchandise. It solely went into Basic Availability in March 2024. This service permits a system administrator to regulate what every consumer can do inside every app, right down to the tiniest element. This service is good to forestall unauthorized entry and information breaches. It additionally helps firms adjust to GDPR (Basic Knowledge Safety Regulation), HIPAA (Well being Insurance coverage Portability and Accountability Act), and related privateness laws.

2. Associate ecosystem

Okta has many companions, together with Palo Alto Networks (PANW), BeyondID, and Zscaler (ZS). Okta’s CFO mentioned on the NASDAQ Investor Convention:

So traditionally, Okta has been reseller targeted or conventional reseller targeted, suppose SHI, CDW and the final time we spoke about it, about 40% of the full income stream got here by way of the associate channel with the overwhelming majority of that being the reseller group. Now, there are two areas that we need to get extra deeply ingrained in, which is the cloud service suppliers like AWS, which we introduced final quarter on the finish of This autumn. It was about $175 million of ACV or Annualized Contract Worth rising about 130% year-over-year.

The Okta CFO additionally talked about that the corporate desires to take a position extra in GSIs (International Programs Integrators). Examples of GSIs embrace Accenture (ACN), PwC (PricewaterhouseCoopers), and Deloitte. The advantage of rising by way of GSIs is that Okta can attain a broader buyer base and enhance gross sales sooner than it might by itself. The most important GSIs have a few of the largest enterprises on the planet as clients. By means of these partnerships, Okta can acquire clients that it might not have acquired utilizing its salesforce. Moreover, GSIs supply purchasers consulting providers to assist deploy, handle, and combine Okta’s options.

Massive cloud suppliers can present advantages much like these of GSIs. Though the CFO emphasised Amazon’s (AMZN) AWS, Alphabet’s (GOOGL)(GOOG) Google Cloud platform, and, to a a lot lesser extent, Microsoft’s (MSFT) Azure are additionally companions. Since Microsoft has a household of id merchandise that compete with Okta, its partnership is shallower than that of AWS and Google.

Okta established a program in April 2023 referred to as Elevate, a revamped associate program to enhance associate engagement, enhance gross sales alternatives, and speed up Okta’s progress. The webpage saying the launch of Elevate states:

We have to do a greater job of attempting to find new logos. To drive that movement, we’re rewarding companions for locating new clients with an improved and streamlined deal registration course of.

If Okta’s emphasis on investing in partnerships works, it ought to velocity up the invention of extra new clients.

3. Hunter-Farmer gross sales mannequin

Okta administration appears to suppose implementing the hunter-farmer gross sales mannequin for small and medium-sized companies (SMBs) will entice new clients. CFO Tighe first introduced the change to this new gross sales technique on Okta’s fourth quarter FY 2024 earnings name (emphasis added):

Beginning at the start of this [fourth] quarter, we shifted our direct gross sales group that focuses on the SMB market within the Americas to what’s generally known as a hunter-farmer mannequin. Which means we now have a group of account executives targeted on driving new buyer acquisition and a separate group of account executives targeted on upsells inside our put in base. We consider that we’re nonetheless very underpenetrated inside our present base of almost 19,000 clients. This pure evolution will allow us to drive higher outcomes with each new and present clients.

The above assertion implies that the earlier gross sales mannequin did not produce sufficient cross-selling and upselling amongst present clients. The corporate generates most of its new income by cross-selling clients’ further merchandise and upselling new seats to a lesser extent. Within the software-as-a-service (“SaaS”) world, a seat means a buyer paying so as to add a consumer to the product license.

Buyers are likely to award SaaS firms like Okta increased valuations the extra profitable they’re at promoting to present clients. It prices an organization much less to promote to an present buyer than to make an preliminary sale to a brand new buyer. So, a SaaS firm that efficiently upsells and cross-sells usually has higher margins than these with much less success in promoting to present clients. You may measure a SaaS firm’s success at promoting to present clients by way of its Greenback-based internet retention fee (DBNRR). In 2020, the heyday for data know-how (“IT”) firms that enabled digital transformation, the market would usually award a SaaS IT firm a premium valuation if it had a DBNRR of over 120%. For instance, Okta had a first-quarter FY 2021 (April 2020) DBNRR of 121%, and the market gave it a price-to-sales (P/S) ratio of 27.94. A DBNRR of 121% means the corporate generated 21% extra income from present purchasers than within the earlier yr.

Okta produced a DBNRR of 111% within the first quarter of FY 2025 (April 2024). Though the quantity continues to be stable, it is much less spectacular than in 2020. The poor macro financial system, the destructive sentiment surrounding the IT sector, and the much less spectacular DBNRR have mixed to cut back traders’ enthusiasm concerning the firm and drastically decrease the P/S ratio into the one digits.

Okta is getting ready for the day when the financial system turns from a big headwind right into a tailwind. The inventory might by no means return to 2021’s P/S ratio highs above 45. Nevertheless, the above strategic strikes by administration are preparations for an financial system the place companies return to investing extra in IT wants and digital transformation. Buyers might award the inventory a better valuation if administration reaccelerates income progress and restores DBNRR to 115% to 120%.

A couple of dangers to contemplate

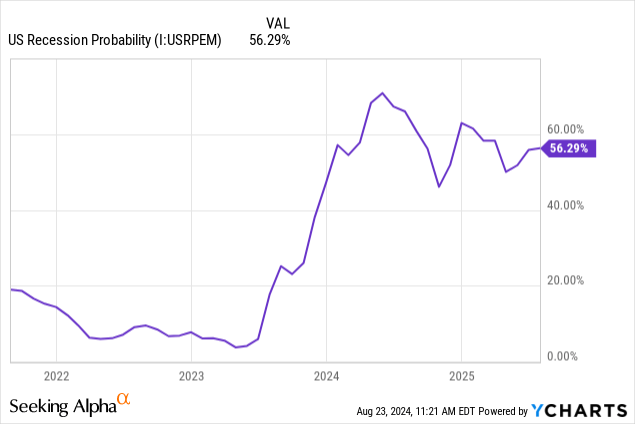

The financial system isn’t out of the woods but. In response to the Estrella & Mishkin technique, a recession continues to be attainable, with a likelihood of 56.29%. So long as that risk stays, SMBs could also be reluctant to develop spending on Okta’s options, and income progress might stay uninspiring to traders.

Potential traders must be conscious that hackers accessed Okta’s recordsdata from September 28, 2023, by way of October 17, 2023. The breach doubtlessly harm a few of its clients. CFO Tighe mentioned on the corporate’s fourth quarter FY 2024 earnings name:

When analyzing our key metrics, we could not attribute a quantifiable impression from the safety incident on our This autumn outcomes. Whereas not quantifiable, the occasion probably had some stage of impression. We’ll proceed to observe this as we transfer by way of FY ’25.

Since Okta considers itself a significant a part of a company’s safety posture, the breach was an egg on its face for my part. Though the occasion was extreme, presuming no reoccurrences, time ought to heal the injury to Okta’s repute. Nonetheless, within the quick time period, the breach might doubtlessly harm gross sales.

Valuation

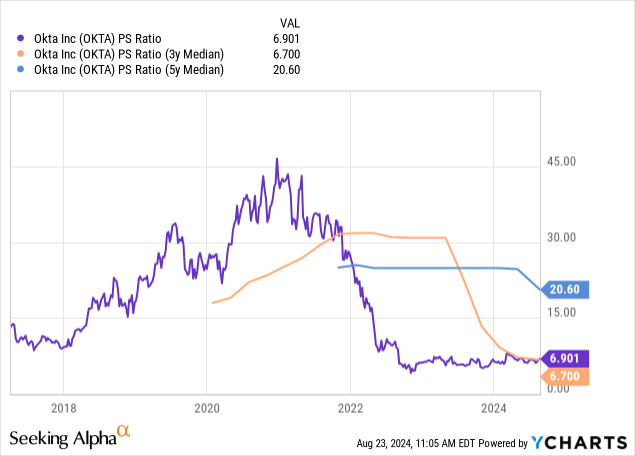

Okta is difficult to worth utilizing many various valuation strategies as a result of it is an unprofitable (GAAP), comparatively early-stage SaaS firm in a downturn. The market can worth a inventory utilizing gross sales when uncertain about how a lot revenue or FCF an organization will finally produce. The TTM P/S ratio might be one of the best ways to worth this inventory, because it has but to make a GAAP revenue. It additionally could also be too early to find out whether or not the corporate is dedicated to increasing its FCF margin or producing constant FCF progress.

Okta has a TTM P/S ratio of 6.9, barely above its three-year median of 6.7 however nicely beneath its five-year median of 20.6. For the reason that firm’s income progress continues to be declining and will take a number of years to rejuvenate income progress, the inventory might be buying and selling at honest worth. Contemplating the chance of a recession holding SMBs again from spending, sluggish income progress, and destructive investor sentiment, the inventory might stagnate round present ranges for the following yr. Moreover, nobody ought to count on the corporate to return to a TTM P/S ratio of 20 any time quickly.

Till two years in the past, Okta had a immediately comparable firm to measure its valuation towards in Ping Id, however that firm went non-public in 2022. The next chart compares Okta’s ahead P/S to a number of different SaaS firms. It is essential to do not forget that not one of the comparisons are apples-to-apples comparisons as a result of every firm is in a unique enterprise. Gross margins can play an element within the P/S ratio wherein the market will award a inventory. SBC and different components may play an element. As an illustration, a excessive gross margin represents a better potential for a corporation producing excessive income. SBC reduces the corporate’s profit-making potential. So, though income progress could also be one of the crucial important components in what P/S ratio the market will award a inventory, it isn’t the one issue, which is why there aren’t any neat guidelines about what P/S ratio the market ought to award a particular income progress fee.

| Firm identify | TTM P/S ratio | TTM gross margin | One-year ahead P/S ratio | Estimated one-year ahead annual income estimated progress fee |

| Crowdstrike | 19.57 | 75.29% | 13.23 | 24.26% |

| Zscaler | 14.45 | 77.85% | 9.3 | 22.43% |

| Snowflake | 9.32 | 67.83% | 8.91 | 22.71% |

| MongoDB | 10.05 | 74.52% | 8.07 | 18.24% |

| Okta | 6.79 | 75.15% | 5.74 | 12.03% |

| Paycom | 5.13 | 82.78% | 4.31 | 11.23% |

Earlier, I mentioned Okta is unlikely to return to a P/S ratio of 20 quickly as a result of it’s unlikely to return to the income progress charges that sustained that P/S ratio. The corporate generated annual income of twenty-two% in its FY 2024. Nevertheless, the corporate gave steering for FY 2025 annual income progress of solely 12% –Yikes! On the chart above, MongoDB has an analogous gross margin to Okta. The market gave MongoDB a P/S ratio of ten for a one-year ahead annual estimated progress fee of 18%. For my part, Okta’s income progress might want to speed up from 12% to the excessive teenagers whereas persevering with to enhance its bottom-line profitability earlier than the market awards it a TTM P/S ratio of 10.0 — a difficult feat. Assuming Okta can return to annual income progress of 15%, the market might award the inventory a P/S ratio of 8.0, which suggests a value of $114.80, round 16% above the August 23 closing value.

Let us take a look at one other approach to worth Okta.

Okta isn’t GAAP worthwhile and has no price-to-earnings (P/E) ratio. Moreover, analysts do not count on it to be GAAP worthwhile within the close to time period. Nevertheless, the corporate achieved annual non-GAAP profitability in FY 2024. The next picture exhibits analysts’ non-GAAP EPS progress estimates and ahead P/E ratios for Okta’s FY 2025 and FY 2026.

In search of Alpha

You may calculate the corporate’s non-GAAP ahead and one-year ahead Worth-to-Earnings Development (“PEG”) ratio utilizing the numbers above. Okta has a ahead PEG ratio of 0.77 (Ahead P/E 40.05 divided by estimated EPS progress of 51.54%) and a one-year ahead PEG ratio of two.77. Buyers with a price mindset contemplate a PEG ratio beneath one undervalued and above one overvalued. Buyers with a progress mentality contemplate a PEG ratio beneath one undervalued, a ratio between one and two pretty valued, and a ratio above two overvalued. Primarily based on these guidelines, worth, and progress traders might contemplate Okta’s FY 2025 estimated EPS progress fee undervalued and its FY 2026 estimated EPS progress fee overvalued. You might interpret these conflicting leads to quite a few methods. Nevertheless, I view these outcomes as inconclusive.

Let us take a look at Okta’s reverse discounted money circulate (“DCF”). I exploit a terminal progress fee of three% as a result of Okta ought to proceed rising its money circulate steadily at that fee after ten years. A reduction fee is the chance price of investing in an organization. Firms with increased danger ranges have increased low cost charges, and decrease danger ranges have decrease low cost charges. I exploit a reduction fee of 10%, representing a median danger stage. I additionally use a levered FCF for this evaluation.

Okta’s Reverse DCF

|

The primary quarter of FY 2024 reported Free Money Stream TTM (Trailing 12 months in thousands and thousands) |

$578 |

| Terminal progress fee | 3% |

| Low cost Charge | 10% |

| Years 1 – 10 progress fee | 12% |

| Inventory Worth (August 23, 2024 closing value) | $99.01 |

| Terminal FCF worth | $1.866 billion |

| Discounted Terminal Worth | $10.275 billion |

| FCF margin | 24.47% |

If the corporate can keep a median FCF margin of 24.5% over the following ten years, it could solely have to develop income by 12% yearly to justify the present inventory value. These numbers are very achievable. The corporate grew income at a 56% compound annual progress fee (“CAGR”) during the last 9 years and a 41.5% CAGR within the earlier 5 years. Okta is without doubt one of the high id options as we speak. In 2023, it was a Chief in Gartner’s (IT) Magic Quadrant™ for Entry Administration for the seventh consecutive yr. It was additionally primary in its skill to execute and third behind solely Microsoft (MSFT) and Ping Id within the completeness of imaginative and prescient. So, the corporate ought to proceed rising its market share.

Administration believes Okta has a complete addressable market (“TAM”) of $80 billion. As of the tip of its first quarter FY 2025, the corporate produced TTM income of $2.36 billion, which is 3% of its TAM.

Okta First Quarter FY 2025 Investor Presentation

Though it might be tough for Okta to maintain income progress on the charges it has prior to now due to important competitors from firms like Microsoft, as soon as spending returns to the IT sector, it ought to nonetheless develop sooner than 12%. If it grows at a 15% fee over the following ten years, it would generate $9.14 billion in annual income in yr 10, or 11.4% of its TAM. Suppose it grows at a 20% CAGR over the following ten years; it would generate round $14 billion in annual income or 17.5% of its TAM. At a 12% CAGR, it could solely generate round $7 billion in yearly income or 8.75% of its TAM.

These figures don’t contemplate that its TAM might develop over the following ten years. So, contemplating the standard of its id merchandise, a 15% annual income progress fee is possible. If Okta maintains a median FCF margin of 24.5% at a median income progress fee of 15% yearly, it implies an estimated intrinsic worth of $123.09, a 24% rise from its August 24 closing value. At a really aggressive 20% annual income progress fee, the estimated intrinsic worth is $177.88.

Okta is a purchase

Id is an important a part of a brand new safety paradigm referred to as Zero Belief, wherein entry is verified and granted primarily based on the consumer’s or system’s id. As firms gravitate to Zero Belief structure, demand for Okta’s options ought to stay wholesome over the medium to long run. Buyers in search of a stable progress firm that ought to outperform over the following three to 5 years because the financial system comes out of the doldrums ought to contemplate including a number of shares of Okta to their portfolio. For the reason that firm might take a yr or two to revive income progress, it makes a perfect candidate for greenback price averaging.

[ad_2]

2024-08-26 17:05:42

Source :https://seekingalpha.com/article/4717156-okta-navigating-economic-headwinds-for-long-term-growth?source=feed_all_articles

{kind=link}

Discussion about this post