[ad_1]

Евгений Харитонов/iStock by way of Getty Photographs

Nordson Company (NASDAQ:NDSN) is ready to publish their Q3 2024 earnings in just some weeks, on August 22, after market shut.

On this article, I thought of together with a evaluation of their current monetary efficiency, protecting some particulars about their current headwinds, significantly within the superior expertise and agricultural sectors.

I may also focus on a few of their strategic initiatives, together with debt discount and up to date acquisition plans. Moreover, I’ll present my view on the corporate’s outlook and valuation.

Lastly, I’ll conclude with the rationale behind my Maintain score.

As at all times, I’ll start my evaluation with a short firm overview for these new to Nordson.

Firm Overview

Nordson is a designer and producer of instruments that dispense supplies like adhesives, coatings, and sealants.

They promote their merchandise to varied industries together with packaging, electronics, medical units, and development.

I thought of together with beneath a listing of their segments, together with a breakdown of web gross sales and working revenue for every phase.

- Industrial precision options: this phase focuses on dispensers of adhesives, coatings, paints, and sealants to industrial, agricultural, and shopper markets.

- Medical and fluid options: this phase contains fluid administration options for medical and high-tech industrial markets.

- Superior expertise options: the merchandise inside this phase embody floor remedy, managed allotting of supplies, and testing & inspection.

| Section | Web Exterior Gross sales (2023) in hundreds of thousands | Working Revenue (2023) in hundreds of thousands |

|---|---|---|

| Industrial Precision Options | $1,391 | $460 |

| Medical and Fluid Options | $660 | $189 |

| Superior Expertise Options | $577 | $101 |

| Whole | $2,628 | $672 |

Creator’s compilation from newest 10-Ok

On condition that they function in additional than 35 international locations, I made a decision to incorporate beneath a breakdown of their annual income per geographical area.

| Geographic Area | Income (2023) in hundreds of thousands |

|---|---|

| Americas | $1,149,760 |

| Asia Pacific | $796,196 |

| Europe | $682,676 |

| Whole | $2,628,632 |

Creator’s compilation from newest 10-Ok

Latest Efficiency

I am going to begin with their current challenges first.

Ongoing pressures within the electronics market throughout Q2 2024 led to a 22% decline in gross sales (YoY) of their superior expertise options phase.

I consider the decline in shopper electronics, which ends up in delayed investments in semiconductor manufacturing, is just not performed but. After seeing the most recent US job report, with unemployment rising above expectations, I consider there are pressures now on the buyer’s disposable revenue.

Moreover, EBITDA for the superior expertise phase was down by 25% YoY.

I’ve to confess that I’m not sweating excessively concerning the EBITDA lower, on condition that they managed to keep up their margin comparatively flat prior to now 12 months. In Q2 2024, this was 21%, in comparison with 22% within the earlier 12 months.

One factor that does make me sweat, is the acquisition of ARAG, which elevated their curiosity bills in Q2 2024 by 94% YoY, and had a direct impression on their complete web revenue, which decreased by $9.6 million in comparison with Q2 2023.

Nevertheless, I view this acquisition as the correct determination in the long run, given the 9% enhance in gross sales of their industrial precision options phase.

Administration did point out in the course of the Q2 earnings convention a current downturn within the agricultural market, resulting in decreased demand and funding in agricultural gear in North America, Europe, and South America.

Nevertheless, I’m involved about how lengthy this downturn will final, given the current dangerous efficiency of agricultural commodities. I consider farmers are holding again investments in new equipment till they see a restoration within the agricultural commodities market.

I thought of together with beneath a screenshot from In search of Alpha, displaying the efficiency of a number of agricultural commodities.

In search of Alpha

With a decline within the double digits over the previous 12 months, I’ve to confess that I’m involved (within the brief time period) about the way forward for agricultural commodities.

Strategic Initiatives

I’ll begin with my favourite initiative from Q2 2024, associated to debt discount.

Within the second quarter, they reported free money move of $108 million, which enabled a virtually $100 million debt discount.

As a fast aspect notice, my funding type favors corporations that use most of their free money move to reinvest of their enterprise, particularly after they retire debt, somewhat than paying dividends to shareholders.

I’m not saying that I do not like dividend shares, however I favor a rational free money move allocation that isn’t restricted by the mentality of accelerating dividend funds simply because shareholders like seeing dividends going up 12 months after 12 months.

Contemplating that Nordson additionally pays dividends, and these have been rising consecutively 12 months over 12 months, I’m doubly impressed.

Regardless of ARAG working primarily within the agricultural sector, and contemplating the current downturn talked about within the earlier part, I consider that when agricultural commodities begin to recuperate, ARAG is properly positioned to drive important progress given its sturdy market presence within the European market.

Moreover, I really feel constructive concerning the current announcement to amass Atrion Company for $460 per share. I consider this acquisition is more likely to undergo earlier than the top of the 12 months, which is able to develop Nordson’s medical portfolio on condition that Atrion generates round $169 million in annual income.

I’ll control the standing of this acquisition in the course of the subsequent earnings launch.

Outlook

I’ve to confess that their weekly chart, issues look favorable.

Buying and selling View

There’s a clear upward development, which in my opinion, is supported by sturdy financials, with web revenue and EBITDA rising since 2017.

Buying and selling View

Moreover, as a contrarian investor, I just like the 15% selloff for the reason that publication of their Q2 2024 outcomes.

I consider shareholders overstated the impression of the current headwinds, and are over pessimistic concerning the up to date steering offered by administration, with a 0% – 2% vary for income progress.

Nevertheless, regardless of believing in Nordson’s long-term progress as a result of strategic initiatives talked about earlier than, I’m not assured in at this time’s share value… And, primarily based on the lack of current insider shopping for exercise, and share buybacks, I consider administration is just not assured both.

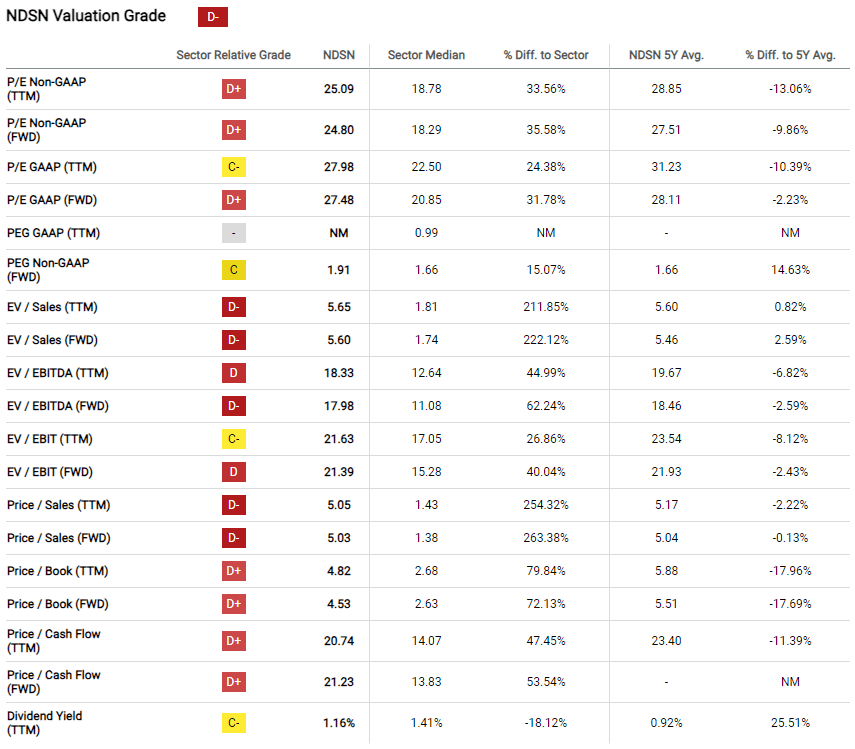

Moreover, a fast have a look at their valuation ratios exhibits that the majority of their ratios are above the sector median. I thought of together with this comparability beneath, though I’ll point out that I largely solely have a look at value to gross sales, EV/EBITDA, and value to ebook worth.

Buying and selling View

Conclusion

In my opinion, Nordson is going through short-term headwinds, significantly within the superior expertise and agricultural segments, because of declining electronics gross sales, and a downturn within the agricultural market.

The acquisition of ARAG led to a big enhance in curiosity bills, which I consider will negatively impression their web income for 2024, though I see the 9% enhance in gross sales as a constructive signal for long run progress within the industrial precision phase, as soon as the agricultural commodities recuperate from their decline.

When it comes to their strategic initiatives, I extremely favor their debt discount of $100 million, particularly after the rise in debt as a result of ARAG acquisition.

Moreover, I really feel assured about their means to generate free money flows, and extremely favor administration’s prudent allocation in direction of debt discount, somewhat than solely specializing in dividends.

However, I’m not proud of the present share value, given the valuation ratios, and the dearth of current insider shopping for exercise and share buybacks.

Subsequently, I price this inventory as a Maintain till I see extra pores and skin within the recreation by administration, and we get extra information on the acquisition of Atrion earlier than the top of this 12 months.

[ad_2]

2024-08-08 06:00:59

Source :https://seekingalpha.com/article/4711944-nordson-earnings-preview-headwinds-still-blowing-compelling-strategic-initiatives?source=feed_all_articles

{kind=link}

Discussion about this post