[ad_1]

Erik Isakson

Funding Thesis

Modine Manufacturing’s (NYSE:MOD) administration sees the potential to generate roughly $1.1 billion in knowledge middle cooling income inside three years. That might triple its present knowledge middle gross sales and almost double its present complete Local weather Options income. It would additionally put the corporate someplace within the vary of producing $3.3 billion yearly. The unbelievable progress and continued acceleration of knowledge middle cooling gross sales, a strategic acquisition that, I consider, has given Modine a possible moat or a minimum of a robust aggressive benefit, and increasing margins give me confidence that the corporate is usually a winner within the knowledge middle cooling area. If Modine can accomplish the kind of income progress that administration speaks about, the inventory may very well be an amazing worth in the present day for long-term traders. After ranking MOD a maintain in my final article, I now contemplate Modine a purchase and have opened a starter place within the firm.

Enhancing Monetary Outlook

Modine is present process a strategic shift, which it calls its 80/20 precept. MOD’s 80/20 adjustments precipitated a significant enchancment in its monetary trajectory. The corporate is divesting from underperforming companies and shifting its focus into larger progress and better margin companies. Section income has flipped from being pushed largely by Efficiency Expertise to now being pushed by Local weather Options. It is a very constructive signal for continued margin enlargement. The Local weather Options enterprise consists of knowledge middle cooling, which generates considerably larger gross and working margins. That is the world of the enterprise I’m specializing in in the meanwhile, as Modine’s administration has talked about that its goal for its knowledge middle cooling enterprise is roughly $1.1 billion in about three years’ time. If this occurs, I consider Modine can rival the present free money circulate margins of Vertiv (VRT) and Trane Applied sciences (TT). FCF margins of 13% may help spectacular shareholder returns.

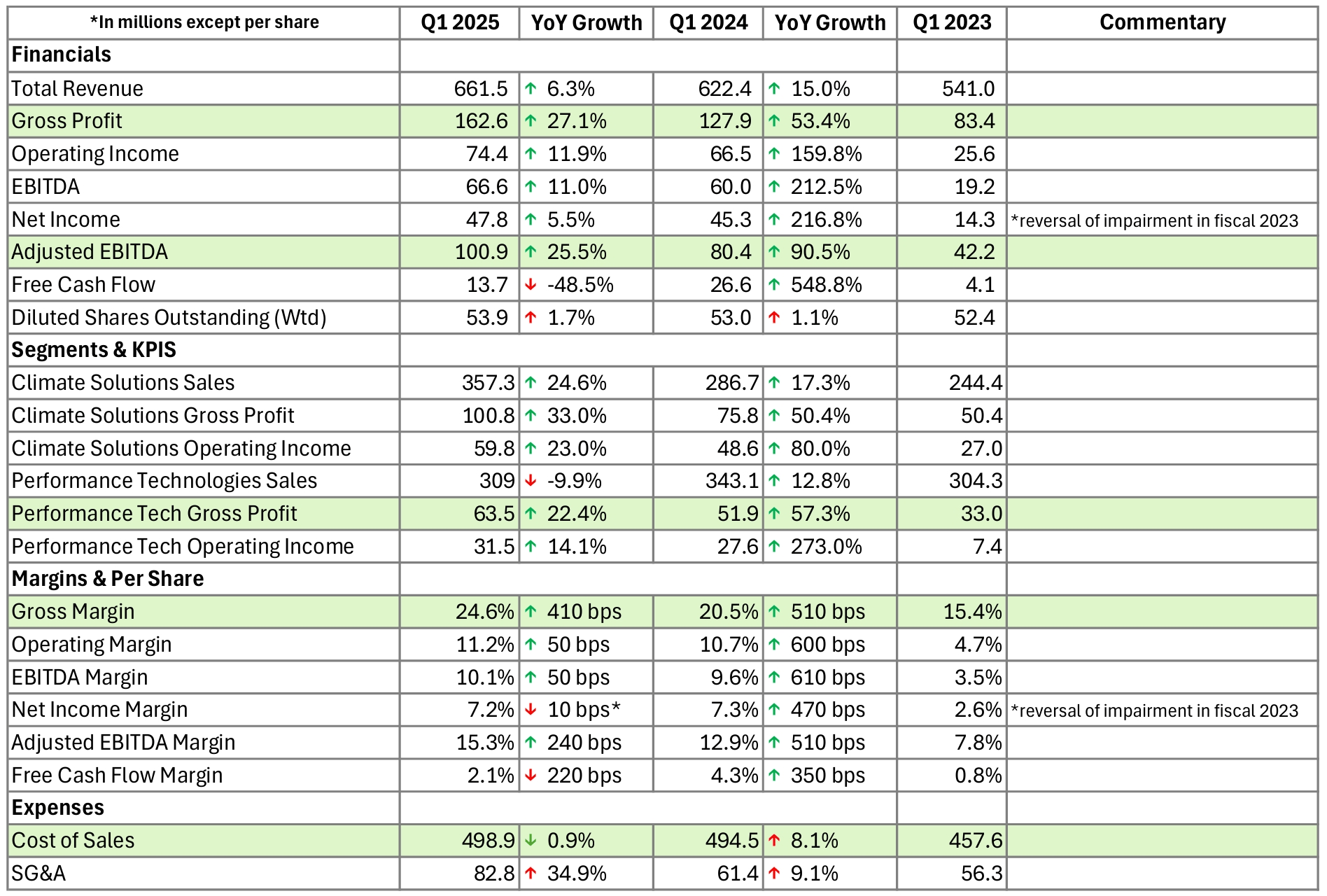

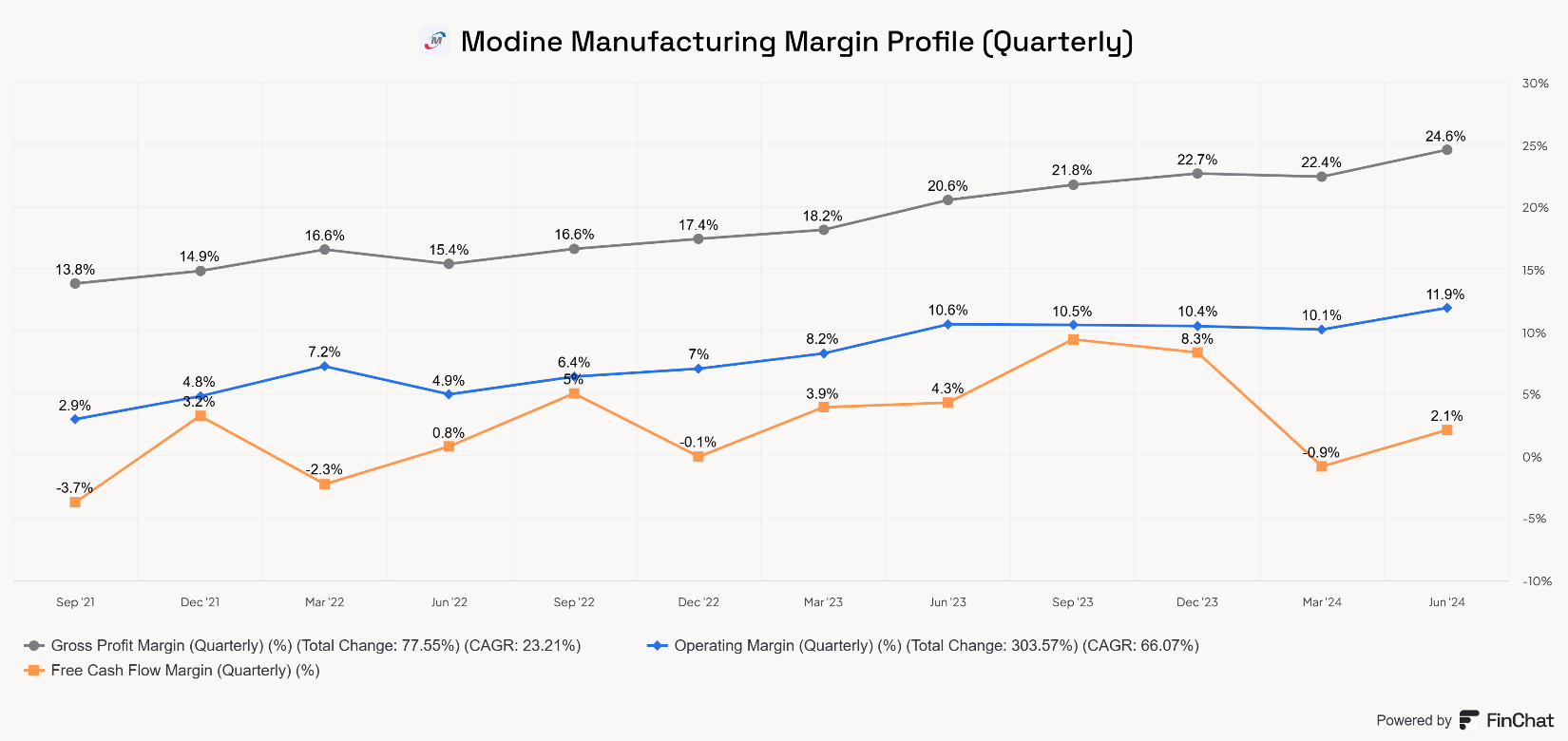

Within the desk beneath, you’ll be able to see that Modine has been capable of obtain spectacular progress in gross revenue and margin, and adjusted EBITDA and margin. Its Local weather Options (CS) section skilled unbelievable income progress (24.6% YoY in Q1) and gross revenue (33.0% in Q1). The Efficiency Applied sciences (PT) section is being shrunk by promoting off underperforming enterprise, nonetheless, regardless of a decline in PT gross sales, Modine grew PT gross revenue by 22.4%, displaying elevated effectivity from its 80/20 adjustments. Modine expects a flattish income outlook, with larger margins in its PT section and continued acceleration in its CS section.

Modine’s Q1 Monetary and KPI Desk (Creator-generated desk, knowledge from SEC filings and transcripts)

Adjusted EBITDA is a extra acceptable measure of Modine’s latest progress on account of a reversal of an impairment cost in 2023 and the unwinding of a few of its legacy automotive companies. Adjusted EBITDA margin has expanded from 7.8% in Q1 2023 to fifteen.3% in Q1 2025. The important thing factor to search for in Modine’s operational efficiency would be the magnitude of the shift in income in the direction of knowledge middle cooling options and continued margin enlargement.

Progress in Knowledge Heart Gross sales and Increasing Margins

Regardless of exiting a few of its Efficiency Tech companies, Modine continues to develop complete income on the power of its CS section, pushed by an acceleration in knowledge middle cooling income.

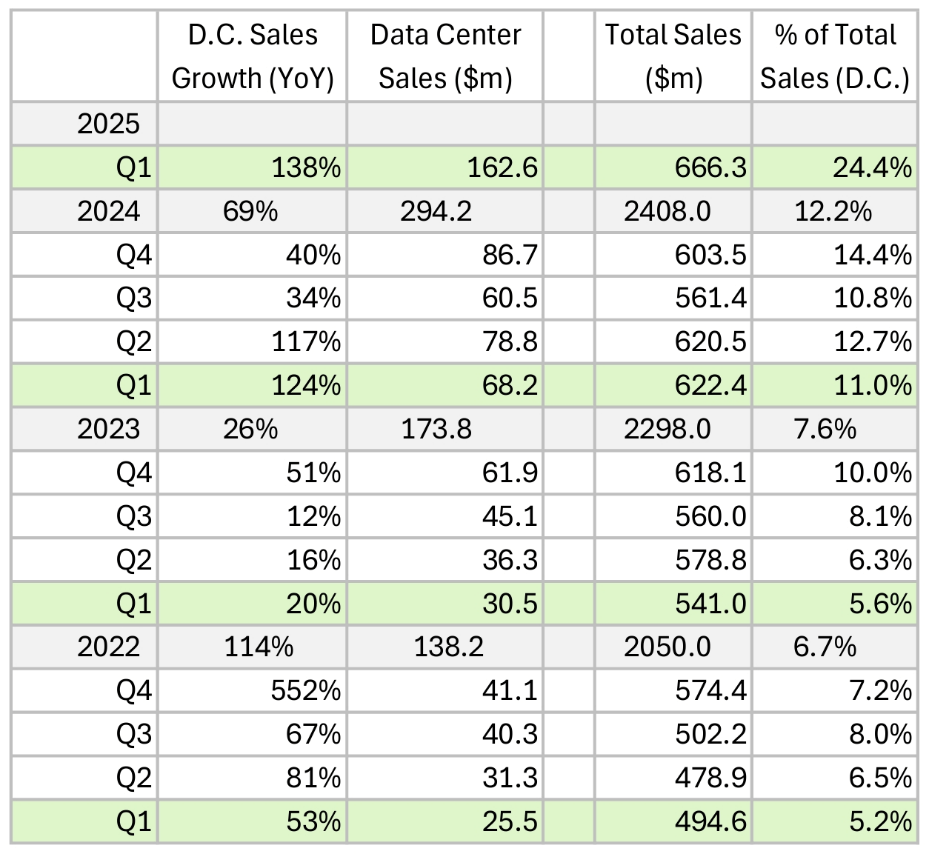

A great quantity of Q1 knowledge middle gross sales progress comes from the Scott Springfield Manufacturing (SSM) acquisition; nonetheless, throughout the Q1 name, administration acknowledged that natural knowledge middle progress almost doubled YoY. Modine acquired SSM to achieve entry to a expertise that it could not present. Now, with the 2 corporations working collectively, the advantages of each ought to kick in. The mixing of SSM and its customized air dealing with models (AHUs) will broaden Modine’s capabilities and permit it to higher serve hyperscale knowledge facilities, strengthening its place in a high-growth vertical. It additionally gained Modine entry to new buyer relationships by including a hyperscale buyer, doubtlessly opening the door to new giant knowledge middle prospects now that the corporate has a seat on the desk. These relationships could also be one of the vital vital aggressive benefits within the knowledge middle cooling market, as important switching prices could also be related to hybrid knowledge middle cooling agreements. Administration has primarily instructed us that the 2 corporations mixed might be stronger than each individually.

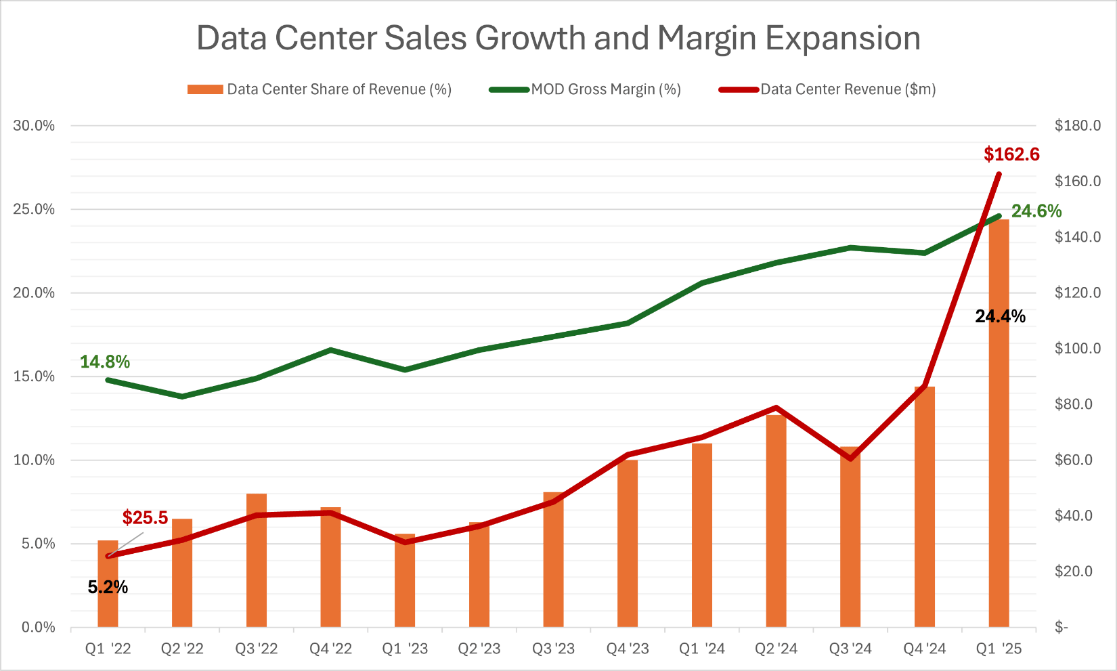

Knowledge middle cooling gross sales have greater than 6x’d since Q1 of 2022, with quarterly gross sales rising at a CAGR of 85.4% over the two-year interval proven beneath. As knowledge middle gross sales have grown, Local weather Options gross margins have improved from 20.6% to twenty-eight.2%, and complete gross margin has expanded from 15.4% to twenty.4%. Knowledge middle gross sales now make up 24.4% of complete income. This determine was solely 5.2% in the identical interval three years in the past.

Modine’s Knowledge Heart Gross sales Progress (Creator-generated desk, knowledge from SEC filings and transcripts)

The chart beneath additional illustrates the connection between knowledge middle gross sales and gross margins. As knowledge middle gross sales (pink line) have grown from $25.5 million to $162.6 million, gross margin (inexperienced line) has considerably expanded and the share of income coming from knowledge middle gross sales (orange bar) has exploded larger.

Creator-generated desk, knowledge from SEC filings and transcripts

How lengthy will this progress proceed? Capex into knowledge middle new builds and expansions continues to be ongoing. These are giant tasks that take time to plan, fund, approve, and construct, this course of ought to proceed to play out for a number of years a minimum of. Dominion Vitality (D) not too long ago stated that new giant knowledge facilities requiring greater than 100 megawatts of electrical energy would withstand seven-year delays because of the lack {of electrical} infrastructure help. Importantly, this won’t have an effect on tasks already within the pipeline. Dominion serves electrical energy in Virginia, one of many extra vital locations within the USA for knowledge facilities. In my article about NextEra Vitality (NEE) in June, a part of my thesis revolved across the long-term progress pipeline for knowledge middle construct outs. Maybe not coincidentally, NEE says that it expects renewables to develop about 3x over the following seven years as in comparison with the prior seven-year interval. This progress in renewables ought to assist help the power to proceed constructing giant knowledge facilities past the seven-year interval Dominion talked about.

The opposite factor that ought to help the power to construct knowledge facilities regardless of the present and near-term limitations of {the electrical} grid is the adoption of liquid cooling options for knowledge infrastructure. As an example, analysis and business articles have mentioned how superior cooling expertise will assist knowledge facilities turn out to be extra environment friendly and that liquid cooling is a essential half of this shift. This demand ought to present a possibility for Modine to proceed constructing on its latest success in constructing an organization with the potential to supply a full suite of knowledge middle cooling expertise.

Free Money Movement Evaluation

In Q1, MOD’s FCF (outlined merely as OCF minus Capex) was $13.7 million, whereas TTM FCF was $113.2 million. Nonetheless, TTM FCF numbers will not be the most effective measure of the corporate’s earnings skill as a result of MOD has made important investments in progress and accelerated income from its knowledge middle cooling section. Due to this, the money circulate assortment from its knowledge middle income could also be considerably delayed for now.

In Q1, OCF was negatively impacted by working capital, with adjustments in accounts receivable (-$18.1 million) and different web working belongings (-$32.6 million) mixed to lower OCF by $50.7 million. On the flip facet, MOD solely benefitted from $20.6 in different working capital gadgets, resembling favorable adjustments in stock, accounts payable, and different web working belongings. I do not wish to make daring assumptions about working capital except I’ve a extremely agency grasp of an organization’s accounting. Nonetheless, within the case of Modine, I really feel assured in its potential to enhance OCF within the coming quarters as a result of knowledge middle cooling gross sales are accelerating and driving margin enlargement. Moreover, FCF was impacted by bigger than traditional capex associated to acquisitions and investments in progress. Capex in Q2 was $26.8 million.

We are able to depend Capex in opposition to MOD’s money flows, however the Capex used to combine Scott Springfield and TMGCore must be seen a long-term funding reasonably than a right away expense, regardless of its accounting therapy. Since these should not capitalized, they affect earnings and free money circulate in the present day. Nonetheless they symbolize long-term progress investments that, beneath completely different accounting therapy, can be capitalized and expensed over their helpful life interval. Over time, as Capex decreases, earnings and free money circulate ought to theoretically enhance, assuming these acquisitions contribute to progress. Fortunately, there are a minimum of early indicators that the SSM acquisition already is.

Returns on Invested Capital and Capital Employed

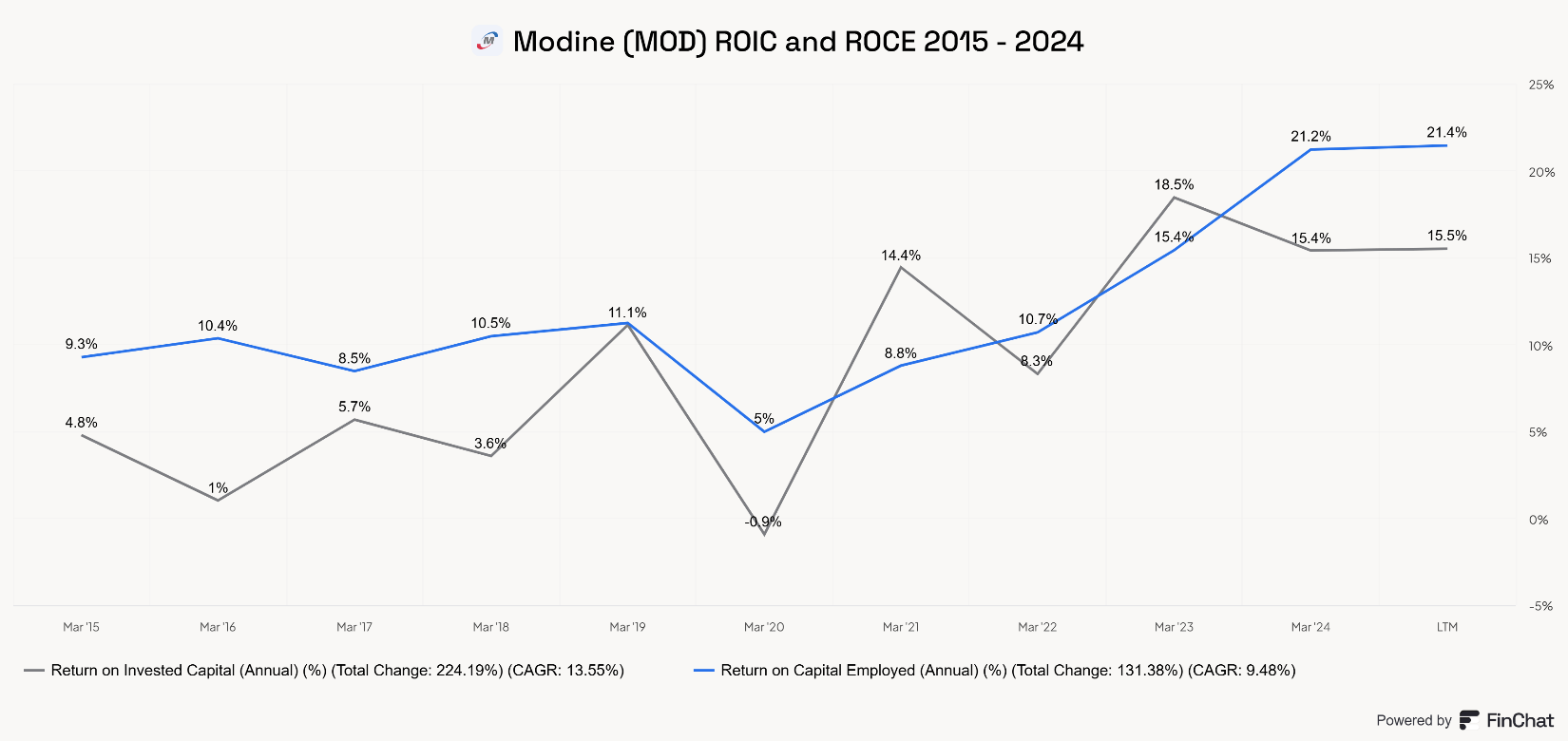

Modine has proven its growing effectivity by means of two crucial measures, ROIC and ROCE. These capital effectivity metrics will go a great distance in indicating if the corporate is bettering the returns it will get on its investments in acquisitions, Capex, and R&D. The corporate has exhibited wholesome and bettering ROIC and ROCE, as seen beneath.

FinChat

Firms that keep wholesome capital effectivity metrics (significantly ROIC and ROCE) usually tend to ship sturdy shareholder returns. Modine has performed this, and this could help bettering free money circulate era sooner or later.

FCF Potential

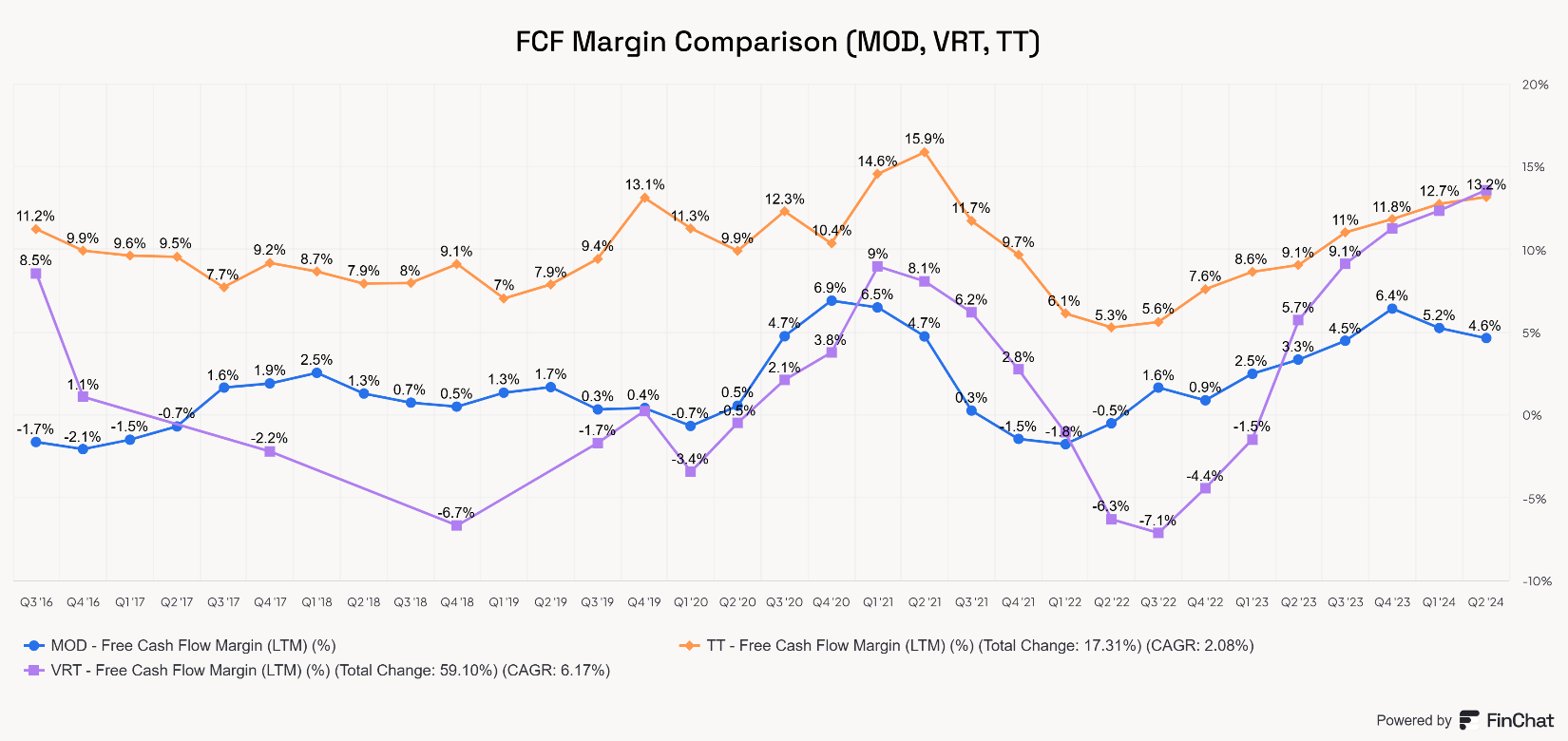

Maybe our greatest comps are Vertiv and Trane Applied sciences. VRT and TT are completely different companies. Trane is established and really numerous, like Modine is. With completely different enterprise segments that make knowledge middle cooling a rising a part of its enterprise however not but a serious income. Vertiv is the quicker rising counterpart to Modine, however differs in that it’s centered primarily on superior cooling techniques options. With the emergence of knowledge middle cooling and liquid cooling as a income for Modine, I see the enterprise aiming to be someplace between Vertiv and Trane, with a diversified mannequin and an growing reliance on knowledge middle cooling.

Each TT and VRT maintain TTM FCF margins simply north of 13%. MOD’s TTM FCF margin is barely 4.6%, with a peak of 6.4% as of the top of fiscal Q3 of 2024 (12/31/2023). Given the enlargement of MOD’s gross and working margins and the truth that a secular progress development and rightsizing of its enterprise is pushing this enlargement, I see 13% as an affordable goal for FCF margins.

FinChat

If Modine can get to a 13% FCF margin throughout the subsequent few years, that may seemingly make the inventory fairly low-cost proper now. Margin enlargement may very well be supported by continued progress in knowledge middle gross sales, decrease integration prices and the synergies or advantages from its latest acquisitions, significantly the Scott Springfield acquisition.

FinChat

Valuation

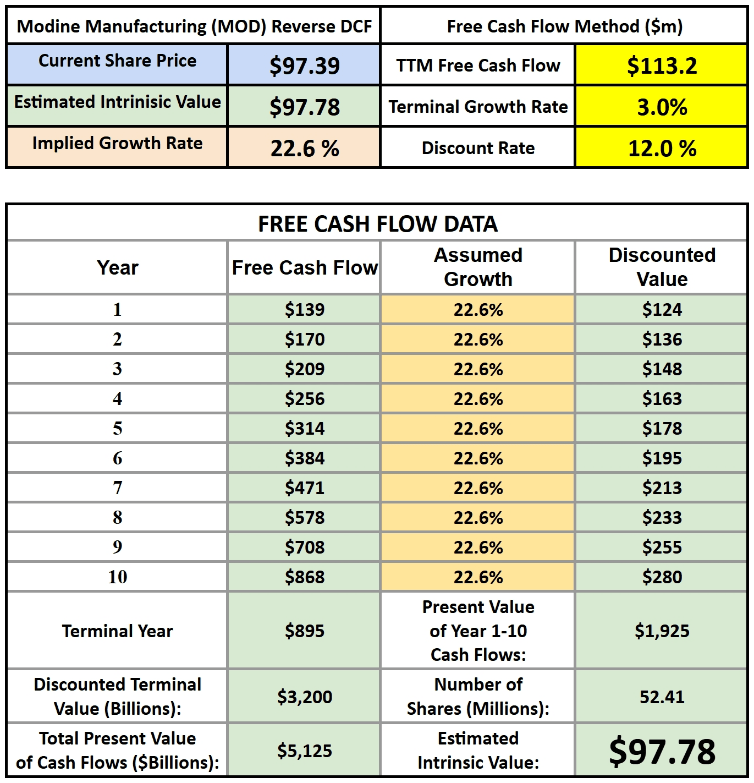

If we use a primary reverse DCF calculator and Modine’s TTM FCF of $113.2 million, a terminal progress price of three.0%, and a reduction price of 12.0%, Modine must develop free money circulate at 22.6% over a ten-year interval. I selected a 12% low cost or hurdle price as a result of I consider that may be a market-beating inventory. The terminal price of three% whereas larger than GDP, seems to be affordable because of the potential tailwinds related to knowledge middle cooling and HVAC/R markets.

Reverse DCF – Modine (MOD) (Creator-Generated Reverse DCF)

The easy reverse DCF may overstate Modine’s must develop free money circulate from its present margins. What if the corporate can proceed to dramatically broaden its margins within the subsequent 12 months or two?

Modine’s latest restructuring for progress and effectivity and the explosion in knowledge middle gross sales, the corporate doesn’t but seem like optimized without cost money circulate era. Let’s return to my assumption that Modine has the potential to match the 13.0% FCF margin that TT and VRT maintain.

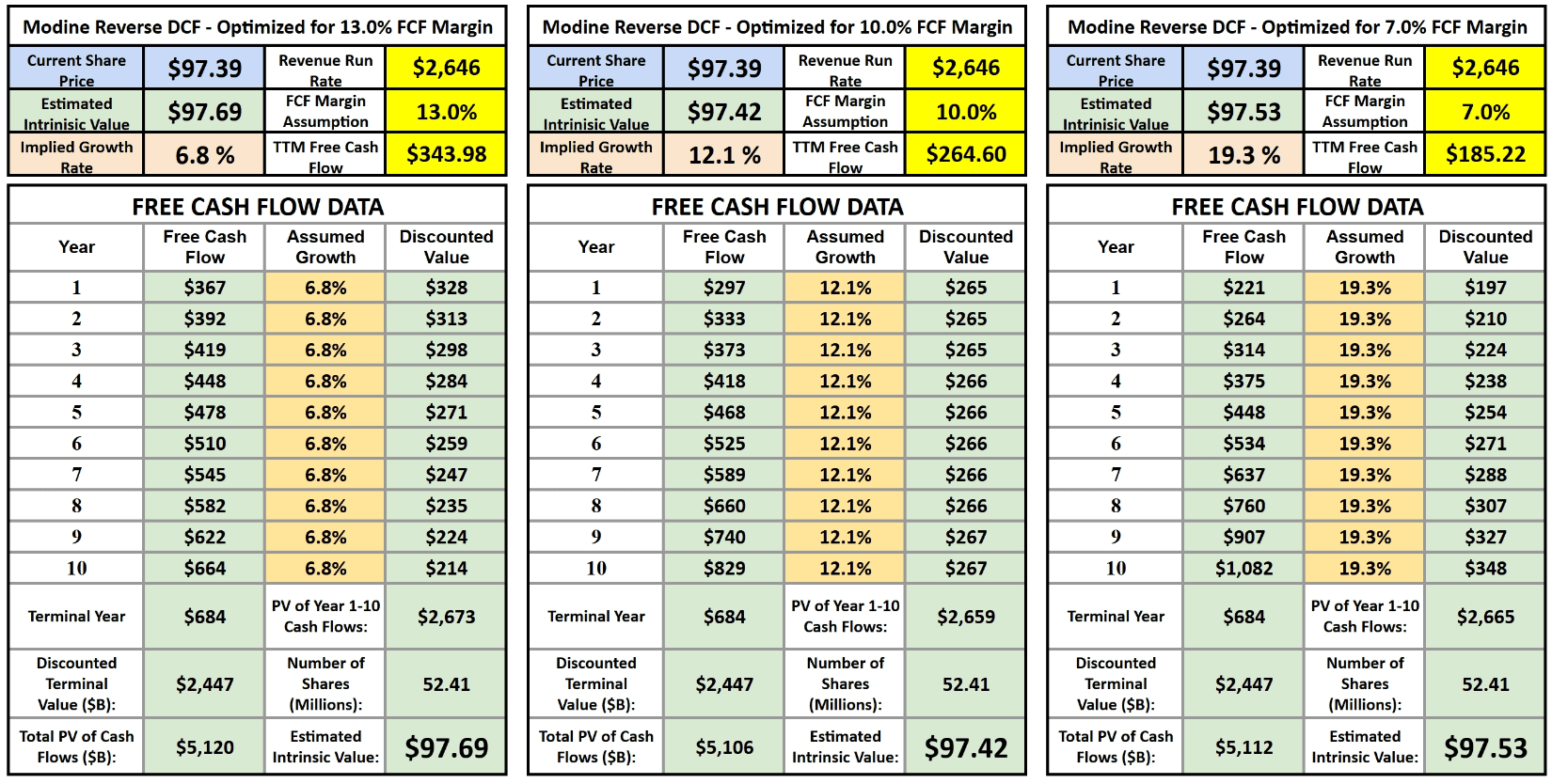

Now, let’s conduct a valuation train, pretending that Modine is already optimized for a free money circulate. I consider 7% to 13% is an acceptable vary for MOD’s medium-term FCF margin. If we assume that the corporate was already optimized for FCF margin and that the margin remained regular for ten years, we will estimate the income progress price required for MOD inventory to be pretty valued utilizing a reverse discounted money circulate mannequin. I need to stress that this isn’t an correct measure of intrinsic worth, simply an estimate of what can be required beneath extra optimum profitability.

If FCF margin have been already 13%, given its twelve-month income run price of $2,646 million in income, Modine can be producing $344 million in FCF and solely must develop income at a 6.8% CAGR to be buying and selling at its estimated intrinsic worth. If Modine have been optimized for 10.0% FCF margins, the required income progress price can be 12.1% yearly, and at 7.0% FCF margin, Modine must develop revenues at a 19.2% CAGR. Every mannequin makes use of a 12.0% low cost price and three% terminal progress price.

I must explicitly state that this mannequin makes assumptions that would look ridiculous in both path sooner or later, and must be thought-about a instrument to guage the potential valuation of Modine beneath optimum profitability that has but to be attained.

3-State of affairs Optimized Reverse DCF – Modine (MOD) (Creator-Generated Reverse DCF)

Combining the 2 fashions used factors to, Modine as a possible market-beating performer within the coming years. As a result of I consider margins will proceed increasing dramatically within the coming years and income will develop from right here, I feel the potential lies someplace between the standard reverse DCF mannequin used and the 3-scenario optimized without cost money circulate reverse DCF mannequin I created.

Given the enlargement of margins that Modine is seeing with the explosion in knowledge middle cooling gross sales, it appears affordable to imagine margins proceed to broaden. The query is, how vast can they broaden? That will rely upon Modine’s skill to create or keep a moat.

Modine’s Moat

My willingness to place religion into the long-term funding thesis for Modine depends on the corporate’s skill to create a moat. In MOD’s case, aggressive benefits may come from giant buyer relationships, patented expertise, and switching prices. MOD is experiencing fast progress from its superior cooling division, led by unbelievable progress in its knowledge middle cooling enterprise and bolstered by the acquisition of SSM.

It is laborious to find out if Modine truly has the potential to develop a moat in liquid cooling. I do not assume it is a winner-take-all business, nevertheless it’s vital to find out if MOD has the potential to a minimum of acquire and keep a number one place within the superior cooling market.

The market has a number of key gamers, resembling LiquidStack (with investments from TT) and Vertiv, in addition to a bunch of different rivals, a few of whom lack the superior capabilities of these talked about above. The market can also be experiencing huge capital inflows from huge tech. This bodes properly for the liquid cooling business and Modine, nevertheless it additionally may invite elevated competitors. Due to this, it’s important for Modine to carry some form of moat to take care of its main place out there.

To me, a moat is such a robust aggressive benefit that it may be sustained over time, even when attacked by different corporations. The sources of aggressive benefits for Modine may come from the quantity of R&D required to enter the liquid cooling market. This might restrict entry into the area for brand new rivals and discourage bigger, diversified HVAC/R corporations from getting instantly concerned within the course of. One other aggressive benefit may come from relationships with knowledge middle suppliers or one or two hyperscale corporations actively spending huge quantities of cash to construct their knowledge middle capabilities. Switching from one cooling supplier to a different might require steep switching prices in the best way of expense and downtime.

Conclusion and Dangers

I consider Modine has sturdy aggressive benefits in all the kinds cited above, however I must study extra about how sustainable this can be. That is what prompted me to take a starter place within the firm following its latest pullback beneath $100 per share.

The dangers to my thesis are that the info middle cooling market lacks sustainable progress if high-performance computing functions fail to ship ample returns on funding for hyperscalers. Nonetheless, it seems that these investments are being made and won’t decelerate for a number of years. As soon as these investments are in place, I consider Modine’s progress inflection could have taken place.

I perceive the chance that MOD’s inventory value may pull again additional as market sentiment might bitter from right here, particularly contemplating the slowing of progress charges seen in Nvidia (NVDA) and the belief that generative AI shares aren’t going to develop linearly.

Nonetheless, after digging deeper into MOD’s funding thesis, I see higher potential for the corporate to proceed increasing margins and rising free money circulate, and I consider the market might not totally notice this potential proper now. I price the inventory a purchase for long-term investing methods and would contemplate upgrading to a robust purchase if the share value falls additional with out my funding thesis being compromised.

[ad_2]

2024-09-09 07:57:00

Source :https://seekingalpha.com/article/4719860-modine-looks-like-a-buy-after-further-analysis?source=feed_all_articles

{kind=link}

Discussion about this post