[ad_1]

P_Wei

Martin Midstream (NASDAQ:MMLP) is presently the main focus of two separate non-binding gives. One of many gives is a $3.05 per unit money supply from Martin Useful resource Administration Company, and the opposite one is a $4.50 per unit money supply from Nut Tree Capital Administration and Caspian Capital.

Martin’s Q2 2024 outcomes have been strong, with its adjusted EBITDA barely exceeding expectations regardless of a $2+ million destructive affect from a few accidents.

This reinforces my perception that Martin’s intrinsic worth is round $4.35 per unit (based mostly on its projected year-end 2024 internet debt), whereas it might be able to cut back its internet debt by $1 per unit in 2025.

Negotiations are nonetheless ongoing, however I can envision a believable state of affairs the place Martin Useful resource Administration Company will increase its bid to $4.00 to $4.50 per unit and a deal will get executed round late 2024 to early 2025.

Present Affords

Nut Tree Capital Administration and Caspian Capital elevated their supply for Martin Midstream’s frequent models to $4.50 in money in July 2024. They beforehand made a money supply of $4.00 per unit in June 2024.

Martin Useful resource Administration Company (which owns Martin Midstream’s basic associate by way of subsidiaries) made a money supply of $3.05 per unit again in Might 2024. The Q2 2024 earnings name talked about that negotiations have been ongoing between Martin Midstream Companions’ Conflicts Committee and Martin Useful resource Administration Company’s advisory agency. Nonetheless, there was no timeframe about when these negotiations can be accomplished (whereas the negotiations might additionally fall by way of).

Martin Useful resource Administration Company indicated that it was solely serious about buying all of Martin Midstream’s excellent frequent models, and that it was not serious about promoting its stake in Martin Midstream or pursuing different strategic options.

Martin Useful resource Administration Company successfully owns roughly 26% of Martin Midstream’s frequent models, together with the quantity owned by Ruben Martin III.

I’m reminded of one other instance the place an MLP was acquired by its basic associate. Blueknight Power Companions obtained a proposal from its basic associate Ergon in October 2021 and finally agreed to an improved supply from its basic associate in April 2022, six and a half months later.

The same timeline would end in some information in December 2024, though every state of affairs is completely different.

Accident Prices

Martin’s Q2 2024 outcomes took a $2 million hit from a few accidents throughout the quarter. Martin’s marine transportation division had a $0.5 million casualty loss reserve as a consequence of a Might 2024 bridge allision (an accident involving just one transferring object) in Galveston, Texas. In the Galveston incident, a tugboat misplaced management of a few barges and one among Martin’s barges ended up hitting and damaging a bridge. The $0.5 million represents the sum of two associated insurance coverage deductibles.

Along with the $0.5 million casualty loss reserve, Martin’s marine transportation division additionally noticed decrease fleet utilization as a result of collision.

Martin’s Terminalling and Storage division noticed a $1.5 million destructive affect from the crude oil spill from the pipeline connecting Martin’s Sandyland Terminal to its Smackover refinery.

The spill was estimated at beneath 2,500 barrels of oil, and the $1.5 million represents the deductibles beneath the insurance coverage insurance policies.

Q2 2024 Outcomes

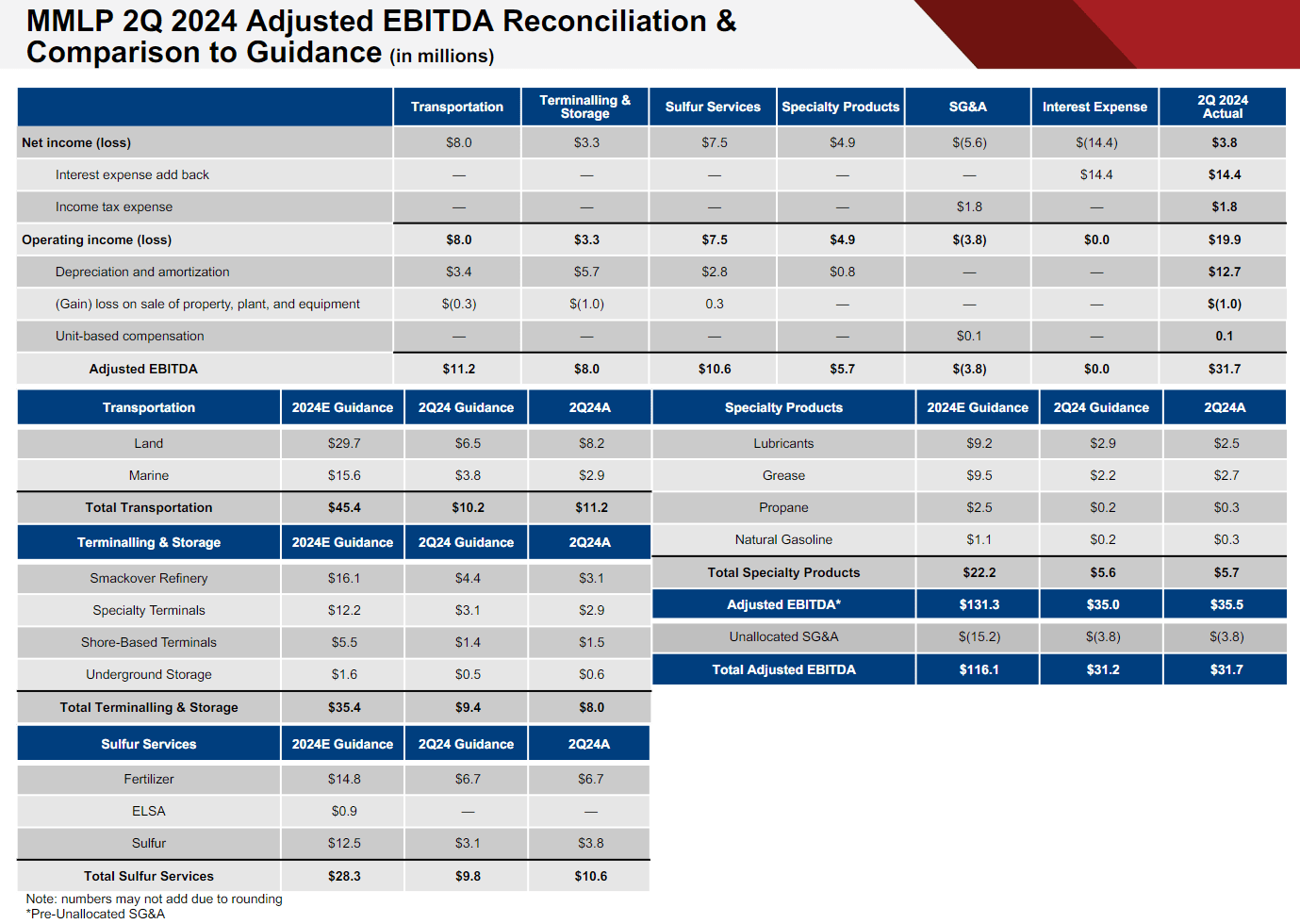

Martin Midstream’s Q2 2024 outcomes have been strong because it generated $31.7 million in adjusted EBITDA versus steerage for $31.2 million in adjusted EBITDA. This got here regardless of the $2+ million hit from the accidents.

Martin’s sulfur companies division rebounded after some challenges in Q1 2024, whereas Martin’s land transportation division continued to be robust.

Martin’s marine transportation division missed its EBITDA steerage by $0.9 million, attributable to the $0.5 million in insurance coverage deductibles and enterprise disruptions attributable to the accident.

Martin’s Q2 2024 EBITDA (mmlp.com (Q2 2024 Presentation))

Martin’s Terminalling and Storage division’s outcomes have been $1.4 million lower than its EBITDA steerage, and this may be attributed to the $1.5 million in insurance coverage deductibles associated to the oil spill.

Notes On Valuation

I beforehand estimated Martin’s worth at round $4.35 per unit based mostly on an EV to 2025 adjusted EBITDA a number of of 5.0x, together with $425 million in year-end 2024 internet debt.

Martin’s enterprise outcomes are typically monitoring in line with expectations, in order that estimated worth stays unchanged for now. Martin’s 1H 2024 EBITDA ended up about $0.6 million under its preliminary steerage, but additionally was affected by $2.0 million in accident-related costs.

If Martin does not improve its distribution, it seems doubtlessly able to decreasing its internet debt by $1 per unit (near $40 million) in 2025. This may make its worth roughly $5.35 based mostly on the same a number of and $385 million in year-end 2025 internet debt.

Assuming that Martin’s enterprise performs as presently anticipated throughout the remainder of 2024 and 2025, it could probably get costlier for Martin Useful resource Administration Company to mount a future bid if it ends negotiations with out a deal.

On condition that Nut Tree Capital Administration and Caspian Capital’s present $4.50 supply is 48% greater than Martin Useful resource Administration Company’s unique $3.05 supply, it additionally appears fairly unlikely that the unique $3.05 supply may very well be justifiably accepted.

Since Martin Useful resource Administration Company is tired of promoting its models, different gives are unlikely to be accepted except there was a considerable overpayment concerned.

Martin Midstream might doubtlessly be capable to justify accepting a proposal from Martin Useful resource Administration Company that a minimum of matches the primary supply from Nut Tree and Caspian Capital.

Thus, I consider there’s a good probability that Martin Useful resource Administration Company will increase its supply and {that a} deal finally will get made within the $4.00 to $4.50 per unit vary by late 2024 to early 2025.

That might be comparatively truthful (in comparison with my estimated worth for Martin) and would nonetheless permit Martin Useful resource Administration Company to get the advantages of the projected improve in free money stream subsequent 12 months.

Conclusion

Martin Midstream has attracted a competing bid that’s now 48% greater than Martin Useful resource Administration Company’s unique bid. Martin Useful resource Administration Company’s shut ties to Martin Midstream imply {that a} competing bid is unlikely to be accepted except there was a considerable overpayment.

The competing bid does imply that Martin Useful resource Administration Company probably wants to extend its bid if it desires to get a deal executed. I estimate Martin Midstream’s truthful worth at round $4.35 per unit based mostly on its projected year-end 2024 internet debt, and consider {that a} $4.00 to $4.50 per unit supply from Martin Useful resource Administration Company can be sufficient to get a deal executed.

[ad_2]

2024-09-04 06:03:31

Source :https://seekingalpha.com/article/4718809-martin-midstream-partners-stock-increased-bid-needed-martin-resource-management?source=feed_all_articles

{kind=link}

Discussion about this post