[ad_1]

onurdongel

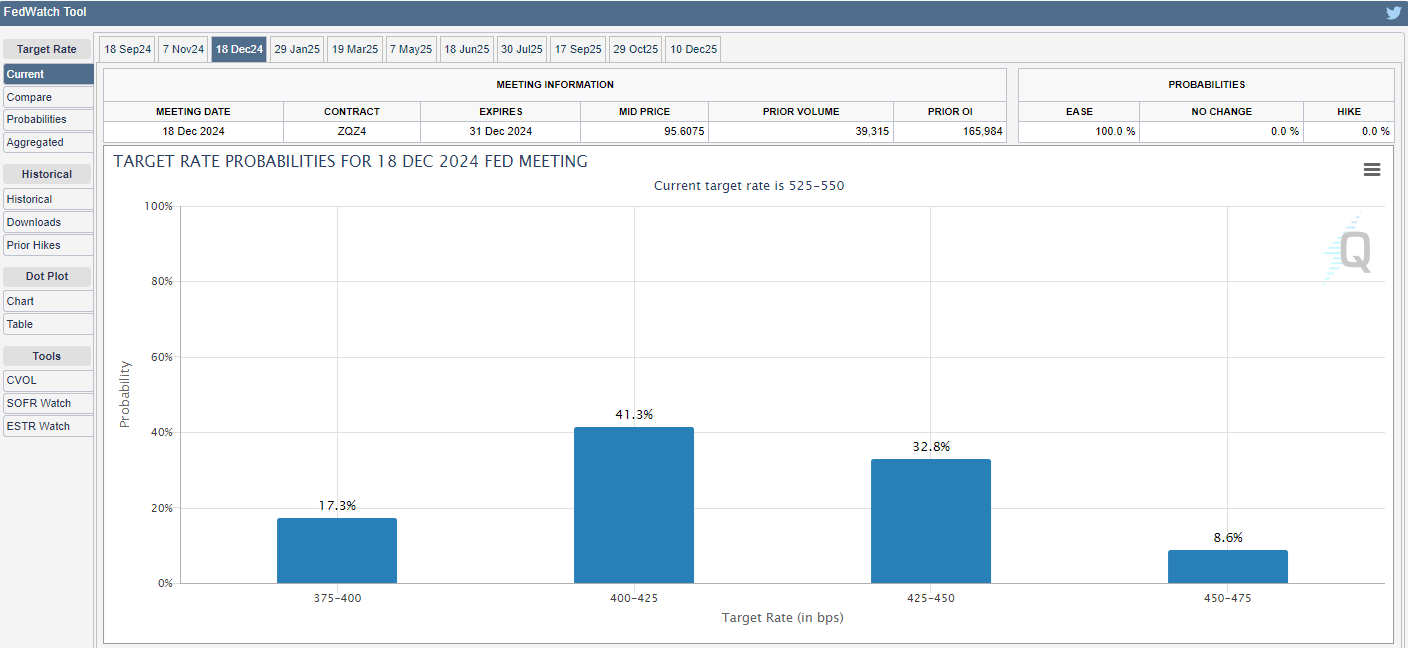

The Kayne Anderson Power Infrastructure Fund (NYSE:KYN) is a closed-end fund that invests primarily in midstream companies and grasp restricted partnerships. That is an asset class that will grow to be extra interesting over the approaching weeks and months because the Federal Reserve is anticipated to start reducing rates of interest later this month. It’s unsure how far it can cut back rates of interest total, however the market is favoring 5 25-basis level cuts by the top of 2024:

Chicago Mercantile Alternate

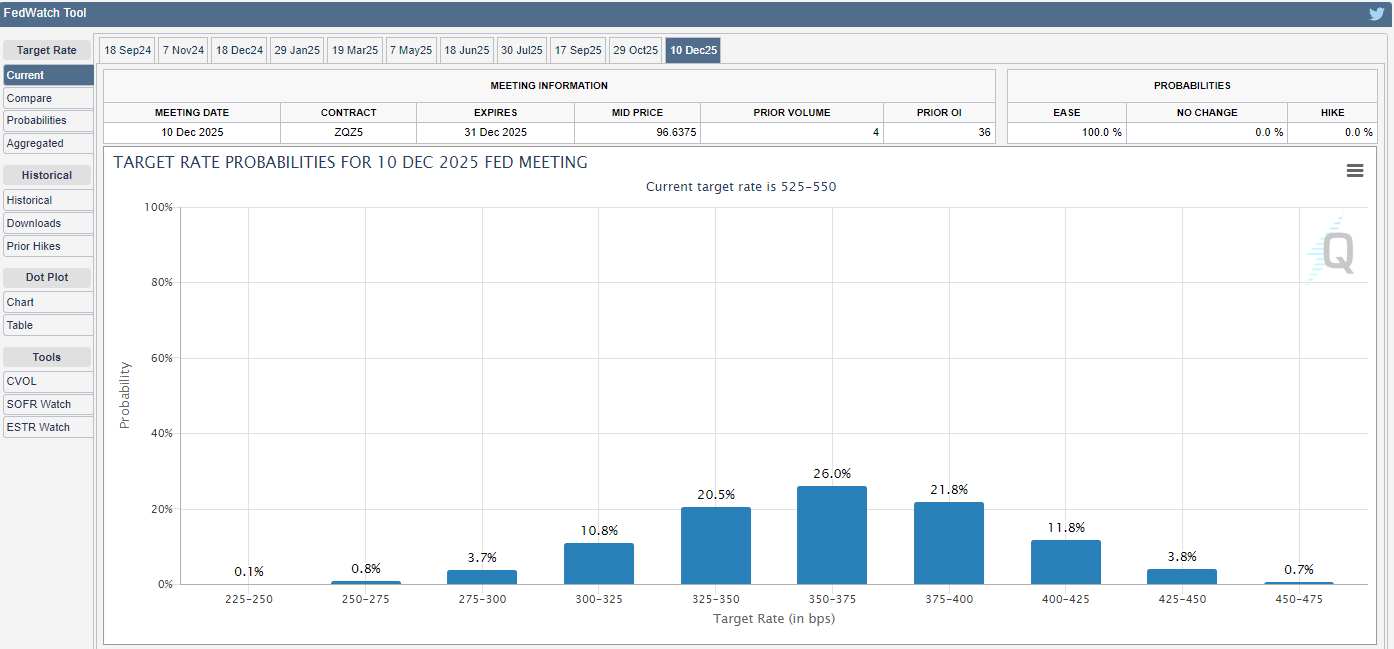

Likewise, the market presently expects that short-term rates of interest will most probably be 3.50% to three.75% by the top of 2025:

Chicago Mercantile Alternate

Whereas the affect that it will have on long-term rates of interest is unsure, it may nonetheless enhance the attractiveness of midstream firms and grasp restricted partnerships. This is because of the truth that these firms usually have very excessive yields. As rates of interest decline, the attractiveness of holding money decreases, and buyers grow to be extra prepared to tackle the dangers of holding high-yielding frequent equities. Thus, midstream firms grow to be comparatively extra engaging in a low-interest price setting. In such a state of affairs, we’d count on that the market worth of midstream firms would enhance and that might profit buyers within the Kayne Anderson Power Infrastructure Fund.

As midstream firms typically have very excessive yields, we’d count on the Kayne Anderson Power Infrastructure Fund to even have a really excessive yield. That is certainly the case, because the fund yields 8.11% on the present share worth. Right here is how that compares to a few of the fund’s friends:

|

Fund Title |

Morningstar Classification |

Present Yield |

|

Kayne Anderson Power Infrastructure Fund |

Fairness-MLP |

8.11% |

|

ClearBridge Power Midstream Alternative Fund (EMO) |

Fairness-MLP |

6.63% |

|

Neuberger Berman Power Infrastructure and Earnings Fund (NML) |

Fairness-MLP |

8.65% |

|

NXG Cushing Midstream Power Fund (SRV) |

Fairness-MLP |

12.63% |

|

Tortoise Pipeline & Power Fund (TTP) |

Fairness-MLP |

5.64% |

As we will clearly see, the Kayne Anderson Power Infrastructure Fund is nowhere close to the highest-yielding fund on this specific sector. Actually, its yield represents the median of this peer group, as there are two higher-yielding funds and two lower-yielding funds. This may occasionally cut back the fund’s enchantment to these buyers who’re searching for to maximise the earnings that they earn from the belongings of their portfolios, however this shouldn’t be the case. In any case, the truth that the Kayne Anderson Power Infrastructure Fund solely manages to boast the median yield is an indication from the market that it expects the distribution to be sustainable on the present degree. That’s one thing that the majority income-seeking buyers can recognize. In any case, one in all our largest targets is to generate a secure earnings from our investments that we will use to pay our payments or cowl different bills.

As common readers could keep in mind, we beforehand mentioned the Kayne Anderson Power Infrastructure Fund in mid-April of 2024. The fairness market since that point has typically been pretty sturdy due each to buyers’ exuberance surrounding generative synthetic intelligence in addition to the expectation of rate of interest cuts within the close to future. In earlier bull cycles, such because the one which lasted from 2010 to 2021, we continuously noticed midstream companies and grasp restricted partnerships neglected of the rally. This was not the case this time, nevertheless, which could be as a result of elevated enchantment of their excessive yields throughout a interval of falling rates of interest. As such, we’d count on the Kayne Anderson Power Infrastructure Fund to have additionally delivered a fairly engaging efficiency.

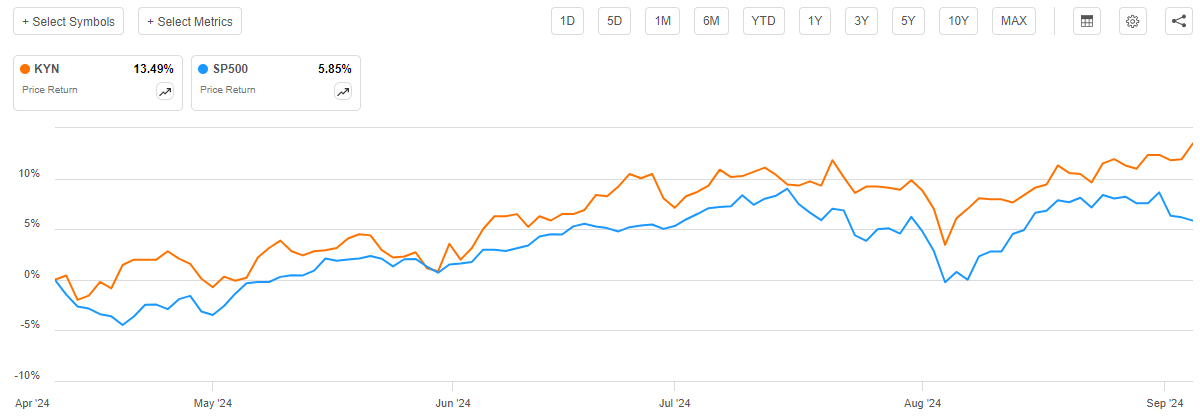

This assumption proves to be right, as shares of the Kayne Anderson Power Infrastructure Fund have risen by a powerful 13.49% since our earlier dialogue:

Searching for Alpha

As we will clearly see, this fund managed to outperform the S&P 500 Index (SP500) by a substantial margin over the roughly five-month interval. That is more likely to be a giant shock to these buyers who’ve been following the midstream sector for some time, because it has usually been fairly uncommon for midstream firms (or certainly something within the conventional power sector) to outperform the S&P 500 Index. Nonetheless, that was the case over the previous few months.

Actually, although, buyers on this fund have outperformed the S&P 500 Index by much more than the above chart suggests. As I said in my earlier article on this fund:

Closed-end funds such because the Kayne Anderson Power Infrastructure Fund usually pay out most or all of their funding income to the shareholders within the type of distributions. The fundamental objective is for the fund’s belongings to stay comparatively secure whereas the shareholders obtain the entire income earned by the portfolio. These distributions embrace each the dividends and different funds made by the belongings within the fund and any capital beneficial properties that the fund manages to appreciate. That is the explanation why closed-end funds often have a lot larger yields than absolutely anything else out there. It additionally implies that shareholders in a fund will usually do significantly better than the share worth efficiency suggests because the distribution itself is an funding return.

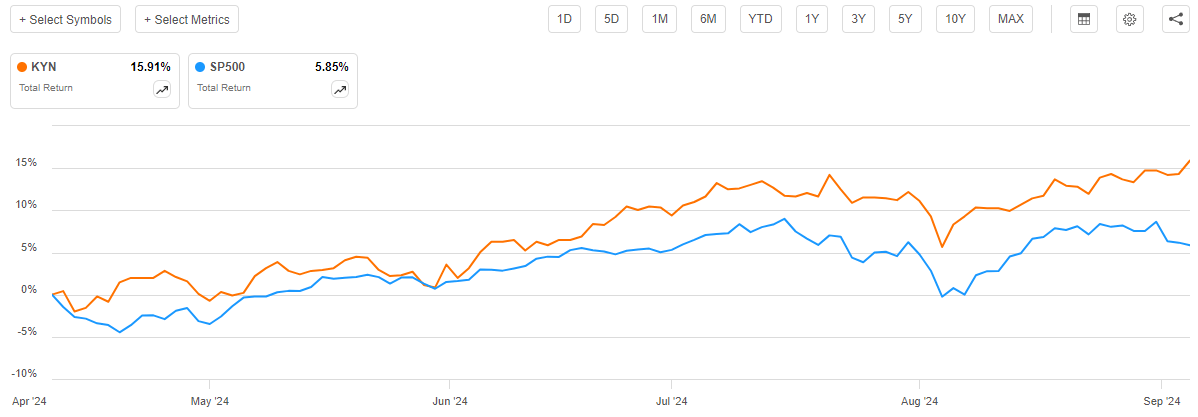

We should always, subsequently, embrace the distributions paid by the fund in our efficiency evaluation. Once we do this, we get this various to the chart above:

Searching for Alpha

The Kayne Anderson Power Infrastructure Fund solely pays a quarterly distribution, so it doesn’t obtain as massive a lift to the full return over 5 months as a month-to-month paying closed-end fund. This is because of the truth that the fund made fewer funds over the interval. Nevertheless, we will nonetheless see that buyers on this fund beat the S&P 500 Index by greater than 10% over a five-month interval. That’s definitely a powerful efficiency, and it appears more likely to enchantment to any investor, no matter their total targets. In any case, all of us prefer to beat the market, and this fund has definitely managed to perform that not too long ago.

As roughly 5 months have handed since we final mentioned the Kayne Anderson Power Infrastructure Fund, it’s probably that many issues have modified. The rest of this text will focus particularly on these modifications, in addition to present an replace on the fund’s distribution protection and total monetary efficiency.

About The Fund

In line with the fund’s web site, the Kayne Anderson Power Infrastructure Fund has the first goal of offering its buyers with a really excessive degree of complete return. This is sensible for an fairness fund as a result of frequent equities are a complete return car. In any case, buyers buy frequent equities as a result of they’re hoping to obtain each present earnings (through dividends and distributions paid by frequent equities) and capital beneficial properties. That’s the very definition of complete return.

The web site makes it clear that the fund is an fairness fund, because it states:

[The Fund’s investment objective is] to offer a excessive after-tax complete return with an emphasis on making money distributions to stockholders. KYN intends to attain this goal by investing at the very least 80% of its complete belongings in securities of power infrastructure firms.

The web site doesn’t precisely outline what the fund considers to be an “power infrastructure firm,”, nevertheless it makes the next statements about this:

Kayne Anderson

The primary bullet level gives a small quantity of perception, because it says that the fund’s investments would possibly embrace midstream firms, liquefied pure fuel producers, utilities, and renewable power producers. It additionally says that the businesses that it invests in will usually have comparatively secure money flows and excessive boundaries to entry. Nevertheless, this final bullet level doesn’t utterly apply to renewable power producers.

As subscribers to Power Income in Dividends are effectively conscious, renewable power firms have been struggling over the previous few years because of a scarcity of profitability. On Tuesday, September 3, 2024, solar energy producer Lumio filed for Chapter 11 chapter safety because of extreme liquidity issues. An article posted to Zero Hedge included some quotes from one in all Lumio’s board members which might be fairly descriptive of the state of affairs:

In a court docket declaration, Jeffrey T. Varsalone, a Lumio board member, stated the corporate has confronted a “extreme liquidity disaster” over the previous yr, which he attributed to “a pointy decline in demand within the photo voltaic market and varied macroeconomic headwinds.

Varsalone blamed will increase in inflation and a subsequent leap in rates of interest to have resulted in “decreased demand throughout all the solar energy trade,” thus negatively impacting Lumio’s monetary efficiency.”

Greater than 100 solar energy firms have filed for chapter safety year-to-date, with most of them making related claims as Lumio. That is definitely not one thing that we’d count on to see in an trade with secure money flows, because the fund’s web site claims. Renewable power firms have been struggling to outlive in a high-interest price setting, even supposing they obtain monumental subsidies from most developed-market governments.

In the meantime, conventional midstream firms haven’t been significantly impacted by rates of interest. For instance, allow us to check out the curiosity bills paid by MPLX (MPLX), which is presently the most important holding within the Kayne Anderson Power Infrastructure Fund. Listed below are the corporate’s quarterly complete and web curiosity bills going again the entire technique to the fourth quarter of 2021:

Searching for Alpha

(all figures in tens of millions of U.S. {dollars})

Within the fourth quarter of 2021, the federal funds price was at 0%, though long-term rates of interest have been starting to rise because the inflation current out there throughout that yr led the market to count on that the Federal Reserve would quickly enhance its benchmark price. For our functions as we speak, we will see that MPLX paid $199.0 million in web curiosity again within the fourth quarter of 2021. That determine elevated to $220.0 million within the second quarter of 2024, which represents a ten.55% enhance over the interval in query.

This 10.55% enhance in web curiosity didn’t pressure MPLX’s money move or liquidity in any respect. We will see this fairly clearly right here:

|

Q2 2024 |

This fall 2021 |

|

|

Adjusted EBITDA |

$1.653 |

$1.445 |

|

Distributable Money Circulation |

$1.404 |

$1.207 |

(all figures in billions of U.S. {dollars})

Distributable money move is after the corporate pays each taxes and curiosity on its debt. As we will clearly see, the corporate managed to submit a rise on this determine over the interval in query even supposing its curiosity bills went up. We see the identical factor with nearly any conventional midstream firm.

Thus, we have now a state of affairs through which most conventional midstream firms match with the fund’s assertion that the businesses that it consists of in its portfolio have secure money flows over time. Nevertheless, most renewable firms don’t fulfill this requirement.

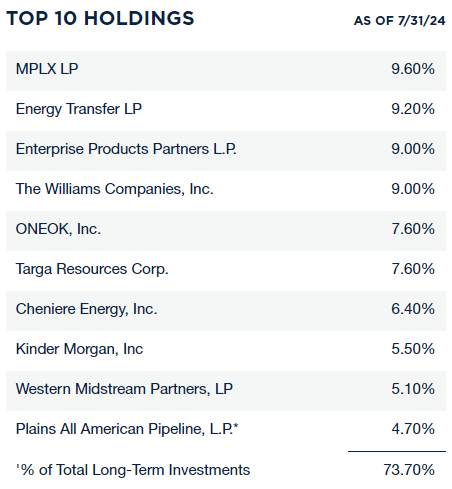

The fund appears to be way more dedicated to its promise to put money into firms with secure money flows than its assertion about together with renewable power within the portfolio. 9 of the ten largest holdings within the fund’s portfolio as of July 31, 2024, have been midstream firms:

Kayne Anderson

The one one in all these firms that isn’t a midstream firm is Cheniere Power (LNG), however that firm is continuously included in power infrastructure funds. Cheniere Power primarily sells its merchandise and generates income primarily based on the phrases of long-term contracts that require its prospects to purchase a certain amount of liquefied pure fuel at a set worth. Nevertheless, this has not precisely resulted within the firm having fun with secure money flows. For instance, listed here are Cheniere Power’s working money flows for every of the previous eleven twelve-month durations:

Searching for Alpha

(all figures in tens of millions of U.S. {dollars})

We will see that Cheniere Power’s working money bounds have been range-bound over the interval, but it surely was a reasonably large vary. The corporate’s working money flows diverse from $2.469 billion to $11.289 billion throughout any given twelve-month interval, which isn’t what most individuals would take into account to be secure.

It’s true that Cheniere Power’s prices will fluctuate over time because of its enterprise mannequin. The corporate operates considerably like a refinery, because it purchases pure fuel and converts it to liquefied pure fuel on the market. As such, we will count on each its income and the price of items bought to fluctuate with pure fuel costs. Nevertheless, the corporate’s gross revenue (outlined as income minus the price of the pure fuel that it buys) has diverse significantly from interval to interval:

Searching for Alpha

(all figures in tens of millions of U.S. {dollars})

Whereas earlier years proven on this chart will be ignored considerably as a result of firm’s manufacturing rising in 2022 when a sixth liquefaction prepare got here on-line at its Sabine Go facility, rendering a few of the earlier durations not utterly akin to later ones, we will nonetheless see that the corporate’s gross revenue tended to exhibit appreciable variation. Thus, Cheniere Power arguably may not utterly match the definition of possessing secure money flows both, however this is only one firm that represents 6.40% of the portfolio. It alone will not be weighted excessive sufficient to alter the truth that the fund appears to favor investing in firms with very secure money move era.

There have been no main modifications to the fund’s largest positions record. All ten of the businesses proven on the record are the identical as have been there once we final mentioned this fund 5 months in the past. The weightings which might be assigned to every of the businesses have modified, nevertheless. That’s to be anticipated although just because every of those shares had a considerably totally different efficiency out there.

Nevertheless, the fund’s semi-annual report states that the Kayne Anderson Power Infrastructure Fund had a 39.4% turnover through the six-month interval that ended on Could 31, 2024. This works out to 78.8% annualized, which means that this fund does a major quantity of buying and selling. We will see additional proof of the fund’s vital buying and selling exercise by trying on the turnover ratios that it had in prior years:

|

FY 2023 |

FY 2022 |

FY 2021 |

FY 2020 |

FY 2019 |

|

|

Portfolio Turnover |

48.8% |

28.2% |

50.8% |

22.3% |

22.0% |

This forces us to attract the conclusion that at the very least a few of the weighting modifications that we observe within the fund’s largest positions record have been intentional on the a part of the fund’s administration workforce. Briefly, the fund bought a few of the shares or models that it held in a single firm and used the proceeds to buy frequent fairness in one other firm. That is precisely what all of us do once we rebalance our private portfolios.

Leverage

As is the case with most closed-end funds, the Kayne Anderson Power Infrastructure Fund employs leverage as a way of boosting the efficient yield and complete return that it earns from the belongings in its portfolio. I defined how this works in my earlier article on this fund:

Mainly, the fund borrows cash after which makes use of that borrowed cash to buy partnership models of midstream firms. So long as the bought belongings have the next yield than the rate of interest that the fund has to pay on the borrowed cash, the technique works fairly effectively to spice up the efficient yield of the portfolio. As this fund is able to borrowing at institutional charges, that are significantly decrease than retail charges, it will often be the case.

Nevertheless, the usage of debt on this trend is a double-edged sword. It is because leverage boosts each beneficial properties and losses. Because of this, we need to be certain that the fund will not be using an excessive amount of leverage since that might expose us to an excessive amount of threat. I typically don’t prefer to see a fund’s leverage exceed a 3rd as a share of its belongings for that reason.

As of the time of writing, the Kayne Anderson Power Infrastructure Fund has leveraged belongings comprising 22.83% of its total portfolio. This represents a reasonably vital decline from the 23.81% leverage that we had the final time that we mentioned this fund, which isn’t precisely shocking. In any case, the fund’s share worth elevated pretty dramatically since our final dialogue, and often that correlates to a decline in a fund’s leverage.

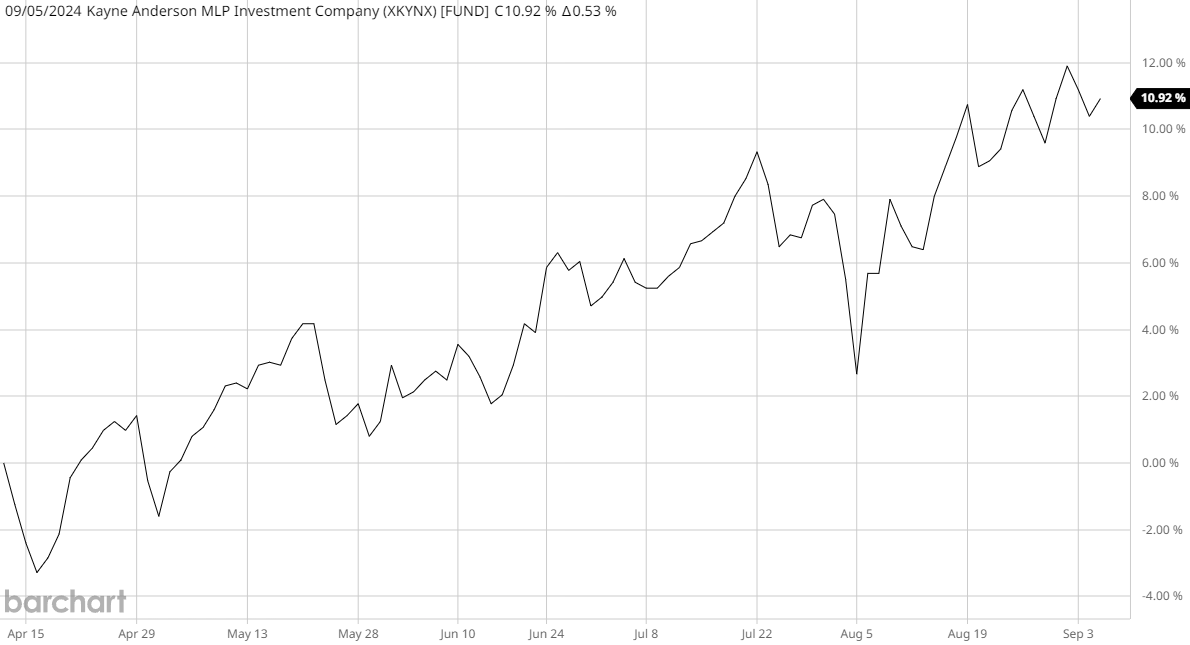

Nevertheless, it’s the web asset worth actions that decide the impact on leverage, not the share worth. In any case, leverage is a share of the portfolio itself and the dimensions of the portfolio may not be the identical because the fund’s market capitalization. Within the case of the Kayne Anderson Power Infrastructure Fund, we will see that its portfolio elevated in measurement over the interval:

Barchart

As we will clearly see, the fund’s web asset worth has elevated by 10.92% because the time of our final dialogue. All else being equal, this causes the fund’s leverage to say no, since leverage is a proportion of the excellent debt to the full measurement of the portfolio. This seems to be the case right here, however admittedly, we’d count on leverage to have declined a bit greater than it did, given the substantial enhance within the fund’s web asset worth.

As was the case the final time that we mentioned this fund, the leverage of the Kayne Anderson Power Infrastructure Fund is considerably under the one-third most that we usually take into account to be acceptable. Nevertheless, that one-third degree is only a generalized determine and is probably not a suitable ratio given the fund’s technique. We should always evaluate its leverage to its friends to find out whether or not or not the fund is utilizing an acceptable quantity of leverage. That is summarized on this chart:

|

Fund Title |

Leverage Ratio |

|

Kayne Anderson Power Infrastructure Fund |

22.83% |

|

ClearBridge Power Midstream Alternative Fund |

29.34% |

|

Neuberger Berman Power Infrastructure and Earnings Fund |

17.07% |

|

NXG Cushing Midstream Power Fund |

29.23% |

|

Tortoise Pipeline and Power Fund |

15.50% |

(all figures from CEF Knowledge)

As was the case with the fund’s distribution yield, the Kayne Anderson Power Infrastructure Fund represents the median degree of leverage out of this peer group. That is an total constructive signal, because it means that the fund is utilizing an acceptable quantity of leverage for its funding technique. General, we should always not want to fret a lot about its debt degree.

Distribution Evaluation

The first goal of the Kayne Anderson Power Infrastructure Fund is to offer its buyers with a really excessive degree of complete return. Nevertheless, the web site states that the fund intends to offer its complete return primarily by way of direct funds to its buyers, and it does observe by way of on this intent. The Kayne Anderson Power Infrastructure Fund presently pays a quarterly distribution of $0.22 per share ($0.88 per share yearly). This offers the fund an 8.11% yield on the present share worth, which is affordable.

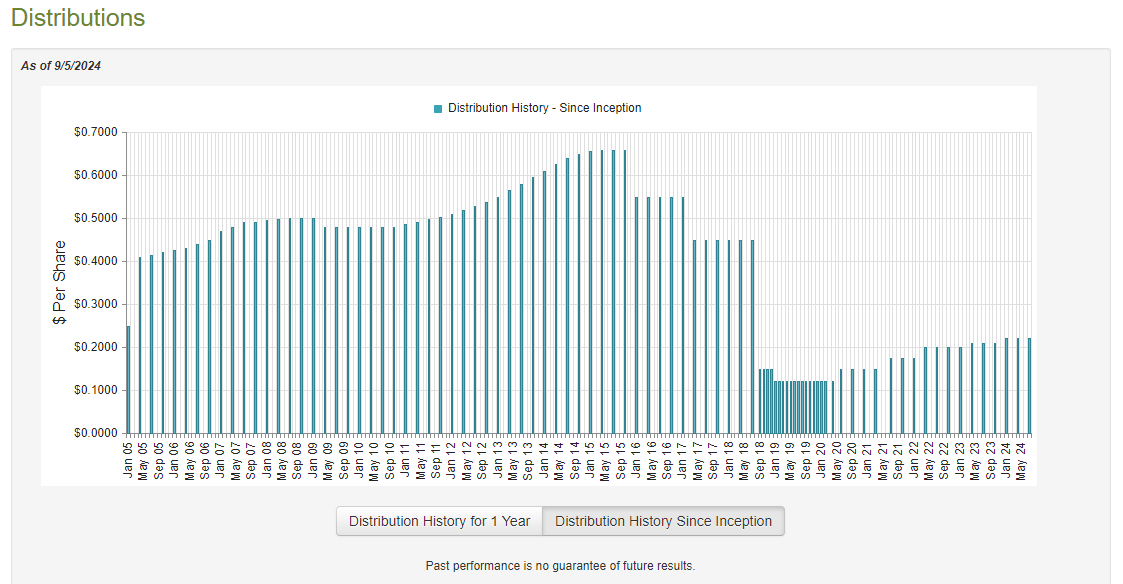

Sadly, the fund has not been particularly dependable with respect to its distributions over time:

CEF Join

From the earlier article:

As we will see, the fund’s distribution has diverse significantly over time, though the long-term pattern has been down. The fund has at the very least been making an attempt to lift its distribution since 2020. This isn’t particularly shocking, as most midstream funds ended up having to chop their distributions in both 2015 or 2020 because the midstream power trade generally encountered disaster circumstances following a fallout in crude oil costs. The market was typically unwilling to finance these firms and so a lot of them have been compelled to chop their distributions and restructure their operations with a purpose to survive. That prompted the fund to endure pretty substantial losses, and it was compelled to cut back its personal payout with a purpose to protect its web asset worth.

The truth that the fund has been elevating its distribution since 2020 is probably going going to enchantment to these buyers who’re searching for a secure and safe source of earnings, though some conservative buyers may not be capable to excuse the fund’s previous. General, although, the midstream power trade is stronger as we speak than it has been in current reminiscence, and this could present a sure degree of confidence. We should always nonetheless examine the fund’s funds and distribution sustainability, nevertheless.

The latest monetary report that’s accessible for the Kayne Anderson Power Infrastructure Fund is the semi-annual report for the six-month interval that ended on Could 31, 2024. A hyperlink to this report was supplied earlier on this article. It is a a lot newer report than the one which was accessible the final time that we mentioned this fund, which is sort of good because it ought to work as an replace.

For the six-month interval that ended on Could 31, 2024, the Kayne Anderson Power Infrastructure Fund obtained dividends and distributions of $40.028 million and surprisingly nothing in curiosity. Nevertheless, a few of this cash got here from grasp restricted partnerships and so it’s not thought of to be funding earnings for tax or accounting functions (it’s a return of capital). We subtract the partnership distributions from the full to reach at a complete funding earnings of $22.846 million for the six-month interval. The fund paid its bills out of this quantity, which left it with $5.676 million accessible to its shareholders. That was not ample to cowl the $74.415 million that the fund paid out in distributions through the interval.

The Kayne Anderson Power Infrastructure Fund was in a position to make up the distinction by way of capital beneficial properties. For the six-month interval that ended on Could 31, 2024, the fund reported web realized beneficial properties of $80.886 million together with $170.550 million of web unrealized capital beneficial properties. General, the fund’s web belongings elevated by $186.224 million after accounting for all beneficial properties and losses through the interval. Thus, the fund simply managed to cowl its distributions with a considerable sum of money left over.

Thus, it doesn’t seem that shareholders want to fret an excessive amount of about potential distribution troubles right here. The fund was in a position to totally cowl its distributions solely with web funding earnings and web realized beneficial properties, so even when the market corrects and causes the fund to lose a few of its unrealized beneficial properties, it ought to nonetheless be okay.

Valuation

Shares of the Kayne Anderson Power Infrastructure Fund are presently buying and selling at a 13.93% low cost on web asset worth. This isn’t as engaging because the 14.76% low cost that the fund’s shares have had on common over the previous month. Nevertheless, it’s nonetheless a double-digit low cost so the fund’s present worth seems to be cheap.

Conclusion

In conclusion, the Kayne Anderson Power Infrastructure Fund is a fairly engaging method so as to add some publicity to power infrastructure firms to your portfolio. Many of those firms have very excessive distribution yields that may solely grow to be extra engaging because the Federal Reserve embarks on its upcoming financial easing cycle. This could be one purpose why grasp restricted partnerships and midstream companies have outperformed the broader large-cap index year-to-date, regardless of power costs remaining comparatively secure. This outperformance is mirrored within the efficiency of this fund, which has additionally crushed the broader large-cap index. The fund additionally boasts a really engaging distribution yield that’s fairly well-covered. Certainly, if the second half of the fund’s fiscal yr finally ends up being nearly as good as the primary half, it’s conceivable that we’d see a distribution enhance within the close to future. That will or is probably not the case, although, and buyers mustn’t count on a distribution enhance when shopping for the fund as we speak.

The truth that this fund additionally has a really engaging valuation is one other bonus. General, there’s a lot to love right here.

Editor’s Notice: This text discusses a number of securities that don’t commerce on a significant U.S. change. Please pay attention to the dangers related to these shares.

[ad_2]

2024-09-07 07:11:08

Source :https://seekingalpha.com/article/4719676-kyn-impending-rate-cuts-improve-relative-attractiveness-energy-infrastructure?source=feed_all_articles

{kind=link}

Discussion about this post