[ad_1]

kool99/iStock by way of Getty Photos

Expensive readers/followers,

Kaiser Aluminum (NASDAQ:KALU) is a enterprise I have been protecting for a couple of years now. My newest protection for this firm has been over 16 months in the past now, in an article that you could find right here. That article has not delivered alpha, however that is additionally not what I anticipated or forecasted. Certainly, I used to be at a “Maintain” suggestion, and on this manner, the corporate has not solely underperformed however underperformed considerably. It is up 11% since early 2023, however the S&P500 is up round 37% within the meantime, that means lower than 0.33x of the S&P500.

On this article, I imply to replace you on this firm’s thesis and upside going into this yr, and the subsequent few years. I am an investor into aluminum and metals total, in addition to mining, and this firm is doubtlessly enticing – however provided that we will get it at a value that is sensible for us.

I don’t imagine that’s what we have now right here – and I’ll spend this text attempting to justify this opinion to you.

Lots of traders I converse to contemplate beating the market to be “simple”, based mostly on what they hear and see. I don’t imagine this to be the case. Beating the market requires, as I see it, cautious consideration, and cautious choosing at conservative valuations. So that is what I give attention to.

I might somewhat have my cash producing 3.7% in a risk-free account than put it into an funding that doesn’t have appreciable upside potential.

Does KALU have this right here?

Let’s examine.

Kaiser Aluminum – The corporate’s outcomes, upside, and what will be seen in 2Q24.

On the subject of steel corporations, a few of my favorites embody Norsk Hydro (OTCQX:NHYDY) and different Swedish and Scandinavian gamers. I additionally personal a good bit of thyssenkrupp (OTCPK:TKAMY).

I’ve made a revenue in each of those investments – however I have never made a revenue in KALU as a result of I’ve not owned it but. This isn’t because of fundamentals. 75 enticing years of enterprise experience makes a convincing thesis for the corporate at a superb value, simply not at any value. Given the operational challenges of aluminum, specializing in the vertically built-in gamers on this area is usually an excellent concept. The corporate combines an natural and inorganic development technique, and the way the corporate operates is itself an argument to speculate. It is very uncommon to seek out vertically built-in aluminum corporations right here – and looking out on the higher percentiles by way of margins and outcomes, not many can measure as much as KALU, even when they don’t seem to be the “highest” as such.

The place KALU shines is in returns – issues like RoE, RoA, ROIC and ROCE – all of this stuff are wanting superb, and it is higher than no less than half of the market relating to these KPIs on this section. The most recent set of firm outcomes affirm the corporate’s long-term upside, however does create challenges within the extra short-term oriented outlook.

We have seen a considerably problematic scenario within the steel markets for over a yr at this level. The corporate noticed usually good developments in gross sales, high and backside line, for more often than not throughout 2Q24. The corporate’s EBITDA got here in at $53.5M, with an EBITDA margin near 14.5%. The present technique is a discount in stock ranges – however this in itself precipitated a little bit of an accounting impact, with a close to 10% cost in LIFO.

The corporate’s outcomes, as they stand, are pushed by strong pricing, decrease prices (and persevering with to drop barely), and good enterprise methods. All of those outcomes have been, in actual fact, regardless of unplanned outages in packaging, which resulted in decrease shipments as nicely.

So from that lens, the corporate really did somewhat nicely. The corporate is executing on said initiatives for development and upside…

Kaiser Aluminum IR (Kaiser Aluminum IR)

…nevertheless it’s equally clear right here that the market shouldn’t be that impressed by the corporate’s efficiency. All it’s worthwhile to do is have a look at what the market did to the corporate’s share value, which was a major drop right here.

So what is going on on?

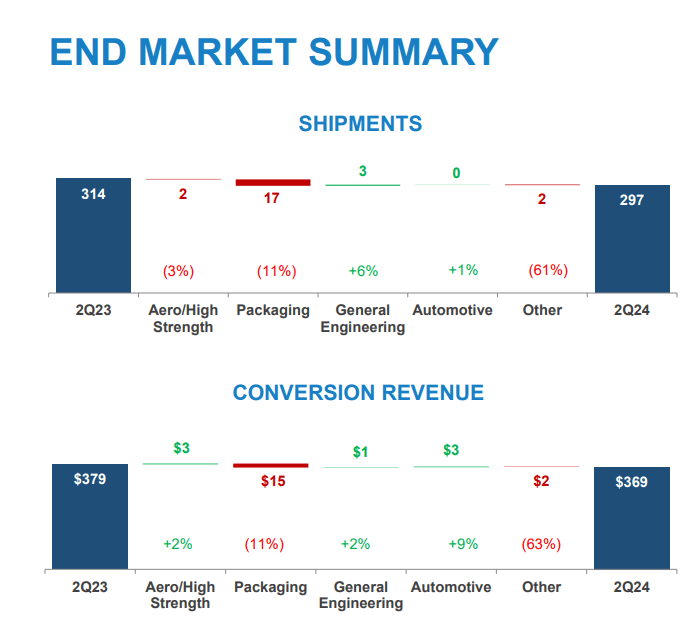

Effectively, a part of it’s most likely a decline in shipments and decrease total conversion.

KALU IR (KALU IR)

What is going on on right here is the upside from Aerospace/Excessive Energy because of higher buyer diversification, and restoration in engineering. Issues will most likely proceed to be down considerably so long as automotive does not present a strong restoration right here – and anybody’s guess appears pretty much as good concept as any right here as to when that is going to occur.

The margins and different outcomes are okay. The corporate is sort of unstable – we’re speaking 14.5%, which is each beneath the very best, however above the bottom kind of consequence. This quarter has seen some points in packaging, so with out that, we needs to be above 15%, which might be a reasonably strong quarter. The corporate did nicely on the sourcing aspect and reduce each administration and overhead, in addition to manufacturing prices. CapEx for the yr is ready to be round $190M on the excessive aspect, and the corporate has over $610M in liquidity as issues stand on June thirtieth.

LTM, the corporate, has managed to generate shipments already in extra of 2023 for among the firm’s key segments. Diversification has been an absolute key in how nicely the corporate has been doing right here, and “combating” in opposition to the influence of OEM construct charges.

For the rest of the complete yr, KALU expects the corporate’s conversion to stay flat (possible a motive why the corporate went down after this report), a slight enchancment in EBITDA margin, specializing in stabilization of operations, versus development, and transferring into a greater place for that development going into 2025E and past.

The corporate does stay a really main participant in crucial fields – together with packaging, Automotive, and common engineering, which I see because the extra attention-grabbing. The sustainability angle from the aluminum packaging area goes to beat the “plastic” strikes from this a part of the business, and this interprets to round 5-7% annualized development price on the highest line by way of the market.

KALU IR (KALU IR)

In the meantime, Automotive, which is all the time a really fickle kind of mistress, is probably going going to be a low-growth space for a while. The NA industrial demand ought to prop issues up a bit, however will probably be in keeping with the re-shoring of home provide, and we’ll see how this goes. The identical factor is true for the Aerospace area, the place it is possible we’ll see development or strikes correlated to how air journey evolves. For now, this appears optimistic, however there are dangers right here. This makes the thesis for the corporate difficult.

Here’s what I see by way of valuation.

Kaiser – sadly not a “Kaiser”/Emperor by way of valuation

The primary disadvantages of this firm embody a less-than-flawless kind of credit standing, with solely a BB- and a leverage of 61.7% in long-term debt to capital. As such, the corporate is considerably extremely leveraged. Other than this, it is also very unstable in a manner that friends like NHYDY usually are not. Between 2019 and 2022, the corporate’s EPS on an adjusted foundation fell 56%, 20%, and 106%, going detrimental in 2022. These outcomes have, in fact, recovered – for 2023, we’re again to $2.74 in EPS, nevertheless it’s necessary to notice that this EPS does not even come near matching 2019, which was at virtually $7/share when the corporate traded materially at an analogous value to the place it does right now.

It is this coupled with the corporate’s volatility which makes me uncertain about investing right here. There’s a forecasted resurgence within the firm’s earnings – we’re speaking 2025E, the place earnings are at the moment forecasted to enhance by round 80% (Source: Paywalled F.A.S.T Graphs Hyperlink).

However how possible is such a growth? 65% of the time, the corporate’s forecasts and analyst forecasts are negatively missed. So such a forecast could be harmful to place an excessive amount of inventory in if the corporate have been to underperform. What KALU has going for it’s, in actual fact, the corporate’s yield, which is definitely over 4% at the moment and which makes this one of many better-yielding steel corporations on the market.

However this comes with a value – and that value is that the corporate doesn’t cowl its dividend with earnings. Not for 2023, not for 2024 even, which nonetheless falls quick 4 cents of protection. If the corporate does enhance earnings subsequent yr, this isn’t a lot of a factor – however once more, we do want to contemplate if the probability if that is excessive or not.

Analysts following the corporate are break up virtually down the center. The corporate has a excessive of over $100 and a low of beneath $70/share. The present share value is $73/share, which is above my final article, however not as a lot as I’d count on, with a mean over the $80/share mark. This has the results of having an upside, based mostly on forecasts of round 10%. Nevertheless, this fails to think about that the corporate doesn’t have its debt beneath management. As I mentioned in my earlier piece, the hurdle for me to put money into KALU is readability. I need the corporate to extra clearly present me a conservative upside, and I don’t imagine the corporate is at the moment able to this.

In my final article, I set a $70/share PT. I may improve it right here, however the truth is that present developments in earnings and the way the corporate’s outcomes look in 2Q24, don’t give me quite a lot of hope that the corporate is about to outperform for the 2024E interval.

This makes the corporate a threat/reward play that’s not enticing, i.e., the chance is simply too excessive for the reward that’s being supplied, and I imagine there are considerably extra enticing alternatives out there right here.

And for that motive, I can solely think about KALU to be a “Maintain” right here. I look ahead to extra readability in 3Q24, to see if there is a justification for a greater upside right here.

Thesis

- Kaiser Aluminum is a not-uninteresting aluminum firm energetic in 4 interesting finish markets. It has a strong yield, not a strong credit score, and tough, unstable forecasts. To be able to just remember to have a superb upside right here, it’s worthwhile to purchase the corporate in the direction of the cheaper finish of its common spectrum.

- I nonetheless view this as being round $70/share – and that is unchanged from my earlier article again in April 2023.

- For that motive, I would not go increased than “HOLD” at the moment – but when the corporate have been to drop sufficient, I can be investing right here. However this could require a drop beneath $70/share, and the place I may see an upside to a conservative 15% annualized.

Keep in mind, I am all about:

- Shopping for undervalued – even when that undervaluation is slight and never mind-numbingly large – corporations at a reduction, permitting them to normalize over time and harvesting capital features and dividends within the meantime.

- If the corporate goes nicely past normalization and goes into overvaluation, I harvest features and rotate my place into different undervalued shares, repeating #1.

- If the corporate does not go into overvaluation however hovers inside a good worth, or goes again right down to undervaluation, I purchase extra as time permits.

- I reinvest proceeds from dividends, financial savings from work, or different money inflows as laid out in #1.

Listed here are my standards and the way the corporate fulfills them (italicized).

- This firm is total qualitative.

- This firm is basically protected/conservative & well-run.

- This firm pays a well-covered dividend.

- This firm is at the moment low cost.

- This firm has a sensible upside that’s excessive sufficient, based mostly on earnings development or a number of enlargement/reversion.

The corporate, because of BB-, and the present market scenario, which is considerably modified, doesn’t fulfill my high quality standards, neither is it low cost. For that motive, I am solely prepared to provide it a “HOLD” at the moment.

[ad_2]

2024-08-30 07:48:34

Source :https://seekingalpha.com/article/4718083-span-stylebackground-color-rgb204-255-153kaiser-aluminum-an-upside-going-into-2024-2025span?source=feed_all_articles

{kind=link}

Discussion about this post