[ad_1]

xijian

JinkoSolar (NYSE:JKS) could look unattractive in the mean time primarily based on its steadiness sheet and an absence of enthusiasm for the inventory available in the market, however I believe there may be probably a deep worth alternative right here that would make for a extremely profitable funding over the long run.

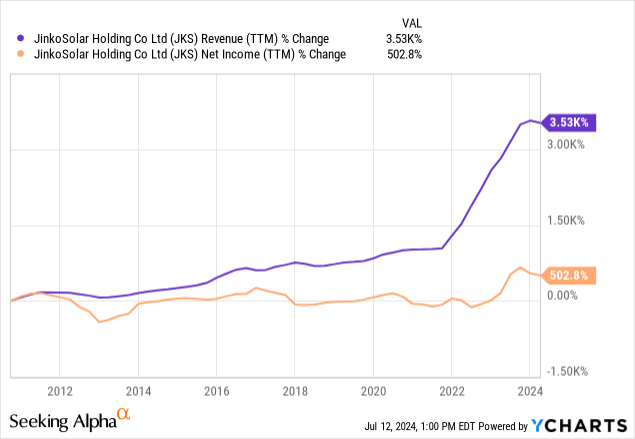

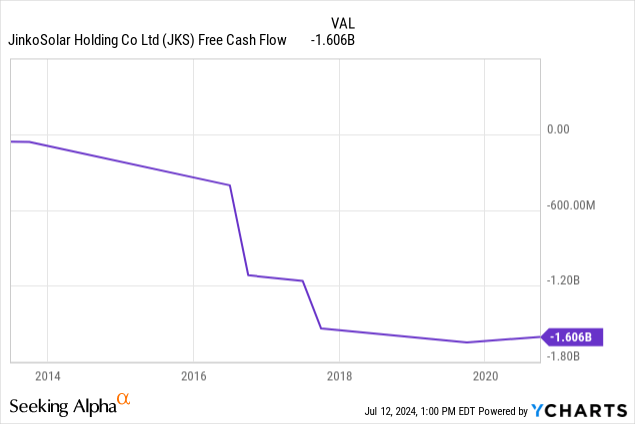

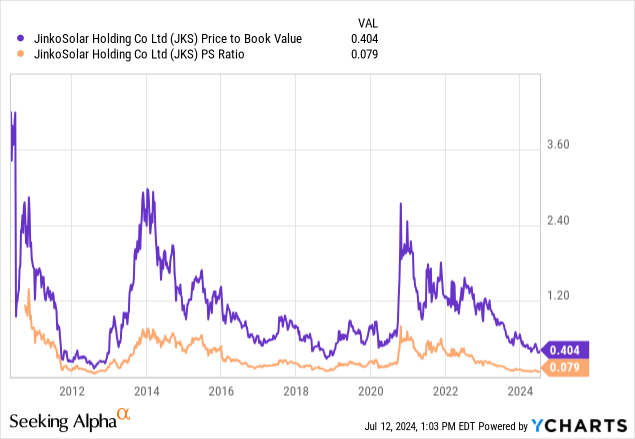

Lots of its valuation multiples are considerably contracted in comparison with historic ranges, and its price-to-book ratio is at present underneath 0.5. Moreover, administration has expressed that it’s actively working to enhance its debt scenario, and this has been made evident within the progress reported within the final quarter. That being stated, the excessive degree of debt may imply that this firm grows slower than one would really like, which means the inventory may go down additional earlier than it goes up—this concern is additional validated by the poor momentum within the inventory worth during the last two years. Administration has been clear that its new N-type panels, that are extremely environment friendly and market-leading, ought to drive progress. Nonetheless, I consider the corporate wants to remodel its expense technique to alleviate considerations with the unfavorable free money move at present reported (which, whereas widespread in photo voltaic corporations, continues to be a weak point, particularly contemplating the excessive ranges of debt the agency has) and should prioritize paying down debt and stabilizing its capital construction. If the agency manages this, the present valuation is extremely engaging and will result in excessive long-term alpha, not simply shorter-term deep-value worth positive factors, in my view.

Operational Evaluation

JinkoSolar is a number one international photo voltaic module producer headquartered in China. It manufactures a variety of solar energy merchandise, with core choices together with silicon ingots, silicon wafers, photo voltaic photovoltaic cells, and monocrystalline and multicrystalline panels. Notably, JinkoSolar was one of many first corporations to supply N-type mono merchandise, that are recognized for his or her superior effectivity and efficiency.

Administration is at present planning to reinforce its operational effectivity by decreasing prices. It desires to leverage the N-type know-how and built-in capability construction, which it has been investing closely in, to enhance profitability, significantly by decreasing manufacturing prices. That is very important as the corporate wants progress in money move to assist it pay down debt, which I’ll clarify in my monetary evaluation beneath. Administration has said that it expects the mass-produced N-type cell effectivity to achieve 26.5% by the tip of 2024, which is far larger than present, the place SunPower can handle an effectivity of 22.8%.

The corporate at present has a present annual manufacturing capability of 75 GW for mono wafers, 75 GW for photo voltaic cells, and 90 GW for photo voltaic modules. Nonetheless, it plans to increase this to 120 GW for mono wafers, 110 GW for photo voltaic cells, and 130 GW for photo voltaic modules by the tip of 2024. Its main enlargement initiatives have included a 56 GW vertically built-in facility in Shanxi, China, and a 4 GW N-type capability in Vietnam, which is deliberate. This explains why the corporate has continued to speculate aggressively and has excessive capex, which has continued to maintain its unfavorable free money move yield. JKS arguably has the lead in solar energy effectivity, however the concern I’ve is the expense this has taken on the corporate’s capital construction.

Monetary & Valuation Evaluation

JinkoSolar has an Altman Z-Rating of 1.15 which falls within the “misery zone” (beneath 1.8), which signifies monetary difficulties in the long run if the scenario would not enhance. Administration is conscious of the weak point right here, and it has decreased the agency’s complete debt from $4.38B in This fall 2023 to $3.66B in Q1 2024.

Charlie Cao, CFO of JinkoSolar Firm Restricted, additionally reported within the Q1 2024 earnings name that web debt improved from $1.63B in This fall 2023 to $1.22B in Q1 2024, indicating “a steady enchancment in our debt construction.” Pan Li, CFO of JinkoSolar Holding Co., Ltd., said they’re “persevering with to enhance the effectivity of our working capital, attaining sustainable progress in working money move and enhancing our resilience to dangers.”

Aside from its debt, the corporate has confirmed long-term top-line progress, however its profitability is extra regarding. Moreover, its free money move progress, as I discussed in my operational evaluation, definitely must be addressed. At present, the excessive ranges of capital expenditure are leaving the corporate with no room totally free money move in any respect.

Regardless of these challenges, the numerous worth alternative for JinkoSolar shareholders if shopping for at this time worth is that the corporate is promoting considerably beneath e-book worth, and likewise at solely a fraction of complete gross sales. If the corporate can tackle its capital construction and emphasize profitability extra, in addition to profit from long-term traits in photo voltaic market adoption the world over, I believe this might be a really profitable long-term funding certainly.

In my view, long-term success all is determined by how a lot progress the corporate can command in its backside line, which might be considerably hampered by the lack to finance progress methods as a consequence of debt considerations. Wall Road EPS consensus estimates for fiscal 2024 are -42.77% YoY progress and 74.56% for fiscal 2025. There are solely 2 or 3 Wall Road analysts overlaying JKS, however the consensus right now is that following 2024, optimistic EPS progress ought to resume at +25% ranges till the 2027 year-end, which is the restrict of forecasts at this stage.

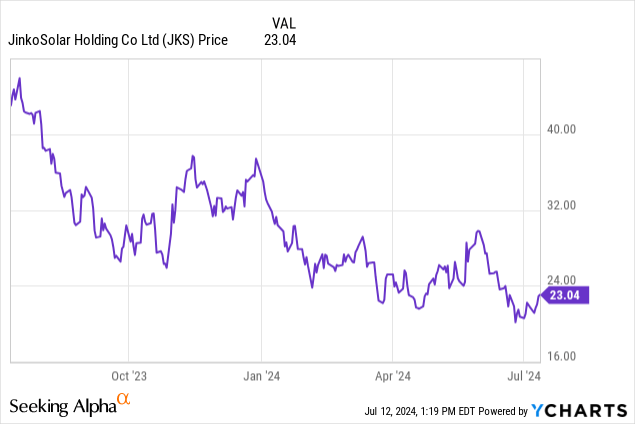

Because of this, I don’t suppose it’s unlikely that the inventory will start to understand in worth very quickly, particularly as 2025 nears and significantly as soon as the corporate begins to report YoY EPS progress in 2025 once more. The normalized PE ratio is at present 2.85, and because the 10Y median is round 9 (though I think about it overvalued for a big proportion of this time), I don’t suppose it’s unreasonable for the corporate’s non-GAAP PE ratio to increase to round 4 by the tip of 2025. Because of this, the inventory could be value $34.32 by 2025-end (primarily based on the consensus normalized EPS estimate of $8.58), indicating a complete worth return from now till then of round 50%, as the present inventory worth is $22.90.

Danger Evaluation

It is potential that the market doesn’t choose the chance up, though I see this unlikely, as when 2025 earnings progress begins to be reported, I believe it’s going to generate curiosity. That being stated, the inventory has a 1Y worth efficiency of -46.82% and a 3M efficiency of -4.46%.

I believe this threat needs to be taken critically, and I believe it may be value ready to speculate when some upward momentum has already been gained to keep away from the corporate falling additional. I believe the rationale the market has been so pessimistic in regards to the firm throughout this time of earnings contraction is that its steadiness sheet is so weak, and likewise its free money move continues to be a notable downside. I believe this considerably reduces the attractiveness of JinkoSolar available in the market, however I believe administration has expressed that it’s conscious of this and so is taking the required steps to deal with the issue sooner or later. Nonetheless, I believe progress expectations over the long run needs to be moderated as a result of its enlargement is probably going considerably inhibited by the present excessive ranges of debt.

Administration has clearly been doing this to maintain the corporate aggressive, and the vertical integration of its enterprise mannequin signifies that JinkoSolar has price management, high quality assurance, and provide chain stability. Nonetheless, it takes excessive capital necessities, which is made evident by the excessive capex affecting free money move, however it additionally reduces flexibility and may have an effect on profitability by making the corporate much less agile and exposing it to dangers with sure components of its mannequin turning into redundant as technological capabilities and manufacturing processes change. Because of this, I believe its vertical integration is a double-edged sword, and I consider JKS shareholders must maintain progress prospects reasonable in opposition to different business opponents, primarily as a result of the extent of debt the corporate has taken on to fund enlargement is simply too excessive proper now, in my view.

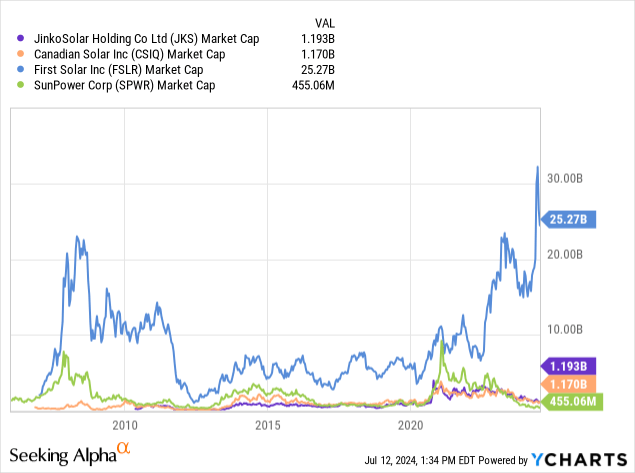

On the word of competitors, the corporate’s major direct opponents are Canadian Photo voltaic (CSIQ), Trina Photo voltaic, First Photo voltaic (FSLR), and SunPower (SPWR).

Of those, First Photo voltaic stands out as being a lot bigger than its smaller direct opponents, and as such, I believe it has the aptitude to proceed to consolidate its moat, significantly in the US, which is its core market (96% of income) in comparison with JKS, which is extra globally diversified. Because of this, I believe extra stress might be positioned on Chinese language imports of Photo voltaic, particularly underneath Trump, which may diminish the expansion alternative in the US, which is among the main adopters of photo voltaic vitality.

Most notably, the best risk is arguably from Trina Photo voltaic, which has know-how management with its 210mm product and N-type i-TOPCon know-how, which is in direct competitors with JinkoSolar’s N-type panels. It has a number of world data in effectivity and energy output, and is equally geographically diversified to JinkoSolar. It has a market cap of $962.5M.

In my view, JinkoSolar has confirmed it’s dedicated to remaining aggressive via its personal N-type providing, and I do not doubt administration’s functionality within the discipline, which is made notable via its sturdy income progress. Nonetheless, I stress once more that whereas I do think about this a deep-value alternative in the mean time, in just a few years’ time, when the corporate is extra pretty valued, the capital construction and progress in profitability will likely be paramount to observe to deal with whether or not the inventory is value holding as soon as it’s extra pretty valued.

Conclusion

In my view, it is a deep-value funding that ought to play out properly over the subsequent 1 to 2 years. Nonetheless, I believe there may be some concern with unfavorable momentum in the mean time within the inventory, so buyers could wish to wait till it’s clearer that the upside has begun earlier than initiating a place. That being stated, from right here towards a extra truthful worth, the potential 1 to 2-year worth progress appears substantial to me. As well as, to assist climate any draw back from the present momentum earlier than my forecasted appreciation, the inventory additionally has a dividend yield of 6.5%.

[ad_2]

2024-07-16 08:35:53

Source :https://seekingalpha.com/article/4704231-jinkosolar-deep-value-opportunity-despite-balance-sheet-concerns?source=feed_all_articles

{kind=link}

Discussion about this post