[ad_1]

Angel Di Bilio

The final article that I wrote that was devoted to JetBlue Airways (NASDAQ:JBLU) was revealed in late January of this yr. At the moment, I used to be assessing the scenario relating to that firm and Spirit Airways (SAVE) as uncertainty began to develop relating to the feasibility of the merger between the 2 corporations closing. In the end, the merger did fail due to regulatory considerations. And since my article in January, shares of JetBlue Airways have carried out properly. Since my article through which I rated the corporate a ‘purchase’, the inventory is up 13.4%. That is a bit higher than the 11.8% rise seen by the S&P 500.

As nice as this outperformance is to see, this comes at a time when basic efficiency for the enterprise has taken successful. When administration introduced monetary outcomes for the primary quarter of this yr, income got here in decrease than it did a yr earlier. Along with this, each revenue and money movement metric that I checked out relating to the agency suffered on a yr over yr foundation. The excellent news is that administration is taking some daring steps aimed toward shoring up operations and making a leaner, extra environment friendly, enterprise transferring ahead. However as with every type of initiative like this, there isn’t any assure it would work.

The excellent news for buyers is that, on July thirtieth, simply earlier than the market opens, administration is predicted to announce monetary outcomes masking the second quarter of the corporate’s 2024 fiscal yr. Main as much as that point, analysts do anticipate a worsening on each the highest and backside strains. However with administration targeted on some huge value chopping plans and targeted on boosting ancillary income, the image may not end up all that terrible. On prime of this, shares are nonetheless attractively priced. And if we are able to get proof of significant enhancements, I feel that additional upside might be justified.

A have a look at latest outcomes

Writer – SEC EDGAR Knowledge

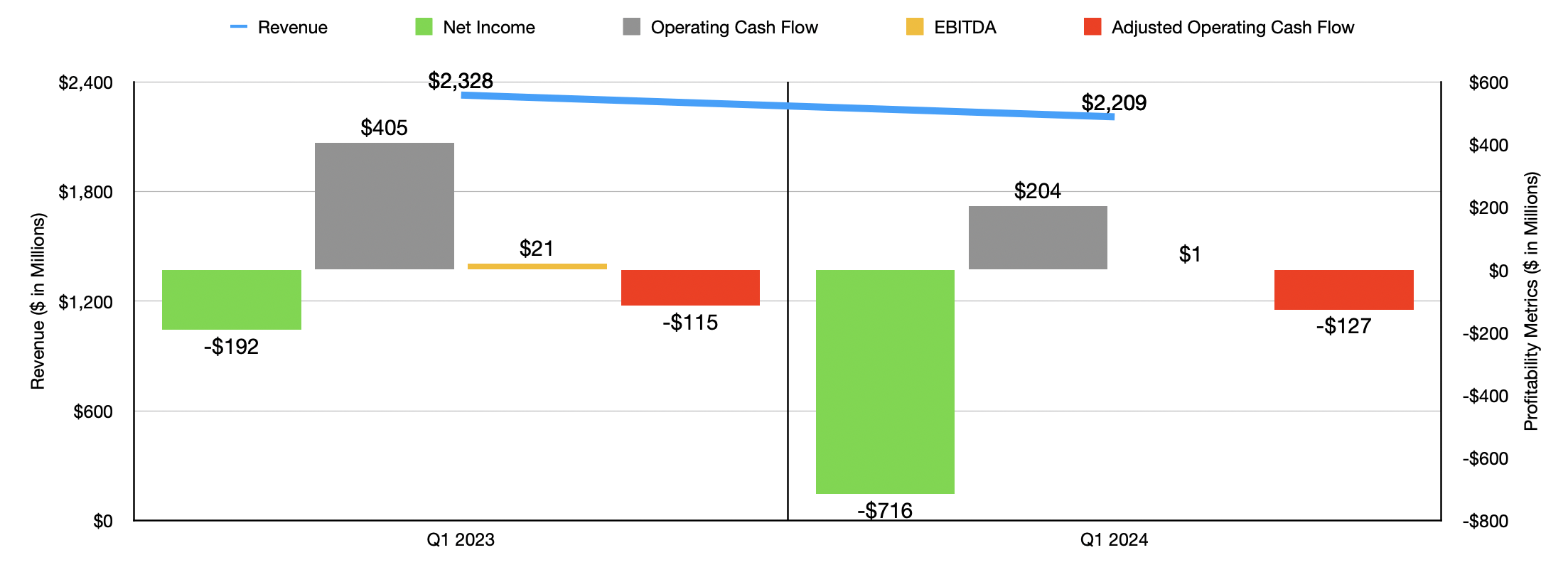

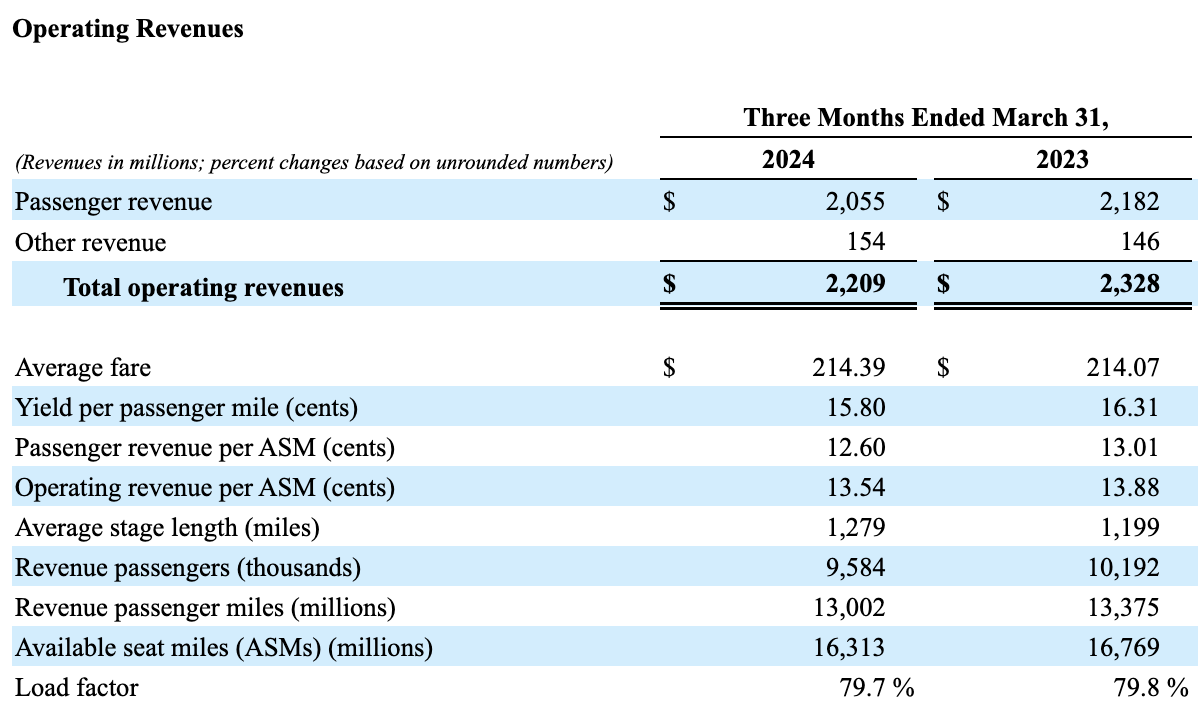

Essentially talking, JetBlue Airways has had higher days. Through the first quarter of the corporate’s 2024 fiscal yr, as an example, income got here in at $2.21 billion. This represents a decline of 5.1% in comparison with the $2.33 billion reported only one yr earlier. This got here though the typical fare per passenger inched up from $214.07 to $214.39. A 3.1% decline in yield per passenger mile harm the corporate. However the greatest hindrance appears to have been a decline within the variety of income passengers from 10.19 million to 9.58 million.

JetBlue Airways

This struck me as odd at first. I say this as a result of, based on the US Bureau of Transportation Statistics, whole passenger enplanements through the first quarter of the 2024 calendar yr got here in at 226.24 million. That occurs to be 6.2% above the 213.06 million reported for a similar window of time of the 2023 calendar yr. Due to profitability points, the corporate has made it a precedence to close down operations in sure underperforming markets. Despite the fact that it is not included in first quarter outcomes, as of June of this yr, the corporate fully pulled out of Kansas Metropolis, Missouri, Bogota, Colombia, Quito, Ecuador, and Lima, Peru. And in some markets the place it is staying, it is chopping down on the variety of flights. Actually, beginning in April of this yr, the agency reduce down on the variety of every day flights working out of the LaGuardia airport from 50 to 30.

With income falling, particularly in such a low margin, asset intensive enterprise, it shouldn’t come as a shock that the agency would see income and money flows take successful as properly. Within the first quarter of final yr, the corporate generated a internet lack of $192 million. That loss exploded to $716 million the identical time this yr. It’s price noting {that a} good chunk of the ache that the corporate skilled within the first quarter of this yr was due to $562 million and bills that the agency incurred due to its makes an attempt to merge with Spirit Airways. That is up from solely $112 million one yr earlier. Working money movement was reduce by practically half from $405 million to $204 million. And even when we alter for modifications in working capital, we get a slight worsening from destructive $115 million to destructive $127 million. And lastly, EBITDA for the enterprise fell from $21 million to solely $1 million.

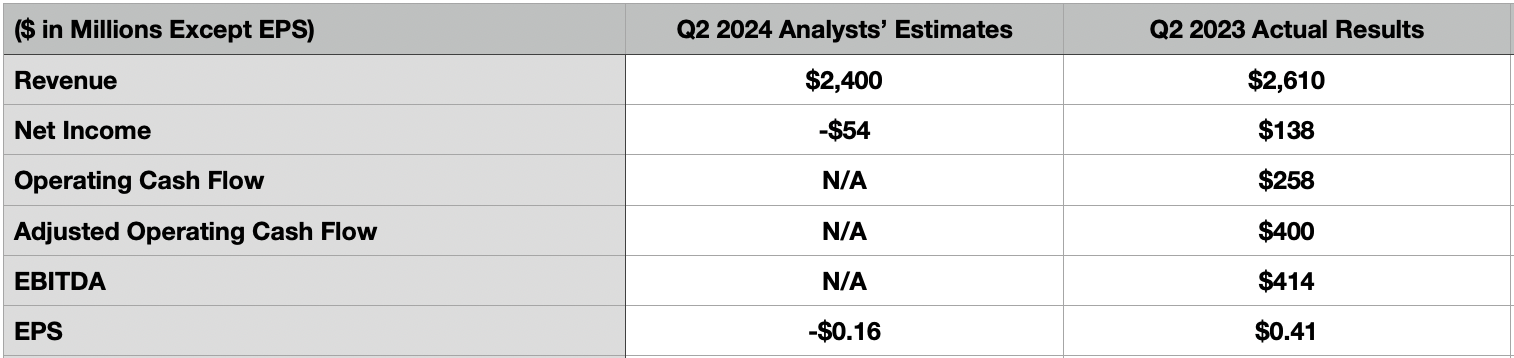

Relating to the second quarter of the 2024 fiscal yr, administration has already supplied some ideas on what the image would possibly appear to be. They mentioned that general income ought to drop by between 6.5% and 10.5% in comparison with what it was final yr. This may indicate income of between $2.34 billion and $2.44 billion. This comes because the variety of out there seat miles for the corporate declines by between 2% and 4%. Analysts have taken word and are at the moment anticipating gross sales of about $2.40 billion. That is down from the $2.61 billion the corporate reported for the second quarter of 2023.

Writer – SEC EDGAR Knowledge

Naturally, the underside line can also be taking successful. Analysts imagine that earnings per share will likely be destructive to the tune of $0.16. That might be down from the $0.41 per share reported final yr. It could additionally imply a decline in profitability from $138 million to destructive $54.4 million. Clearly, a few of this ache is due to the forecasted drop in gross sales and the affect that can have on margins alone. Nevertheless, administration additionally expects the price per out there seat mile, excluding gasoline, to rise by between 5.5% and seven.5% on a yr over yr foundation. Within the desk above, you may see another profitability metrics for the second quarter of 2023. In all probability, these may even worsen yr over yr.

As disappointing as these expectations may appear, administration is working laborious on bettering issues. If the corporate is to be believed, then there needs to be someplace round $275 million of annualized value financial savings captured by the enterprise all through this yr. That is along with $300 million price of income initiatives that the corporate is focusing on for this yr, round $40 million of which was achieved within the first quarter alone. This extra forecasted income is predicted to come back from numerous maneuvers the corporate is making, corresponding to the advantages of rebalancing its community to give attention to extra worthwhile areas, and capturing seat ancillary gross sales.

Writer – SEC EDGAR Knowledge

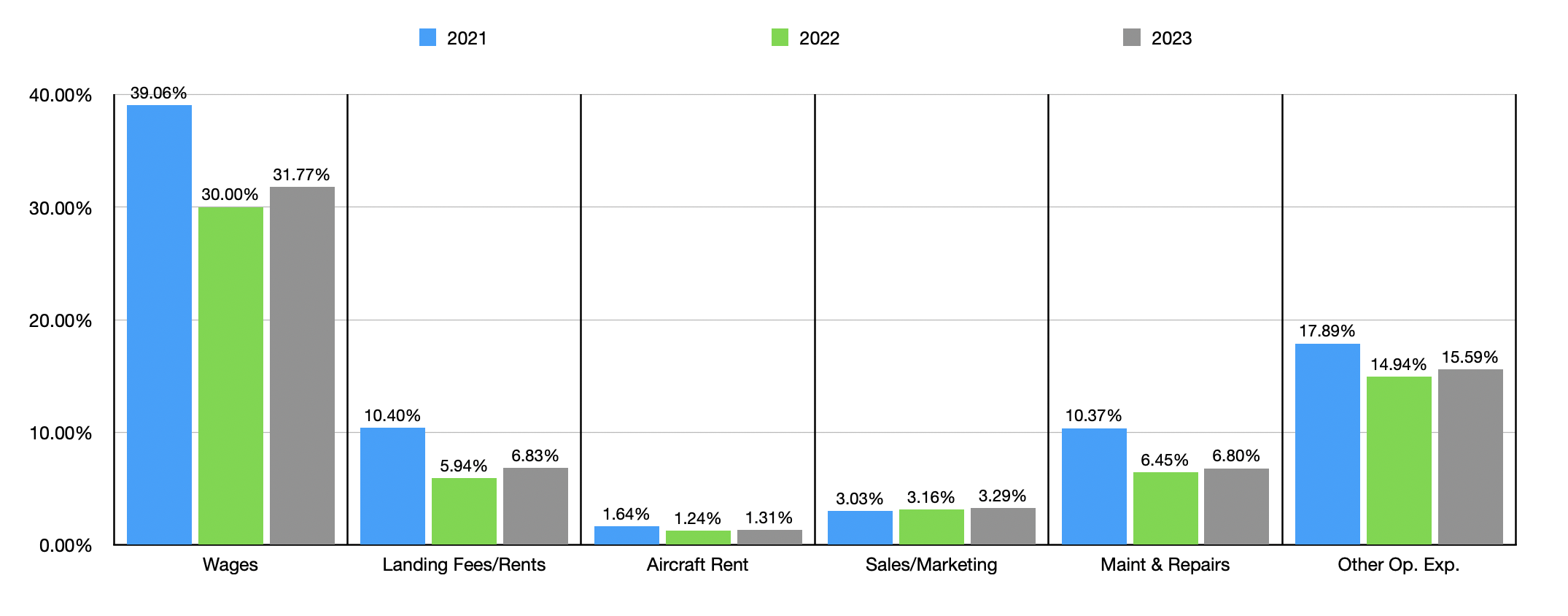

I’m glad that administration is pushing to chop these bills. In spite of everything, as you may see within the chart above and within the chart under, margins relating to non-fuel expense objects which might be core to the enterprise have largely exploded as of late. Admittedly, the image is generally higher than it was again in 2021. However that was an uncommon time for the reason that airline business was nonetheless coping with the fallout of the COVID-19 pandemic. It is simply this yr that we’re seeing world air site visitors rise above what it was earlier than the pandemic. However sadly, with wages taking pictures by means of the roof, to not point out different larger prices like touchdown charges and different miscellaneous bills, value chopping is crucial at this level. However between the price chopping plans that the corporate is diligently engaged on, and the agency’s skill to defer round $2.5 billion in capital spending relating to issues like plane supply, I stay cautiously optimistic about what’s to come back.

Writer – SEC EDGAR Knowledge

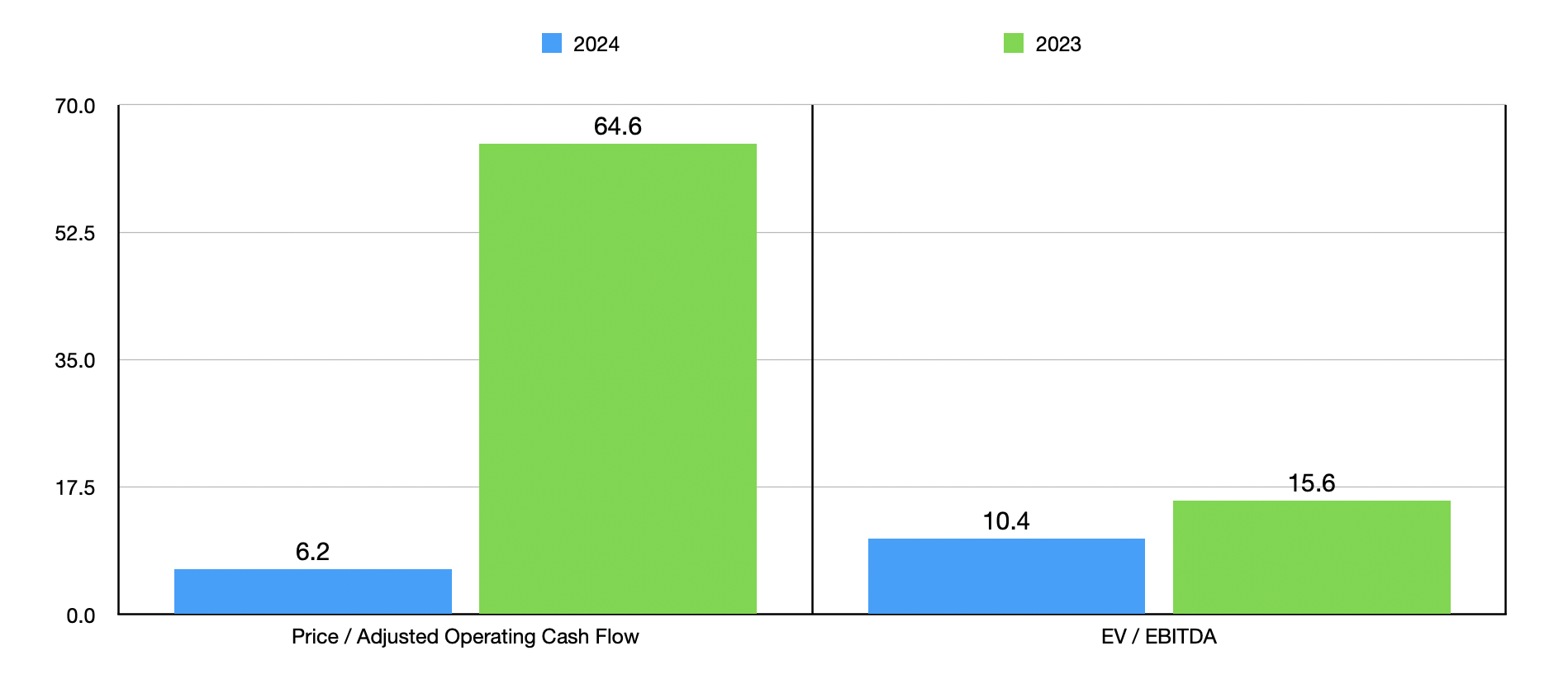

Sadly, all of this uncertainty makes valuing the corporate actually difficult. We do not know what the remainder of this yr will appear to be. We do know that administration is forecasting a low single digit decline in income. And in all probability, this yr will look worse than final yr was, even with value chopping initiatives in play. However with world air site visitors prone to proceed climbing for the foreseeable future, it is not unreasonable to suppose that monetary efficiency may finally get again to what it was final yr. Within the chart under, you may see how shares can be valued if this does come to move. And on this case, the inventory does look pretty attractively priced.

Writer – SEC EDGAR Knowledge

Takeaway

The previous few months have been good for shareholders of JetBlue Airways. The inventory has outperformed the broader market since my final standalone article on the enterprise. However this doesn’t suggest that this image will proceed ceaselessly. The very fact of the matter is that JetBlue Airways does have some actual issues. Nevertheless, administration additionally has plans for addressing these issues. Naturally, we’ll wish to see what the information seems to be like when it does come out within the coming days. If the agency does fall in need of expectations and/or if he comes clear that value chopping will not be materializing in a means that it ought to, a downgrade of the inventory would completely be warranted. However for now, I am conserving the enterprise rated a smooth ‘purchase’.

[ad_2]

2024-07-26 08:43:59

Source :https://seekingalpha.com/article/4707017-jetblue-airways-lot-riding-on-upcoming-earnings?source=feed_all_articles

{kind=link}

Discussion about this post