[ad_1]

JHVEPhoto

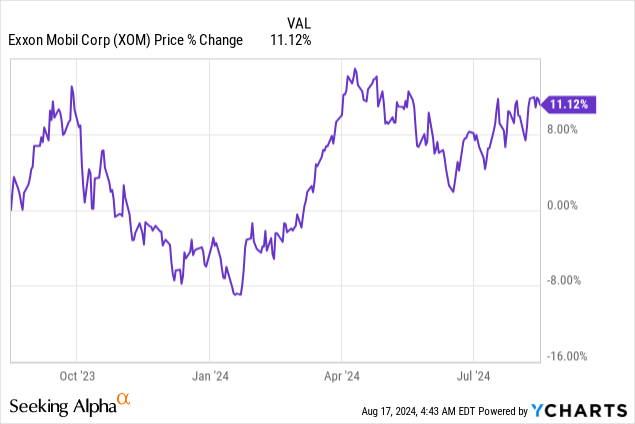

Exxon Mobil (NYSE:XOM) generated a substantial quantity of free money movement from its operations within the second-quarter and guided for $20B of annual inventory buybacks till the tip of subsequent yr. ExxonMobil nonetheless advantages from petroleum costs within the $70s worth vary and can probably proceed to generate a variety of free money movement from its manufacturing belongings going ahead, particularly after the corporate’s $60B acquisition of Pioneer Sources, which has already began to make a optimistic manufacturing impression. In my view, ExxonMobil continues to be a pretty funding for revenue buyers particularly and shares are priced at a really cheap P/E ratio of 12.6X.

Earlier score

I rated shares of ExxonMobil a powerful purchase in June after OPEC+ introduced the extension of provide limitations which offered essential assist to petroleum costs: OPEC+ Driving Earnings Upside. I consider the finished Pioneer Sources acquisition will likely be a lift to the corporate’s manufacturing volumes which in flip must be a optimistic catalyst without spending a dime money movement development. With $20B in inventory buybacks this yr and subsequent yr, I consider ExxonMobil is doing the proper factor.

Manufacturing features mirrored in Exxon Mobil’s Q2, strong free money movement

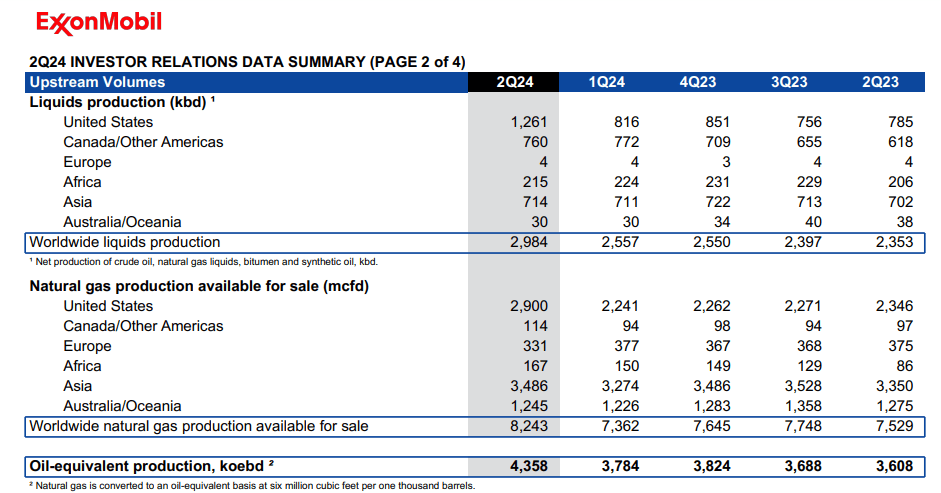

ExxonMobil introduced the acquisition of Pioneer Sources final yr for $60B in an all-stock transaction. The acquisition was meant to mainly enhance ExxonMobil’s U.S. manufacturing, particularly within the excessive potential Permian basin. Following the shut of the transaction, ExxonMobil expects to double its manufacturing to 1.3M barrels of oil equal per day within the Permian. ExxonMobil is already seeing a substantial enhance to its U.S. liquids manufacturing in addition to complete worldwide manufacturing in Q2’24. Within the second-quarter, ExxonMobil’s U.S. operations produced 1.26M barrels of oil equal per day, exhibiting 55% quarter-over-quarter development. ExxonMobil’s complete worldwide liquids manufacturing did not climb practically as considerably as U.S. manufacturing, however it was nonetheless up 17% quarter-over-quarter.

ExxonMobil

The primary cause to purchase ExxonMobil, in my view, is that the petroleum firm derives a substantial quantity of recurring free money movement from its strategic manufacturing belongings, particularly within the U.S. ExxonMobil generated $5.0B in free money movement within the second-quarter (after the completion of asset gross sales) which implies that the corporate didn’t see any free money movement development in any respect on a year-over-year foundation. Nonetheless, ExxonMobil’s accomplished Pioneer Sources acquisition is ready to be a significant free money movement catalyst going ahead as the corporate has guided to double its Permian manufacturing after the shut of the transaction.

Moreover, OPEC+ has confirmed to be extremely accommodating this yr when it comes to extending provide cuts. By limiting manufacturing in key manufacturing nations, particularly Russia and Saudi Arabia, OPEC+ has helped stabilize and assist petroleum costs which advantages giant producers like ExxonMobil.

|

Exxon Mobil |

FY 2024 |

FY 2023 |

||||

|

$B |

Quarter 2 |

Quarter 1 |

Quarter 4 |

Quarter 3 |

Quarter 2 |

Y/Y Progress |

|

Money Circulation from Working Actions |

$10.6 |

$14.7 |

$13.7 |

$16.0 |

$9.4 |

12.8% |

|

Proceeds from Asset Gross sales |

$0.9 |

$0.7 |

$1.0 |

$0.9 |

$1.3 |

-30.8% |

|

Money Circulation from Operations and Asset Gross sales |

$11.5 |

$15.4 |

$14.7 |

$16.9 |

$10.7 |

7.5% |

|

PP&E Provides / Investments & Advances |

($6.5) |

($5.3) |

($6.7) |

($5.2) |

($5.7) |

14.0% |

|

Free Money Circulation |

$5.0 |

$10.1 |

$8.0 |

$11.7 |

$5.0 |

0.0% |

(Source: Writer)

Exxon Mobil’s valuation

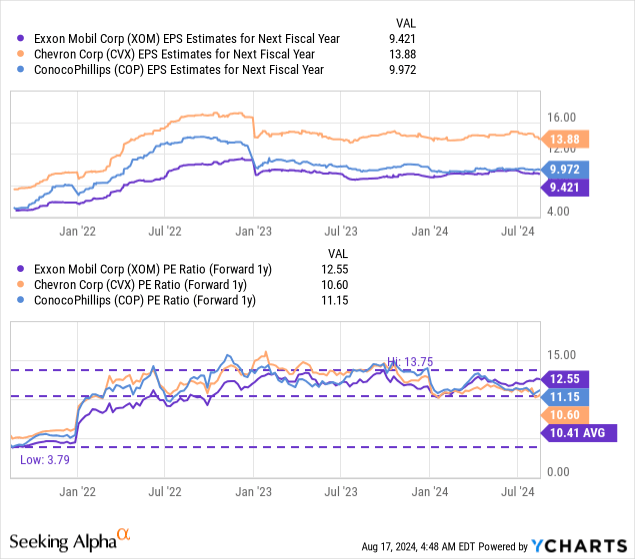

Shares of ExxonMobil are presently valued at a price-to-earnings ratio of 12.6X which is about 20% greater than the long term P/E common of 10.4X. Chevron, ExxonMobil’s largest rival within the U.S. power market, is buying and selling at a price-to-earnings ratio of 10.6X and ConocoPhillips (COP), which is a pure-play upstream firm, has a P/E ratio of 11.2X.

Because of ExxonMobil’s sturdy free money movement, giant dimension and sturdy capital return plan, I consider ExxonMobil might commerce at 13-14X FY 2025 earnings which, assuming a consensus earnings estimate of $9.42, implies a good worth vary between $122 and $132 per-share.

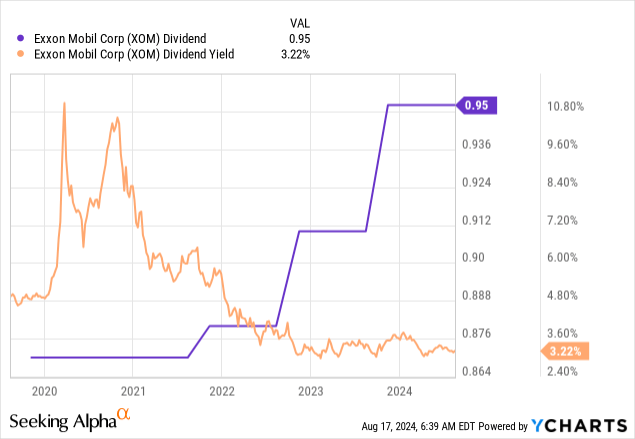

One of the best cause to personal shares of ExxonMobil, in my view, pertains to the corporate’s capital return potential. The petroleum firm guided for greater than $19B in inventory buybacks this yr and ~$20B subsequent yr. Moreover, ExxonMobil pays a rising dividend that’s backed by the corporate’s appreciable manufacturing belongings, each within the U.S. and overseas. ExxonMobil gives a strong 3%+ dividend yield and the corporate’s dividend has been rising, indicating that the corporate could possibly be a pretty capital return play for buyers going ahead.

Dangers with Exxon Mobil

ExxonMobil is and can stay depending on excessive petroleum costs which is each a energy and a weak spot. To this point, OPEC+ has offered appreciable assist for markets by extending provide cuts till the tip of FY 2025. Nonetheless, there are dangers to manufacturing development in ExxonMobil’s portfolio, particularly because it pertains to fossil gas investments. Any type of laws limiting investments within the fossil gas business would probably additionally restrict ExxonMobil’s earnings and free money movement potential. What would change my thoughts about XOM is that if the corporate have been to see a drastic lower in its free money flows and a cut-back in inventory buybacks.

Remaining ideas

I nonetheless like ExxonMobil: the petroleum firm closed the Pioneer Sources acquisition within the second-quarter which is now already making a optimistic contribution to ExxonMobil’s liquids manufacturing. Additional, the corporate is trying to double Permian manufacturing which bodes properly for the corporate’s natural free money movement development… particularly with petroleum costs holding regular within the mid-seventies. Moreover, I like that ExxonMobil could be purchased for what I consider is a really cheap price-to-earnings ratio. The chance profile, in my view, continues to be very a lot skewed to the upside right here and revenue buyers with a long run funding focus are probably going to learn from rising dividend revenue over time.

[ad_2]

2024-08-19 02:02:05

Source :https://seekingalpha.com/article/4715508-exxon-mobil-stock-capital-return-dividend-growth-play?source=feed_all_articles

{kind=link}

Discussion about this post