[ad_1]

Richard D. Affolder/iStock through Getty Pictures

Evolution Petroleum Company (NYSE:EPM) is an vitality small-cap targeted on onshore oil and fuel in the USA. Its technique is to construct a portfolio of diversified belongings by creating and buying non-operating pursuits in a number of fields throughout the USA. Within the first quarter of 2024, EPM had a mean each day manufacturing (BOEPD) of seven,209. Nevertheless, whereas manufacturing has been up 1.7% since final yr, costs weighted per unit had been truly down 39.3%, destroying margins (2024Q3 MD&A, web page 33).

After just lately transitioning in direction of extra oil fields, its reserves are break up as follows: 49% pure fuel, 32% oil, and 19% NGL (pure fuel conversion ratio of 6:1). Evolution’s giant fuel manufacturing means it profited closely on the spike in fuel costs but additionally acquired harm by the following crash. Evolution tends to make use of little hedges, leaving a big upside when fuel costs finally get better.

Evolution’s technique is to purchase counter-cyclical belongings, sharply priced by the low commodity costs. Their latest SCOOP/STACK and Chaveroo acquisitions present they’re now evolving in direction of long-life manufacturing, making them extra resilient to commodity value downswings.

Administration’s efficient technique, together with their nice set of diversified belongings at ridiculously low costs, makes it a transparent, robust purchase for my part.

Asset Overview

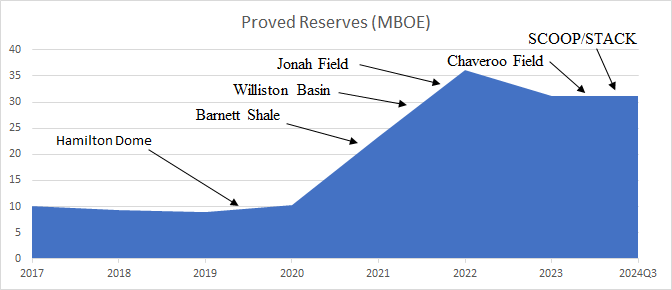

From October 2019 by way of February 2024, Evolution has participated in six main transactions, placing over $119 million to work for our shareholders. Throughout that point, we have paid down over $41 million of borrowings, whereas our share rely has remained just about unchanged. (2024Q3 Earnings Name).

Beginning in 2023, Evolution has taken a brand new path with the Chaveroo and SCOOP/STACK acquisitions. Evolution used to buy mature wells, late within the stage of manufacturing, that means small depletion charges, however little resiliency to low commodity costs. Now, with fuel costs hitting lows of $1.53/MMBtu in 2023, administration had alternatives to purchase counter-cyclical belongings at depressed costs, explaining the $42.5M enhance in debt.

Reserves Progress and Acquisitions (Annual Studies)

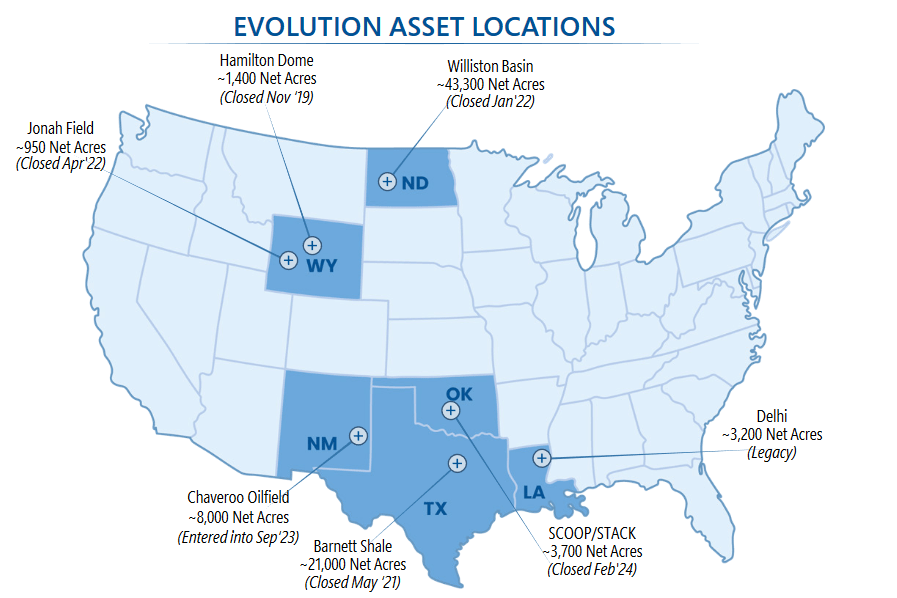

Earlier than the acquisitions, the Delhi Discipline was Evolution’s foremost asset. Final quarter, it produced 1,022 BOEPD, comprising 71% oil and 29% pure fuel liquids (NGL). Although it is one in all Evolution’s legacy belongings, its working associate continues to be increasing the sphere. Evolution diversifies by constantly proudly owning small working pursuits (principally) in giant quantities of wells in numerous fields.

Asset Places (Evolution)

Let’s deal with the efficiency of their latest acquisitions, beginning with their earliest.

Hamilton Dome/Williston

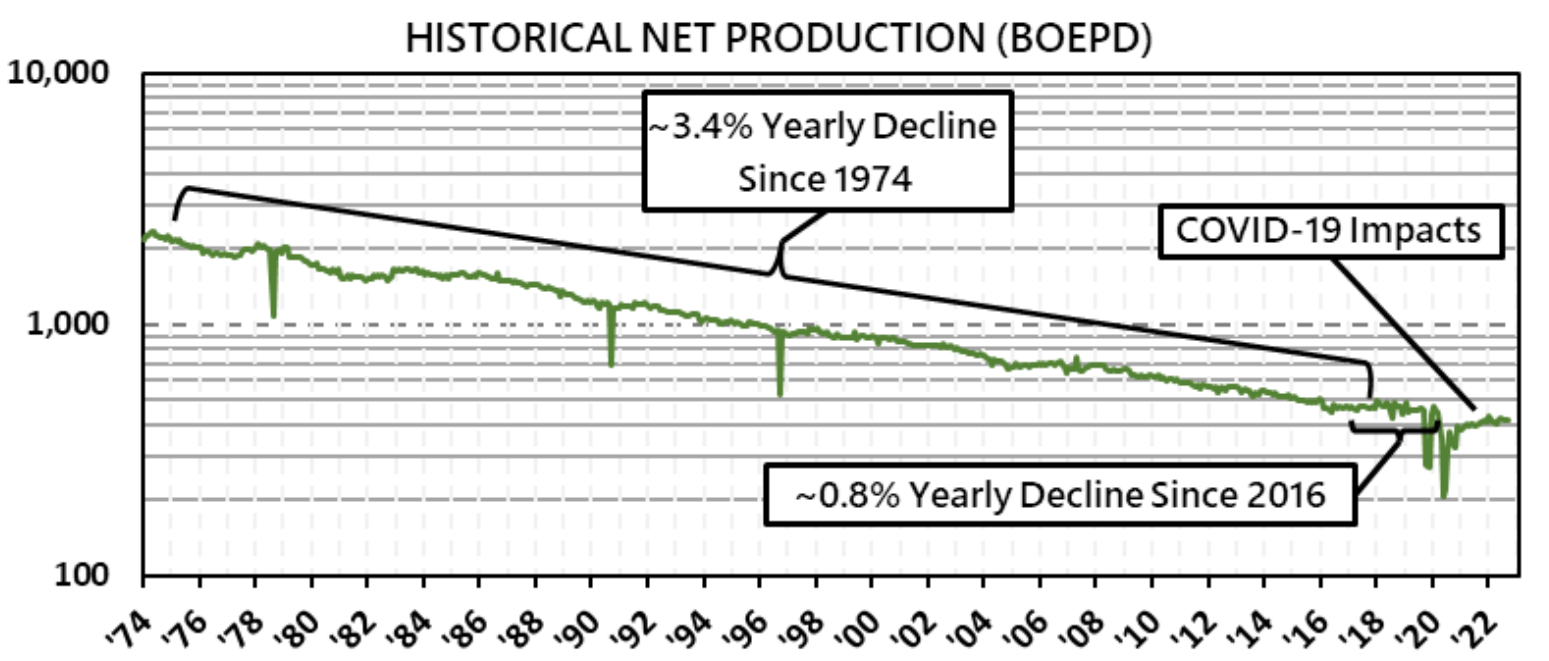

Evolution acquired the complete oil Hamilton Dome discipline for $9.5M in November 2019. Since then, manufacturing has been fairly constant, moreover the COVID disruptions. The depletion fee has been slowing down and is now at 0.8% yearly since 2016. Their funding has achieved magnificently, and I calculated a 21% inner fee of return with the next standards.

Final quarter’s manufacturing sat at 385 BOEPD, offered at oil costs of $61.21/bbl for the previous 91 days. This resulted in $1.56M of revenues, and $578K of pre-tax quarterly revenue, excluding administrative prices. And consider, these numbers are barely impacted by workover tasks originally of the quarter. Yearly, this transfers to $2.3M of working money move.

For the IRR calculation, assume a 2% annual decline fee. And calculate it over the following 15 years as a result of Hamilton Dome’s present Web PDP Reserves/ Web Manufacturing sits at 16 years. At its manufacturing value of $9.5M, the inner fee of return sits at 21%, conservatively calculated, which is noteworthy.

Hamilton Dome’s Web Manufacturing (EPM)

Equally to Hamilton Dome, the Williston discipline is basically an oil discipline (74%). With 462 BOEPD, it provides one other layer of diversification and publicity to grease for Evolution.

Jonah Discipline/Barnett Shale

Realized pure fuel costs decreased 71.7% from the prior yr interval, which was the most important portion of the motive force of the lower in revenues. This was partially attributed to the prior yr interval advantage of robust pure fuel value differentials obtained on the Jonah Discipline the place we realized a mean pure fuel value of $20.31 per MCF within the prior yr interval in comparison with $3.94 per MCF within the present yr quarter. (MD&A 2024).

The Jonah Discipline was bought for $27.5MM and closed on April 1, 2022. Its commodity break up seems as follows: 88% pure fuel, 7% NGL, and 5% oil. It produces 10.4 MMCFEPD, which equates to 1,736 BOEPD with a 6:1 conversion ratio. Primarily based on present costs, that ratio is definitely nearer to 40:1, so do not put an excessive amount of belief within the weighted BOEPD numbers. The Jonah Discipline considerably profited from the spike in fuel costs, repaying the funding in two years.

Jonah Discipline sits at 21% of Evolution’s complete reserves, and Barnett Shale sits at 40%. These percentages are possible overstated as a result of they use the 6:1 pure fuel conversion ratio. Nevertheless, when fuel costs revert to their imply, this leaves a big upside for Evolution.

SCOOP/STACK and Chaveroo

The addition of Chaveroo and SCOOP/STACK are good suits for our evolving technique of each including long-life manufacturing throughout commodity value downswings and including undeveloped areas by making acquisitions by way of the drill bit. (Q3 Earnings Name).

For his or her new acquisitions, SCOOP/STACK reaches round 1,550 BOEPD at a 6:1 pure fuel conversion ratio, comprising 40% oil, 13% NGL, and 47% pure fuel. For $40.5M, Evolution purchased a ~3% working curiosity in 247 lively wells, with the potential for cooperating on 300+ extra with its operators. This makes it extremely diversified, however tough to promote within the occasion of a liquidation. The low liquidity on these small pursuits creates shopping for alternatives for administration.

SCOOP/STACK receives the best gross sales costs of all Evolution’s fields. Simply assuming steady manufacturing with steady costs at a 30% netback margin results in $3.2M of funds from operations (FFO) for a single quarter. For under $40.5M!

Chaveroo is one other welcome addition to Evolution, particularly including to its oil publicity. There are presently three wells in manufacturing, with a 41% NRI. Moreover, in response to their Q3 Earnings Name: At the side of the operator, we’re planning to drill the following 4 wells starting in September 2024, adopted by one other six wells starting in April 2025.

These are wells paying again in 16 months! After every pays itself again, assume a long-term, slowly reducing manufacturing of round 50 BOEPD. Yearly, at a $40/bbl netback at a 41% NRI, this provides an additional $300K of yearly money move per effectively.

Chaveroo effectively manufacturing curve (Evolution Investor Presentation)

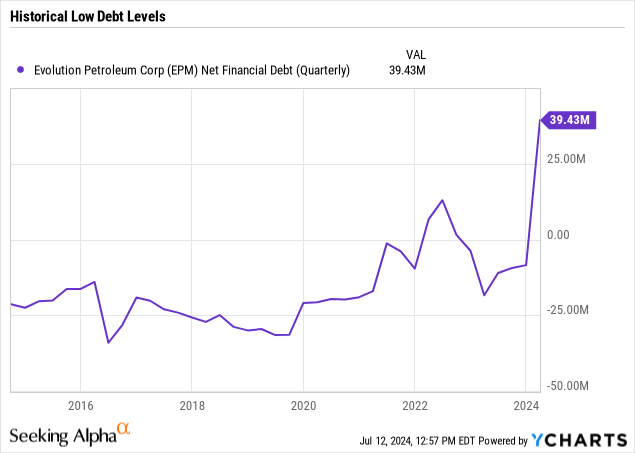

Heightened Leverage

The latest SCOOP/STACK acquisitions had been funded by taking out $42.5M in borrowings beneath the Senior Secured Credit score Facility. This doesn’t but mirror the influence of internet money Evolution expects to obtain for the ultimate buy of the acquisitions. Administration goals to maintain their internet debt to professional forma EBITDA ratio beneath 1x. This means administration is devoted to shortly paying down debt. Nevertheless, they did state that this should not be a purpose to cross on every other enticing offers coming their approach.

As may be seen by Evolution’s historic internet debt ranges, it is extremely uncommon for administration to take out such a big debt place, this heightens the danger of default within the case of sustained decrease costs. However, this implies administration’s confidence in greater costs going ahead and the enticing value of its latest acquisitions. As can be mentioned later, this threat is balanced out by them promoting fuel futures, which stand considerably greater trying a yr later.

In keeping with their 10-Q (Notice 5. Senior Secured Credit score Facility):

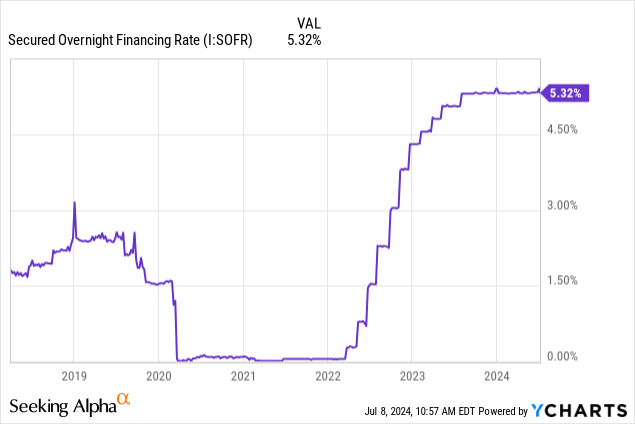

On Might 5, 2023, Evolution prolonged the maturity of its debt contract to April 9, 2026. They’re borrowing on the Secured In a single day Financing Price (I:SOFR) plus 2.80%, with a minimal of 0.50%, or on the Prime Price plus 1.00%. Concurrently, the worth of the belongings backing the mortgage was elevated to $95 million. Their renewed contract now permits for extra versatile hedges.

Their present rate of interest quantities to eight.12% (5.32% + 2.80%). Assuming they do not prolong the maturity date, they usually pay down the debt in three years, they’d begin off paying $3.45M in curiosity, taking place shortly afterward as they pay down 14.2M of the principal yearly over three years. This excludes the online money they already obtained after the completion of the acquisition.

Fuel Costs

Evolution’s Proved Reserves are made up of 49% Pure Fuel and 19% NGL. Its 2024Q3 income consisted of 63% of oil, nonetheless, as fuel costs have been hitting lows, down 85% from their 2022 peak. The inherent cyclic nature of the fuel market makes for some nice counter-cyclical buys, now EPM is down 45% in nearly a yr.

Whereas the fuel business will proceed to slowly develop at the least over the following 15 years, it would lose market share to renewables. Nevertheless, fuel will stay an integral a part of the worldwide vitality market. Because the world appears to be destroying its vitality infrastructure, pure fuel can be there to again up the failures of unreliable renewables. In keeping with the EIA, in 2023, 33% of U.S. vitality consumption nonetheless got here from pure fuel.

I feel this quote sums it up fairly effectively: Coal is just too soiled. Oil is just too messy. And renewables are too intermittent. However pure fuel is good. -Chris Tomlinson

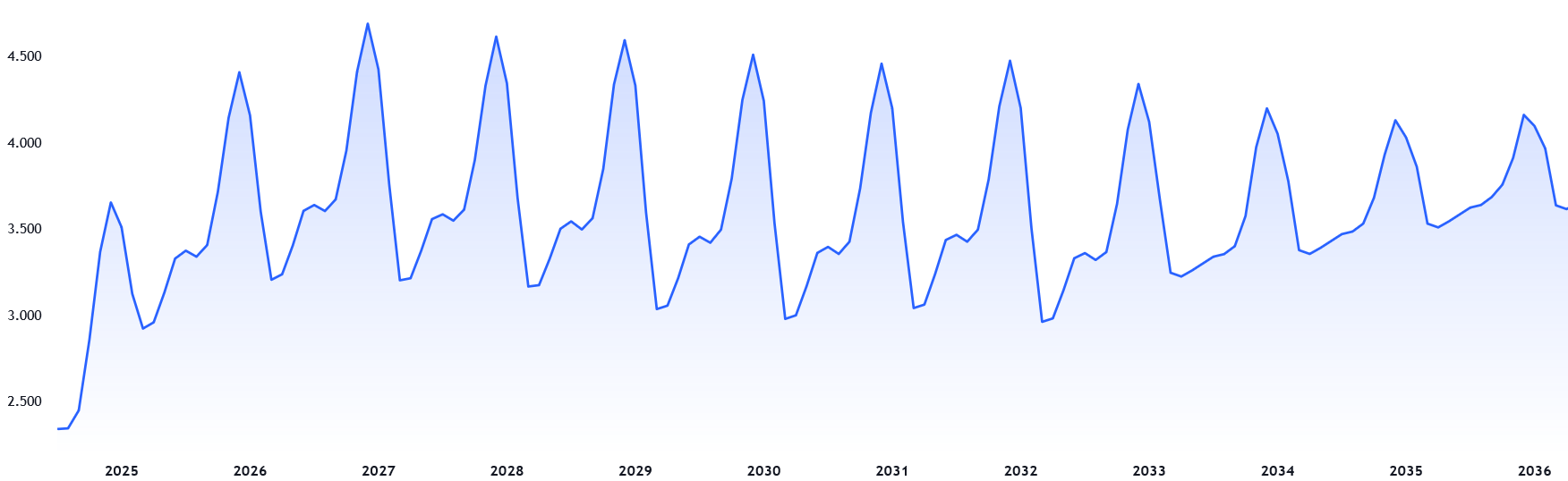

The largest purpose this chance exists is due to worry round future fuel costs. However, taking a look at fuel futures, greater costs appear to be partially sure. Particularly contemplating what Evolution introduced of their Q3 earnings name:

We additionally hedged pure fuel past the required 12-month interval to capitalize on the excessive costs out there within the calendar yr 2025 and past.

Fuel Futures Ahead Curve Henry Hub USD/MMBTU (TradingView)

Dangers

Whereas hedging future commodity costs takes away a big chunk of potential dangers, their heightened leverage makes them extra vulnerable to different dangers. Evolution owns small working pursuits in fields it would not function. Operators may make Evolution contribute capital expenditures when it’s already tight on money. Moreover, its discipline operators’ self-interest could not all the time be aligned with that of Evolution.

Evolution’s operations could encounter extra workover than anticipated. Their legacy belongings particularly, since these shallow reserves require dearer drilling. Most necessary of all, is its commodity pricing threat. If oil costs fall and fuel costs keep low or go even decrease, they’re going to battle to pay down debt, and it may get ugly, even with hedges in place.

Valuation And Dividend

Evolution has been paying out $4 million in quarterly dividends for the final 7 quarters. This is a mannequin breaking down their last-quarter manufacturing and costs. I added a piece mentioning what would occur if fuel costs had been to normalize, which they’ve already partially capitalized on with future contracts.

| 2024Q3 | Nat Fuel (MBBL) | LNG (MMCF) | Oil (MBBL) | Whole |

| Whole Manufacturing | 2,115 | 104 | 199 | |

| Present Worth | $2.77/MCF | $25.26/bbl | $73.06/bbl | |

| Revenues | $5.9M | $2.6M | $14.5M | $23M |

| Potential Worth | $5.00/MCF | $30.00/bbl | $70.00/bbl | |

| New Revenues | $10.58M | $3.1M | $13.9M | $27.6M |

The important thing assumption right here is that pure fuel costs had been to go to $5.00/MCF. And if fuel costs had been to return to $7.50/MCF, that will add one other $5M+ to revenues.

Bills

Let’s deduct all of their bills: $10M for LOE, $1.5M for CO2 prices, $2M for G&A, together with stock-based compensation, and $2.5M for elevated curiosity bills. And at last, assume $2M tax prices, closely depending on income. This totals $18M in complete prices, which seems barely conservative, contemplating Funds From Operations was $8.64M in 2024Q3.

| Lease Working Bills | CO2 Prices | G&A | Curiosity Bills | Taxes |

| $10M | $1.5M | $2M | $2.5M | $2M |

Dividend

Evolution is dedicated to persevering with their capital spending even throughout low commodity costs. Administration would not present any steering for capital expenditures going ahead. It is going to largely rely on how a lot free money move Evolution can generate after paying down debt and the bottom dividend.

Assuming costs restore to the “Potential” value I wrote above, we’d see round 10M of FFO, after which we’ll see a couple of million of capital expenditures, $3M would maintain operations and fortunately help the drilling of recent wells in SCOOP/STACK and Chaveroo. Now, with $7M of FCF, we nonetheless want the debt principal repayments of $3.5M per quarter. This leaves us with $3.5M for the dividend, simply wanting the $4M quarterly funds. Contemplating they’ve $11M in money, the dividend will proceed to be comfortably payable sooner or later.

| Revenues on Restored Costs | Whole Prices | Capex | Debt Reimbursement | Dividend |

| $28M | $18M | $3M | $3.5M | $3.5M |

Personally, I am not an enormous fan of constantly paying dividends by way of downturns as they must dip into their working capital (presently at $7.5M). Sadly, they must please the market, and it’s comprehensible; that is how the market works. At the moment, Evolution is providing an 8.80% dividend yield.

Evolution Petroleum cannot actually be valued utilizing EV/EBITDA, as a result of the latest debt enhance disrupts its enterprise worth, whereas manufacturing hasn’t adopted but. This is a DCF to attempt to estimate a price for the intermediate run when costs have barely recovered, as seen above within the “Potential” value.

For its preliminary annual FCF, we multiply the quarterly $7M by 4. Assume a 3% progress fee over 10 years, since they’re significantly investing in progress. I used a P/FCF ratio of 5, which appears adequately conservative, traditionally.

| Preliminary FCF | Interval | Low cost Price | Progress Price | Terminal Worth (P/FCF) |

| $28M | 10 Years | 10% | 3% | 5 |

These enter variables lead to an intrinsic worth of $268M, leaving a 42% upside if fuel costs get better solely partially. That equates to $8.16 per share.

Conclusion

Take into account, that each one you want is for fuel costs to get better, which is already priced in futures contracts. After administration pays down debt over the following three years, this leaves room for elevated progress capex or a better dividend. Normally, Evolution goals for little hedging, leaving an enormous upside. Every thing appears to level to an amazing funding over the following three years. Precisely how nice will rely on how chilly the following couple of winters can be and subsequent fuel costs.

[ad_2]

2024-07-16 14:55:49

Source :https://seekingalpha.com/article/4704337-evolution-petroleum-strategic-management-cheap-assets-recovering-gas-prices?source=feed_all_articles

{kind=link}

Discussion about this post