[ad_1]

FocusEye/E+ by way of Getty Photos

Pricey subscribers,

Generally you may’t assist being thrilled about a number of the drops you see available on the market. That is a kind of occasions. For those who observe my work, you already know that I’ve already established a big place (and rising) within the British firm Diageo – a distiller/vintner with a world-leading place in sure key areas.

I’ve been increasing my Diageo (NYSE:DEO) place for a variety of months at this level. I began investing after I believed the corporate to be low-cost, however Diageo has declined extra since – so I’ve added extra (clearly after checking that it’s not something elementary that’s the difficulty for the corporate).

Diageo, to me, is extra of a complete return than an earnings funding. There’s a lot concerning the firm to love. How about A-rated credit score and a 3.2%+ yield from one of many world’s main liquor producers and distributors? As a result of that is what the corporate affords.

Sure, in the course of the fiscal 2024 and going into 2025E, we’re anticipated to truly see a little bit of a decline for the enterprise. Diageo troughing is predicted to occur in the course of the fiscal – after which we’re anticipating to see a rebound again to progress.

It is a $70B market cap firm regardless of the slight tumble it’s been taking, and I’m completely happy to take a position right here. Let me present you why I’m a big-time investor in Diageo.

What there may be to love about Diageo

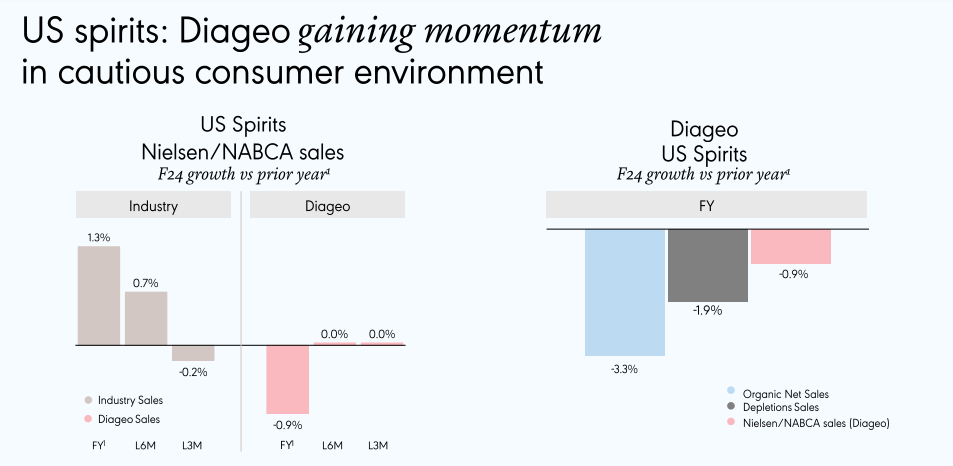

Even with the corporate seeing some stress right here, and Diageo itself calling this firm a difficult 12 months, there’s a lot to love about the best way this firm operates and what it has. First off, some annual outcomes (for the 2024 interval). Firm natural quantity was down 3.5%, natural internet gross sales had been down 60 bps, and working margin declined by round 1.3%. Nonetheless, FCF was as much as $2.6B, and the corporate delivered yet one more (anticipated) improve in its dividend.

Like different massive and diversified liquor corporations, a part of Diageo’s strengths comes from its large and various footprint. And within the final 12 months, in every single place within the firm’s operations except for the US and South America truly did effectively, with Africa rising double digits.

Corporations like Diageo are going to have “down” years. It’s the identical with any enterprise or sector – and that spirits have been struggling is obvious, since a few of my different investments within the sector, similar to Pernod Ricard, are additionally down.

Does this fear me?

No, probably not. There’s a level of cyclicality to this enterprise that does recur, and there are sufficient indicators that the corporate is definitely gaining momentum at the same time as I’m writing this text.

DEO IR (DEO IR)

Scotch, as an example, is gaining class share in 9 out of 10 of the biggest scotch markets on this planet. Tequila, for one more instance, is one other stable phase strengthened by good model constructing and really robust advertising. And Guinness is Guinness – this well-known model is seeing double-digit progress for the seventh consecutive 12 months.

So anybody saying that the corporate is in dire straits or in peril of a elementary decline, effectively, I’d say you may need been ingesting a bit an excessive amount of of the corporate’s well-known ale! I don’t imagine this to be the case. Is the corporate seeing a decline fully in step with the volatility for the remainder of the sector? Sure, it’s. Key efficiency metrics are displaying a decline throughout the board for a number of the corporations right here – however on the similar time, Diageo will not be precisely inactive. Reinvestments and constructive price management solely mildly impacted by short-term challenges are in my opinion central to the corporate’s long-term upside right here.

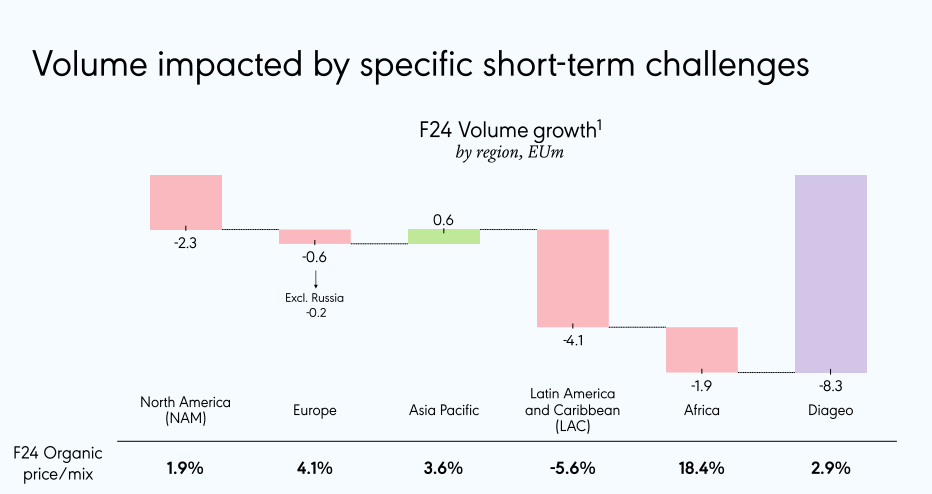

Let’s look precisely at what’s driving these destructive traits or points right here.

DEO IR (DEO IR)

As you may see, from a geographic perspective, the corporate’s quantity challenges are broad-based. However as soon as we begin delving deeper into these numbers, we are going to begin discovering that the corporate’s present technique is aimed toward serving the corporate’s strengths right here – together with the docs on worth, normal, and premium segments, that are driving gross sales. The corporate has continued confidence within the premiumization of its total portfolio. It is a firm with what I contemplate to be a large moat. Its 2024 outcomes got here as not too long ago as a month again – and so they weren’t good, however it’s necessary to view this in context.

This marks the top of an excellent progress streak the place it grew 13.5% every year over the past 3 years. When taking this into consideration, a sub-10% natural internet gross sales decline is admittedly nothing worrying and even stunning. Sure, there have been some exterior impacts, similar to client sentiment points in LATAM and the like, however the value/combine for all areas, besides LAC, was constructive, with good premiumization of Guinness above all.

The bullish arguments right here, that are these I observe and advocate, would say that the corporate has one of many strongest positions on the market. Its assist base, together with its distribution networks, makes any form of long-term downturn so long as folks drink the corporate’s merchandise unlikely. Premium distilled spirits is a so-called reasonably priced luxurious that most individuals proceed to spend on, supplied they prefer to drink the merchandise. This interprets into the potential for long-term demand, each from so-called want-to-be and already high-income prospects.

There’s additionally one thing that you actually need to know spirits to grasp. Diageo owns an enormous stock of getting old and aged spirits. It shouldn’t be doubtful that aged spirits are value greater than getting old or freshly barrelled spirits – however as issues are, these aged spirits are being held on the books at the price of getting old. This results in a ebook worth understatement that I’ve raised earlier than, and that different analysts have raised as effectively. As issues stand, I imagine the corporate’s ebook worth is value at the very least £2.5-£.3.5B extra, relying on the way you consider these – and this additional widens the valuation hole.

I began investing in different spirits corporations previous to Diageo when the downturn within the sector began. Nonetheless, because it grew to become clear that Diageo too was being pulled down, I began allocating funds right here. My place in Diageo is now at a decent 1% dimension, each non-public and industrial, and I’ve no qualms about increasing right here.

Whereas I totally admit that there are dangers to the enterprise, and we’ll undoubtedly take a look at these, it’s my view that the present valuation overstates these dangers which ends up in a constructive potential RoR – and I’ll present you what I anticipate from right here on out.

Valuation for Diageo – Optimistic, even at simply 15-17x P/E

Diageo, right here, is now buying and selling at under 17.5x P/E normalized as of the time of writing this text. It’s an A-rated spirits enterprise that sometimes warrants one thing like a 25x P/E. That is considerably influenced by the final three years of progress, so let’s normalize that to someplace alongside the strains of twenty-two.5x P/E. Something lower than that may be unfair, however greater than that might be argued to not be conservative sufficient.

The corporate is within the midst of an inarguable decline right now, and it’s additionally a transparent expectation that this decline will go on into the subsequent fiscal. That is additionally the expectation for different spirits companies, not simply Diageo.

Nonetheless, at this valuation it’s a probable improvement that we’ll see a 15% annualized RoR even at only a 22.4x P/E – and for this reason I’m so constructive on Diageo at under $125/share for the NYSE ticker (although I spend money on the native).

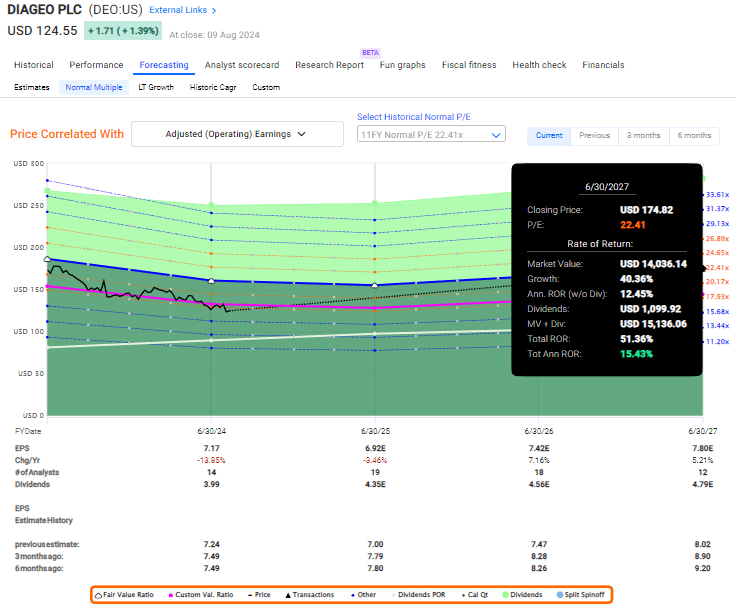

F.A.S.T Graphs Diageo Upside (F.A.S.T Graphs Diageo Upside)

As you may see, Diageo is an organization right here the place you on the premise of A-credit with a yield of over 3.2% can get a 15% annualized RoR for the subsequent 2–3 years even within the case of what I contemplate to be a conservative efficiency or goal.

And that is what I sometimes search for. My different “decide” this week was Realty Revenue. Realty Revenue, whereas having recovered markedly, can be nonetheless enticing on a conservative foundation (albeit not as enticing because it as soon as was). I attempt, relating to most of my portfolio, to keep away from getting “fancy”. I simply search for that 15% annualized, and I’m going from there.

Just a few causes for it, however most of them need to do with 15% being sufficient for me at this stage, with the truth that extreme RoR sometimes implies extreme danger, and that I’m actually involved in capital preservation above extreme capital appreciation, supplied I get my “cash” whereas I’m ready.

This strategy has served me effectively for the previous 10 years, and I’ll proceed to make use of it.

Even with the chance of continued declines included, I imagine that Diageo’s share value right now marks a gorgeous potential and a gorgeous entry level to this nice enterprise.

Some dangers exist – and here’s what I believe they’re.

Dangers to Diageo – Cyclicality and traits

I’ve famous over the previous few years as I invested in Spirits that the spirits enterprise tends in direction of increased levels of volatility than merchandise like beer. That is very true the extra premium you go – and that is the place Diageo is at “house”. It signifies that throughout a worldwide slowdown of the economic system, which is what we presently have, Diageo would possibly damage greater than others due to how its merchandise and segments are positioned. That is, what I imagine that we’re seeing proper now.

As with Pernod and different related companies, Diageo can be uncovered to vital regulatory and political dangers. Russia’s and Chinese language strikes to try to curb alcohol consumption are solely the most recent of those. It must be stated clearly nevertheless that governments have been attempting to do that for hundreds of years with out success and I don’t imagine it to achieve success right here both.

As a result of Diageo is such a mature enterprise, the potential for natural progress is low. The corporate’s progress, as evidenced by the previous few years, is generally inorganic right here. M&A progress comes with the chance of overpaying, and that is very true for Diageo which is attempting to maneuver deeper into premium spirits and the like.

These are the primary dangers to a constructive thesis for Diageo right now – none of which, I imagine, are vital sufficient to offset the potential for funding.

Thus, I say the corporate is a “BUY” right here.

Thesis

-

This is likely one of the most high quality beverage companies on the planet, and it sometimes trades above 25X. The present firm value for the native ticker DGE on the LSE implies a P/E of 17.6x, which is the bottom it has been in a while and has pushed the yield to virtually 3.3%.

-

Due to that, and due to the market, I imagine it’s time to shift my stance on DEO, which is what I’m doing right here.

-

I contemplate DEO a “BUY”, and the upside to that purchase is at the very least 15+% annualized to a normalized 22-25x P/E, which I contemplate legitimate for the biggest spirit and beer play in these classes.

-

I give Diageo a local PT of at the very least £38/share and an ADR PT of $180/share.

Keep in mind, I am all about:

-

Shopping for undervalued – even when that undervaluation is slight and never mind-numbingly large – corporations at a reduction, permitting them to normalize over time and harvesting capital positive aspects and dividends within the meantime.

-

If the corporate goes effectively past normalization and goes into overvaluation, I harvest positive aspects and rotate my place into different undervalued shares, repeating #1.

-

If the corporate does not go into overvaluation however hovers inside a good worth, or goes again all the way down to undervaluation, I purchase extra as time permits.

-

I reinvest proceeds from dividends, financial savings from work, or different money inflows as laid out in #1.

The corporate additionally fulfills a number of of my funding standards.

-

This firm is total qualitative.

-

This firm is basically protected/conservative & well-run.

-

This firm pays a well-covered dividend.

-

This firm is presently low-cost.

- This firm has a sensible upside based mostly on earnings progress or a number of enlargement/reversion.

Which means that the corporate fulfills all of my standards, and I contemplate it a “BUY”.

[ad_2]

2024-09-02 15:30:30

Source :https://seekingalpha.com/article/4718537-diageo-fundamentally-conservative-with-a-well-covered-dividend?source=feed_all_articles

{kind=link}

Discussion about this post