[ad_1]

Esa Hiltula

The targets of revenue investing might be cut up into two broad classes: 1) to fund residing bills and retirement with the portfolio distributions with out tapping into the principal itself, and a pair of) to pocket present revenue that might be reinvested again in yield-bearing property, thereby facilitating the so-called “snowball” impact.

In apply, it could be in order that throughout the pre-retirement interval, traders apply the second strategy after which as soon as the retirement kicks in, the portfolio proceeds are taken out to cowl day by day wants. This apply is related in my case as properly.

It clearly is dependent upon every investor’s danger tolerance and urge for food for danger, however I don’t assume it might be improper to say that the next components kind a structural foundation on how the technique is devised by such traders:

- Discovering securities that provide yields which might be enticing on an absolute foundation and are undoubtedly above what the growth-oriented indices present.

- Protecting the possibilities of distribution cuts as little as attainable.

- Capturing a further layer of returns, largely within the type of periodic dividend hikes.

Successfully, it boils right down to a pure play purchase and maintain course of, the place a big quantity of due diligence is finished earlier than investing to essentially make it possible for the snowball will regularly change into bigger as time progresses.

My private purpose is to seek out strong revenue compounders, add them to a portfolio and promote provided that there’s a elementary change within the enterprise (e.g., firm decides to enterprise into dangerous segments to accommodate progress on the expense of sound steadiness sheet). What this implies is that I’m truly not that eager on experiencing share worth run-ups, because it simply makes the dividend reinvestment course of much less enticing due to the diminished yield stage. As an alternative, crucial factor is to have revenue streams which might be predictable, immune to completely different form of financial uncertainties and, in fact, enticing sufficient with out the presence of speculative situations.

Within the article beneath, I’ll elaborate on two layers which might be important for accommodating such de-risked revenue snowball technique.

Getting the slope and dimension proper

One of many first questions that the traders must ask themselves is whether or not to place a heavier emphasis on progress or yield. The underlying query is whether or not it’s price taking a decrease yield initially to in the end entry a bigger revenue portfolio that might be supported by a robust dividend progress profile.

Theoretically, the longer the time horizon, the heavier the bias needs to be put in direction of growth-oriented shares. It’s attainable to seek out blue-chip corporations that present constant dividends with very enticing revenue progress dynamics. Not surprisingly, nonetheless, these yields are mechanically decrease than what might be discovered within the larger yield house. Probably the greatest proxies for this particular class is Schwab U.S. Dividend Fairness ETF (NYSEARCA:SCHD), which incorporates 103 completely different large-cap dividend progress targeted shares.

With that being mentioned, my desire goes to larger yielding options (whilst an investor, who has greater than 20 years till retirement). Let me clarify.

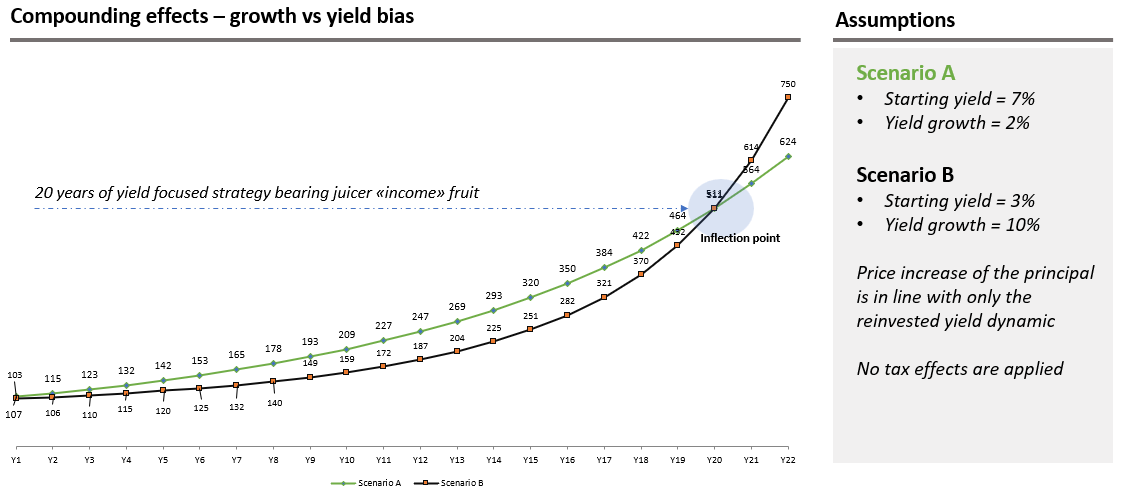

First, let’s check out two hypothetical eventualities, which I’ve tried to depict in (hopefully) comprehensible style beneath. The state of affairs A assumes beginning yield of seven% and revenue progress of two%, whereas state of affairs B is predicated on beginning yield of three% and dividend progress of 10%. In my humble opinion, these are fully lifelike assumptions for de-risked revenue methods given the prevailing rate of interest backdrop.

Created by creator

What this chart reveals is that by sticking to state of affairs B, it might take ~ 20 years for revenue progress traders to meet up with those who’ve determined to put money into larger yielding, however slower progress securities. Granted, if we took a extra notable worth appreciation element into consideration, we may possible anticipate a greater complete return end result for the expansion state of affairs. But, in that case, we must also acknowledge a unfavorable impact on the yields as every greenback reinvested could be topic to the next asset worth, making the reinvestment yield decrease accordingly.

Second, every time an funding resolution is predicated on some return assumptions that stretch far into the long run, the general danger profile will get mechanically larger. Right here, I’m fairly skeptical about corporations that might have the ability to ship double-digit or near that dividend progress statistics for many years in a row. The bigger the corporate will get, the harder it’s to maintain the expansion charge as often the market shares change into exhausted, the pricing energy diminishes and merchandise / companies are likely to finally be substituted with different revolutionary gadgets. Now, I’m not saying that rising dividends at 10% for 10 or 20+ years isn’t attainable. It’s simply that the percentages should not that top.

Third, often after we speak about attractively yielding names which might be underpinned by sturdy money flows, the sectors that pop up are typically system-critical for which there’ll (extremely possible) be all the time a requirement for. For instance, it’s tough to think about a scenario, the place actual property will now not be obligatory (consider properly yielding fairness REITs). Equally, the possibilities are very low that midstream infrastructure will disappear from the financial exercise within the subsequent 20 or 30 years (consider MLPs). Moreover, if we consider state of affairs A, attaining 2% progress charge every year is admittedly not that tough or speculative. In lots of cases, these high-yielding shares have their money flows linked to long-term contracts that carry an embedded element of periodic money movement bumps, that are at or carefully reflective of CPI.

Lastly, given the time wanted for revenue progress targeted technique to surpass the capital generated by larger yielding methods in addition to the underlying dangers concerned across the progress corporations truly delivering of excessive progress charge targets for a protracted time frame, I discover it extra helpful to deal with juicy dividend yields which might be topic to conservative progress ranges.

In different phrases, for me, it boils right down to beginning with a bigger snowball and rolling it ahead on a not that steep scope to keep away from dangers.

Making the snowball resilient

Within the means of attaining that attractive compound-effect of revenue investing, it’s crucial to deal with the dangers earlier than letting the snowball down the hill.

I’ll describe a few elementary components that clearly de-risk this course of, lowering the possibilities of revenue loss.

The essence right here is properly captured by Warren Buffett’s well-known quote:

If we keep away from the losers, the winners will deal with themselves.

Technique – when choosing high-yield names, we’ve to know that there are usually three explanation why a specific safety gives juicy revenue ranges. The primary one might be attributable to a monetary misery, the place the money movement prospects are unclear. The second might be associated to a scenario through which the enterprise itself is speculative and depending on, say, risky commodity costs or macro-sensitive demand dynamics. And the third one might be related to “boring enterprise mannequin”, the place the expansion trajectory doesn’t look that enticing. When attempting to entry sustainable yields, the third class is the place we wish to be. The most typical examples of this embody actual property, midstream property, public infrastructure, regulated utilities and different sectors or corporations which might be well-established, however lack that profitable progress story.

Steadiness sheet – in lots of circumstances, the place the dividends have been reduce, it was the dearth of a sturdy steadiness sheet that didn’t present the mandatory safety. In reality, the notion of a weak steadiness sheet, virtually per definition, implies an elevated debt profile, which consists of aggressive borrowings that create a strain on money flows (i.e., via principal and curiosity value service parts). Having an funding grade steadiness sheet doesn’t solely assist mitigate the monetary danger, however it additionally performs an important function for a lot of “boring” companies in making the expansion occur. For example, for REITs possessing a fortress steadiness sheet permits to cut back the price of capital, which in flip warrants a extra enticing unfold seize when shopping for properties. The decrease the price of capital, the upper the unfold potential (or alternatively, buying top quality / low cap charge properties can change into accretive to the enterprise).

Dividend protection – because the outlined technique is based on excessive and sustainable revenue, it is vitally necessary to keep up ample headroom on the dividend protection finish. Conservative money movement payout ratio helps corporations that wish to distribute uninterrupted revenue streams protect their companies from counting on debt in case or inside money reserves to fund the distributions in case of non permanent monetary shocks. One other crucial component on why it’s essential to have some undistributed portion of money technology is to accommodate progress with out reliance on solely debt associated capital. This fashion, a very sustainable progress might be achieved.

The underside line

To realize enticing compounding results from an revenue investing technique, traders must first perceive steadiness high-yield and low progress with mediocre yield and high-growth securities. There are execs and cons for each of them. The important thing argument in opposition to the high-yield strategy is that the worth appreciation potential is inherently decrease and sooner or later far sooner or later, revenue growth-based strategy may begin delivering outsized distributions. But, in my view, the notion of company registering double-digit revenue progress figures for many years in a row is simply too speculative and unsure. Plus, if the revenue return is the one funding goal, it might take simply an excessive amount of time for the dividend progress technique to catch up.

Lastly, regardless of what technique is devised, ensuring that the snowball is as resilient as attainable is equally necessary for each eventualities. Right here beneath I’m highlighting three particular securities, which, in my view, tick the entire obligatory packing containers from the chance perspective and on the identical time supply yields which might be 7% or above.

- EPR Properties (NYSE:EPR), dividend yield of seven.2% – see my article right here.

- MPLX LP (NYSE:MPLX), dividend yield of seven.9% – see my article right here.

- Enterprise Merchandise Companions (NYSE:EPD), dividend yield of seven.1% – see my article right here.

[ad_2]

2024-08-26 05:59:23

Source :https://seekingalpha.com/article/4717012-delayering-the-dividend-snowball-for-long-term-income-investors?source=feed_all_articles

{kind=link}

Discussion about this post