[ad_1]

Sundry Images

What Occurred Because the IT Outrage

CrowdStrike Holdings, Inc. (NASDAQ:CRWD) beat on each income and non-GAAP EPS estimates in Q2 FY2025, however forecasted a disappointing outlook. Though the corporate managed the disaster successfully, CRWD’s high precedence is now to strengthen buyer engagement. I imagine some clients could hesitate to resume the Platform merchandise within the close to time period, resulting in a decrease internet income retention charge and impacting top-line development. To protect goodwill, CRWD has made concessions, equivalent to providing reductions to sure clients, which might end in a major slowdown in ARR development in coming quarters.

Following the outage, I beforehand issued a maintain ranking on the inventory because of the appreciable uncertainty surrounding the corporate’s development trajectory, as rebuilding its repute will take time. The inventory has recovered some losses from its August lows, indicating its valuation multiples getting extra elevated.

Subsequently, on account of a disappointing ahead income and EPS steerage, I am reiterating my maintain ranking on CRWD, anticipating a major development slowdown within the coming quarters as it really works to rebuild buyer loyalty. Furthermore, I am cautiously optimistic in regards to the firm’s long-term chief within the core Endpoint market, as CRWD is prone to face growing competitors and potential market share loss following this incident.

Providing Concessions Will Impression Close to-Time period Development

The corporate mannequin

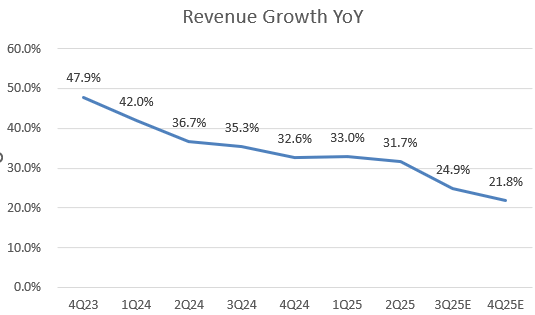

CRWD delivered better-than-expected 2Q outcomes, with income development nonetheless displaying resiliency at 31.7% YoY. Because the outage occurred in July, I anticipate the monetary influence to start materializing in 3Q FY2025, because the administration talked about that this coming quarter will embody an estimated $30 million extra value from the concession bundle. Significantly, the midpoint of the corporate’s 3Q FY2025 and FY2025 steerage falls under market estimates, implying a YoY development of 24.9% in 3Q and 21.8% in 4Q. The chart clearly reveals that the expansion trajectory is beginning to decelerate considerably in 3Q.

The corporate mannequin

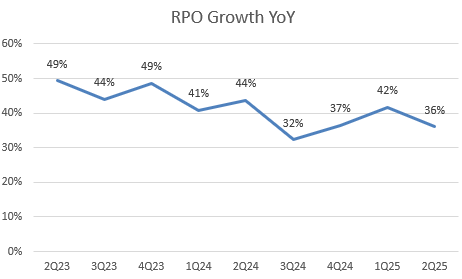

Furthermore, the corporate’s key metrics, equivalent to RPO, dollar-based internet retention, and ARR is not going to absolutely replicate the destructive influence of the latest outrage. Nevertheless, we did observe some modest slowdown in 2Q, as its RPO grew 36% YoY, displaying a sequential slowdown. The administration indicated that the dollar-based churn was modestly decrease on a YoY foundation. ARR development additionally skilled a 1% sequential decline.

In the course of the 2Q FY2025 earnings name, the administration mentioned their buyer dedication bundle to strengthen the shopper retention and improve Falcon adoption. The concessions bundle will influence internet new ARR and subscription income by round $60 million {and professional} service income by $5 million to $10 million in 2H FY2025. Subsequently, I imagine these key metrics are anticipated to see a major deceleration in 3Q.

Nevertheless, the administration is assured that this bundle will improve buyer engagement, which is able to ultimately create a better platform adoption. I imagine it is too early to verify this narrative given growing competitors within the cybersecurity trade, as we’re seeing CRWD dropping market share following the incident.

Anticipating A Sharp Margin Decline

The corporate mannequin

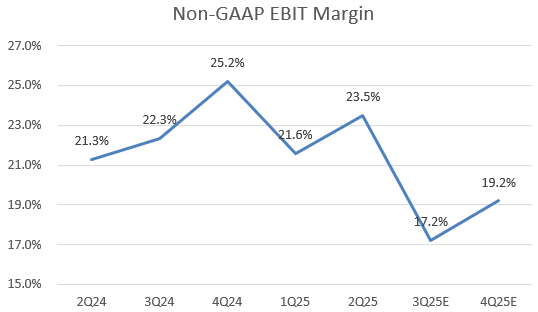

CRWD can be anticipated to expertise a contraction in non-GAAP EBIT margin in 2H FY2025, as the corporate will incur extra G&A bills following the outage. With a major slowdown in income development coinciding with a margin decline, the corporate has indicated a YoY decline in its non-GAAP EPS for 3Q. The midpoint of FY2025 steerage suggests a continued YoY decline in non-GAAP EPS in 4Q as nicely. I imagine the road will doubtless revise its ahead EPS consensus downward following this muted outlook. It is potential that the ahead 12-month EPS shall be decrease than its TTM foundation, which might make the ahead valuation a number of seem pricier.

Nonetheless, as the corporate continues to put money into R&D to assist development whereas specializing in buyer retention, administration anticipates a gradual enchancment in EBIT margin in FY2026.

Gaining Market Shares from Different Cyber Gamers

Regardless of CRWD’s main place within the Endpoint Safety market, some analysts on the road imagine that the corporate could face incremental market share loss within the close to time period, notably to cybersecurity friends like SentinelOne (S) and Palo Alto Networks (PANW). Though these firms at present maintain a smaller share of the market, they’ve been steadily gaining floor lately. Significantly, SentinelOne is predicted to seize extra bookings at CRWD’s expense. A latest survey indicated that SentinelOne’s outcomes elevated by 29% each sequentially and year-over-year, partly because of the firm providing reductions to clients.

Earlier this week, SentinelOne delivered better-than-expected Q2 earnings and raised its ahead income outlook. I imagine that after an organization’s repute is broken, it could take a very long time to totally get better. As opponents could catch up and achieve market share, we have to hear the administration’s feedback on the FY2026 outlook early subsequent yr to realize extra shade into the restoration course of, notably regarding internet new ARR development. Subsequently, it is untimely to be bullish on the inventory at the moment, particularly given its nonetheless elevated valuation.

Valuation

In search of Alpha

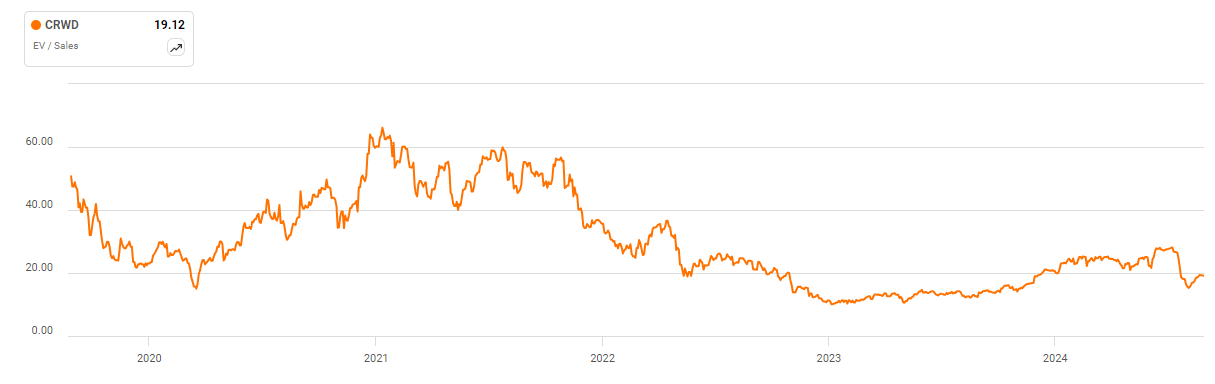

CRWD’s valuation was costly earlier than the outrage however was supported by its robust development momentum, with a +30% YoY income development development. Following the latest sharp pullback, I imagine that some near-term development headwinds have been priced in. Its EV/gross sales TTM is at present buying and selling at 19.1x, regardless of under its 5-year common, nonetheless greater than PANW and S. As well as, its non-GAAP P/E fwd sits at 69x, dearer than Nvidia’s (NVDA) 46x and PANW’s 55x. This means a lofty valuation and additional draw back potential for CRWD. Nevertheless, administration inspired traders to look previous the near-term development slowdown. They acknowledged that the “buyer dedication bundle will drive much more Falcon utilization and platform worth realization in each the brief and long run.” Subsequently, it is prudent to remain on the sidelines in the intervening time.

Conclusion

In conclusion, though CRWD delivered better-than-expected Q2 outcomes, this doesn’t mitigate the numerous near-term challenges posed by the latest IT outage. The disappointing ahead steerage has raised issues about potential slowdowns in key development metrics equivalent to ARR and RPO. Furthermore, the corporate could face intensified competitors and potential market share loss as rivals like S and PANW capitalize on the scenario and increase their ahead steerage for the upcoming quarters.

Given the chance of downward revisions to EPS estimates and CrowdStrike Holdings, Inc.’s nonetheless elevated valuation multiples, it is untimely to purchase the dip. We have to hear an optimistic administration’s commentary on the FY2026 outlook, notably relating to internet new ARR development, earlier than contemplating a extra bullish view on CRWD.

[ad_2]

2024-08-29 22:18:22

Source :https://seekingalpha.com/article/4718027-crowdstrike-customer-commitment-package-is-a-double-edged-sword?source=feed_all_articles

{kind=link}

Discussion about this post