[ad_1]

M. Suhail

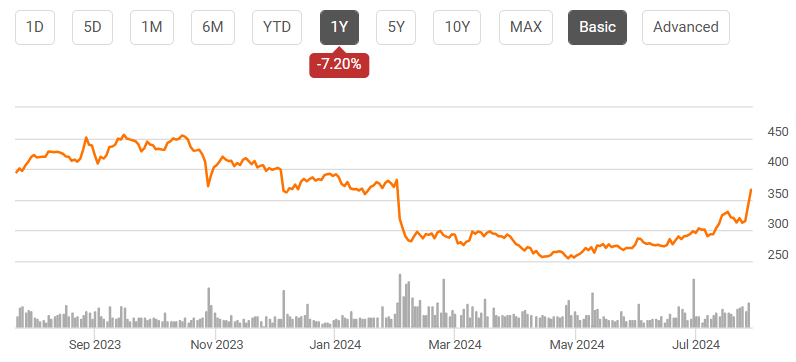

Shares of Constitution Communications (NASDAQ:CHTR) have been a poor performer over the previous yr, dropping 7%. Nonetheless, Friday was a much-needed jolt with shares surging 16% after reporting strong Q2 earnings. Again in April, I upgraded shares of Constitution to a “maintain” from a “promote,” having fallen 31% since that promote suggestion. Whereas I used to be proper to improve shares, the “maintain” has confirmed too cautious after their post-earnings rally. With shares up 37% and new financials, now is an effective time to revisit Constitution. I’m inspired by money stream tendencies, however this enchancment is mirrored within the latest rally, leading to me sustaining a maintain score.

In search of Alpha

Within the firm’s second quarter, Constitution earned $8.49, beating consensus by $0.59 as income rose by 0.3% to $13.7 billion. Total, the corporate continues to see related working tendencies as in latest quarters, particularly customers chopping the twine for video service whereas its smaller cell unit sees dramatic progress. Nonetheless, its decrease cap-ex steering was the foremost spotlight. Capital spending and decrease free money stream have been my main source of concern, and this quarter went a major approach to addressing it. Due to decrease cap-ex, I now count on about $2.5 billion of 2024 free money stream.

enterprise outcomes, residential income fell by 0.6% to $10.8 billion whereas industrial rose by 2.1% to $1.8 billion and promoting jumped 3.3% due to political spending. Constitution’s native information channels profit from increased political spending throughout Presidential Election years, which additionally see many Home and Senate races. In reality, political spending boosted advert income by 5.5%. In any other case, advert spending was down about 2%, according to the tighter budgets from nationwide accounts that we’ve heard about from many ad-selling corporations.

Constitution continues to face headwinds from clients chopping the twine, a stress it’s making an attempt to offset with worth improve and tight value self-discipline. Certainly, residential relationships fell by 1.3% to 29.6 million. Partially offsetting this, residential income per buyer rose by 0.4% to $120.77. The industrial aspect has confirmed to be extra resilient, with small and medium dimension enterprise (“SMB”) relationships rising by 0.2% to 2.2 million due to progress in web and cell.

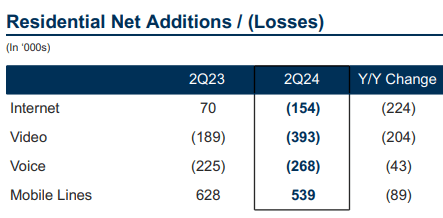

As you possibly can see under, its shopper enterprise continues to face sustained buyer attrition. In its three core merchandise, losses had been worse than final yr with video primarily doubling to just about 400k misplaced clients. In idea, web ought to show to be extra resilient as you want web entry to stream Netflix (NFLX) and different streaming providers. Nonetheless, even right here, outcomes had been disappointing.

Constitution

One problem for the corporate has been that the housing market has been fairly subdued. When customers transfer, that may be a key alternative to win a brand new buyer, however with dwelling gross sales so muted, that avenue of progress is proscribed. Whereas cell progress slowed, its buyer rely is up 33% from final yr. Cellular income was up 37%. This was a major inflection level. CHTR has aggressively added cell clients via outsized promotions, which have meant buyer progress exceeded income progress. Now as promotions roll off, we’re seeing cell revenues flex increased. In that context, I’m snug with slower line progress.

That mentioned, it is very important reiterate cell continues to be a small piece of the enterprise. In shopper, web income rose by 1.3% to $5.8 billion, whereas video fell by 7.7% to $3.9 billion. Cellular income rose by 37%, however that’s lower than $200 million of profit, primarily simply offsetting the misplaced video income. Now, as a result of it has fewer clients, video programming prices fell by 9.8% to $268 million. Thanks to cost improve, video income is outperforming programming prices by 210bps. It is a enterprise clearly in decline, however Constitution is managing via it.

42.9% of shoppers are non-video, up 4% from final yr. In consequence, three or extra product penetration fell by 170bps to 19.2%, resulting in a 20bp rise in 2 product penetration and additional rise in 1 product penetration. Nonetheless, adjusted EBITDA of $5.7 billion was up 2.6% from final yr as margins expanded by 100bps to 41.4%.

There are a number of objects happening right here. First due to excessive programming prices, video could be a decrease margin enterprise, so the combination shift away from video is boosting margins. Moreover, worth will increase are, for now, offsetting buyer losses. Lastly, it’s managing bills pretty properly. Service prices fell by $88 million resulting from decrease labor and unhealthy debt expense. Gross sales and advertising rose by a reasonably modest 1.9%, or $17 million. It is a enterprise with minimal, if any, underlying progress, given secular shifts in shopper tastes, however it’s managing this decline moderately.

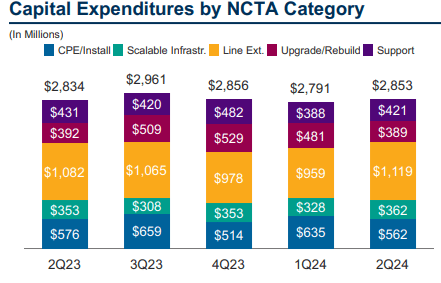

I used to be extra inspired by revised capital plans. Given its lackluster progress prospects, its cap-ex finances appeared too massive, weighing on potential free money stream and limiting potential buybacks In Q2, Constitution did $2.9 billion of cap-ex. There was a $37 million improve in line-extension spending in sponsored rural development; in any other case, cap-ex was down $18 million from final yr. Q2 spending was modestly under expectations.

Constitution

Much more importantly, full yr capital spending is now forecast to be round $12 billion, down $300 million from its prior estimate, although it nonetheless implies a ramp throughout H2 relative to H1. Given the weak buyer net-addition surroundings, administration has been in a position to scale back capital plans. It is a clear constructive, because the return on that spending was doubtful in my opinion, given the secular headwinds Constitution faces. Cap-ex needs to be peaking over the subsequent twelve months after which step by step migrate down towards $11 billion in 2026, or maybe decrease now.

That’s vital as a result of CHTR wants free money stream to handle its debt and return capital to shareholders. Within the second quarter, CHTR generated $1.3 billion in free money stream, which included $471 million of working capital advantages. For the yr, it now sees working capital being a slight tailwind. With this free money stream, we noticed a reasonable quantity of share repurchases, about $400 million. Due to its buyback program, there was 4.6% share rely discount over the previous yr.

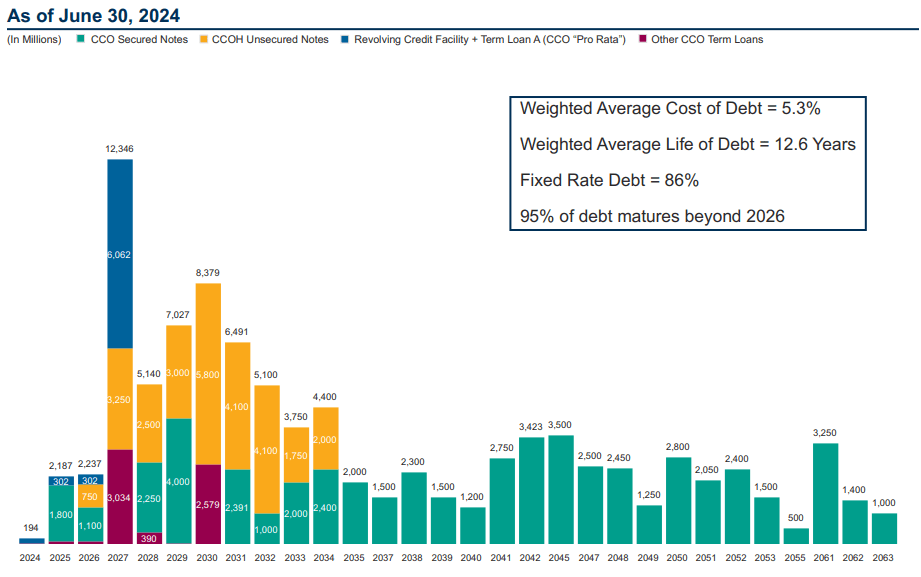

Equally necessary, CHTR did $370 million of debt discount within the quarter. Nonetheless given refinancing, curiosity expense rose by $30 million to $1.33 billion. The corporate has 4.3x debt/EBITDA, the midpoint of its 4-4.5x goal. It has $96.5 billion of debt with restricted near-term maturities. As such, rate of interest danger needs to be manageable.

Constitution

Professional forma for share-based compensation, I now count on Constitution to generate $2.4-$2.6 billion of free money stream this yr with 2025 free money stream prone to be related. That’s about $18/share. That provides shares a few 4.9% free money stream yield, which is able to allow vital share-count discount. By 2026, I’d count on nearer to $3.4 billion in free money stream, or about $24 a share.

In the end, I view honest worth as a ~6% long-term free money stream yield, as buyer progress of about 0% and worth progress of about 2% helps ~2% natural money stream progress, which mixed with a 6% beginning yield ought to allow 8% returns. With my 2026 free money stream estimate, I see shares reaching $400 by the top of 2025, a few 9% return over the subsequent 12-16 months.

I view this as according to a “maintain” score as shares have upside however lower than my 10% annual return goal for a “purchase” score. After Friday’s rally, Constitution seems to be pricing in a lot of the improved information. As such, I stay a maintain. If we see shares transfer nearer to $400, I’d be inclined to take earnings. Equally, if shares had been to tug again to about $350, I’d be a purchaser.

[ad_2]

2024-07-29 14:30:38

Source :https://seekingalpha.com/article/4707666-charter-communications-improved-cash-flow-outlook-largely-reflected-in-valuation?source=feed_all_articles

{kind=link}

Discussion about this post