[ad_1]

VV Photographs

Introduction

Citigroup (NYSE:C) is likely one of the largest banks on the earth, and referred to as a “too massive to fail” financial institution. I’ve coated Citigroup through the years, however most just lately, I wrote in regards to the financial institution’s 9.5% yielding most popular shares again in October. Since then, the popular shares have been known as and the financial institution’s frequent shares have rallied by greater than 50%. Regardless of the rally, I consider that traders ought to think about taking an extended place in Citigroup.

Citigroup Monetary Outcomes

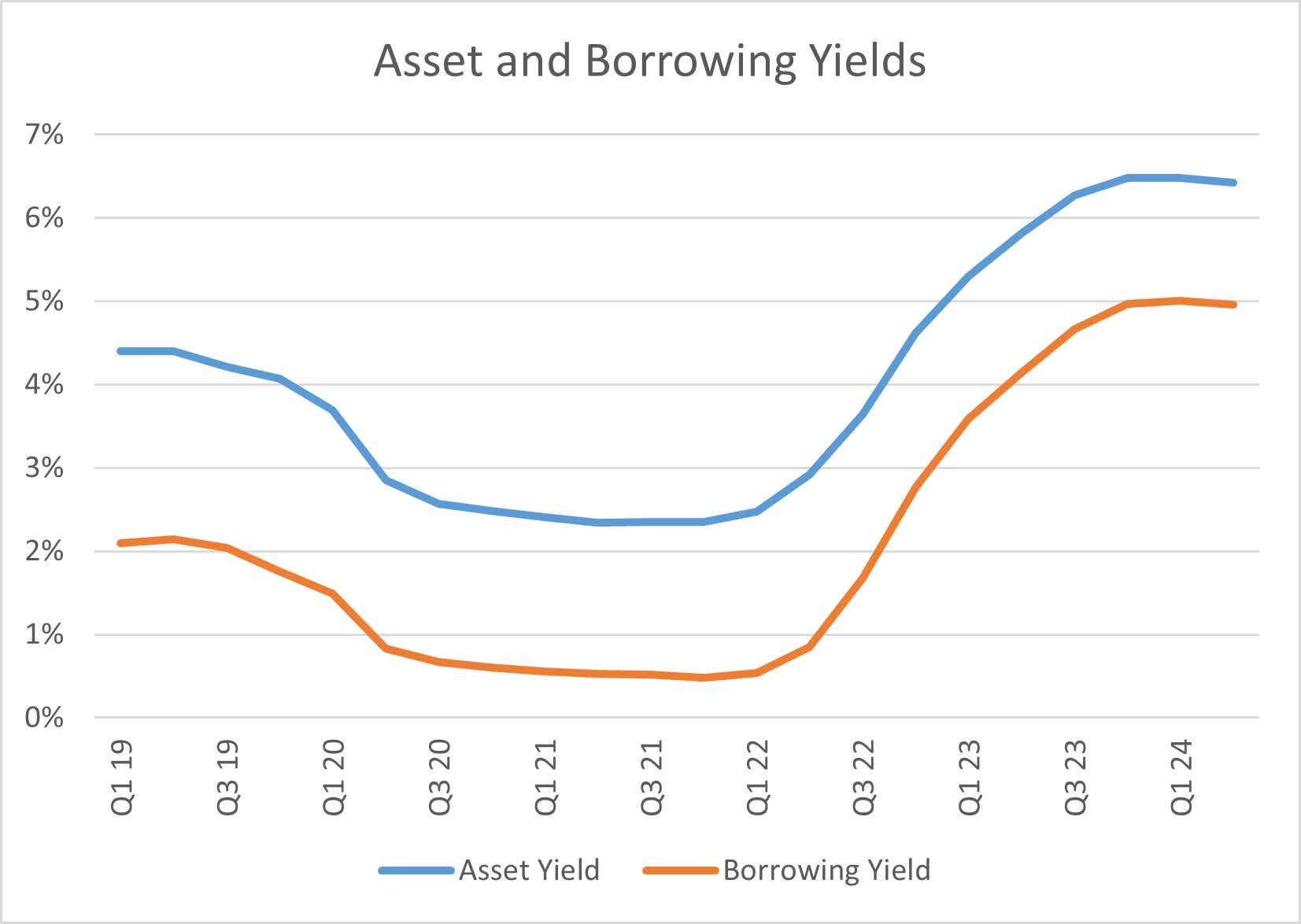

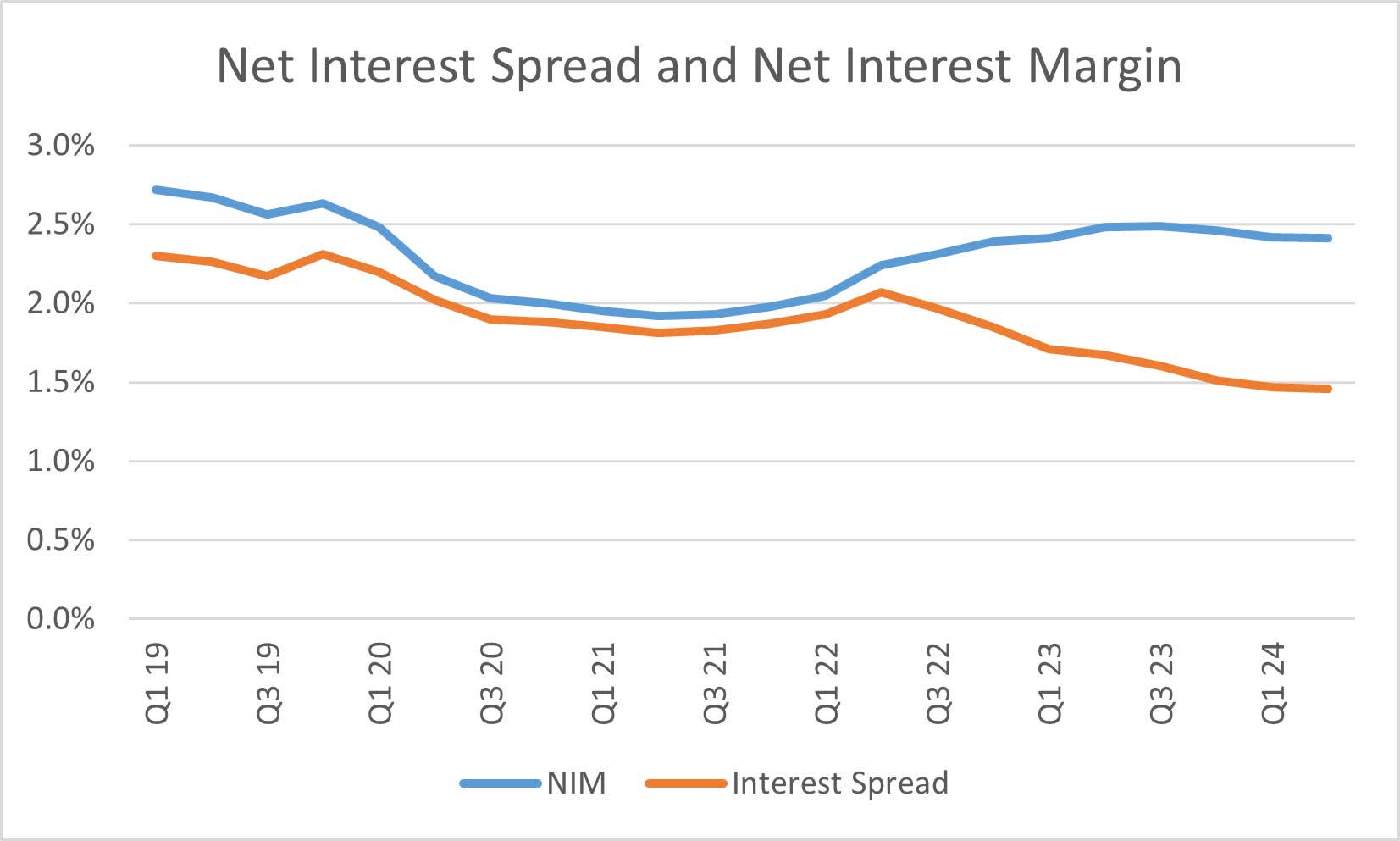

Like every other financial institution, Citigroup shouldn’t be exempt from the adjustments in rates of interest. In the course of the pandemic, unprecedented easing drove the financial institution’s borrowing yields right down to round 0.5% whereas asset yields have been under 2.5%. Because the Federal Reserve aggressively elevated rates of interest to struggle inflation, the financial institution noticed its asset yields climb to over 6%, however its borrowing yields additionally grew to over 5%. Regardless of the web curiosity unfold (asset yield much less borrowing yield) falling to underneath 1.5%, the financial institution has managed to scale back leverage and preserve its web curiosity margin above pandemic period ranges.

Firm Financials

Firm Financials

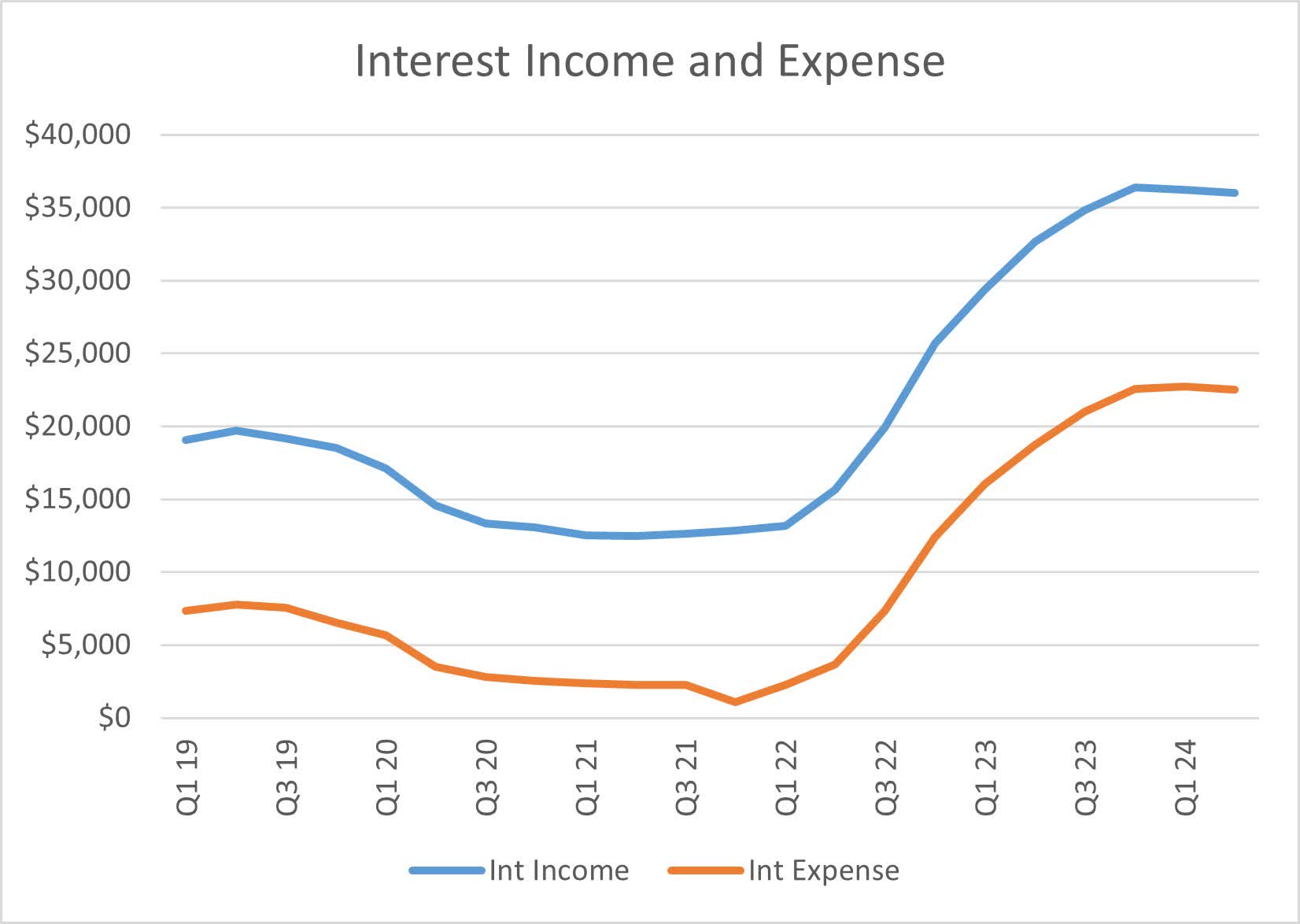

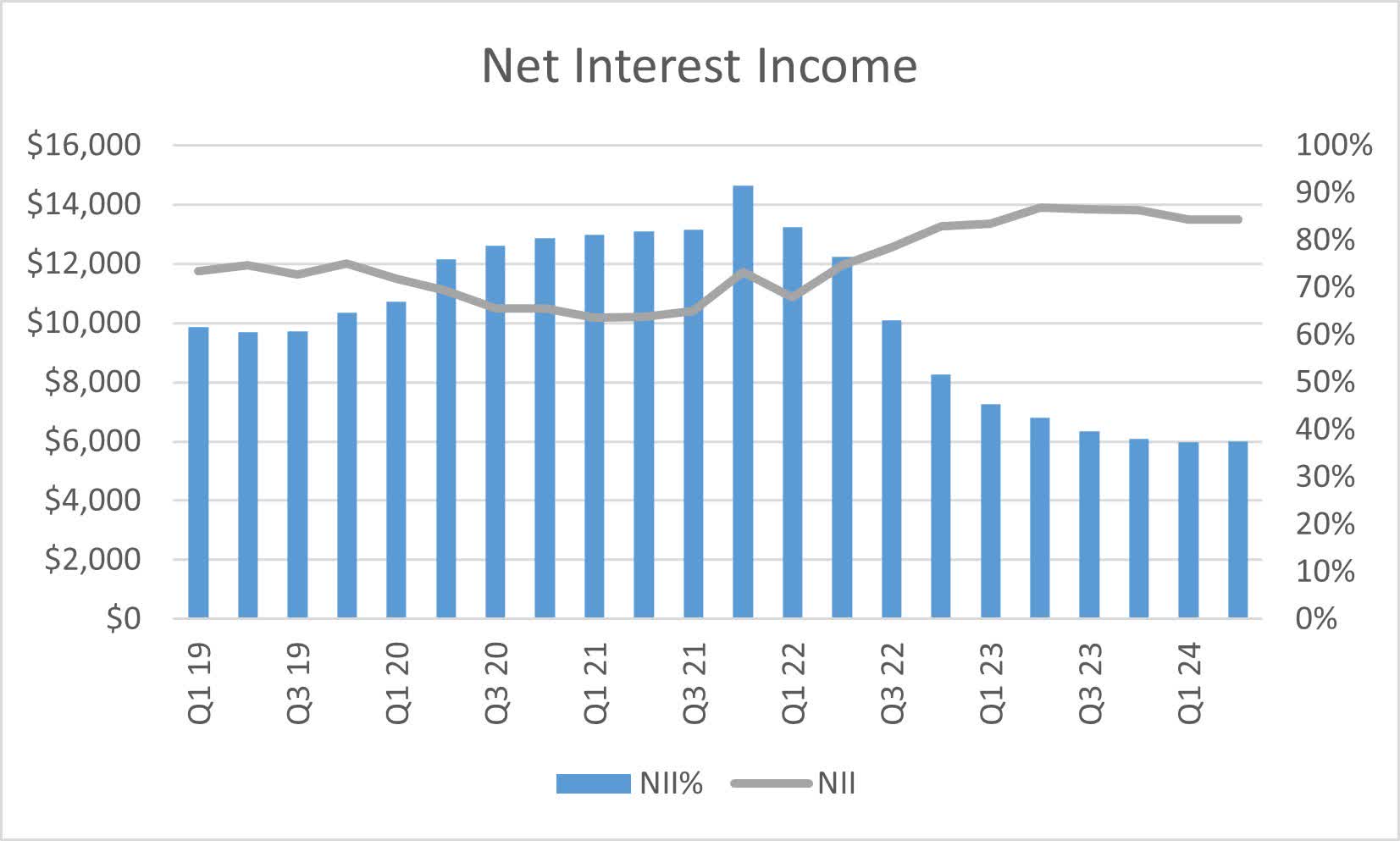

With respect to earnings, Citigroup noticed its curiosity earnings and curiosity expense pattern with asset and borrowing yields during the last 5 years, though every fell barely within the second quarter. Regardless of the headwinds of upper rates of interest, web curiosity earnings (curiosity earnings much less curiosity expense) stays properly above pandemic and pre-pandemic ranges and solely barely off the highs achieved late final 12 months.

Firm Financials

Firm Financials

Loans and Deposits

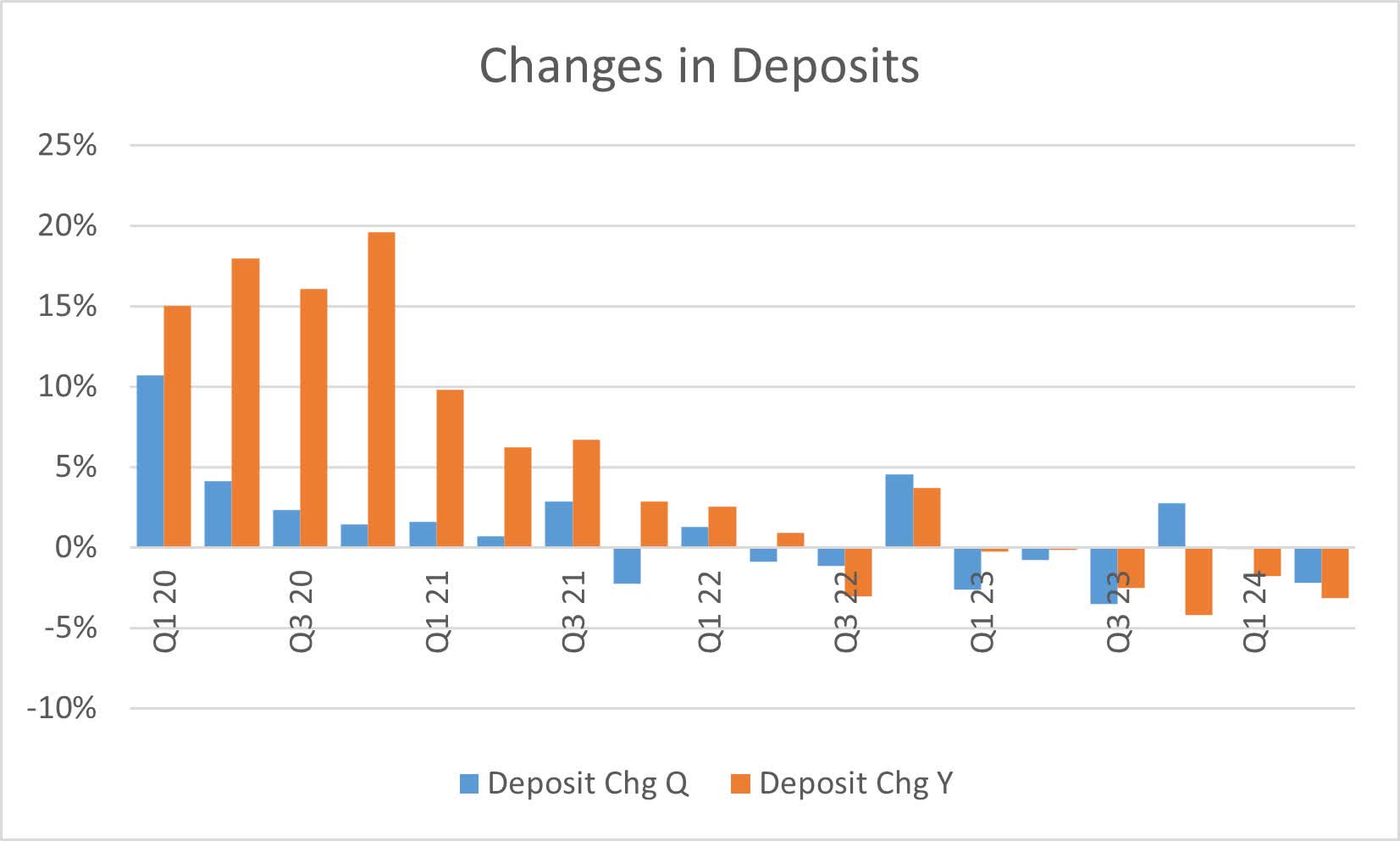

When the regional banking disaster hit final March, media shops reported that deposits have been fleeing regional banks and ending up in “too massive to fail” banks. The one drawback with that principle is that it wasn’t true, particularly for Citigroup. The financial institution has seen deposits decline on a year-over-year foundation for six consecutive and 7 out of the final eight quarters.

Firm Financials

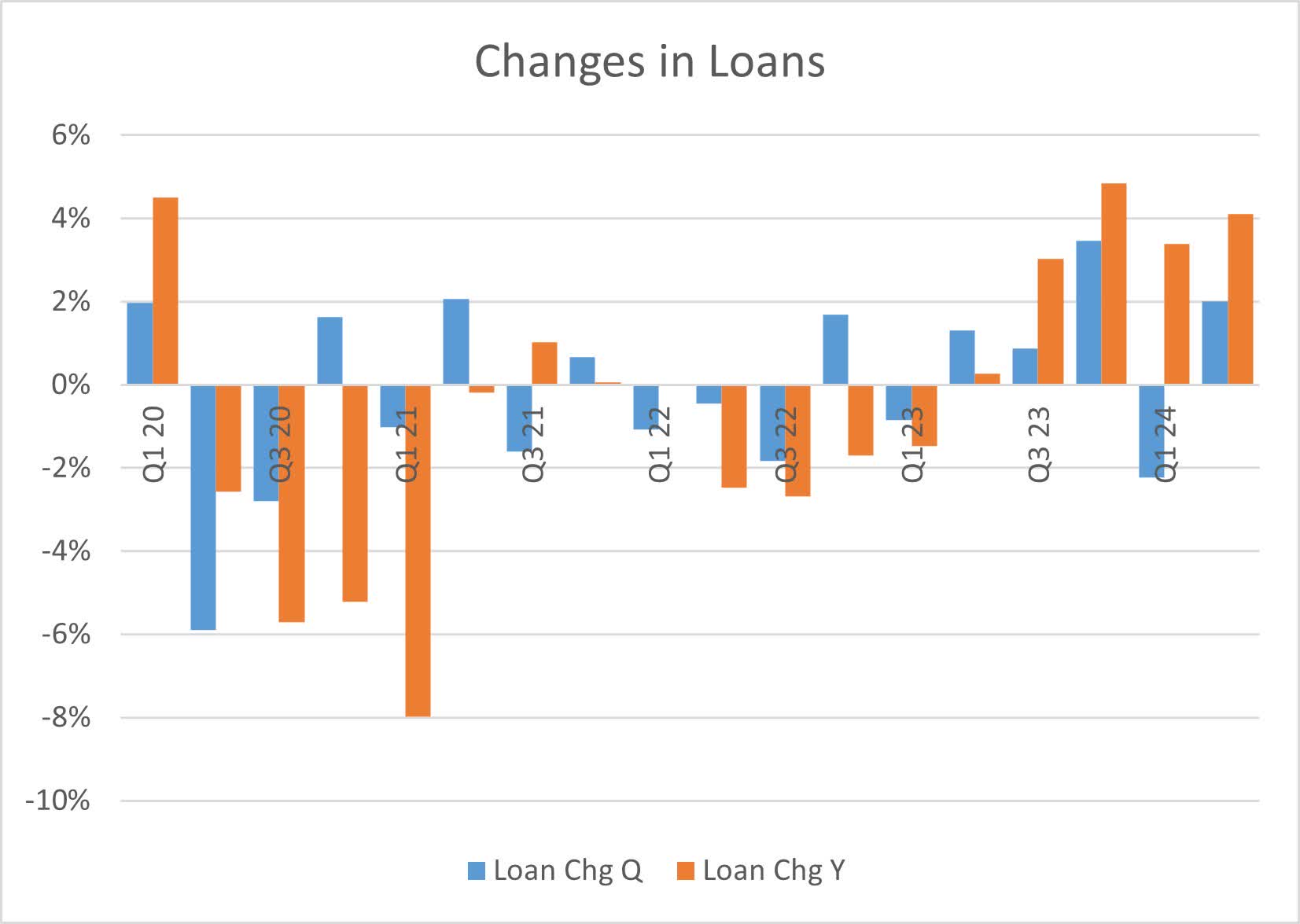

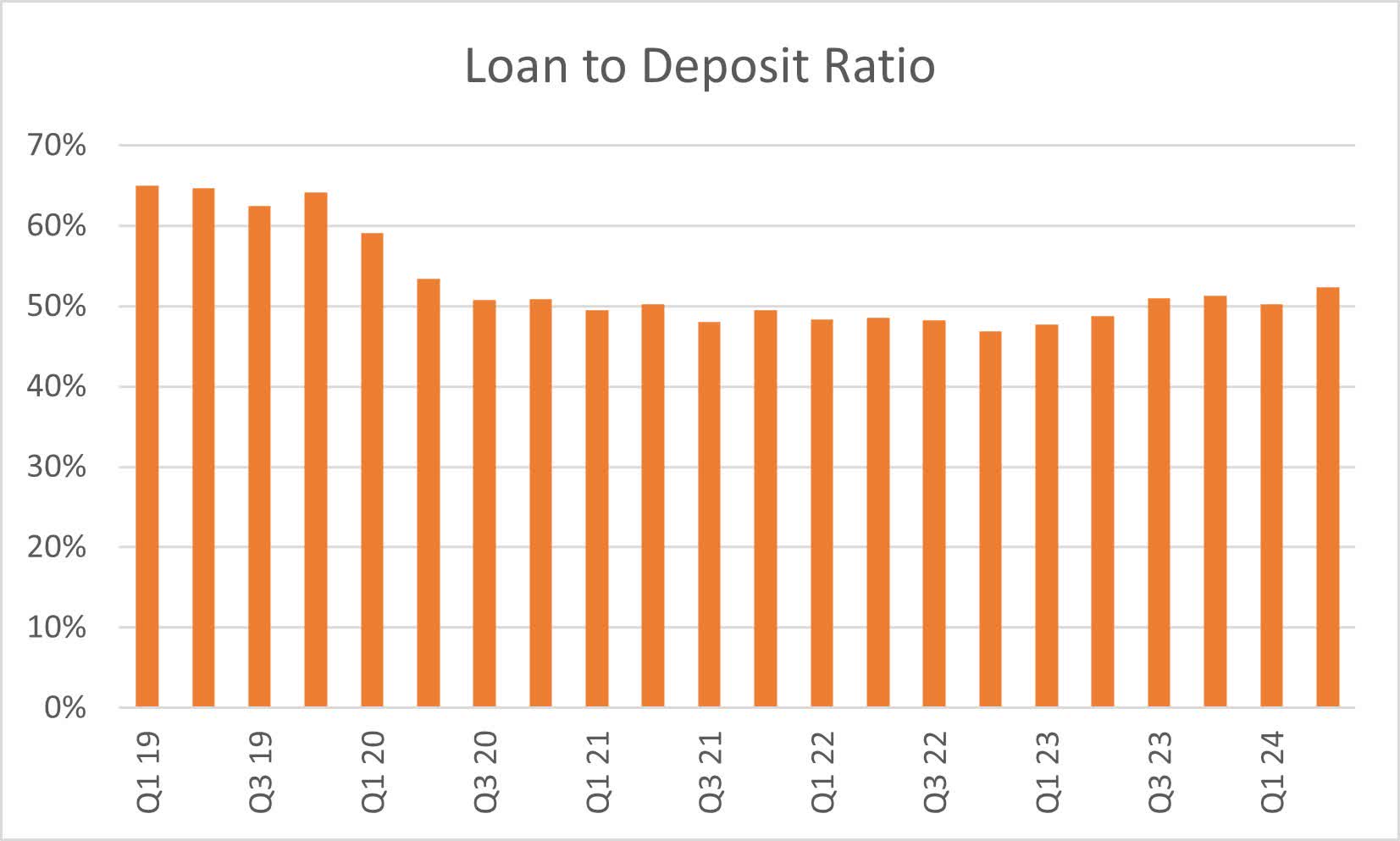

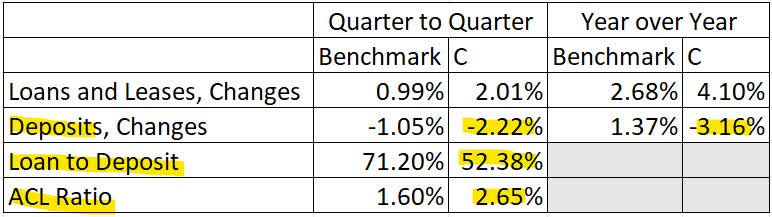

On the mortgage facet, Citigroup noticed a rebound in mortgage progress after declines in 2022 and early 2023. Mortgage progress presently stands above 4% on a year-over-year foundation. One problem with mortgage progress when deposits are shrinking is that it will increase the financial institution’s mortgage to deposit ratio, which may improve the financial institution’s dependence on exterior financing and create earnings headwinds. Happily, Citigroup has one of many lowest, if not the bottom, mortgage to deposit ratios within the business at 52%. Regardless of the rise within the mortgage to deposit ratio, Citigroup has managed to scale back its long-term debt by greater than $6 billion within the first half of 2024.

Firm Financials

Firm Financials

Federal Reserve & Firm Financials

SEC 10-Q

The Dangers and the Future

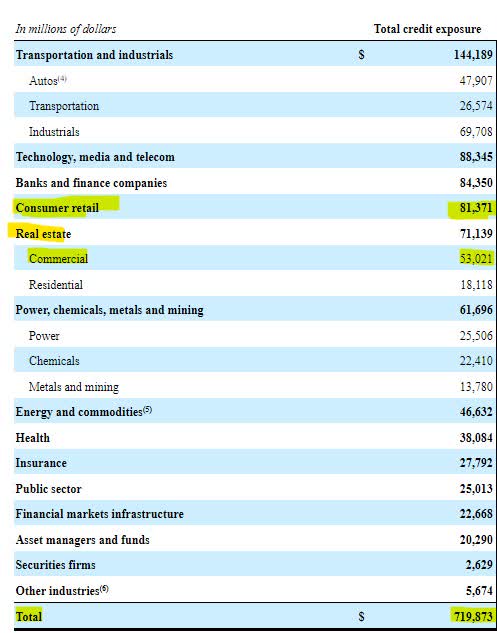

The mortgage composition and efficiency of banks are going to be underneath scrutiny because the business actual property sector undergoes adjustments referring to the pandemic. Happily, Citigroup’s $719 billion mortgage publicity solely contains $53 billion to business actual property, or simply underneath 8% of the whole portfolio. Traders needs to be extra involved with the financial institution’s $81 billion publicity to client retail, which has carried out simply as poorly because the workplace area for an prolonged interval. Happily, Citigroup is buffered by an allowance for credit score losses equaling 2.5% of gross loans, which is 90 foundation factors larger than the typical business financial institution.

SEC 10-Q

Firm Financials

Analysts are assured in Citigroup’s means to trim prices and develop earnings as they’re presently estimating 2025 earnings at over $7 per share, or 21% larger than 2024 earnings estimates. For 2026, a smaller group of analysts is estimating earnings of over $8 per share, putting as we speak’s share worth at just below 7.5 instances 2026 earnings.

Yahoo Finance

Valuation Relative to Friends

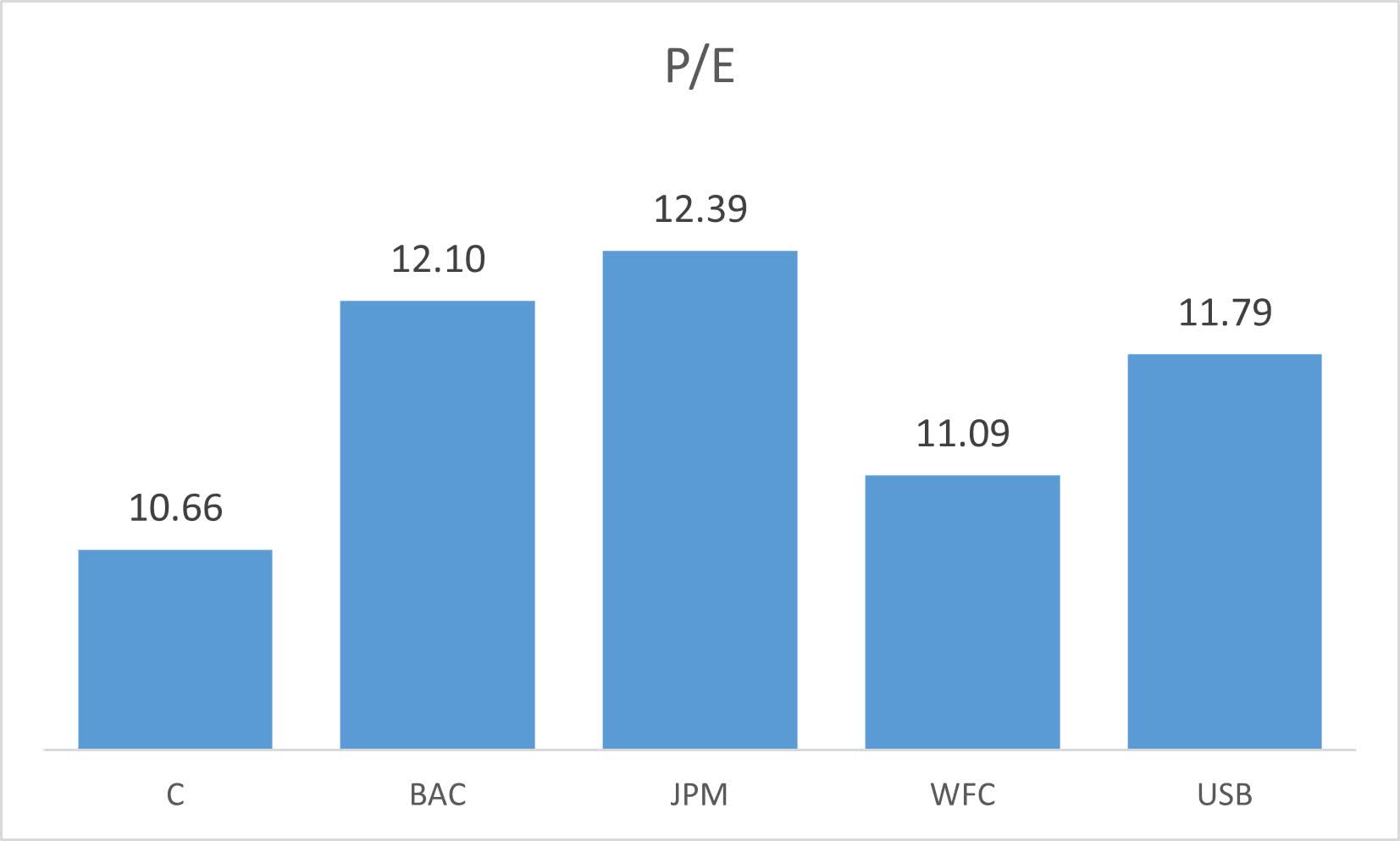

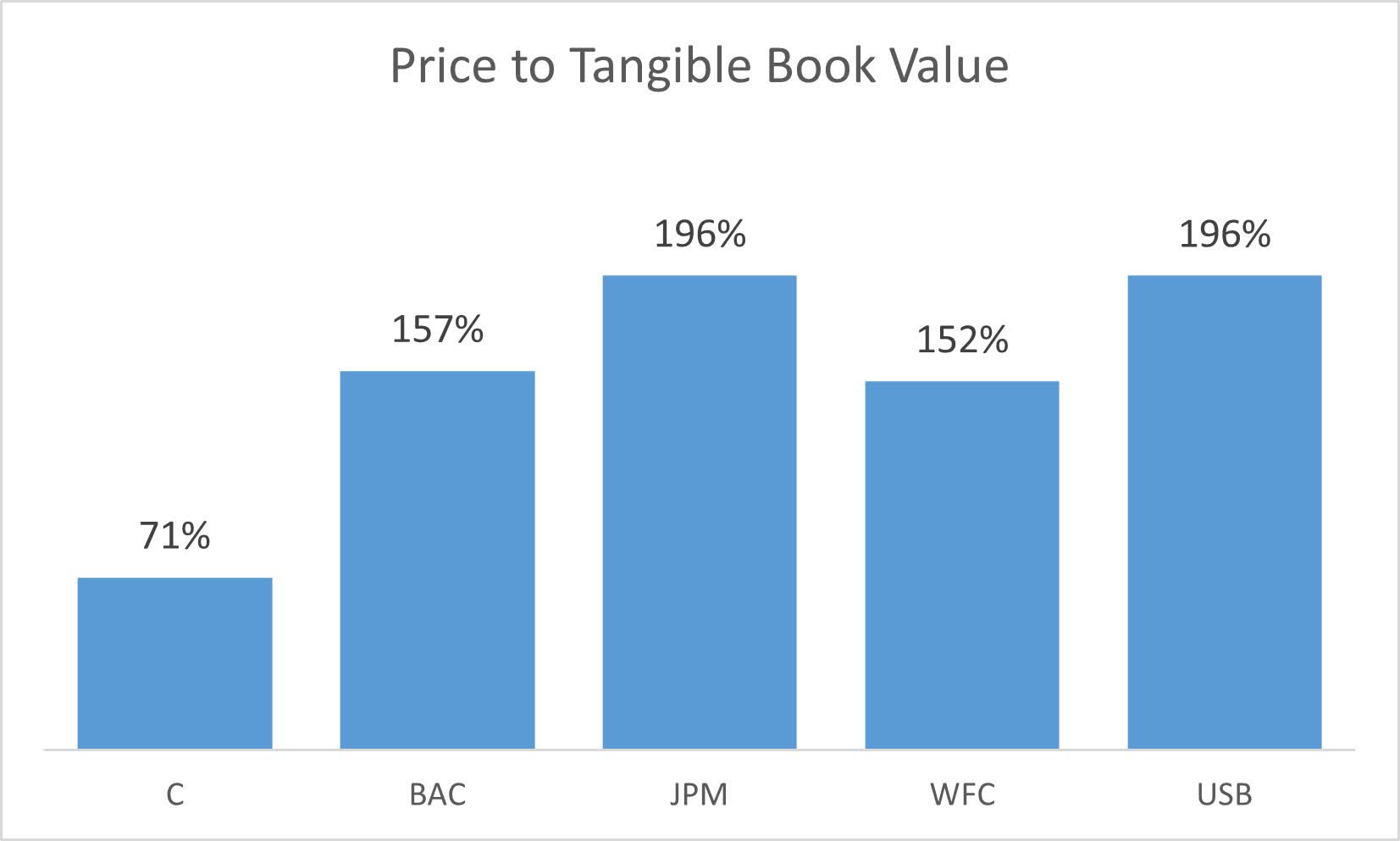

Regardless of the 50% run up in share worth during the last 12 months, Citigroup remains to be low cost when in comparison with its friends. Citigroup is among the many high 5 banks within the US by asset dimension. When evaluating Citigroup to the opposite 4 friends, the financial institution is presently buying and selling on the lowest worth to ahead earnings, however that isn’t essentially the most obvious comparability. When worth to tangible guide worth, Citigroup is properly under its peer establishments. If the turnaround succeeds and Citigroup grows earnings, the financial institution’s shares will start to maneuver in the direction of their friends and share worth progress ought to outpace earnings progress.

In search of Alpha

Earnings Releases

Conclusion

Citigroup’s conservative steadiness sheet goes to be the cornerstone of its earnings progress over the following couple of years. The financial institution has enough mortgage variety to trip out a storm and an ample allowance for mortgage losses to guard earnings. A low mortgage to deposit ratio will enable it to finance its mortgage progress as demand rises with decrease rates of interest. A budget valuation in comparison with friends is icing on the cake. I’m anticipating Citigroup to reach its turnaround initiatives over the following three years and for shareholders to be the first beneficiaries.

[ad_2]

2024-08-29 12:25:18

Source :https://seekingalpha.com/article/4717851-citigroup-shares-at-near-new-highs-but-still-cheap?source=feed_all_articles

{kind=link}

Discussion about this post