[ad_1]

Ejla/E+ through Getty Pictures

By Lynn Tune

Extra unhealthy information for the property market will proceed to weigh on confidence

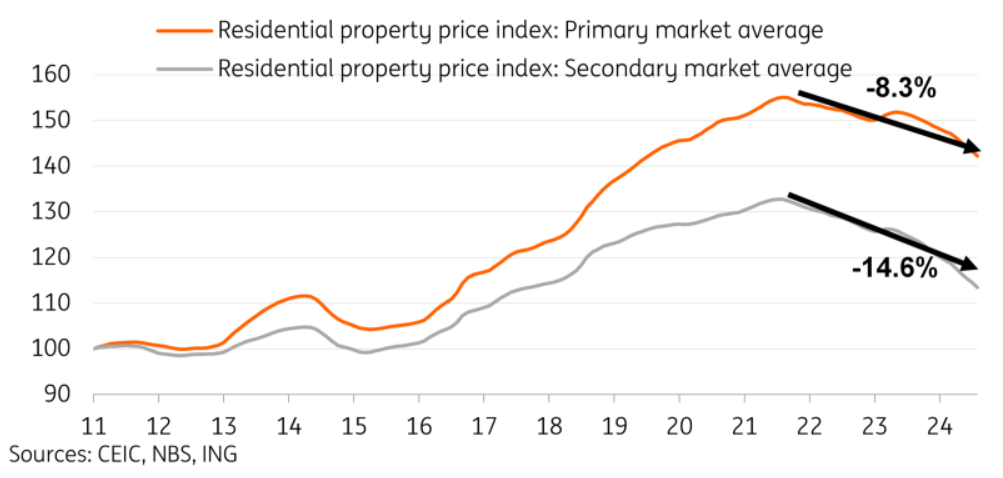

The Nationwide Bureau of Statistics printed the 70-city housing costs for August, which confirmed house costs declined at an accelerated tempo. New house costs fell by -0.73% MoM, versus a -0.65% MoM dip in July. Secondary market costs fell by -0.95% MoM versus a -0.80% MoM transfer in July. The drop in new house costs was the steepest month-to-month decline of this cycle, whereas the decline in secondary market costs was the steepest since Could.

In comparison with the height of the cycle, new house costs are actually down -8.3% whereas secondary market costs are down -14.6%.

Breaking down the 70-city pattern, for the brand new house market, 67 out of 70 cities continued to see falling new house costs, Xi’an was secure, and a pair of cities (Shanghai and Nanjing) confirmed a slight worth enhance.

Within the secondary market, 69 cities noticed worth declines, with Jilin the lone metropolis seeing a miniscule worth uptick of 0.1%. Disappointingly, the inexperienced shoots of stabilisation that we noticed in tier 1 cities pale, with Beijing (-1%), Shanghai (-0.6%), Shenzhen (-1.3%), and Guangzhou (-0.7%) all seeing pretty notable declines this month. We place a larger weight on secondary market costs as they extra immediately affect family confidence and stability sheets.

Funding and building exercise unsurprisingly remained weak. Property funding fell by -10.2% YoY ytd, whereas new house begins fell by -22.5% YoY ytd, and housing completions fell -23.6% YoY ytd.

This month’s information makes it tougher to search for silver linings and reveals that the underside has not but been established. Market experiences for a minimize to current mortgages will assist alleviate the ache for households, however we nonetheless assume that stabilising house costs stays very important for restoring confidence.

Property costs proceed to slip

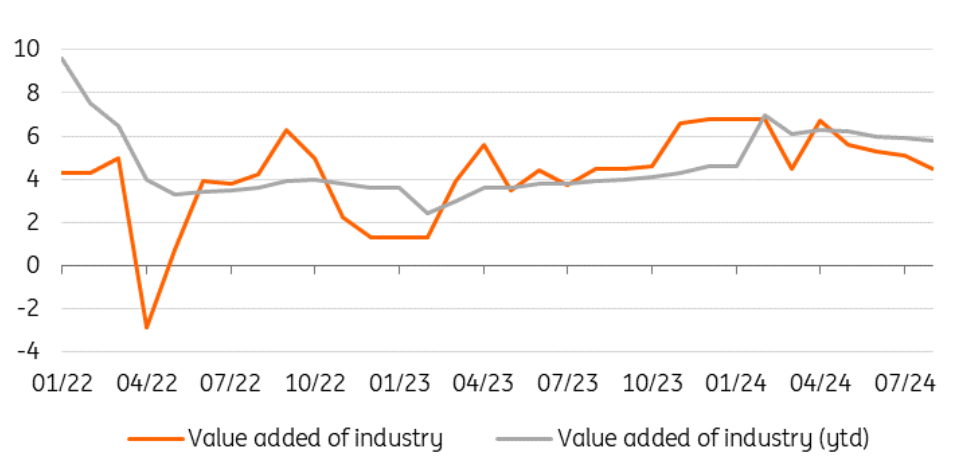

Worth added of business slumps because the drag from the “previous economic system” outweighs new progress classes

The worth added of business progress slowed to 4.5% YoY in August, down from 5.1% YoY. The 4.5% YoY progress fee was tied with a number of different months for a 13-month low, and got here in slightly weaker than consensus forecasts.

The persistent weak spot of the previous few months of PMI information has already foreshadowed this slowdown of producing.

Trying on the output of business merchandise, we will see the clear affect of the property market decline play out. Metal manufacturing dropped to -6.5% YoY, as China’s metal demand has dropped off sharply. That is per all the opposite information we have seen, together with an increase in metal export volumes and a decline in imports. Cement additionally noticed an -11.9% YoY decline in August.

The worth added of the auto business was broadly secure, registering a 4.5% YoY degree in August, a small uptick from July. Nonetheless, the amount of auto manufacturing fell -2.3% YoY. We stay involved that the auto sector might transfer from a tailwind to a headwind.

The industries favoured by China’s industrial insurance policies moderated however managed fairly spectacular progress total. Hello-tech manufacturing maintained strong progress of 8.6% YoY in August. Semiconductors (17.8%), computer systems, communications, and electrical gear (11.3%), and rail, ships, and aeroplanes (12.0%) manufacturing all continued to see strong progress charges.

After driving progress within the first half of the 12 months, it appears like manufacturing is going through some stress within the second half of the 12 months. Transferring ahead, whether or not or not the bump in August exports was a blip or a development ought to be essential in how a lot industrial manufacturing can proceed to be a progress driver. If exterior demand can keep resilient for slightly longer we may see some resilience however given incoming tariffs and slowing international momentum we’re erring on the facet of warning.

Worth added of business slumped additional in August

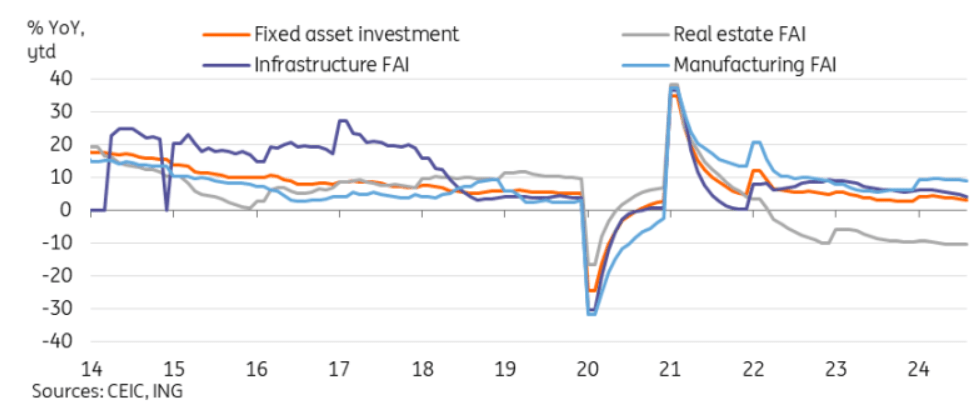

Fastened asset funding progress fell to the bottom degree of the 12 months

Fastened asset funding (FAI) progress fell to three.4% YoY ytd via the primary eight months of the 12 months, down from 3.6% YoY ytd. This was additionally slightly weaker than consensus and our forecasts for 3.5% YoY ytd.

We continued to see lots of the similar developments of the previous few months play out. Non-public funding progress, which had been progressively slowing in earlier months, lastly tipped into unfavourable territory, falling to -0.2% YoY ytd from a flat 0.0% final month. Cautious sentiment continues to restrict non-public funding.

Infrastructure FAI fell to only 4.4% YoY ytd, as targets for funding haven’t been as apparent as in years previous.

Manufacturing FAI continued to outperform, although it additionally slowed to 9.1% YoY ytd from 9.3% YoY ytd within the earlier month. Inside this class, electrical equipment and gear manufacturing (-0.3%) and auto manufacturing (5.4%) had been laggards, whereas many different classes together with meals manufacturing (26.1%) and railway, marine, aerospace and different transport gear manufacturing (30.7%) noticed speedy progress.

Hello-tech FAI grew by 10.2% YoY ytd and will proceed to profit from the technological self-sufficiency drive.

Trying forward, barring a large-scale progressive assist package deal for consumption, funding will possible should be ramped up if China hopes to attain its 5% progress goal.

FAI slowed to the bottom degree of the 12 months

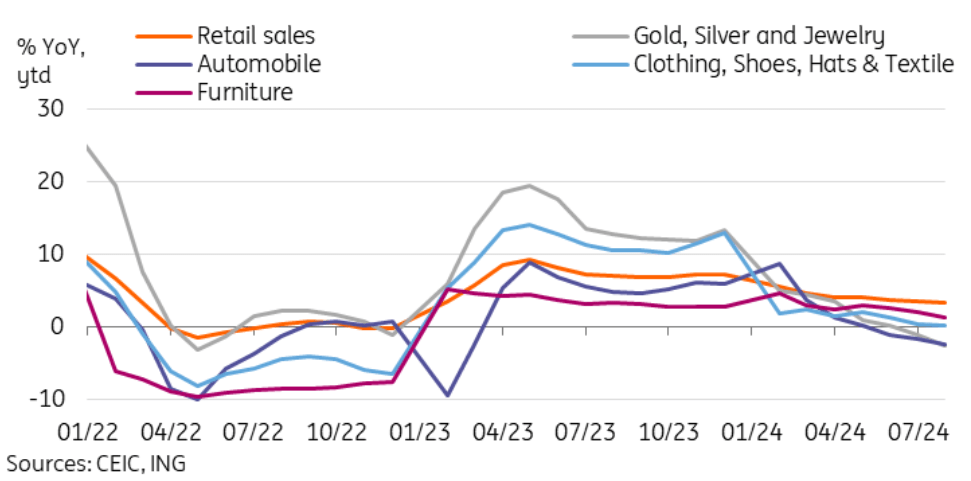

Retail gross sales confirmed consumption momentum persevering with to falter

Retail gross sales progress fell to 2.1% YoY in August, down from 2.7% YoY in July, decrease than consensus forecasts although barely managing to keep away from reaching a brand new post-pandemic low. Final month’s shopper confidence information confirmed family confidence slumping again towards pandemic lows, and this clearly continues to suppress consumption.

The information continues to color a transparent image of cautious family spending. Discretionary consumption classes specifically had been exhausting hit in August. Gold and jewelry (-12.0%), autos (-7.3%), and cosmetics (-6.1%) had been the largest drags on retail gross sales. Classes tied to the housing market, together with furnishings (-3.7%) and constructing supplies (-6.7%) had been additionally in contraction.

Our “eat drink and play” theme continued to be the lone silver lining in consumption, although it additionally reveals indicators of slowing down. Catering (3.3%), meals (10.1%), tobacco and alcohol (3.1%), and sports activities and recreation (3.2%) all outperformed headline progress.

Weak confidence has closely dragged on discretionary consumption

Further coverage assist will likely be wanted so as to attain 5% this 12 months

Month-to-month momentum has slowed in the previous few months, and mixed with a much less supportive base impact, will probably be difficult to succeed in this 12 months’s 5% progress goal if there isn’t a vital change forward. Whereas we’ve got seen many supportive insurance policies introduced this 12 months, they’ve been piecemeal and haven’t but been ample to show the momentum round.

President Xi reportedly known as upon authorities officers to “attempt to attain the full-year financial and social improvement objectives” at a gathering in Lanzhou this week. We consider that this name may enhance the short-term urgency of coverage rollout. As we’re already towards the tail-end of the third quarter, time is operating low for policymakers to introduce measures to buoy the economic system amid quite a few headwinds.

Content material Disclaimer

This publication has been ready by ING solely for data functions regardless of a specific person’s means, monetary scenario or funding targets. The data doesn’t represent funding advice, and neither is it funding, authorized or tax recommendation or a proposal or solicitation to buy or promote any monetary instrument. Learn extra

Editor’s Be aware: The abstract bullets for this text had been chosen by Looking for Alpha editors.

[ad_2]

2024-09-14 09:35:00

Source :https://seekingalpha.com/article/4721116-china-data-dump-time-running-out-to-achieve-this-years-growth-target?source=feed_all_articles

{kind=link}

Discussion about this post