[ad_1]

mediamasmedia

Funding motion

I really helpful a purchase score for Carrefour (OTCPK:CRRFY) (OTCPK:CRERF) after I wrote about it in Could final 12 months, as I anticipated multiples to rerate greater because the enterprise executes and beats consensus expectations, which it has carried out for 1Q23 (final time I wrote about it). Primarily based on my present outlook and evaluation, I stay a purchase score for CRRFY, as I feel the valuation remains to be very low cost relative to historical past and friends. Whereas Europe (ex-France) remains to be performing poorly, macro-recovery and normalizing climate ought to assist enhance progress. There are additionally constructive features that saved me inspired: revenue efficiency in France and constructive outcomes from value investments; sturdy Brazil efficiency; and largely steady general P&L traits.

Assessment

CRRFY reported earnings yesterday, and the outcomes weren’t precisely the perfect. 1H24 internet gross sales had been flattish vs. final 12 months at EUR40.6 billion, dragged down by poor France efficiency of -2.9%, offset by sturdy LATAM efficiency of 10.7% progress. Nonetheless, the expansion pattern softened into 2Q24, the place like-for-like [LFL] progress for France fell by 3.5% (from -0.5% in 1Q24) and Europe fell by 2.7% (from -0.2% in 1Q24). The constructive takeaway was that EBITDA grew regardless of flat prime line efficiency, as margins improved by 17 bps, which led to EBIT progress of 20% (the EBIT margin expanded by 11 bps).

The primary downside with CRRFY funding case is efficiency in the remainder of Europe (excluding France), which noticed LFL progress of two.7%, pushed by unfavorable efficiency throughout the board, aside from Romania (0.2% LFL progress, which is mainly flat). Recurring working revenue [ROI] was additionally down by an enormous share, from EUR164 million in 1H23 to EUR84 million. The frequent offender throughout the area was the dangerous climate and poor client spending surroundings (which is why CRRFY invested in pricing to remain aggressive). It is a sizable a part of CRRFY enterprise, so I can not simply rub it off, however I’m not positive if the efficiency could be as dangerous as it’s in 1H24 if not for the dangerous climate and poor spending surroundings. Be aware that 1Q24 LFL was down 0.2%, and regardless of all of the unfavorable impacts, LFL progress was solely down 2.7% in 2Q24, and that is in opposition to a reasonably sturdy comp base in 2Q24 (7.4% LFL progress). If we make some assumption that unfavorable climate + poor client surroundings + robust comp base = low-single-digit headwind (say 1%), LFL progress is basically solely down 1.7%, which isn’t that alarming (in the mean time). Therefore, I don’t assume traders ought to extrapolate Europe’s (excluding France’s) 2Q24 efficiency for the remainder of the 12 months for now.

Placing apart the above, there are a number of constructive takeaways from this consequence which are price highlighting.

In France, climate and a poor client spending surroundings had been additionally headwinds for this area. The three.5% LFL decline was pushed by hypermarket LFL declines of 5.5% y/y and grocery store LFL declines of 1.5%. Regardless of this, France’s ROI managed to develop by 6.2% to EUR 286 million, and its working margin was up 14bps to 1.6%. Notably, the ROI grew regardless of CRRFY investing closely in value (value is now again to pre-peak inflation ranges), which suggests the incremental quantity has been extraordinarily accretive to P&L. Much more importantly, the margin enchancment is because of structural components, provided that it was pushed by price financial savings and the contribution of strategic initiatives. What this additionally means is that submit the present financial uncertainty in France, the place customers are extra keen to spend and climate turns into regular, the ROI margin profile is prone to go greater.

Efficiency in Brazil was additionally very encouraging, because it printed LFL progress of 6% for 2Q24. Gross sales momentum in Brazil is encouraging, as each pricing and quantity drivers are again in constructive mode. The CRRFY acquisition of Atacadao (and conversions of Carrefour shops to Atacadao) is delivering very constructive outcomes, with LFL progress of 21.4% (for BIG shops transformed to Atacadao). B2B gross sales at money and carry are additionally rising by double digits as clients restock stock. One other promising space is retail, the place a 2.3% enhance in LFL reveals that the corporate’s revised pricing technique and portfolio changes are paying off. Progress to extract synergies can also be heading in the right direction, with Atacadao already reaching R$2.3 billion per 12 months and never anticipating to attain annual synergies of R$3 billion by the tip of 2025 (extra room for margin to increase).

Total, regardless of all of the discuss poor LFL progress, macro headwinds, and poor climate, if we take a step again and take a look at CRRFY financials, the P&L is fairly stable. Gross margin stood at 19.4% of internet gross sales, only a 40-bps decline from 1H23. Do not forget that 1H23 LFL progress was constructive within the high-single-digits. Importantly, the compression was because of CRRFY’s value funding technique and pivoting in the direction of an built-in/franchised retailer combine, and as such, it was not because of poor working efficiency (this is a crucial level to notice). Down the P&L, distribution prices even improved by 53bps to fifteen.1% of internet gross sales vs. 15.6% in 1H23 because of sturdy price self-discipline, and CRRFY has additionally efficiently applied its cost-saving plan, with EUR580 million achieved in 1H24. Total, CRRFY managed to drive 11bps enchancment to 1H24 EBIT margin of 1.79% (EUR743 million).

Valuation and dividend yield at very enticing ranges

Writer’s work

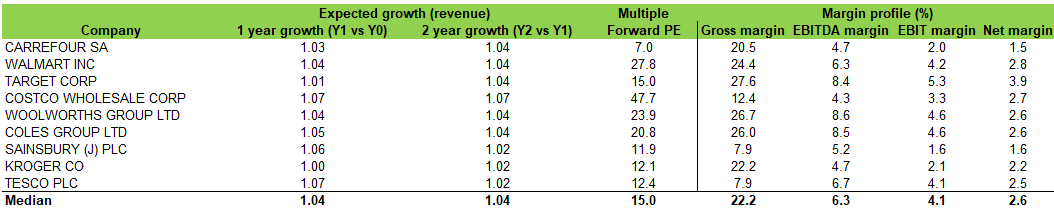

Lastly, CRRFY is now buying and selling at much more enticing valuation ranges relative to historical past. Traditionally, CRRFY traded at 12.2x ahead earnings and is now buying and selling at 7x. Even in opposition to friends, the inventory trades at a steep low cost regardless of having an analogous income progress outlook (~mid-single-digits). I get the purpose that CRRFY has a poorer margin profile, however the enterprise has been enhancing margins (internet margin was 1.1% in 2018), and even on this present robust working surroundings, it managed to enhance margins (as will be seen within the 2Q24 outcomes). Whereas it’s unlikely that CRRFY can shut the hole between itself and friends’ common of two.6% inside the subsequent few years, I don’t assume it’s unattainable to succeed in the identical stage as Sainsbury (1.6% internet margin) since CRRFY already achieved it final 12 months. Regardless of this, Sainsbury trades at 12x, however CRRFY solely trades at 7x. I consider an enormous a part of this low cost is due to the unsure European surroundings, and the market is ready for extra certainty.

I can not time when the Europe client spending surroundings will get higher, however the excellent news is that whereas ready, CRRFY now gives ~6% dividend yield (indicated), which isn’t that dangerous contemplating that charges are getting minimize in Europe and the US is prone to minimize charges in 2H24 too.

Danger

The massive threat for CRRFY stems from the poor macro surroundings that has immediately impacted customers spending energy, and if this example will get worse in Europe, it is not going to solely drag down CRRFY’s potential to recuperate progress, however I additionally anticipate the market to proceed attaching a reduction to CRRFY.

Remaining ideas

My suggestion is a purchase score for CRRFY. Whereas general prime line progress was muted, the corporate demonstrated resilience by means of margin enlargement and stable efficiency in key areas like France and Brazil. A notable facet is CRRFY’s potential to enhance profitability regardless of a difficult working surroundings. CRRFY valuation additionally stays low cost relative to historic ranges and friends.

Editor’s Be aware: This text discusses a number of securities that don’t commerce on a significant U.S. change. Please concentrate on the dangers related to these shares.

[ad_2]

2024-07-25 06:57:36

Source :https://seekingalpha.com/article/4706442-carrefour-earnings-still-positive-on-stock-as-valuation-remains-cheap?source=feed_all_articles

{kind=link}

Discussion about this post