[ad_1]

Sundry Images/iStock Editorial by way of Getty Pictures

AT&T (NYSE:T) made the basic mistake of trying to develop into a mega conglomerate. The corporate invested in wholly unrelated belongings resembling DirecTV and TimeWarner, each of which it was compelled to spin-off. As we’ll see all through this text, the corporate’s latest earnings spotlight the energy of its new enterprise mannequin, which is able to assist shareholder returns.

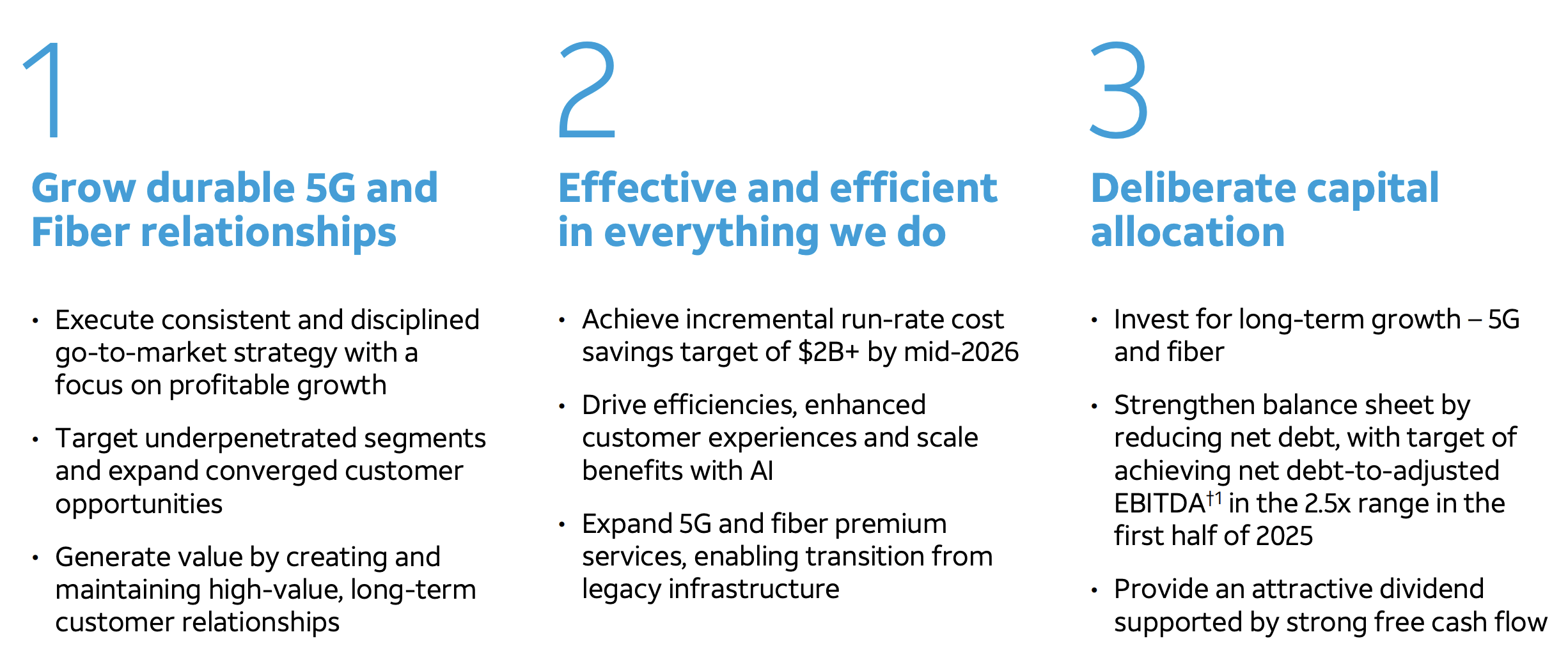

AT&T Enterprise Priorities

The corporate has various enterprise priorities we would wish to see it deal with with its refocused portfolio.

AT&T Investor Presentation

The corporate’s first objective is to develop 5G, now that the most important funding and spectrum buy cycles are finished. The corporate will hopefully be capable to develop income and hold bills low. The corporate is combining this with run-rate price financial savings anticipated to be within the billions, and synergies between its infrastructure.

The corporate has been punished by the market for a very long time by its debt load. The corporate expects to attain its long-term internet debt-to-adjusted EBITDA goal of two.5x in 1H 2025. That may allow the corporate to take care of its dividend of just about 6% and drive general shareholder returns.

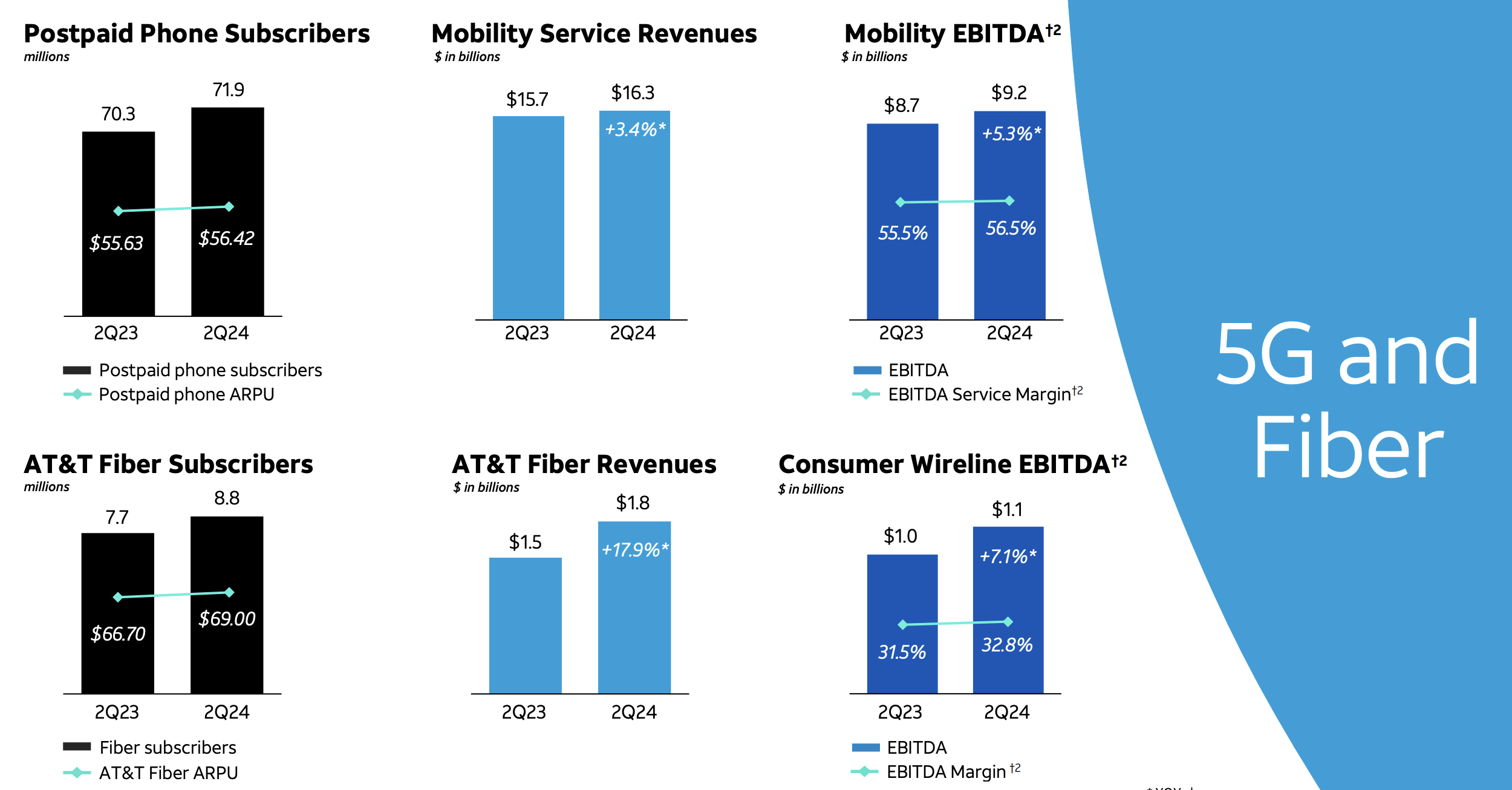

AT&T YoY Progress

The corporate has seen robust quantifiable YoY progress amongst all of its enterprise segments.

AT&T Investor Presentation

The corporate noticed postpaid telephone subscribers improve by 2% together with an identical 2% progress in ARPU. That progress strains up with inflation for ARPU, but it surely reveals the corporate’s skill to proceed getting subscribers in a saturated market. This enabled the corporate to each develop its income and EBITDA margin.

The corporate’s fiber enterprise, which we’ll focus on in additional element under, has additionally remained extremely robust, with fiber revenues rising virtually 18% YoY. That led to robust high line EBITDA and EBITDA margin progress.

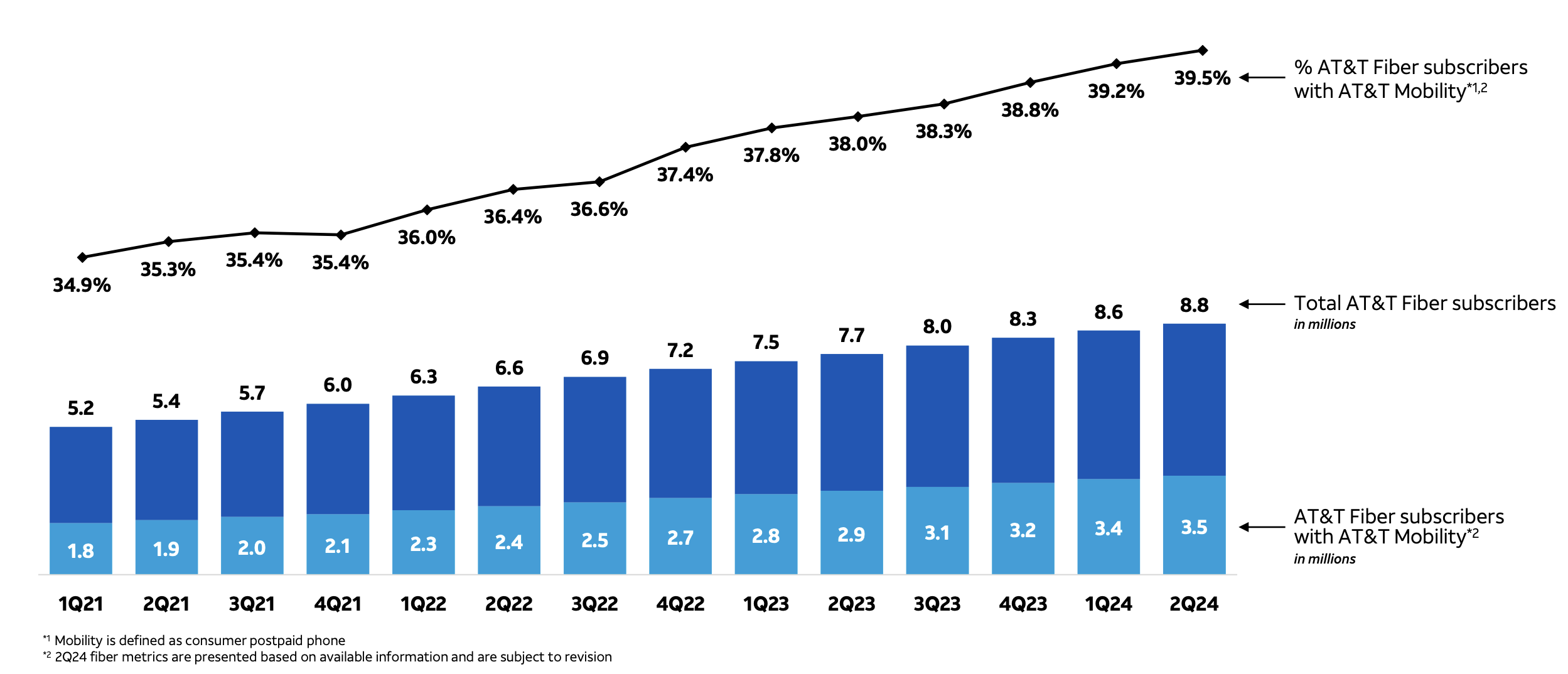

AT&T Fiber Progress

AT&T has been a serious source of progress in its fiber enterprise, one thing it is continued to chase.

AT&T Investor Presentation

The corporate has managed to develop to eight.8 million complete fiber subscribers, as common fiber income has gone as much as virtually $2 billion quarterly. As somebody who’s anecdotally used each AT&T fiber and main competitor Comcast fiber, AT&T is considerably extra dependable, gives symmetric up and down bandwidth, and has no knowledge caps. That makes it a way more pleasing expertise.

The corporate has labored to chase synergies with its AT&T mobility enterprise, with not solely fiber subscriptions rising, however the % of consumers with AT&T mobility has grown as nicely. That ratio is now virtually 40% for the corporate. The corporate’s focus in each these segments will assist long-term income progress.

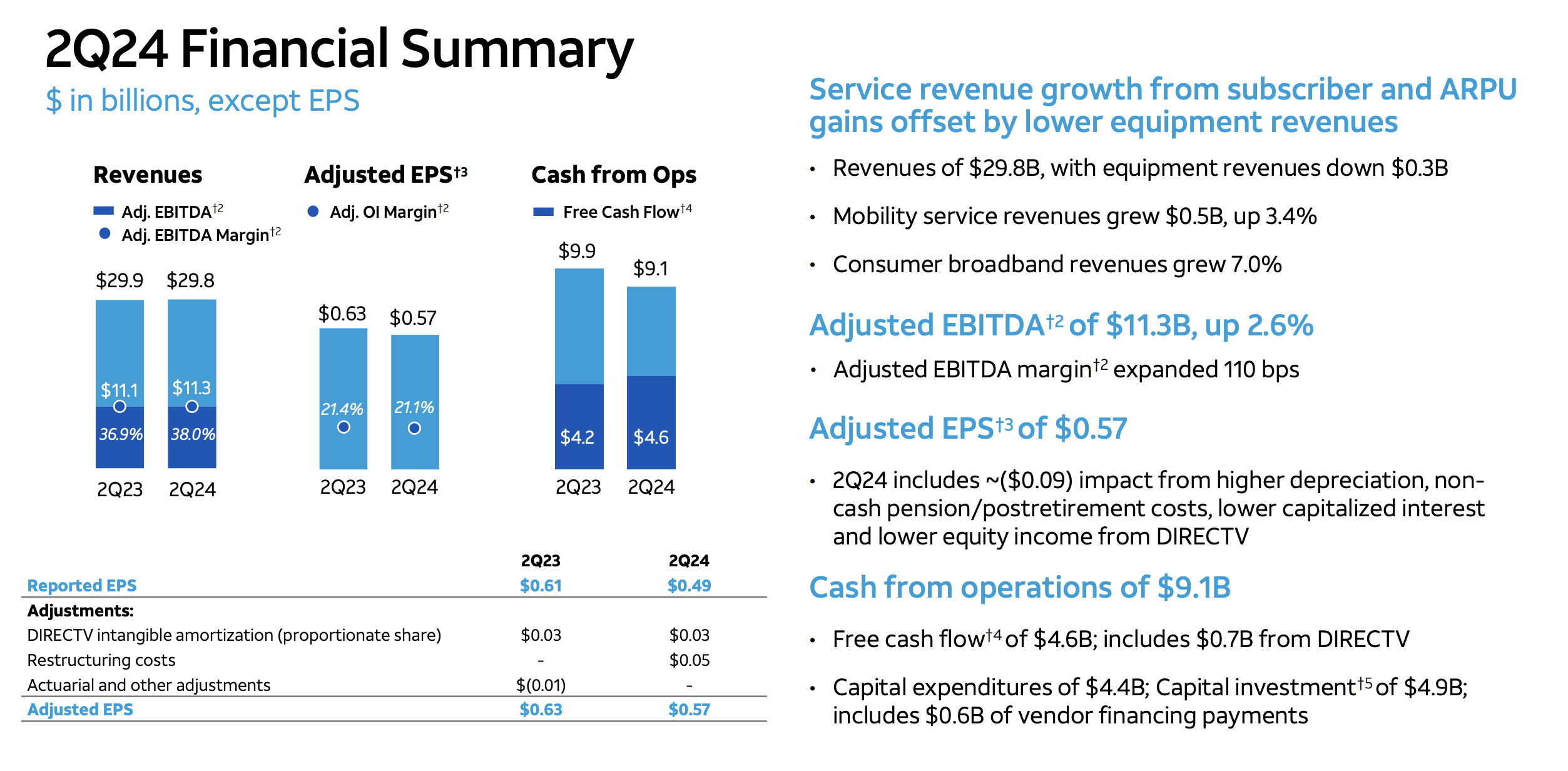

AT&T Monetary Efficiency

The corporate had fairly robust efficiency by way of the quarter, regardless that CFFO declined.

AT&T Investor Presentation

Financially, the corporate’s general enterprise remained robust. The corporate’s income remained roughly flat, nonetheless, the corporate’s EBITDA margin grew by 1% to greater than $11.3 billion in adjusted EBITDA. The corporate benefited from energy throughout the board. EPS of $0.57 declined barely YoY, however many of the affect was from numerous depreciation and retirement prices.

The corporate’s FCF stays robust, and the corporate continues to generate robust FCF from DirecTV regardless of the enterprise’ declining nature. The corporate’s FCF yield annualized is ~15% which is able to allow large shareholder returns.

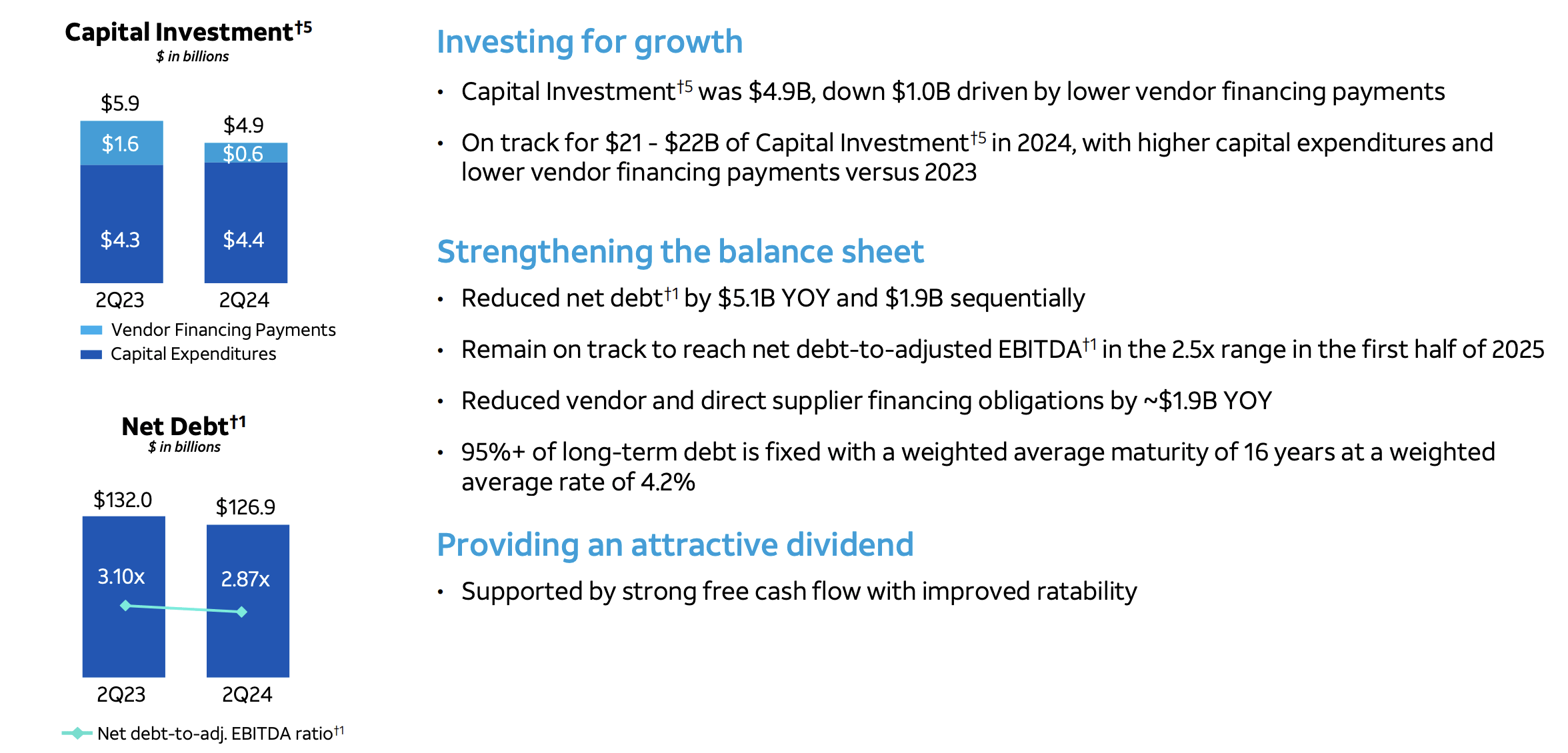

AT&T Capital Allocation

The corporate’s capital allocation continues to be supported by FCF and its skill to show that into shareholder returns. That is versus the corporate’s modest $135 billion market capitalization.

AT&T Investor Presentation

The corporate has continued to handle its investing whereas betting on its future and progress. The corporate spent $4.9 billion in capital funding, annualized at virtually $20 billion. The corporate expects $21.5 billion in capital funding for 2024, with decrease vendor financing funds. That allows the corporate to speculate extra immediately into its enterprise.

The corporate has managed to cut back internet debt by $5.1 billion whereas rising its EBITDA. The corporate stays on observe to hit 2.5x within the subsequent 12 months. This has include lowered vendor and financing obligations as nicely, and the corporate’s common curiosity is a mere 4.2%. Meaning the corporate is paying solely ~$5.5 billion in annual curiosity, nicely under market charges, and it is one thing it may comfortably afford.

The corporate’s money stream allows robust continued shareholder returns.

AT&T Shareholder Returns

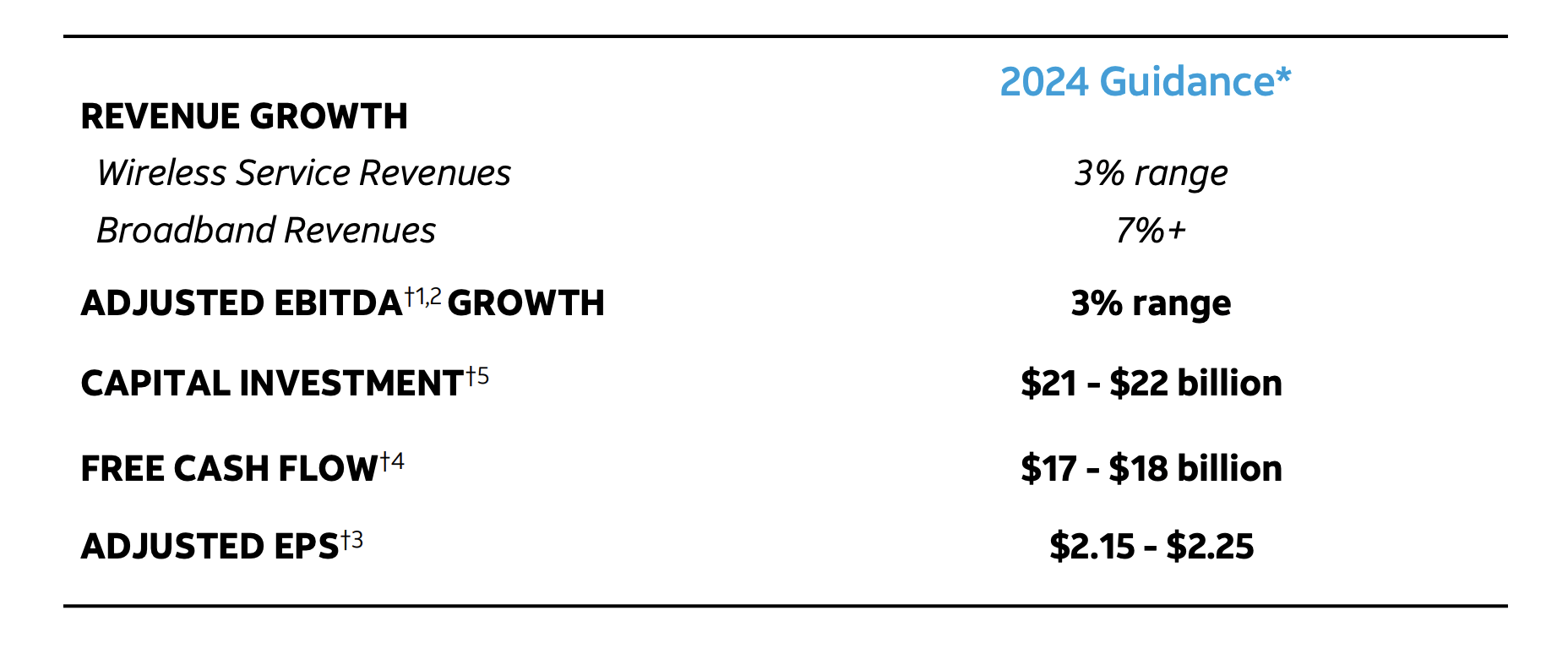

The corporate’s 2024 steerage reveals the corporate’s skill to proceed driving shareholder returns.

AT&T Investor Presentation

General, AT&T can drive robust shareholder returns. Even when the big firm is not rising like loopy, it is nonetheless rising. The corporate is seeing 3% adjusted EBITDA progress and continued income energy. Capital funding is remaining hefty as the corporate is constant to spend money on its enterprise for the long run.

The corporate’s adjusted EPS places it within the stable single-digit P/E ratio vary, and the corporate’s FCF is $17.5 billion. That is FCF that may comfortably cowl the corporate’s virtually 6% dividend yield and help share buybacks and different types of returns as nicely. For affected person buyers, we anticipate shareholder returns to proceed rising.

Thesis Threat

The most important threat to our thesis is AT&T administration’s historical past of lofty ambitions and spending on poor investments. The corporate has labored laborious to scrub up its portfolio of belongings and drive future returns, nonetheless, there is no assure that administration does not get carried away sooner or later and make extra poor selections.

Conclusion

AT&T has recovered by 40% from its 52-week lows set final August. Regardless of that large restoration, the corporate has room to develop as buyers settle for what we have argued for some time. The corporate’s debt is just not a priority, with its long-term period and 4.2% common weighted charge. That, mixed with rising EBITDA, can allow the debt to be paid down simply.

On the identical time, the corporate is constant to generate robust FCF. It is sustaining its dividend yield of just about 6%, and it has the power to drive hefty shareholder returns by way of repurchases, debt pay down, and dividends. All of that collectively helps make the corporate a invaluable long-term funding alternative.

[ad_2]

2024-08-01 07:50:10

Source :https://seekingalpha.com/article/4708956-att-earnings-highlights-continued-recovery-potential?source=feed_all_articles

{kind=link}

Discussion about this post