[ad_1]

AndreyPopov

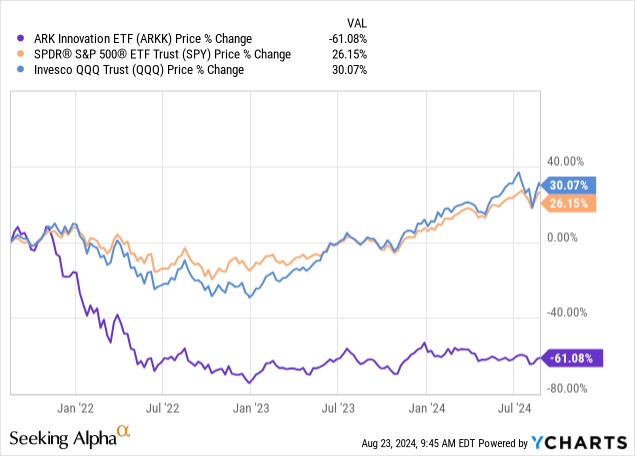

Asana (NYSE:ASAN) was a major instance of the exuberance of 2021 and the eventual bust within the inventory costs that adopted shortly after. In hindsight, many do not think about the correction typically market throughout that point as something vital as inventory market rebounded to all time highs inside a brief timeframe. However there are loads of names which might be nonetheless buying and selling round all time lows (I discover ARKK to be good proxy to measure this phenomena)

Whereas I believe many such names could by no means get better as their enterprise fundamentals proceed to weaken going right into a weaker economic system, once I have a look at Asana I really feel the worst could also be behind us.

Asana’s merchandise and its relevance within the present surroundings

Asana is a number one work administration platform that helps groups manage, monitor, and handle their work and capabilities as a robust instrument for enhancing productiveness and collaboration throughout organizations. It operates on a subscription-based mannequin with a number of pricing tiers which permits the corporate to cater to a variety of consumers. The primary promoting level is its proprietary “work graph,” a multi-dimensional knowledge mannequin that captures duties, initiatives, targets, and their relationships. This know-how offers dynamic views and real-time insights, enabling groups to handle work extra successfully.

Asana’s platform is extremely related in right now’s surroundings, the place distant and distributed workforces have gotten the norm and offers for seamless collaboration guaranteeing that groups can work collectively successfully with out location being an impediment. Moreover, one other massive development I’ve personally seen in right now’s workplaces is shorter product lifecycles and an extended rising want for agile and environment friendly workflows. With the product’s concentrate on decreasing “work about work” it performs a giant position in rising productiveness.

Asana’s meteoric rise and fall

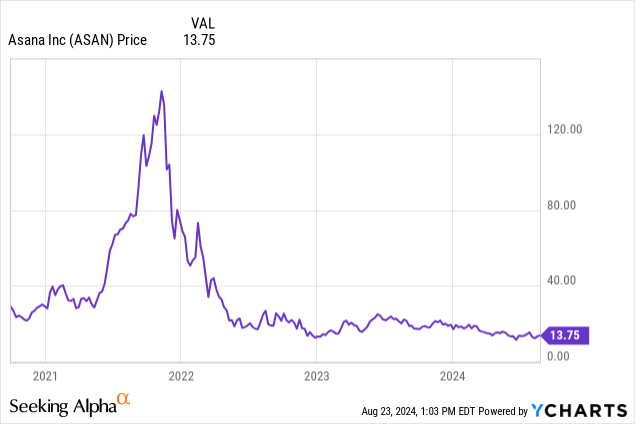

The inventory’s meteoric rise was supported initially by an exponential topline development. However as development tales go, every massive beat in development comes with even larger expectations for the long run. When the truth stops matching expectations the inventory sees a dramatic reset in its valuations and worth (PS ratio was 72x at its peak worth of $142)

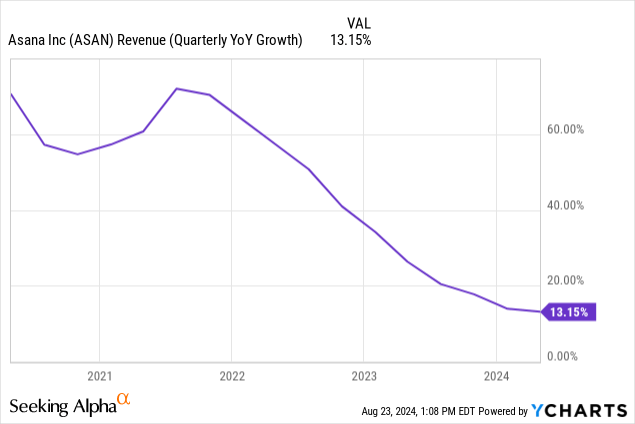

Summarizing its journey, we noticed a peak topline development of near 70% which has now come down all the way in which to low double digits. On the identical time the drawdown from its peak inventory worth has been roughly 90%!

Is the worst behind us?

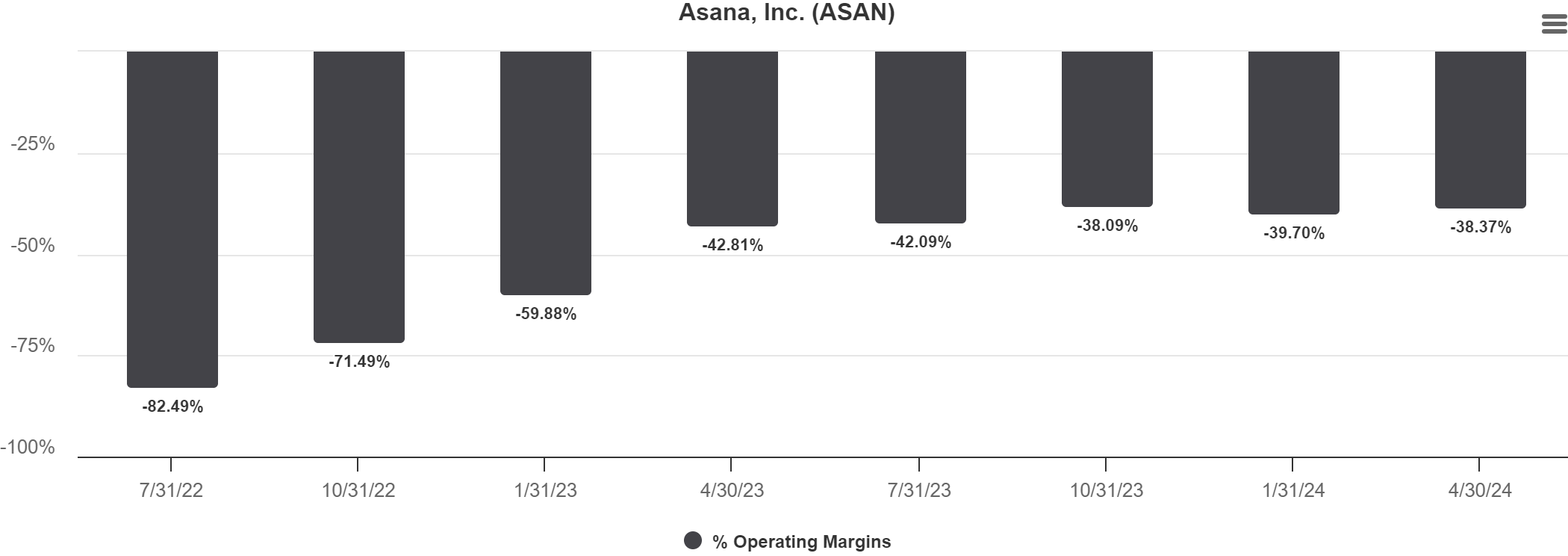

Exhibit A: Stabilizing financials

I’m in no way saying a inventory that has fallen 90% from its highs will not have room to fall additional. However by what we have now noticed within the final yr plainly the worst of the transfer could also be behind us.

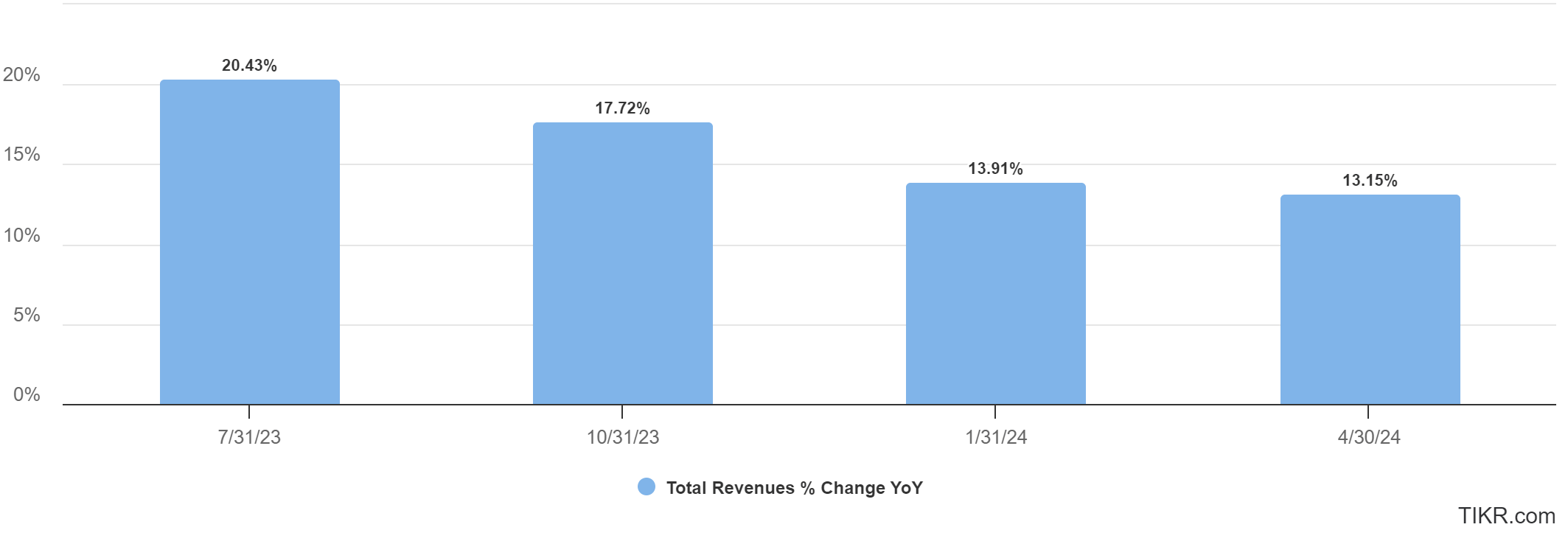

Tikr

Tikr

Change in development charges has considerably come down and has stabilized in current quarters. Whereas the corporate has not offered any indications of when it will likely be GAAP worthwhile, it has indicated in its most up-to-date earnings name that it will likely be Free Money circulation optimistic for Fiscal 2025. Though this may get deceptive in terms of inventory based mostly compensation, there are clear indications that the corporate is making an attempt to enhance its bottom-line. Its gross margins have at all times been excessive round 90% however the wrongdoer was its gross sales and advertising bills. They’ve began to rein this in ensuing within the enchancment of its working margins.

Exhibit B: Q2 Earnings Preview

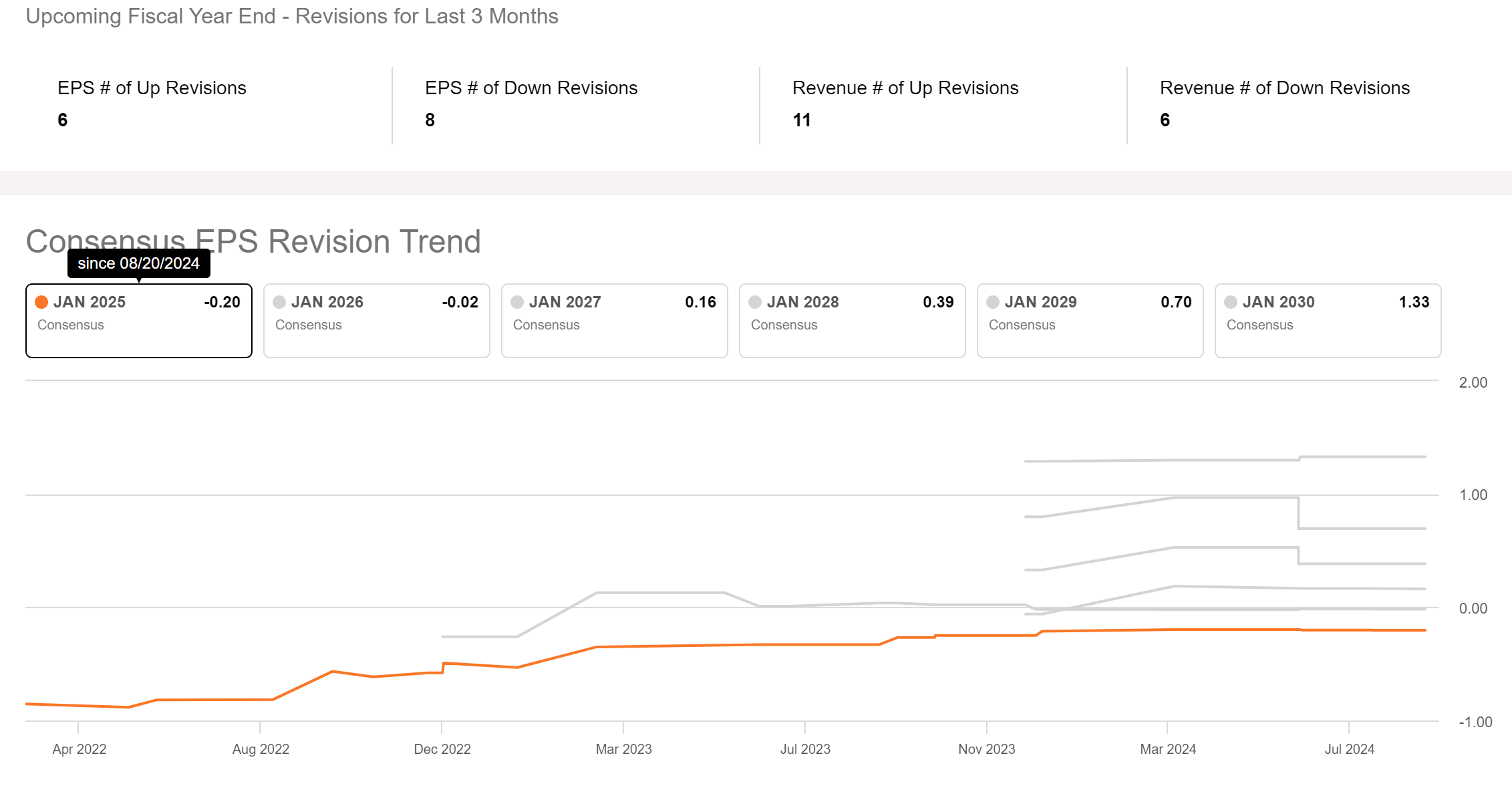

Within the final 12 months we have now seen web revenues of $672M and a diluted EPS of -$1.16. For Q2 Fiscal 2025, the corporate anticipates revenues of $177M – $178M, reflecting a year-over-year development of 9% – 10%. For the total FY 2025, they anticipate revenues to vary between $719M and $724M, representing a development of 10% – 11% year-over-year. Nonetheless, they venture a non-GAAP loss from operations between $55M and $59M, with an working margin of roughly unfavourable 8% on the midpoint of their steering and a web loss per share of $0.21 to $0.19.

Earnings Revisions for FY (SA)

Analysts are solidly divided of their estimates for the yr because the variety of up revisions and down revisions are roughly equal however the consensus is alongside the traces of what the administration has laid out.

General, the takeaway right here is that income development charges will proceed to stabilize, backside line will proceed to enhance and the worst could also be behind us.

Exhibit C: Valuation that has come right down to earth

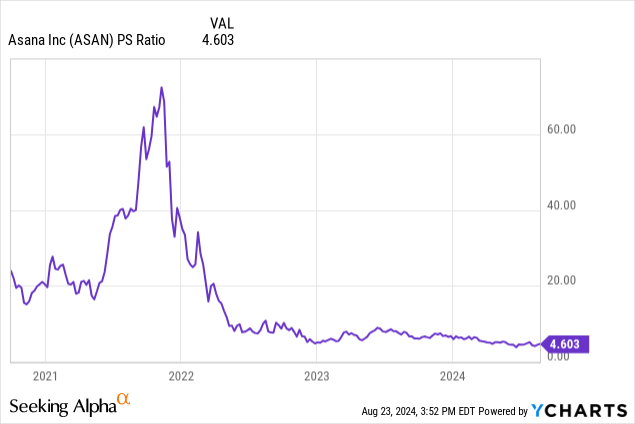

As talked about earlier, the corporate at one level was buying and selling at a Worth to Gross sales a number of of roughly 72x on the top of the exuberance seen within the inventory market throughout 2021. Certain there was some justification with excessive development charges however clearly a lot of the occasions its not sustainable. The excellent news is that it seems to be quite a bit higher now and once you have a look at its percentile rank it’s additional clear that it’s presently buying and selling near its lowest multiples in historical past.

The percentile rank chart under exhibits that 97% of the time the Worth to Gross sales ratio was greater that it’s now.

Valuation Percentile Rank (Koyfin)

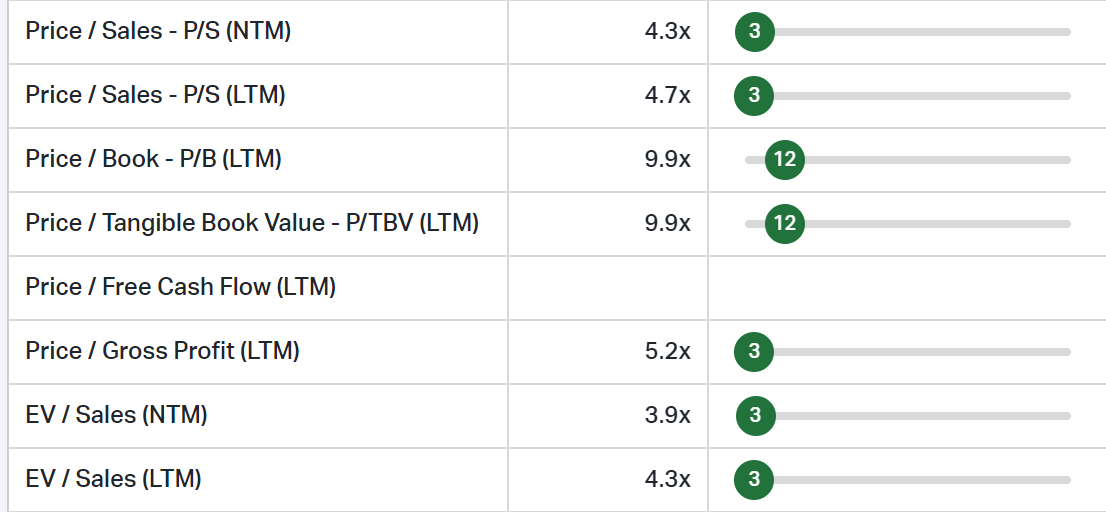

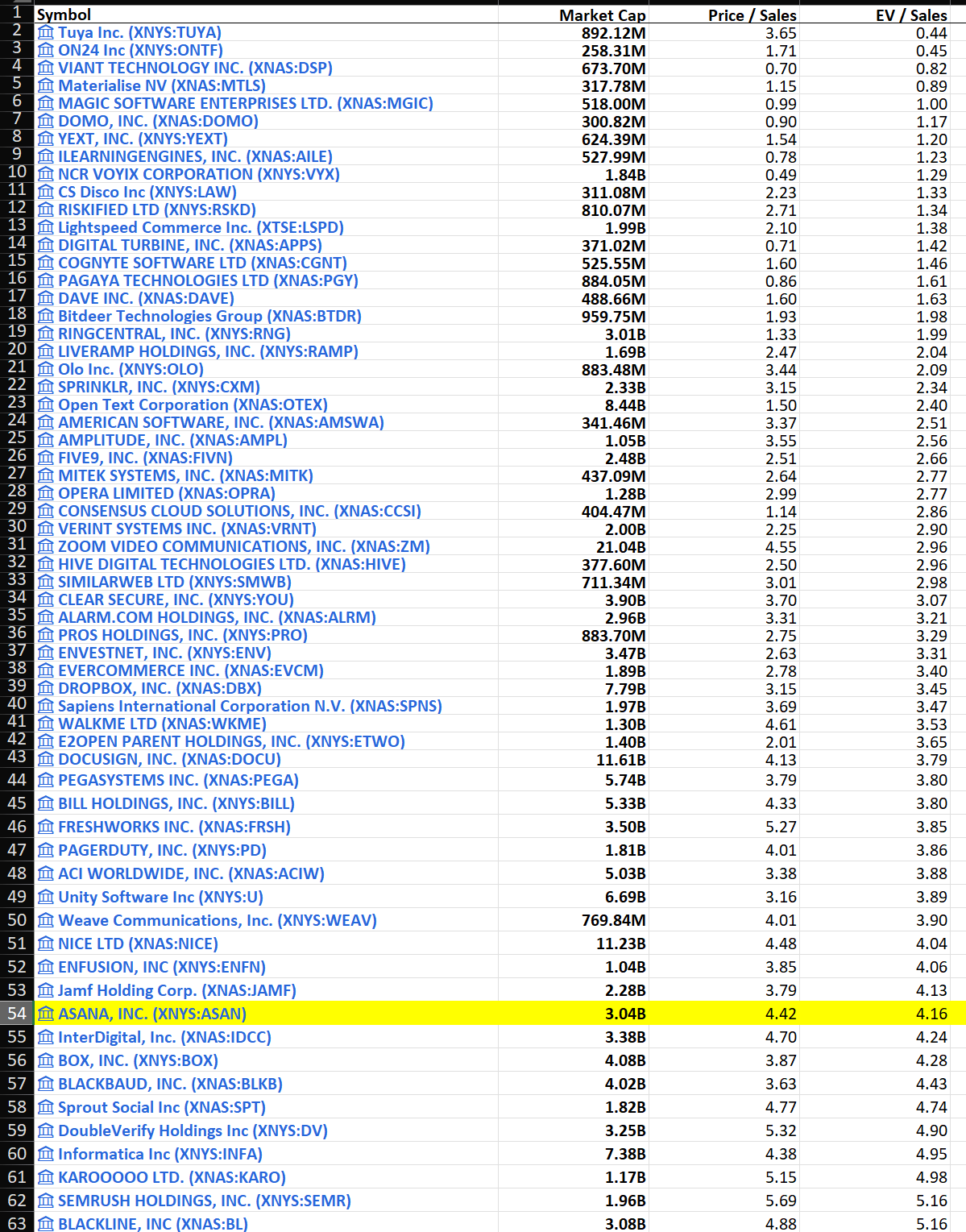

Could also be a extra essential query to reply can be to test if its valuation holds up when in comparison with its personal business. I took an export from In search of Alpha for all of the Utility Software program business parts and thought of solely shares with market caps above $250M and ended with a listing of 135 corporations. Asana ranks 55 (decrease than the median) for its Worth to Gross sales and if we attempt to leverage the energy of its stability sheet (It has additional cash than its complete debt) and have a look at its EV/Gross sales ratio the outcomes don’t change a lot (Rank 53). With 10% development charge this ratio might go decrease and there’s a good case to be made right here once more that the worst might be behind us.

Software program Utility Trade comps (SA)

Why this can be a Maintain?

I like the corporate, I’ve used its merchandise and I believe its a beautiful match for right now’s software program growth workflow wants. I’d like to be an investor within the firm however I would really like take a wait and watch strategy for the next causes –

1. Progress has stabilized and is forecasted to develop at low double digits however with out a timeline in direction of particular profitability it’s too early to be an investor

2. Earnings will present additional affirmation on the path of the corporate

3. Valuation is honest now however doesn’t supply a gorgeous reward from a threat perspective

4. The inventory has entered a consolidation section and I haven’t got to get in on the absolute backside. I want to see if the corporate is ready to exceed expectations from right here on which might propel the inventory greater after which revisit my thesis.

[ad_2]

2024-08-24 12:13:39

Source :https://seekingalpha.com/article/4716887-asana-the-worst-may-be-behind-us-q2-earnings-preview?source=feed_all_articles

{kind=link}

Discussion about this post