[ad_1]

Lina Moiseienko

Computer systems are silly.

They by no means did, don’t now, and won’t ever “suppose.”

All they’ll ever do is acknowledge and react to the distinction between electrical present being “on” or “off.” In machine language, that is expressed as “1” or “0.”

That is so even with AI.

Don’t take my phrase for that. Right here’s how ChatGPT 4o (the general public poster baby for AI) places it:

Whereas the conceptual and algorithmic foundations of AI contain complicated mathematical and statistical strategies, the implementation of those strategies depends on the binary computation capabilities of conventional laptop {hardware}. Thus, AI, in observe, is deeply rooted within the binary (ones and zeros) basis of classical computing programs.

The whole lot about as we speak’s computer systems is constructed to make these mixtures of 1 and 0 understandable, helpful, and fascinating to common people.

Programmers sometimes use high-level languages like C++ or Python. These use syntax that’s readily realized and utilized by people who select to review programming.

Beneath that’s meeting language. This interprets high-level language programming into 1s and 0s.

Numbers and letters every have particular binary (for mathematicians, that’s “base 2”) equivalents.

Numerically, we’re accustomed to base 10. Meaning we use ten digits, starting from 0 via 9. Then, we begin one other sequence; 10, 11, and many others.

Base 2 binary has solely 0 and 1. So its sequence is 0, 1, 10, 11, 100, 101, 110, 111, 1000, and many others.

In base 9, let’s imagine 6. In base 2, that’s equal to 110.

Each letter has a numerical “ASCI” code. (You could have seen this when you’ve ever gone between textual content and numbers in Excel.) The ASCI code for “E” is 69. In binary, that’s 01000101.

There are additionally binary equivalents for numerical codes that symbolize colours and sounds.

This implies clever computing, coaching on knowledge, and many others. are illusions.

People are doing the entire so-called laptop considering – and I actually imply ALL of it.

Right here’s ChatGPT 4o’s tackle this (i.e., itself):

Whereas AI is constructed upon subtle coding and algorithms, it lacks the acutely aware understanding and self-awareness that characterize human intelligence. AI programs are {powerful} instruments able to performing complicated duties and studying from knowledge, however they achieve this via statistical strategies and sample recognition slightly than true cognitive processing. The excellence between slim AI and the theoretical idea of normal AI highlights the present limitations and future aspirations throughout the subject.

So now, we understand what AI actually is. It means extra processing. It means extra velocity. It means higher output.

Finally, it’s the identical units of issues we’ve all the time accomplished with computer systems. The distinction is that AI means a lot, a lot, a lot, a lot, a lot, a lot, a lot, extra; and far, a lot, a lot, a lot, a lot, a lot, significantly better.

Consider it just like the distinction between a tiny black-and white circa-Nineteen Forties tv versus a recent big internet-capable high-definition medium, even perhaps like watching a film, say, on an Apple Imaginative and prescient Professional.

Photographs individuals and many others. shifting in visible settings with context-relevant sounds all come right down to the identical units of issues… human coded binary (1-0 or slightly on-off). However one is exponentially higher than the opposite.

- Now think about what it took to make an old-time Commodore 64 (when you can nonetheless discover one) show “Hey World” on an old-time TV display.

- Subsequent think about what it’ll take to get ChatGPT 4o to compose a poem, compose music, to put in writing a novel, to create sensible movies, to clarify your medical signs, to docs, to create an image, or to drive a automobile.

The latter requires two units of main advances.

It requires a spectacular quantity of extra coded instruction.

I get a headache even imagining what number of programmed if-then-and-or kind logic timber ChatGPT 4o would require. Take into account too what number of databases it must contact.

After which, attempt to think about how far more such work it takes to “prepare” fashions on knowledge and make computer systems imitate human output.

So secondly, we’d like unprecedentedly extra velocity… particularly if we wish solutions instantaneously, as a substitute of checking again in three weeks.

(And don’t anticipate the world to affected person ready for output. I bear in mind the early pre-broadband web. Response occasions I’d have thought-about nice within the Eighties would as we speak have me screaming and cursing.)

It’ll additionally imply bringing a significant portion of AI work down from the cloud. The brand new AI computer systems and telephones we hear about will course of plenty of the AI domestically… on the units.

This is a crucial change.

ChatGPT4o instructed me about seven benefits to device-based AI:

1. Privateness and safety: Knowledge stays on the machine, lowering the chance of privateness breaches or knowledge leaks related to cloud storage and processing.

2. Sooner Response Occasions: AI processes knowledge domestically, minimizing latency related to sending knowledge forwards and backwards to cloud servers. That is essential for functions requiring real-time responses, comparable to autonomous autos or medical units.

3. Offline functionality: Native AI can operate with out an web connection, making it appropriate for environments the place connectivity is restricted or unreliable.

4. Value Effectivity: By lowering reliance on cloud providers, organizations can probably save on cloud computing prices, particularly for functions that require steady or high-volume processing.

5. Scalability: Native AI will be scaled by upgrading {hardware} or software program domestically, with out counting on cloud infrastructure scalability, which can contain further prices and complexities.

6. Regulatory Compliance: Sure industries or areas might have regulatory necessities that prohibit using cloud providers or mandate knowledge localization. Native AI helps in complying with such laws.

7. Edge Computing: Native AI helps edge computing paradigms the place processing happens nearer to the info source or end-user machine, enhancing effectivity and lowering community site visitors.

So finally, AI isn’t actually about thought, intelligence or cognition. It’s about extra and higher.

And this units up a terrific development alternative for Dell Applied sciences, Inc. (NYSE:DELL).

Nevertheless a lot we love enjoying with instruments like ChatGPT now, and nevertheless a lot we admire what firms are doing as we speak with AI, not one of the {hardware} with which we work as we speak will suffice for for much longer.

For AI (far more processing, far more velocity and significantly better output) to really develop into a part of our world, I consider we’ll have to switch a lot of, maybe all, of as we speak’s {hardware}.

And as with the primary wave of private computerization, it might not be cheap to anticipate to get all we’ll want on day one.

We might have years, or many years price of successive upgrades till we attain maturity.

This implies we’re now poised at first of a generational new {hardware} cycle.

Ought to we name this secular development? Ought to we name this an occasion of extended cyclical development? Extra to the purpose… Who cares?

All we have to name it’s a heck of much more new enterprise and development for Dell than is mirrored in its circa-16 P/E.

That’s development investing!

However earlier than leaping in headfirst, now we have to grasp why DELL has such a modest P/E

There’s Baggage Right here

We are able to’t naively assume low P/E is bullish.

We are able to debate whether or not the market is completely “environment friendly” (educated). Nevertheless it’s not completely dumb.

We have to know why Dell’s P/E is low. And we’d like causes to consider it gained’t fall even decrease.

There’s excellent news: We all know the solutions.

For starters, Dell has had a checkered historical past.

Most notably, Founder/CEO Michael Dell was a part of a gaggle that accomplished a buyout of the corporate in 2013. In late 2016, Dell made an enormous acquisition of EMC. And in 2018, it once more grew to become a publicly traded firm.

That’s only a tiny pattern of all the various board battles, negotiations, discussions with exterior buyers, different transactions, product missteps, and many others. involving this firm.

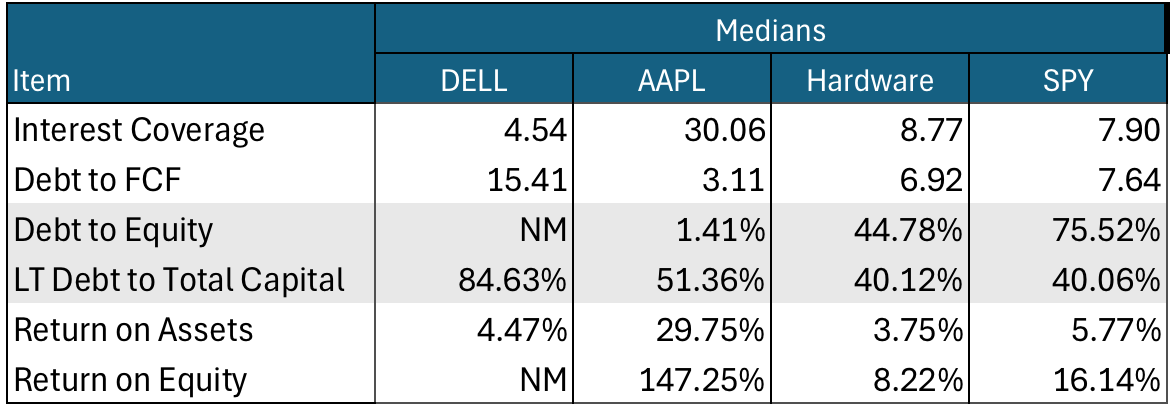

The machinations go away as we speak’s Dell with a set of fundamentals that pale compared to these of Apple (AAPL), one other massive {hardware} provider.

Creator’s computations and abstract from knowledge displayed in In search of Alpha Portfolios

(I choose medians since these aren’t impacted by wild distortions typically attributable to uncommon knowledge gadgets, even in massive firms that may dominate weighted averages.)

On July 8, 2024, I defined why I’m no fan of Apple’s company suite. However I do must tip my hat in a single respect…

Thus far, consultants, funding bankers, attorneys and accountants appear to have had a a lot much less impression on Apple. Dell, then again, appears to have been a house away from dwelling for a lot of such outsiders.

By now scorning such company maneuvers, I suppose I’m doing penance. (My early skilled years had been in legislation and managing a junk-bond mutual fund.) Higher late than by no means.

However even when we get previous Dell’s prior dependancy to heavy company stuff, there’s extra to deal with.

Take into account the product line for which Dell is greatest identified…private computer systems (together with laptops) and associated issues IT professionals use to attach them (to at least one one other and the cloud).

For a lot of my early profession, this was a scorching sizzling enterprise. Demand and development had been big as a lot of the world went transformed from no computer systems to having them.

And the early units had been fairly primitive (from as we speak’s vantage level). So, for a very long time, there was a number of cash to being made promoting new and improved units to present customers.

Dell wasn’t the one provider. However the pie was sufficiently big and rising briskly sufficient to feed a number of mouths.

Finally, although, Father Time outran the Know-how {Hardware}, Storage and Peripherals Trade.

New {hardware} choices currently have been incrementally higher than their predecessors. However they haven’t been radically higher.

So, consumers have develop into a lot slower to improve.

Not too long ago raised rates of interest and financial uncertainty and rising inventories additional dimmed demand for what Dell sells.

This was mirrored within the funding neighborhood’s disdain for Dell’s Could 30, 2024 earnings-guidance launch. The inventory’s responded with a 1-day 18% drop.

That’s sufficient negativity. No less than it’s prior to now.

As buyers, particularly when contemplating a development funding, we have to look ahead…

The Bull Case for DELL Is About AI – About Promoting “Extra” and “Higher”

Dell is introducing AI into key merchandise.

This isn’t a futuristic dream. It’s actual as we speak. And it’s very early in what will likely be a protracted development cycle.

Dell organizes itself round two segments.

Many people take care of the corporate via its Shopper Options Group (CSG). It sells desktop pcs, notebooks, and workstations. It additionally sells acquainted peripherals like docking stations, keyboards, mice, and webcams.

This calls to thoughts low-margin commodity-like merchandise devoid of any form of financial moat.

I don’t care in regards to the absence of a moat.

Moat is a horrible metaphor… one hundred pc of all moat-protected Medieval seats of energy didn’t survive, attributable to sieges, catapults, and many others. (And had any lasted into the 1900s, aerial bombardment would have killed them off.)

Companies should compete or die. And on condition that, CSG has what I actually wish to see, on sub-markets price preventing for.

DELL IR

So, if John Doe chooses to go on CheapJunkyPCs.com and purchase a cut-rate product, that’s wonderful. Dell gained’t battle exhausting for that buyer.

IT professionals are more likely to additionally work with Dell’s Infrastructure Options Group (ISG). Right here, Dell sells issues like high-performance servers, storage (the massive stuff, not the form of gizmos peculiar people purchase), and virtualization software program.

The latter creates the expertise of engaged on a computer, for instance. However there is no such thing as a actual computer. It’s within the cloud. If your organization is already doing AI, it’s doubtless utilizing the form of servers, and many others. ISG sells.

Listed here are Dell’s market shares in key ISG product classes.

DELL IR DELL IR

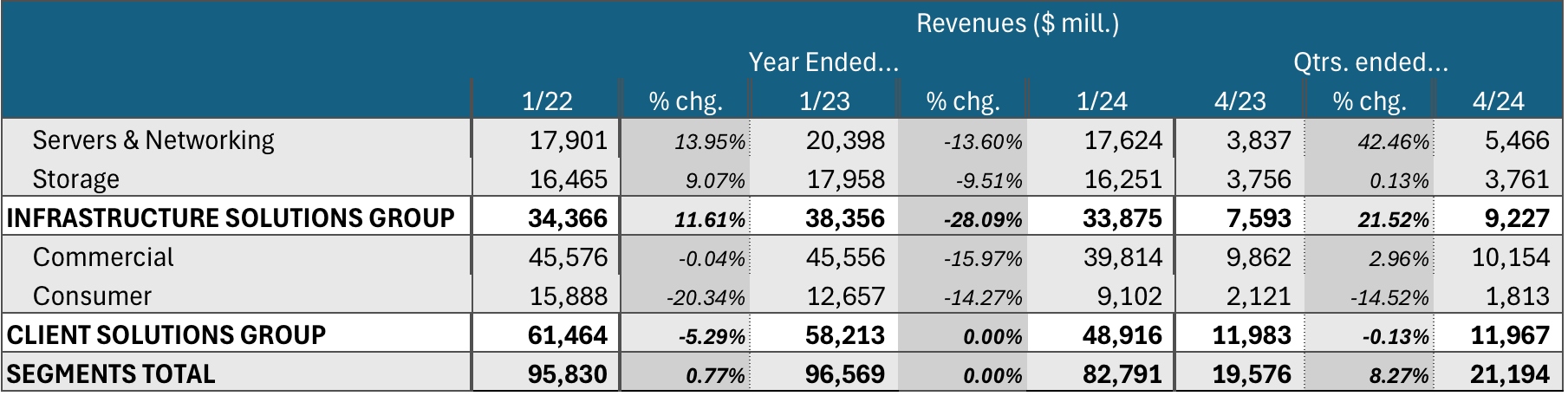

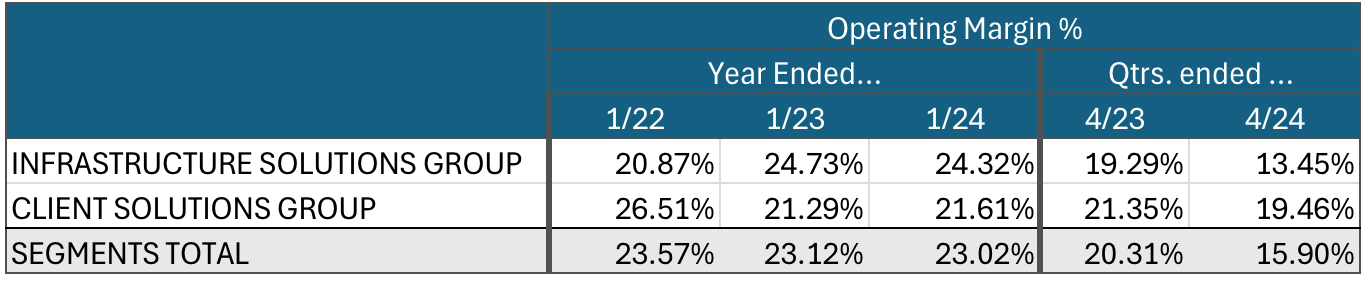

Right here’s how the segments contributed to Revenues and working Income:

Creator Compilation and Calculations primarily based on knowledge from newest 10-Okay and 10-Q Creator Compilation and Calculations primarily based on knowledge from newest 10-Okay and 10-Q Creator Compilation and Calculations primarily based on knowledge from newest 10-Okay and 10-Q

Not too long ago, I identified imbalances in Alphabet (GOOGL) and Apple (AAPL). They’re overwhelmingly dominated by one factor…. (promoting and iPhone, respectively).

We see above that Dell is extra moderately balanced throughout ISG and CSG.

Each teams have been weak currently. The economic system and the so-far uninspiring cycle hit each. The Shopper portion of CSG appears to have been actually taking it on the chin.

However once more, I don’t care in regards to the previous. From our vantage level within the unhealthy a part of a cycle, the long run naturally seems higher.

Right here’s Dell’s view of an AI-driven future.

DELL IR

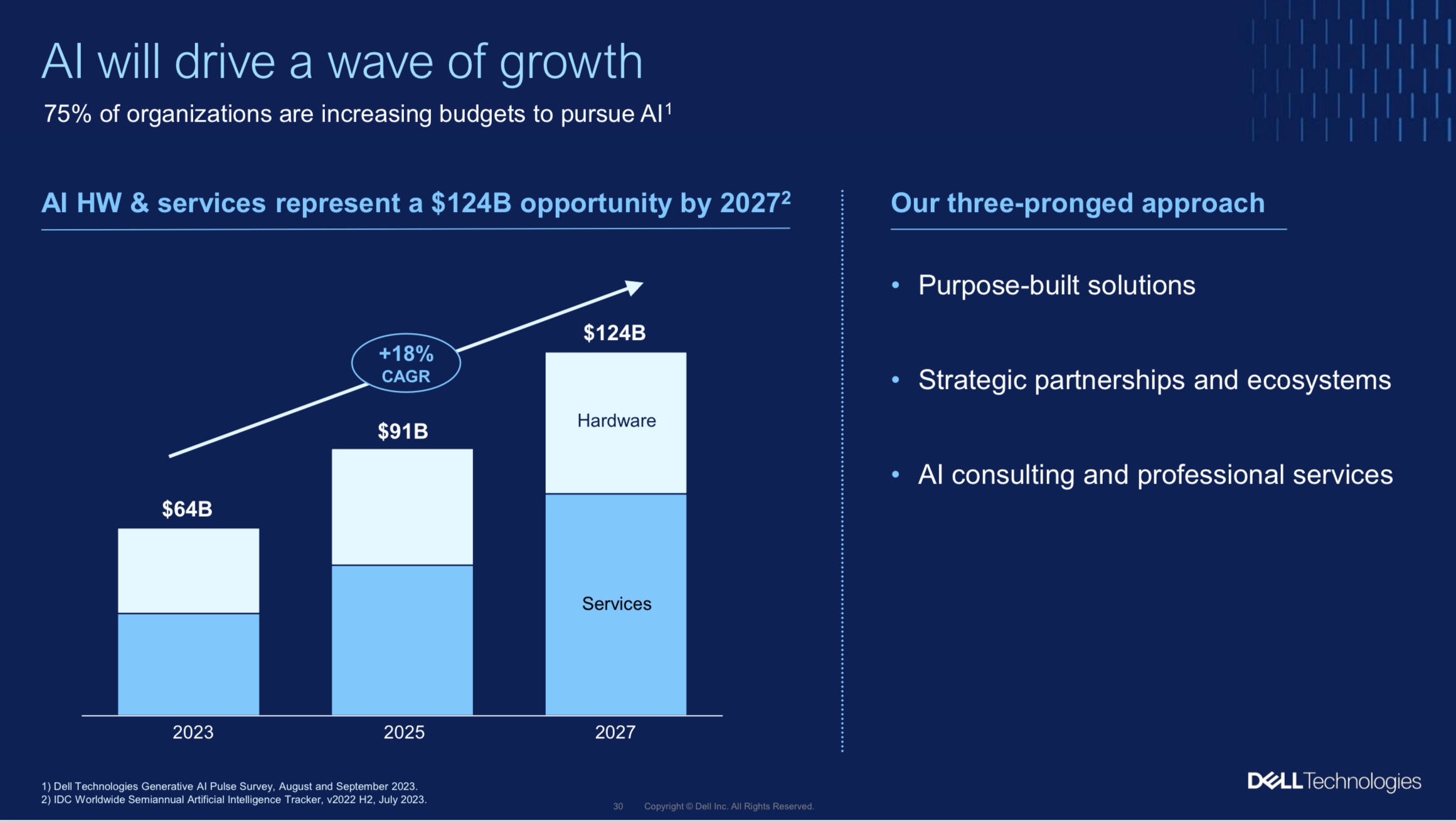

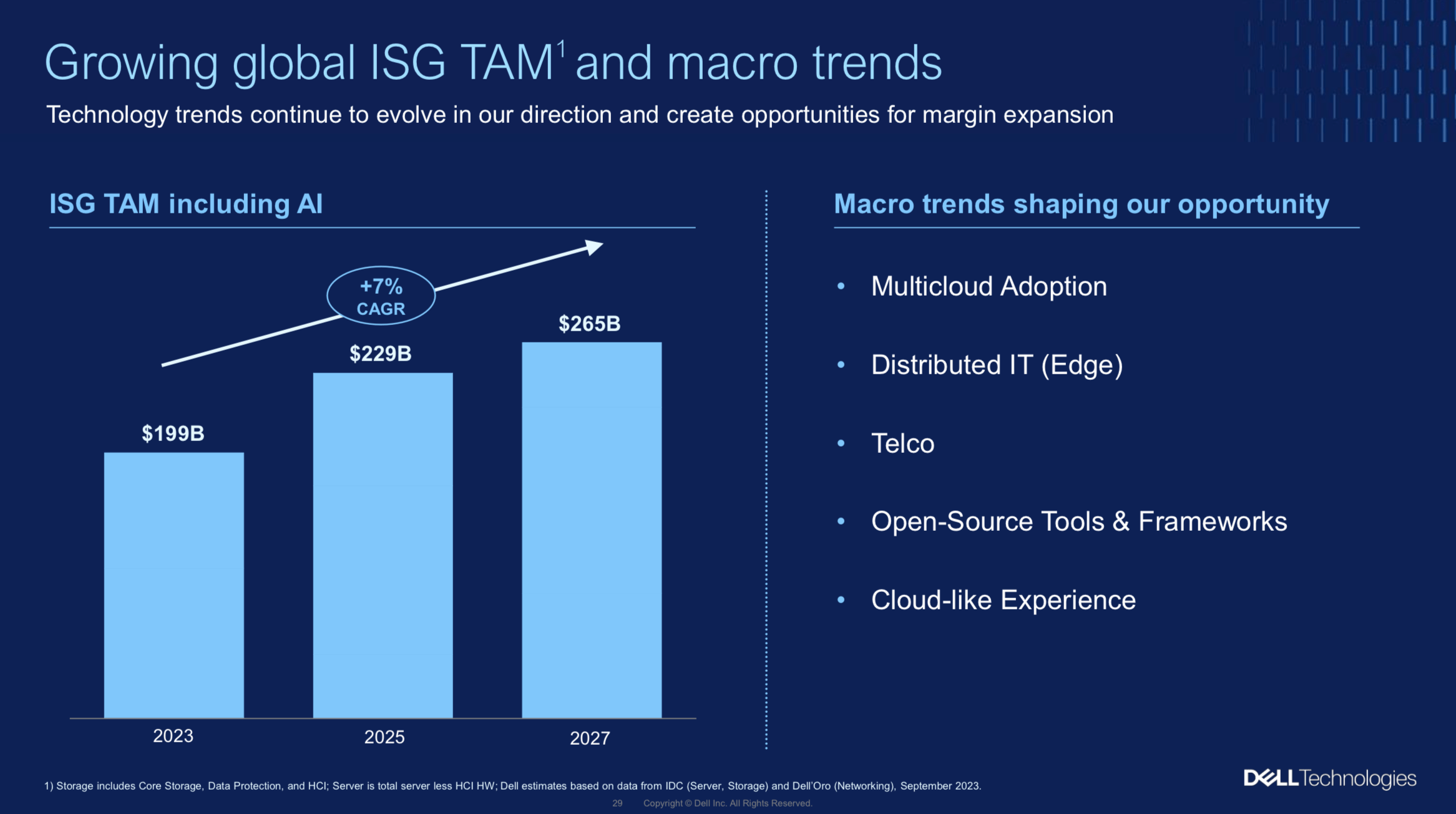

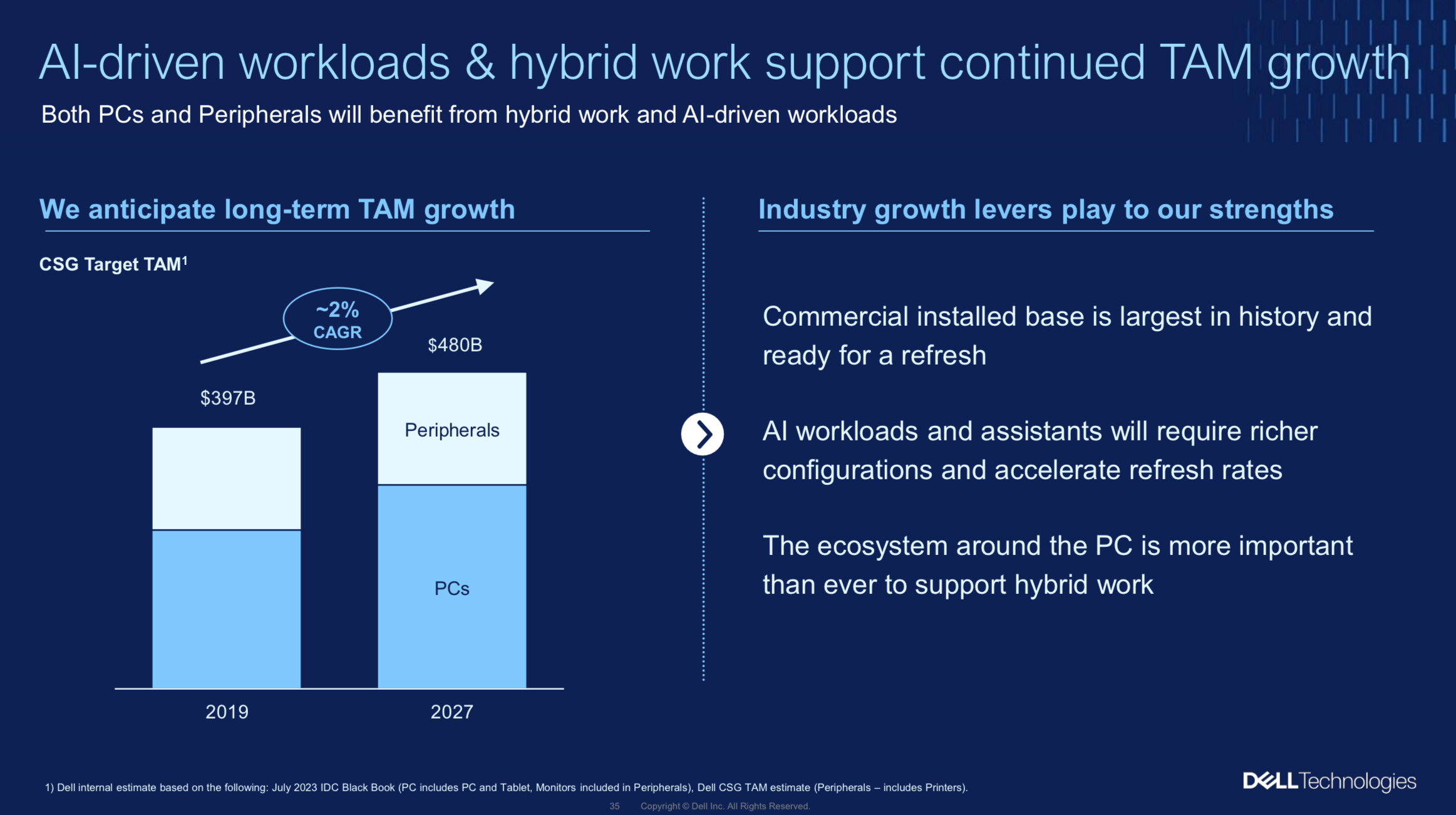

The subsequent two pictures present Dell’s expectations concerning AI’s affect on section TAM (Complete Addressable Market).

Right here it’s for ISG.

DELL IR

And right here’s it’s CSG. View.

DELL IR

Discover what the final two pictures don’t declare.

We’re not being overpowered by dazzling projections of stupendous near-term development.

That’s wonderful. Tech typically and AI significantly have hyped extra boldly than something I’ve seen in a few years.

I’d be bothered by DELL’s down-to-earth projections if the inventory’s P/E had been, say, 75. Nevertheless it’s not.

DELL can afford to current a extra measured view. Keep in mind, its inventory sells for under 16.16 occasions the consensus next-year earnings estimate.

We are able to take a longer-term view. And we’d like not stretch “longer” into the very distant future.

As famous, buyers hated the latest quarter. However that doesn’t change the target actuality that Dell’s long-term future has already began to take form.

DELL IR

Take a look at the next tables.

Analyst Compilation primarily based on Knowledge from In search of Alpha Earnings and Financials Displays Analyst Compilation primarily based on Knowledge from In search of Alpha Earnings and Financials Displays

The foregoing suggests Dell is within the technique of passing via an inflection level between falling and rising outcomes.

Threat

The CrowdStrike (CRWD) replace bug that not too long ago took down so many Microsoft-based computer systems world-wide might develop into a problem.

Microsoft (MSFT) wasn’t instantly at fault. And Dell had no position in any respect within the outage.

Dell sells {hardware} that runs on Microsoft working programs. So, if MSFT loses market share, it will harm Dell.

That would occur if customers take growing umbrage at MSFT’s reputed safety weaknesses and extra reliance on an out of doors vendor (i.e., CRWD) to deal with this.

Microsoft is simply too nicely established to lose its massive gorilla standing.

However I’ve to acknowledge the likelihood it might lose some floor. That may impression different companies, like Dell, that function inside MSFT’s orbit.

A extremely massive unknown right here is strictly how lengthy it’ll take for the massive bucks to start out displaying up in Dell’s earnings. Perhaps we’ll begin seeing a major quantity earlier than this 12 months ends. Perhaps we’ll want a slower ramp up.

Critical development buyers focus primarily on the a lot brighter future, the vacation spot.

However for what it’s price, many buyers, even many who suppose they’re development buyers, care primarily in regards to the path.

Living proof – the beating DELL inventory took after the final convention name. As steerage continues to jockey with actuality, such an episode might be repeated.

In the meantime, Dell is extra debt-heavy than different large-cap big-name AI performs.

Regardless of that, Dell is money stream optimistic. It’s paying a dividend. And it buys again inventory.

However stronger steadiness sheets are extra comforting. You ever know what is going to occur sooner or later.

Valuation

DELL shares are attractively valued.

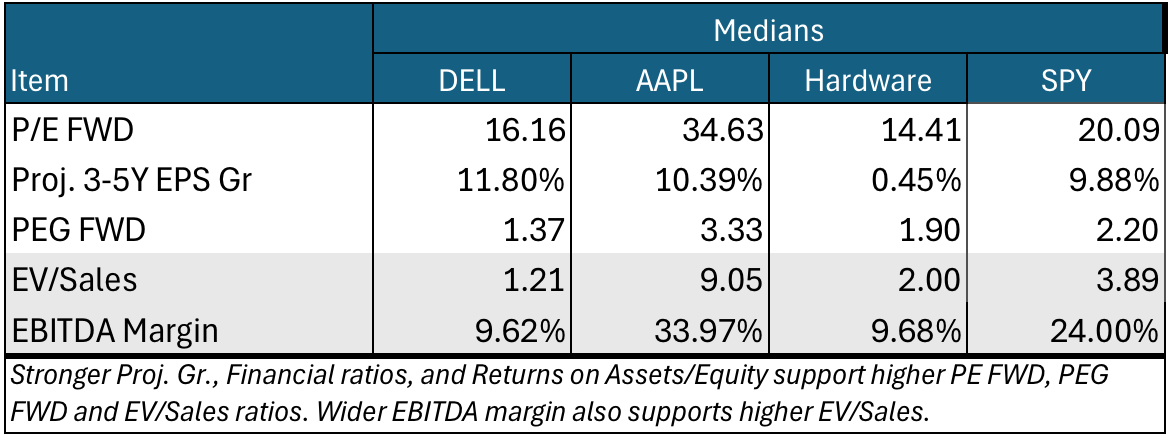

Creator’s computations and abstract from knowledge displayed in In search of Alpha Portfolios

Based mostly on EV/Gross sales, this inventory is cut price priced. The ratio, for DELL, is nicely beneath medians for SPY and the Trade. Dell’s EV/Gross sales ratio is way beneath that of AAPL.

DELL’s EBITDA Margin, related in figuring out how excessive or low an EV/Gross sales ratio ought to be, shouldn’t be nice. However comparatively talking, it’s not practically low sufficient to justify the inventory’s meager EV/Gross sales ratio.

DELL’s P/E FWD is about on par with the median for the lackluster business. However the firm’s Proj. 3-5Y EPS Gr is on par with that of AAPL and a bit above the SPY median. So DELL is cut price priced in comparison with these benchmarks.

The Trade P/E FWD is a tad decrease. However analysts have a lot decrease long-term EPS development for a lot of firms in that group.

The valuation we see for DELL is a hard-to-resist rarity within the AI world.

What to do About DELL Inventory

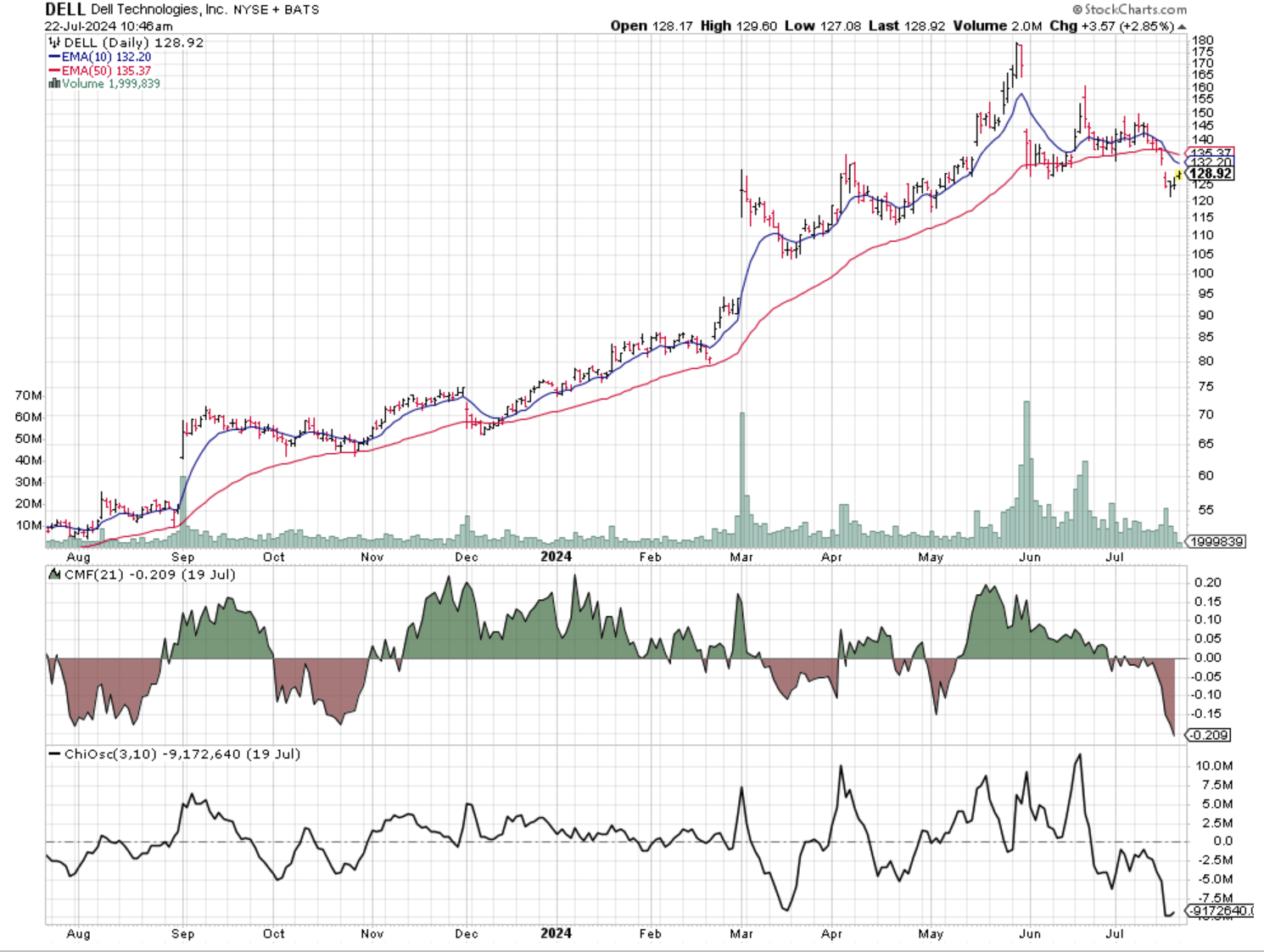

Whereas DELL’s valuation seems good, its worth chart is middling.

StockCharts.com

The value not too long ago crossed beneath the 10-day exponential shifting common (EMA). And the 10-day EMA not too long ago dropped beneath the lackluster 50-day EMA.

There’s no encouragement from the Chaikin Cash Circulation (CMF) or the Chaikin Oscillator (CO). Each measure which occasion to trades is extra motivated. CMF does it for institutional buyers. CO does it for the market generally.

Each indicators are unfavorable. That tells us sellers are extra motivated. That’s a headwind in opposition to shares as they attempt to advance.

If I had been a pure technical analyst, I’d say to attend on DELL. However I’m not. I exploit charts so as to add context to the current, not predict the long run.

I get Mr. Market’s lack of rapid enthusiasm. Many are nonetheless licking wounds incurred within the wake of DELL’s final earnings launch and disappointing near-term steerage.

However I don’t base my funding case on that. As an alternative, it is motivated by the lengthy product upcycle at which DELL now stands on the edge.

Shareholders might not profit subsequent week or subsequent month. However development buyers ought not bypass a chance to plant a stake at as we speak’s valuation.

As I’ve mentioned earlier than, my funding stance relies upon primarily on whether or not I believe a inventory will likely be higher than, according to, or worse than the market.

Right here’s how I apply that to the In search of Alpha ranking system:

- “Robust Purchase” means I see the inventory as being higher than the market, and I’m bullish in regards to the course of the market.

- “Purchase” means I see the inventory as being higher than the market, however am not assured in regards to the market’s near-term course.

- “Maintain” means I see the inventory as shifting according to the market.

- “Promote” means I see the inventory as being worse than the market, however am not assured in regards to the market’s near-term course.

- “Robust Promote” means I see the inventory as being worse than the market, and I’m bearish in regards to the course of the market.

Based mostly on this scale, I’m ranking DELL as a “Purchase.”

[ad_2]

2024-07-24 04:12:47

Source :https://seekingalpha.com/article/4706011-ai-is-ultimately-about-more-and-better-and-that-makes-a-powerful-growth-case-for-dell?source=feed_all_articles

{kind=link}

Discussion about this post