[ad_1]

Sundry Images

I gave Keysight Applied sciences (NYSE:KEYS) inventory a ‘Sturdy Purchase’ ranking in my earlier article revealed in July 2023, highlighting the corporate’s potential to capitalize on 5G and software program options. The corporate launched their Q3 outcomes on August 20th. The brand new order development appears to have bottomed out through the quarter. I estimate the corporate will return to constructive income development by FY25. I reiterate a ‘Sturdy Purchase’ ranking with a one-year value goal of $180 per share.

Order Restoration Amid Weak Finish-Market Calls for

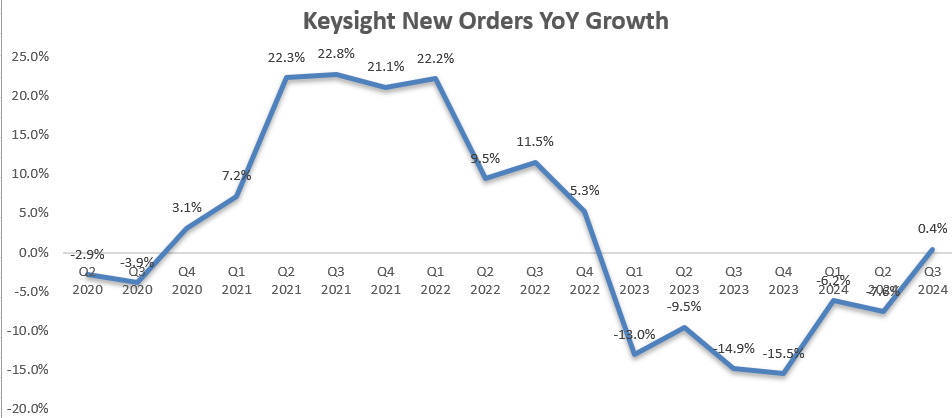

As depicted within the chart beneath, Keysight’s new orders grew by 0.4% year-over-year in Q3. It seems to me that the order development has already emerged from the underside of the cycle.

Keysight Quarterly Earnings

The order development is pushed by a number of elements:

- Throughout the quarter, the Business Communications enterprise delivered low-double-digit order development. As communicated over the earnings name, conventional wi-fi enterprise stays to be weak as telco corporations are decreasing investments in conventional communication infrastructure. Then again, wireline’s order development was tremendous sturdy, propelled by AI investments from hyperscalers and knowledge middle operators. As mentioned in my initiation report, Keysight’s measurement merchandise are wildly utilized in business communication and knowledge facilities. As such, I’m not stunned to see their enterprise benefiting from the speedy AI investments.

- Keysight has been investing in their very own R&D assets for key functions together with GPU servers, AI workload emulation and efficiency benchmarking, as highlighted over the decision. For example, Keysight launched their AI knowledge middle check platform, able to emulating high-scale AI workloads with measurement constancy.

- Within the aerospace, protection and authorities section, each income and orders declined year-over-year. The administration attributed the weak spot to the delay of U.S. finances approval. I consider the weak spot is non permanent, as authorities spending is extra prone to proceed sooner or later. I anticipate the enterprise will begin to recuperate within the coming quarters.

Progress in Software program and Providers

As mentioned in my initiation report, Keysight has been rising their software program and repair enterprise, aiming to scale back the earnings volatility for the agency. At present, software program and companies characterize round 39% of whole income, and they’re rising sooner than the corporate’s general fee.

On March 28, 2024, Keysight introduced to accumulate Spirent Communications for £1,158 million (US$ $1,463 million). Spirent is a number one world supplier of automated check and assurance options for networks, cybersecurity, and positioning. I believe the deal aligns nicely with Keysight’s acquisition technique, and Spirent’s options and software program can probably improve Keysight’s power within the 5G, SD-WAN, Cloud and autonomous autos markets. Spirent’s {hardware} and software program options will be totally built-in into Keysight’s present software program and companies options, in my opinion.

Outlook and Valuation

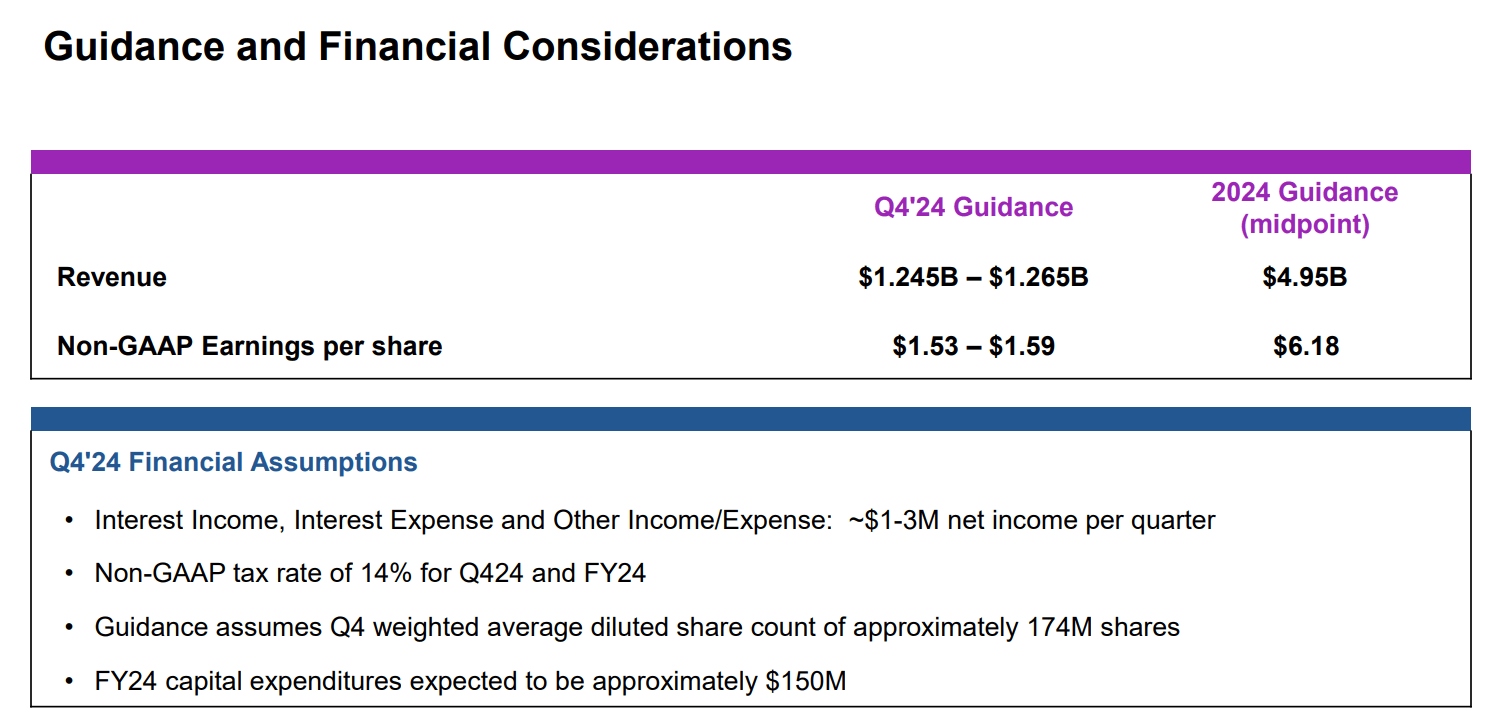

Keysight is guiding for round 9.3% decline in income for FY24, as detailed within the chart beneath. Their steerage assumes a gradual restoration within the communication market through the second half of FY24 and into FY25.

Keysight Investor Presentation

For FY24’s development, I break down the expansion into three main end-markets:

- Aerospace, Protection and Authorities: As mentioned beforehand, the market was weak in Q3 because of the delay in authorities tasks. As illustrated within the desk beneath, the discretionary portion of the federal finances is anticipated to develop by 4.5% in 2024. Nevertheless, because of the delay, I anticipate the section income will develop by 3% in FY24.

The Congressional Price range Workplace

- Business Communications: Conventional telecom funding is extra prone to face structural challenges within the close to future in my opinion; nonetheless, new development areas equivalent to knowledge middle and AI will positively impression Keysight. I calculate Keysight’s income in business communications will decline by 5% in FY24.

- Digital Industrial: I anticipate the weak spot will stay within the coming quarters, and the section income will decline by 20% in FY24.

Because of this, I calculate Keysight’s general income will decline by 8% in FY24. For the expansion from FY25 onwards, I assume a gradual restoration within the end-markets, and Keysight’s development will revert to historic common: Aerospace, 5% development in Protection and Authorities; 7% in business communications; and 5% in digital industrial. Thus, the general natural development is anticipated to be 6%.

I mannequin 20bps annual margin enlargement, assuming:

- 15bps margin enchancment from gross earnings on account of new merchandise launch, combine in direction of software program.

- 10bps working leverage from SG&A

- As the corporate invests in AI expertise, I anticipate the elevated R&D investments will create a 5bps headwind for margin enlargement.

With these parameters, the DCF abstract:

Keysight DCF

The free money circulation from fairness is calculated as follows:

Keysight DCF

The price of fairness is calculated to be 13.6% assuming: risk-free fee 3.8% ((US 10Y Treasury)); beta 1.4 (SA); fairness threat premium 7%. With these assumptions, I calculate the one-year goal value of Keysight’s inventory to be $180 per share.

Key Dangers

Throughout the earnings name, there have been a number of questions concerning the weak spot within the automotive market, notably within the EV market. As Keysight offers testing tools for the automotive market, their enterprise can be affected by weak calls for. It sounds just like the administration lacks visibilities on the timing of the restoration within the broader automotive market.

Conclusion

The restoration in new order development is sort of encouraging, indicating a gradual restoration within the end-markets. I favor the corporate’s investments in AI and knowledge middle testing, in addition to software program and companies. I reiterate a ‘Sturdy Purchase’ ranking with a one-year value goal of $180 per share.

[ad_2]

2024-08-21 13:45:42

Source :https://seekingalpha.com/article/4716191-keysight-q3-order-recovery-is-encouraging?source=feed_all_articles

{kind=link}

Discussion about this post