[ad_1]

Summary Aerial Artwork/DigitalVision by way of Getty Pictures

Lyft (NASDAQ:LYFT) inventory offered off huge after reporting its Q2 2024 outcomes and outlook, pulling again over 17%, regardless of reaching its first-ever quarter of GAAP profitability. I reiterate my purchase ranking on Lyft, as I feel Lyft is now higher positioned to outperform within the second half of FY2024, as we’ve gotten the negatives out of the best way. The inventory offered off after earnings as buyers panicked as a consequence of 1) a slight miss on gross bookings, coming in at a 17% enhance year-over-year to $4.02 billion versus consensus of $4.07 billion and a pair of) 3Q24 gentle steering of gross bookings within the vary of $4 billion- $4.1 billion versus estimates of $4.14 billion and adjusted EBITDA of $90 million – $95 million versus estimates of $104 million. What we realized this quarter was that my constructive outlook proposed again in early Could performed out when it comes to boosted rides as a consequence of buyer obsession-based initiatives and decrease web loss as a consequence of cost-cutting efforts, however it was not sufficient to offset the 25% decline in Primetime.

I feel Lyft’s gentle information for Q3 is as a result of administration is preemptively pricing in headwinds from Primetime that might spill into the following quarter. I count on the brand new Worth Lock initiative to counteract the Primetime headwinds as 3Q coincides with the summer season journey season, again to high school, and again to work. Moreover, the double-digit decline in Primetime, although not very best within the brief time period, ought to assist with rider retention and conversion in the long term and translate to share acquire for Lyft in opposition to competitor Uber (UBER).

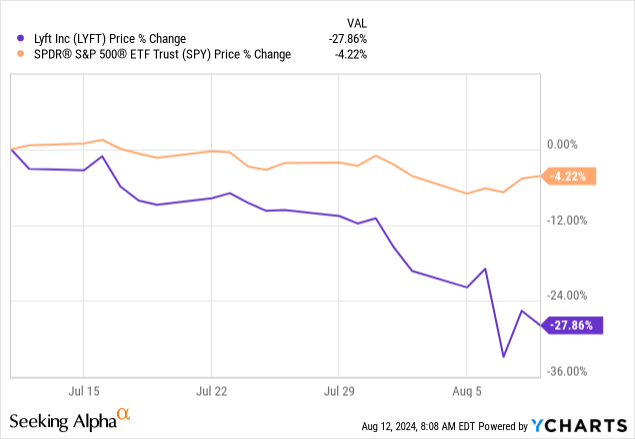

I proceed to be optimistic about Lyft’s “go-to-market technique beneath Risher will present extra upside in 2024,” as per my final funding thesis. Administration’s “buyer obsession drives worthwhile progress” motto has been profitable, particularly by means of initiatives like Girls+ Join, on-time pickup guarantees, and many others. I feel the negatives on the conservative steering have been priced in. As seen under, Lyft is down ~28% in opposition to the S&P500, down ~4% on the one-month chart. I imagine the inventory affords a small window for buyers to leap in after the pullback, as I see restricted draw back danger from right here and count on Lyft to be higher positioned after its disappointing Q3 steering to beat estimates subsequent quarter.

YCharts

Monetary Breakdown & Tailwinds Forward

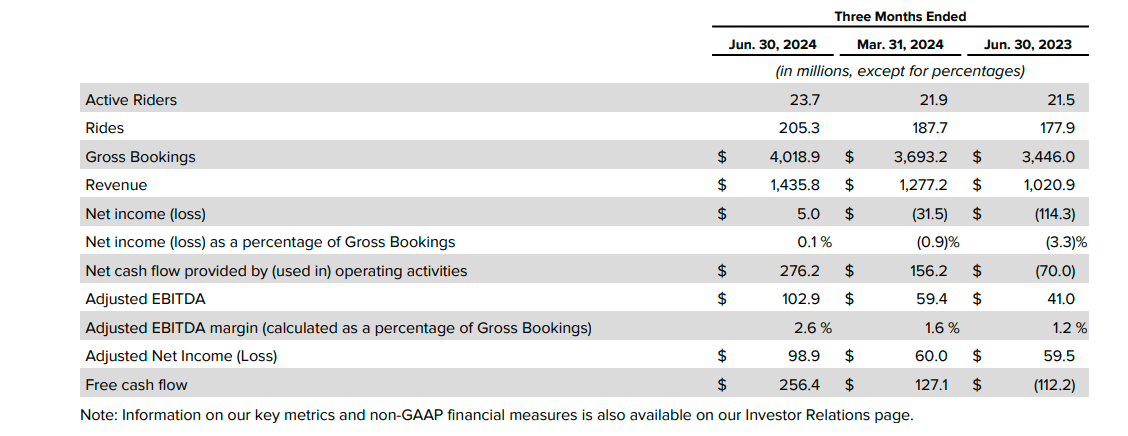

Lyft had a good quarter throughout the board, aside from the gross reserving miss and softer steering. Income got here in at $1.4 billion and was up 41% from a yr in the past quarter at $1.02 billion. I foresaw “administration’s self-discipline with cost-cutting measures will repay in decrease web loss,” and this quarter’s web revenue got here at $5 million and was 0.1% of gross bookings, whereas the corporate reported a web lack of $114.3 million and was 3.3% of gross bookings in a yr in the past quarter. Adjusted EBITDA got here in at $102.9 million, considerably larger from a yr in the past quarter at $41 million. Free money circulate got here in at $256.4 million, additionally larger yr over yr at a lack of $112.2 million.

In line with my expectations, energetic riders reached an all-time excessive of 23.7 million this quarter, up 10% yr over yr from 21.5 million. Rides reached a report of 205 million, 15% up from a yr in the past quarter’s 177.9 million. This was primarily as a consequence of driver hours additionally hitting an all-time excessive since 2019; I feel that is partly as a result of Girls+ Join initiative taking part in out. New drivers have been the best quantity the corporate had in any quarter since 2019, with over 34% extra ladies and nonbinary drivers yr over yr. I feel that is one occasion the place Lyft is exhibiting dedication to its buyer obsession, and I imagine the numbers inform us that it is working, though this isn’t but being mirrored within the gross bookings steering.

Lyft 2Q24 incomes outcomes

Initiating “Worth Lock”: Let the pricing wars proceed

Lyft acknowledges that “Primetime,” also called Uber’s “surge pricing,” will at all times be a part of its enterprise. For context, that is an occasion the place costs grow to be larger as a consequence of heightened buyer demand or decrease driver availability. So, to be extra reasonably priced than its largest competitor, Uber, particularly amidst the present financial headwinds, Lyft CEO Risher mentioned the corporate would “open a can of whoop-ass on Primetime” by means of its new Worth Lock initiative. The latter permits riders, particularly on a regular basis commuters, to join a month-to-month subscription that locks in a selected value for a set time and a route. I imagine this can be a great way for the corporate to match provide and demand. This quarter’s common Primetime decreased 25% year-over-year, and administration is forecasting for additional decline subsequent quarter. I feel my earlier funding thesis on Lyft fell by means of as a result of the positives of buyer obsession-centered initiatives weren’t capable of offset the decrease Primetime. I feel there will probably be restricted draw back from the Primetime headwind within the second half as administration has factored for this headwind in its outlook and buyers have factored it into the inventory value. I count on that what’s now a near-term ache will flip right into a flex for Lyft in FY25 and allow the corporate to attain higher conversion charges. For instance, the markets that witnessed the steepest decline in Primetime (Phoenix, Baltimore, Orlando) confirmed higher enchancment in conversion charges than in different markets.

As an underdog within the ride-hailing enterprise, I imagine Lyft is doing a superb job of reaching profitability with out taking it out of the shopper’s pockets. I imagine this places them in a greater place to maintain up with Uber, which has additionally been eager to extend affordability by means of cheaper choices and reductions. Administration realizes that “dependable pricing is especially necessary to them [customers] as a result of they know what their journey ought to price and hate it when costs change,” and I imagine this buyer obsession mindset is what differentiates Lyft from the peer group. Administration desires to take one factor clients hate, Primetime, and switch it into a brand new promoting level by means of Worth Lock.

Lyft Media as a New leg for progress

The section was introduced in 2022 and is taken into account the promoting leg of the enterprise. Lyft is monetizing the advert enterprise by means of a number of shops: Lyft Halo (rooftop screens), Lyft Tablets, Lyft Bikes, Lyft Skins, and the newest addition, Lyft in App, which makes use of customized focusing on, attention-grabbing codecs, and measurable outcomes.

Lyft Media income grew by round 70% year-over-year this quarter. This got here as much less spectacular than final quarter, which had a 250% enhance yr over yr. I imagine what we’re seeing is the macro-uncertainty and headwinds with the roaming worry of a recession. Final quarter, Lyft added new clients, comparable to Zillow and Mastercard, in addition to Nielsen and Oracle Promoting, as new companions for focusing on functions. This quarter, the corporate signed offers with 44 new manufacturers, comparable to T-Cell, and resigned with Amazon, Constancy, and NBCUniversal. Lyft advert movies, a brand new addition to the media section, generated over “10 instances the advert business’s typical click-through charge” and campaigns seven instances “the influence relative to the norm, on-brand notion and buy intent” final quarter. The in-app video advertisements “proceed to drive curiosity from manufacturers to energy this progress,” with income rising over ten instances yr over yr. This quarter’s new main companions embody Google marketing campaign supervisor, which, I imagine, is Lyft’s means of critically contemplating the media section as the brand new leg of progress. I feel the advert enterprise could possibly be extra profitable for Lyft and the broader peer group as soon as macro uncertainty eases in 2025.

What might go unsuitable?

Macro uncertainty in North America might weigh on shopper discretionary spending and, by extension, energetic rides, making it extra seemingly for riders to decide out of taking a Lyft or Uber for cheaper types of transport. Uber’s regional diversification turns out to be useful to assist offset the macro uncertainty going through North America specifically. Lyft would not have that further leg to face on.

I feel Lyft is specializing in consolidating its market share within the U.S. and Canada extra, and I do not assume Lyft will want a world presence to drive near-term outperformance. The corporate is already making large achievements within the Canadian market, the place rider and driver obsession is obvious. Lyft is in 5 of the biggest cities in Canada and round 13 smaller ones. Canada journey got here in double what they have been in a yr in the past quarter, making Toronto their eighth largest market. Administration believes this opens alternatives for Lyft outdoors the U.S. Lyft is taking its attain in North America critically, which, together with all its new initiatives, offers it a near-term edge over Uber.

Valuation

In line with knowledge from Refinitiv, Lyft’s value/earnings ratio for C2024 is 13.5, considerably decrease than the peer group common of 41.2. The inventory’s EV/Gross sales ratio can be decrease than the peer group common and considerably decrease than its largest competitor within the ride-hailing business, Uber. In my view, Lyft is undervalued for what I estimate the inventory’s near-to-mid-term worth to be, and I feel there’s extra upside for Lyft than the market is pricing in at present ranges.

Market sentiment on Lyft could possibly be extra constructive. The present median PT is $15, revised down from the median of $18 in Could and $19 all through June and July. The present imply PT is $15.5, once more revised down from a imply of $18.4 in Could, $19.2 in June, and $18.9 in July. This isn’t a superb look. Traders are reflecting a less-than-optimistic sentiment, as solely ~7% of Road Analysts give the inventory a powerful purchase, and 20.5% give it a purchase. The vast majority of Road Analysts, making up over 65%, give the inventory a maintain, and round 2% give it a promote. This tells me that negatives from gentle steering are being priced in, and I count on the inventory to rebound earlier than subsequent quarter.

The corporate held its Investor Day occasion in June final quarter, confirming my constructive outlook on profitability and the customer-obsessed Lyft strategy. This earnings name got here in to say that Lyft is “effectively forward of schedule” and mentioned administration is on monitor to “generate constructive free money circulate for the total yr, and given our robust progress within the first half of 2024 and our elevated visibility, we now count on that greater than 90% of adjusted EBITDA will convert to free money circulate for the total yr 2024.” In my view, Lyft will proceed to enhance its financials and develop its home buyer base within the second half of the yr.

What’s subsequent?

With the worry of Robotaxis taking up the ride-hailing business, everybody desires a chunk of the cake. Lyft isn’t any completely different; the corporate believes that AVs pose an enormous alternative as a consequence of its community of over 40 million riders a yr in Canada and the US and round 2 million rides a day. The mentioned community is why Lyft succeeded in Las Vegas with its AV penetration and has secured over 130,000 AV rides to date. The corporate has had a “Flexdrive subsidiary” for years and now has round 15,000 automobiles working on-line. Truthfully, except for administration’s “energetic conversations” with companions, I don’t count on this to be a part of Lyft’s worthwhile endeavors within the close to future. I additionally don’t assume it causes any near-term danger to Lyft’s market share. I feel it’s going to be years earlier than the world takes automotive technique of transportation critically within the ridesharing business.

I’m additionally waiting for the development with Primetime and anticipating conversion charges to indicate up in FY25. I feel the second half of the yr will assist assess how profitable the brand new Worth Lock initiative will probably be.

[ad_2]

2024-08-14 07:16:26

Source :https://seekingalpha.com/article/4714326-lyft-some-near-term-heavy-lifting-for-longer-term-growth?source=feed_all_articles

{kind=link}

Discussion about this post