[ad_1]

Trevor Williams

Corsair Gaming, Inc. (NASDAQ:CRSR) reported the corporate’s Q2 earnings on the 1st of August, posting a pointy beforehand communicated income decline and weakening profitability pushed once more by weak point in element gross sales. The corporate additionally revised its 2024 monetary outlook downwards notably, and with the weak point coming in even worse than anticipated, Corsair’s inventory dove -19% to the outcomes regardless of the revenues being preliminarily communicated.

I beforehand printed an article, discussing Corsair’s element weak point in Q1, titled: “Corsair Gaming: Q1 Weak point Anticipated To Subside”. On the time, Corsair communicated to consider in a sequential restoration, and with the inventory being practically pretty valued in my view on the time, I rated the inventory at a Maintain score. For the reason that article was printed, Corsair’s inventory has misplaced -45% of its worth whereas the S&P 500 has returned a tiny 1% with the extremely weak Q2 outcomes.

My Ranking Historical past on CRSR (In search of Alpha)

Q2 Report: Even Bleaker Element Gross sales

After warning the market with preliminary revenues a few weeks previous to the quarterly report, Corsair reported the ultimate, extremely weak Q2 outcomes on the 1st of August. Revenues got here in at $261.3 million at a large year-on-year decline of -19.7%, down from the expressed Q1 softness of only a -4.7% year-on-year decline, lacking prior Wall Avenue estimates by $29 million in revenues and by $0.14 within the reported adjusted EPS of -$0.07.

Corsair’s Gaming Pheriperals phase once more had nice momentum, rising by 19.7% in gross sales into $94.2 million and posting a formidable 5.5 share level gross margin enlargement, once more outpacing no less than Logitech’s (LOGI) development of 11.7% within the quarter.

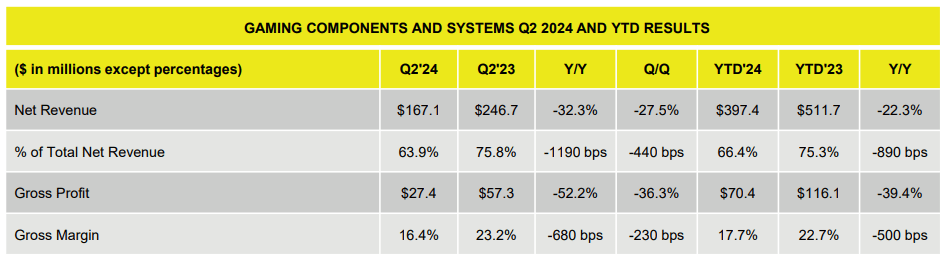

The Gaming Parts and Techniques phase alternatively had a fair bleaker consequence than in Q1 at a year-on-year decline of -32.3% in revenues, whereas the gross margin additionally contracted by 6.8 share factors.

CRSR Q2 Investor Presentation

Corsair associated the weak point once more to macroeconomic circumstances, but additionally to channel stock changes that had round a 15% impact on revenues as Corsair’s element retailers lowered stock ranges to regulate for decrease demand – the extremely bleak revenues don’t absolutely present underlying demand for Corsair’s parts, though I consider that channel stock changes are nonetheless prone to proceed into upcoming quarters as nicely.

As a 3rd issue, Corsair expressed NVIDIA’s anticipated new gaming GPU launches in late 2024 to early 2025 that many players are ready for to replace their gaming methods – an RTX 5090 GPU is rumored to be launched in This autumn/2024 with the RTX 5080 following in a number of weeks.

However, element producers present a combined image to the weak element gross sales – AMD (AMD) reported a dramatically sharp income decline of -59% in gaming revenues in Q2. Intel (INTL) did report a 9% improve in Shopper Computing Group revenues within the newest quarter, however the phase isn’t absolutely similar to gaming revenues alone. NVIDIA (NVDA) has but to report Q2 outcomes, being probably the most crucial GPU producer, however the firm did report good Q1 development in gaming revenues as beforehand talked about.

I consider that the relations is smart, though once more, buyers ought to take warning within the phase’s efficiency coming from the Covid-pandemic demand peak. Element producers are offering a combined image of the trade’s demand, making Corsair’s declines probably partly structural as nicely.

Corsair nonetheless believes new recreation releases, particularly COD Black Ops 6 in This autumn and GTA 6 in 2025 to drive greater eventual demand, and as methods constructed throughout the Covid pandemic begin to be in want of upgrades, alternative revenues ought to finally help revenues as nicely. But, I don’t suppose that Corsair’s outlook is fairly within the close to time period, though I do consider in a large mid-term restoration. The PC gaming trade remains to be estimated to develop by Statista, though at a decrease tempo than traditionally, and Corsair’s established place within the trade ought to help peripheral momentum and a element restoration.

Corsair’s 2024 Steerage Was Now Lowered

Corsair lowered its 2024 income outlook from $1.45-1.60 billion into simply $1.25-1.35 billion at a brand new mid-point -11.0% decline and small declines in H2 from the present trailing revenues of $1.38 billion. The adjusted working revenue is predicted at $48-63 million, down by practically half from the earlier $92-112 million steering vary. Apparently, the steering vary in adjusted working revenue solely widened after a half of the yr’s financials have already been reported, in my view regarding a probable cloudy and turbulent near-term outlook.

Corsair already anticipated a sequential restoration after Q1 that clearly didn’t maintain water in Q2, making wholesome skepticism justified in the interim. The brand new steering may be missed if demand doesn’t enhance – NVIDIA’s new 5-series GPUs aren’t probably going to materially impression 2024 outcomes but and the shopper sentiment stays low within the US. As a base situation, I consider that the element phase will solely return to development in 2025.

Potential Acquisition of ENDOR

Corsair has beforehand introduced its intention to amass ENDOR AG (OTC:ENDRF), an organization recognized for its Fanatec gaming sim model. Because the German firm was reaching insolvency, Corsair has beforehand already reached an settlement to finance the corporate with 70 million euros in debt, resulting in an eventual acquisition if no regulatory points come up.

ENDOR has had spectacular income development from simply $4.8 million in 2013 into $90.1 million as of Q3/2022, additionally reaching $7.8 million in working revenue in 2019 even previous to the Covid pandemic. ANDOR has now filed for insolvency, although, and the insolvency proceedings program in the end decides the framework affecting Corsair’s capacity to amass the corporate. Corsair remains to be pursuing the strategic, and probably very accretive acquisition.

CRSR’s Valuation Is Enticing, However Warning Is Wanted Due To Elevated Dangers

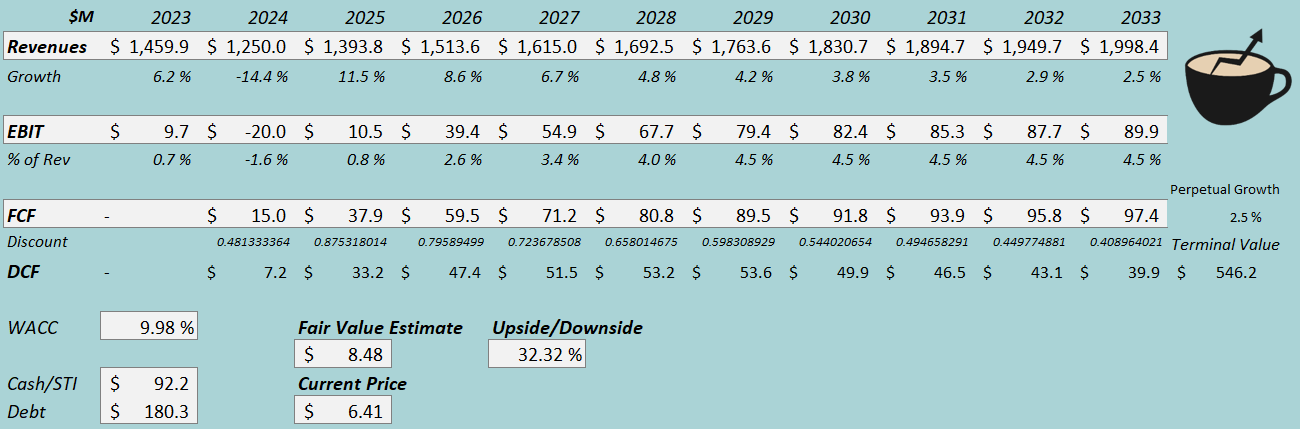

I up to date my DCF mannequin, now estimating the decrease sure of Corsair’s new 2024 income steering. Nonetheless, for the long-term, I estimate good income development after a 2025 11.5% restoration, at a complete income CAGR of 5.4% from 2024 to 2033. The estimates nonetheless signify a mid-term restoration within the element phase, and will face important modifications within the outlook in coming quarters.

For the EBIT margin, I estimate a -1.6% GAAP margin in 2024, however elevation into 4.5% with the weak phase’s restoration and working leverage. I beforehand estimated a greater 5.0% sustained margin degree, however the weak point in element gross sales requires extra warning now.

The corporate’s money movement conversion ought to stay extremely good attributable to a considerable amount of non-cash amortization.

DCF Mannequin (Writer’s Calculation)

With the talked about estimates, the DCF mannequin now estimates Corsair’s honest worth at $8.48, round 32% above the inventory worth on the time of writing – after beforehand estimating slight draw back two occasions, the valuation is now beginning to get engaging when anticipating a partly element phase restoration and good peripheral momentum. The honest worth estimate is down from $10.52 beforehand.

But, with probably turbulence forward, I consider that buyers ought to stay cautious. Additional inventory weak point, or a reported beginning turnaround, might make the inventory a really attention-grabbing shopping for alternative contemplating the valuation.

CAPM

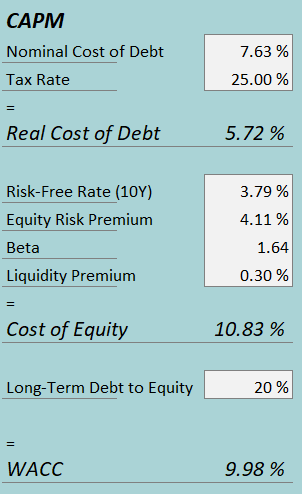

A weighted common value of capital of 9.98% is used within the DCF mannequin. The used WACC is derived from a capital asset pricing mannequin:

CAPM (Writer’s Calculation)

In Q2, Corsair had $3.4 million in curiosity bills. With the corporate’s present quantity of interest-bearing debt, Corsair’s annualized rate of interest comes as much as 7.63%. I now estimate a 20% long-term debt-to-equity ratio, greater than the 15% beforehand attributable to a decrease fairness valuation.

For the risk-free fee on the price of fairness facet, I take advantage of america’ 10-year bond yield of three.79%. The fairness danger premium of 4.11% is Professor Aswath Damodaran’s newest estimate for america, up to date in July. I’ve stored the beta estimate at 1.64. Lastly, I add a small liquidity premium of 0.3%, creating a price of fairness of 10.83% and a WACC of 9.98%.

Takeaway

Corsair reported an extremely weak Q2 when it comes to element gross sales, inflicting a really sharp inventory decline. Macroeconomic circumstances, the anticipated launch of recent NVIDIA GPUs, and retailer stock destocking mixed to trigger chaos within the quarter with continued robust peripheral development solely partly countering the weak momentum in parts. I consider that nice warning is required within the brief time period, though I do nonetheless consider in a mid-term restoration. The valuation has gotten engaging when anticipating a element restoration, however with the elevated danger degree, I cautiously nonetheless stay at a Maintain score in the interim.

[ad_2]

2024-08-04 14:53:19

Source :https://seekingalpha.com/article/4710333-corsair-gaming-stock-q2-earnings-deeper-component-sales-disaster?source=feed_all_articles

{kind=link}

Discussion about this post