[ad_1]

SrdjanPav/E+ through Getty Photos

I don’t wish to trick readers into pondering this text is the rest.

In some way, I had the concept that I ought to rant about accounting. Accounting needs to be boring, however accounting is driving a failure of environment friendly markets.

Buyers who care about being profitable ought to care about this.

Realistically, many traders received’t. If traders cared about fundamentals as a substitute of vivid lights and loud sounds, Jim Cramer would wish to supply a really completely different present.

Then once more, you’re studying In search of Alpha as a substitute of “In search of Fairly Colours,” so that you’ve in all probability seen the sunshine.

Even perhaps higher, you’re studying the analyst recognized for digging into these items and breaking them down.

Ideally, I break them down in order that they make sense for readers.

Generally I fall quick and find yourself leaving readers confused.

Immediately’s Lesson on Investing

I’m going with the identical mixture of shares I’ve been speaking about currently. It’s Dynex Capital (DX) and AGNC Funding (AGNC).

I’ve been instructing traders in regards to the distinction in TER (Complete Financial Returns) and TSR (Complete Shareholder Returns).

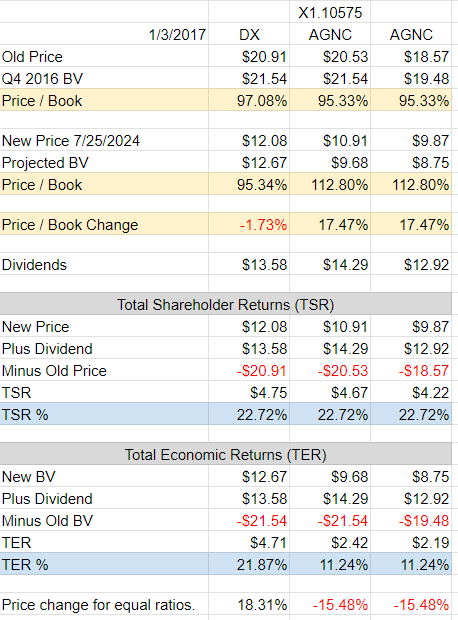

For this comparability, I’m displaying traders the distinction between one share of DX and 1.10575 shares of AGNC.

I’m doing it that approach as a result of it permits us to have exactly the identical beginning e book worth for every funding.

Reasonably than put you to sleep, I’ll leap into dividends. The remaining will turn out to be clear (hopefully) as we go.

Dividend Variations

DX and AGNC paid out completely different ranges of dividends throughout that point.

It wasn’t dramatically completely different, nevertheless it was completely different. We have to issue that into our math.

We’re going to calculate two metrics:

- Complete Shareholder Returns: That is vital for the investor.

- Complete Financial Returns: It is a software for evaluating administration.

So right here’s what we have now:

The REIT Discussion board

Notice: BV estimates from The REIT Discussion board. They’re as of seven/19/2024 however adjusted for the ex-dividend on DX earlier this week.

There’s an enormous disconnect within the valuation.

However what about AGNC’s superb earnings?

Shouldn’t we throw all the opposite due diligence within the trash, take a look at earnings, and name that due diligence?

Afterall, consensus earnings (normalized) for AGNC for 2024 is $2.16.

If shares of AGNC are $10.15, they commerce at solely 4.69x 2024 projected earnings!

Wow, that’s superb. Amazingly ineffective.

Who right here has really examined AGNC’s earnings assertion? Everybody? That was shocking.

Simply in case, let’s go over some numbers once more.

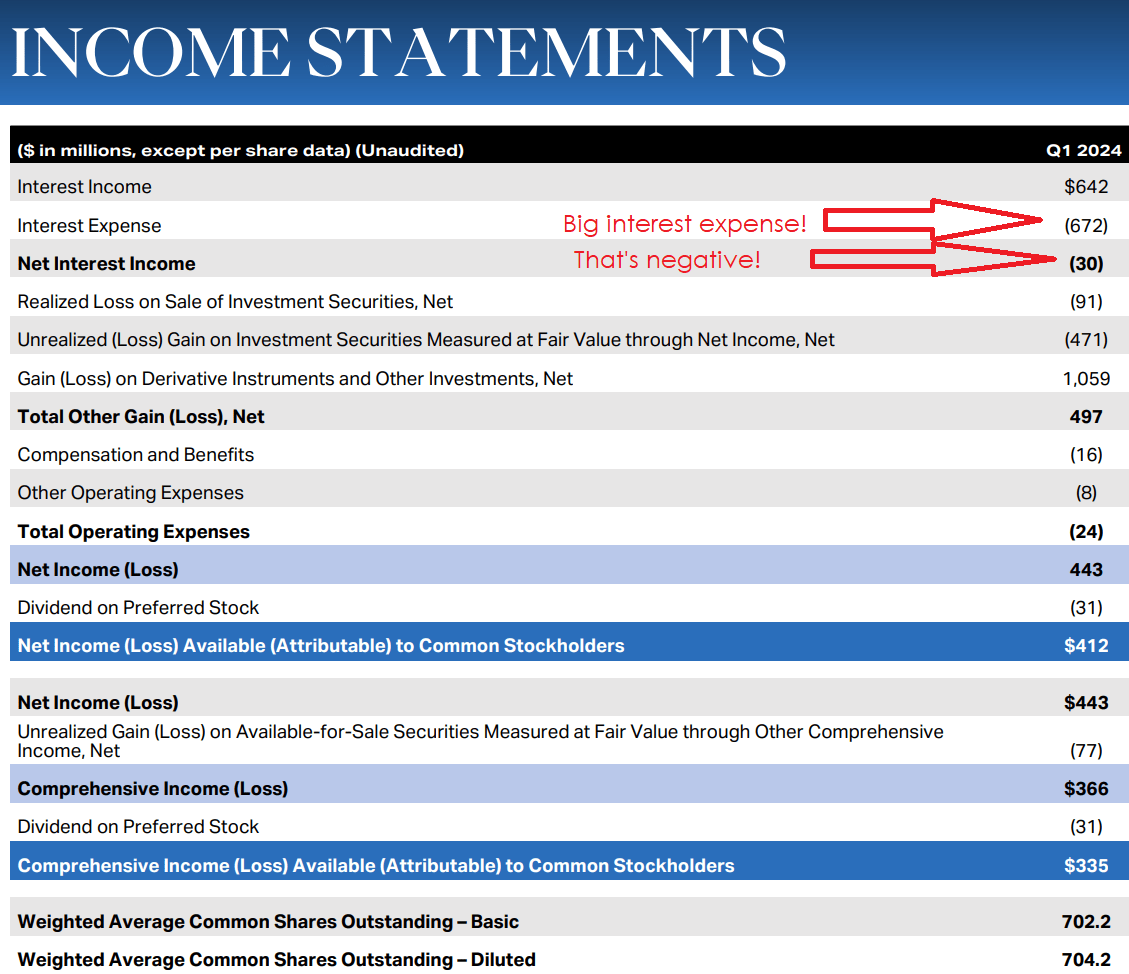

AGNC

Now we will see that AGNC really had damaging web curiosity earnings. That’s coming straight from AGNC’s presentation. They constructed that slide.

However don’t they’ve superb margins? How can they’ve damaging web curiosity earnings?

It comes right down to hedges. Particularly, the hedges don’t get counted on this presentation.

Let’s go get these hedges.

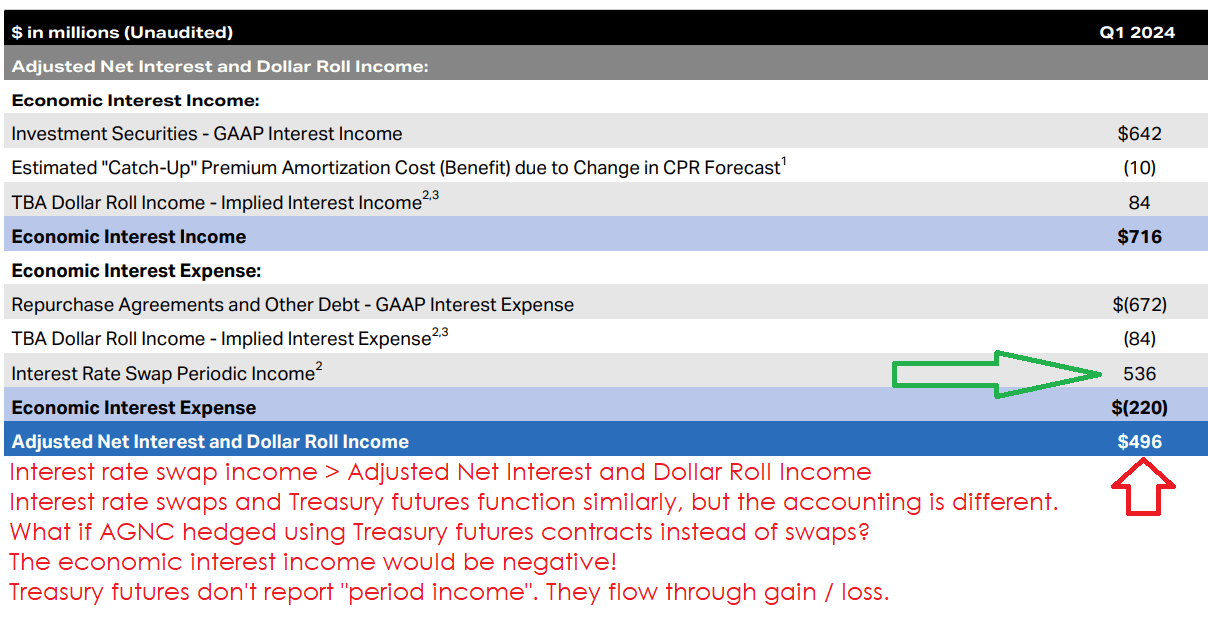

AGNC, The REIT Discussion board for commentary

Now we all know that AGNC’s superb earnings are a perform of working their hedges as LIBOR swaps.

How does DX hedge?

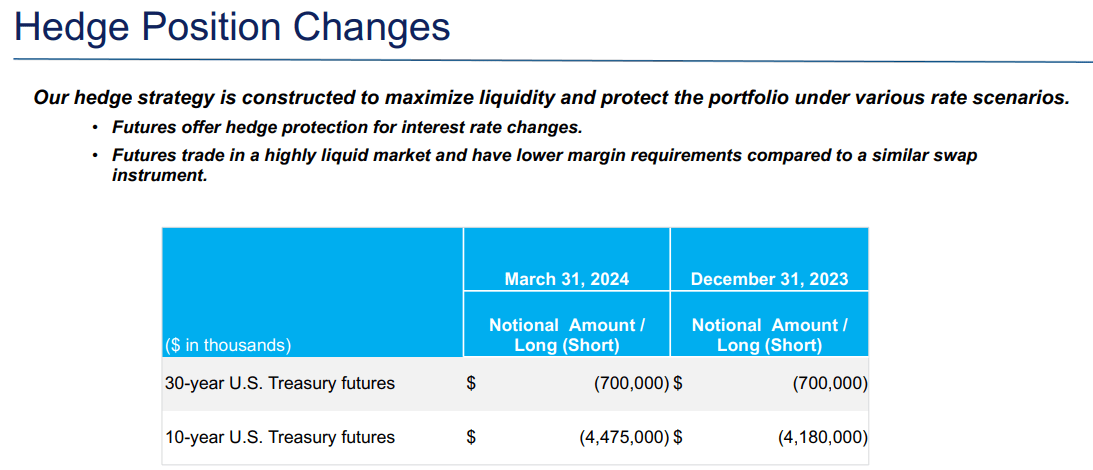

DX

DX is utilizing Treasury futures. Utilizing futures is an alternate solution to hedge. It is a extremely liquid market and has decrease margin necessities. That enables DX to handle the hedge positions actively. The one draw back is that the place flows by realized features and losses on derivatives. That is an accounting distinction.

What Did Colorado Simply Say?

Sorry, these phrases in all probability confused some individuals.

Permit me to attempt an alternate rationalization.

The futures contracts and the LIBOR swap will present a particularly comparable complete return over time.

The LIBOR swap has two elements:

- A web curiosity fee from one occasion to the opposite.

- Posting a collateral reserve (or margin) to cowl the mark-to-market for the unrealized achieve or loss.

With the futures contract, you eradicate the web curiosity fee. Subsequently, you could have one half:

- Posting a collateral reserve (or margin) to cowl the mark-to-market for the unrealized achieve or loss. As a result of there was no web curiosity fee, this modification will probably be bigger.

Why is there some reserve to cowl mark-to-market?

As a result of if there was none, some hedge fund would create a number of LLCs and enter into a number of billion {dollars} of LIBOR swaps with completely different counterparties.

The LLC holding the dropping swaps would file for chapter and disappear.

That might destroy the market. To stop that technique, there is a regulatory system in place and frequent mark-to-market.

Subsequently, the precise impression in your money flows is fairly comparable as long as Treasury charges and LIBOR charges stay very extremely correlated. That is often the case, so the distinction in hedging technique doesn’t have a huge impact on the underlying portfolio for the mortgage REIT. On this case, DX is utilizing the futures as a result of it permits them to commerce positions (and alter their length publicity) with much less friction than in the event that they had been utilizing LIBOR swaps.

A Third Strive

It is a arduous idea for some individuals, so I’ve a 3rd solution to display it.

Think about that AGNC had a web curiosity fee of $5 on a swap and an unrealized achieve frees up $10 of margin.

AGNC’s money place elevated by $15.

DX has a futures place masking the identical a part of the curve.

DX has no web curiosity fee. The unrealized achieve frees up $15 of margin.

DX’s money place elevated by $15.

Each positions have their collateral totally happy.

Each REITs had the identical change in money.

For AGNC, $5 flows by the curiosity earnings on swaps and $10 flows by the unrealized achieve on derivatives.

For DX, $15 flows the unrealized achieve on derivatives.

Easy sufficient?

Similar end result.

But the market is satisfied that AGNC’s result’s higher purely due to the accounting.

Extremely Correlated

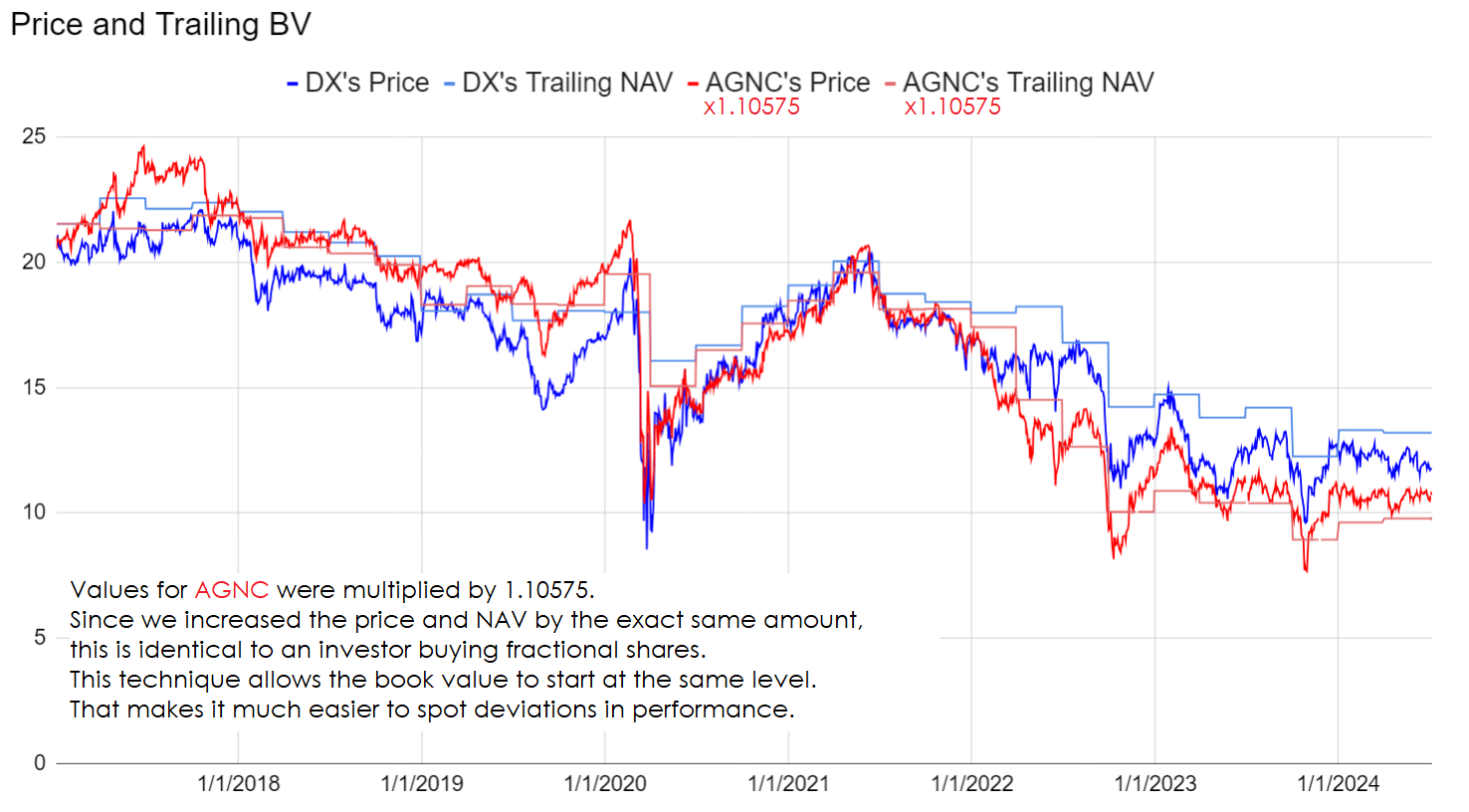

The change in e book worth for AGNC and DX by quarter was extraordinarily extremely correlated. You possibly can confirm that utilizing the chart displaying e book worth (and share worth) over time.

Since a few of you received’t have seen that chart, I’m offering it right here once more. This chart doesn’t have the previous couple of days, however that doesn’t actually matter once we’re offering about eight years of historical past:

The REIT Discussion board

Why are they so extremely correlated?

As a result of they personal comparable property and run hedging portfolios that produce an identical change in worth, regardless that it flows by a special line merchandise.

I proceed to imagine that DX is a greater worth than AGNC. This unfold in price-to-book ratios seems to be a perform of traders (or computer systems) who merely don’t perceive the distinction in accounting.

Thanks for listening to (or studying) my rant about accounting. I am amazed and grateful that individuals select to learn my articles even once I’m going off about accounting.

Extra Guides Coming

One of many issues I’ve realized over my final decade of publishing articles on In search of Alpha is the significance of getting guides.

I’ve ready fairly a number of over time, however I foolishly left a lot of them behind a paywall.

Over the subsequent a number of weeks I plan to republish a lot of them for readers as instablogs or free articles.

As I publish them, you’ll see this part in my articles develop so I can present an organized record of the guides.

Nevertheless, I nonetheless want to supply extra guides.

If there’s an idea associated to REITs that you just want to perceive higher, let me hear about it within the feedback.

Most well-liked Share Information

I recurrently encourage traders to give attention to most well-liked shares for this sector fairly than widespread shares. The popular shares usually supply a significantly better complete shareholder return over lengthy durations and so they do it with far much less unstable. Consequently, it’s a significantly better alternative for long-term traders. The popular share guides additionally present some alternatives to swap between comparable shares, which may improve returns.

When you’re all for most well-liked shares, be sure that to take a look at our large free information to most well-liked shares.

it’s nice, as a result of I wrote it. it’s lengthy, as a result of it’s over 67 pages. Examples take house.

We might’ve had much less examples, however then it wouldn’t be pretty much as good.

Many readers have advised me it’s their major useful resource for studying how most well-liked shares work.

It took a number of years to deliver all of it collectively, so I hope readers get pleasure from it.

Inventory Desk

We are going to shut out the remainder of the article with the tables and charts we offer for readers to assist them monitor the sector for each widespread shares and most well-liked shares.

We’re together with a fast desk for the widespread shares that will probably be proven in our tables:

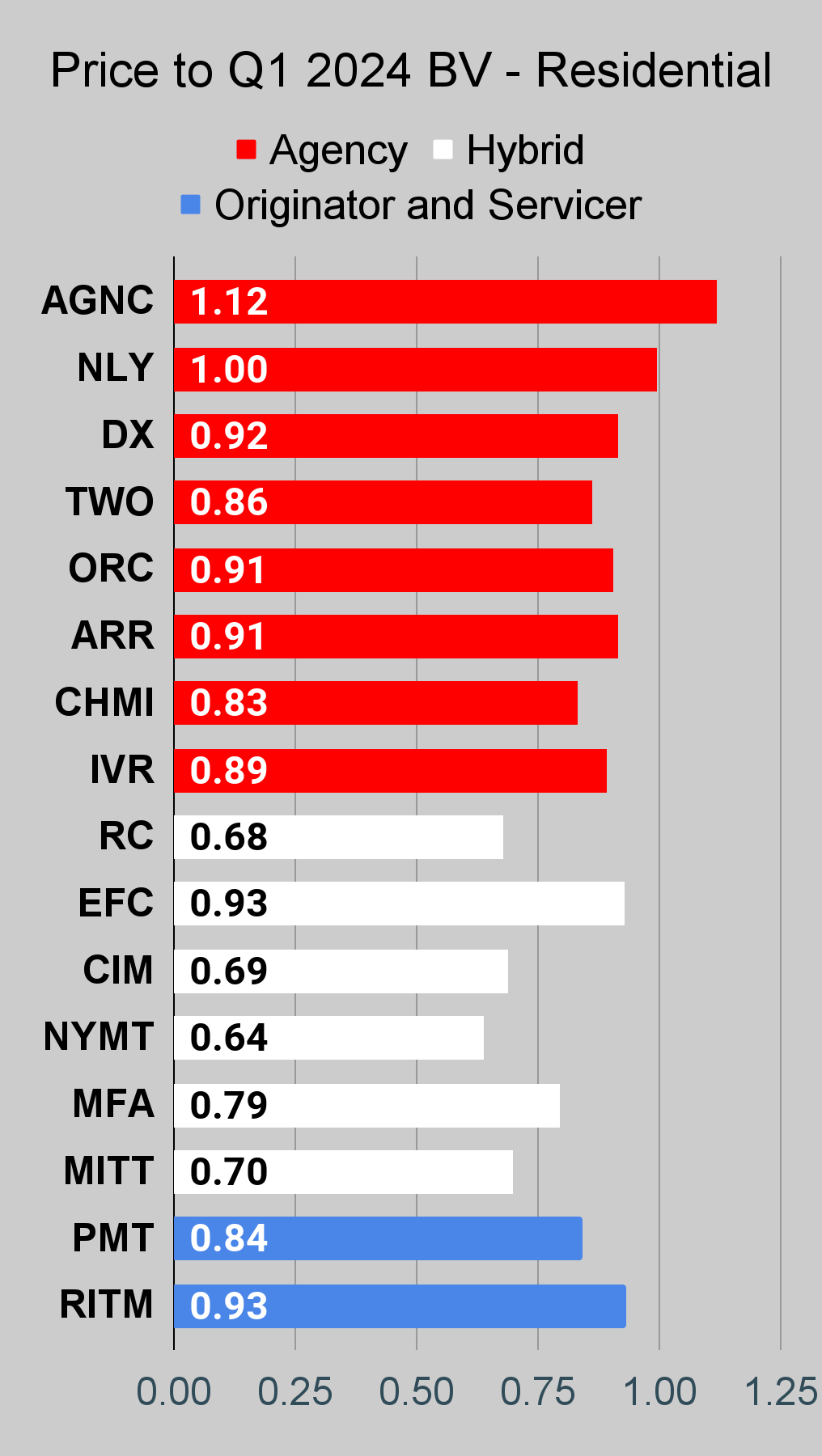

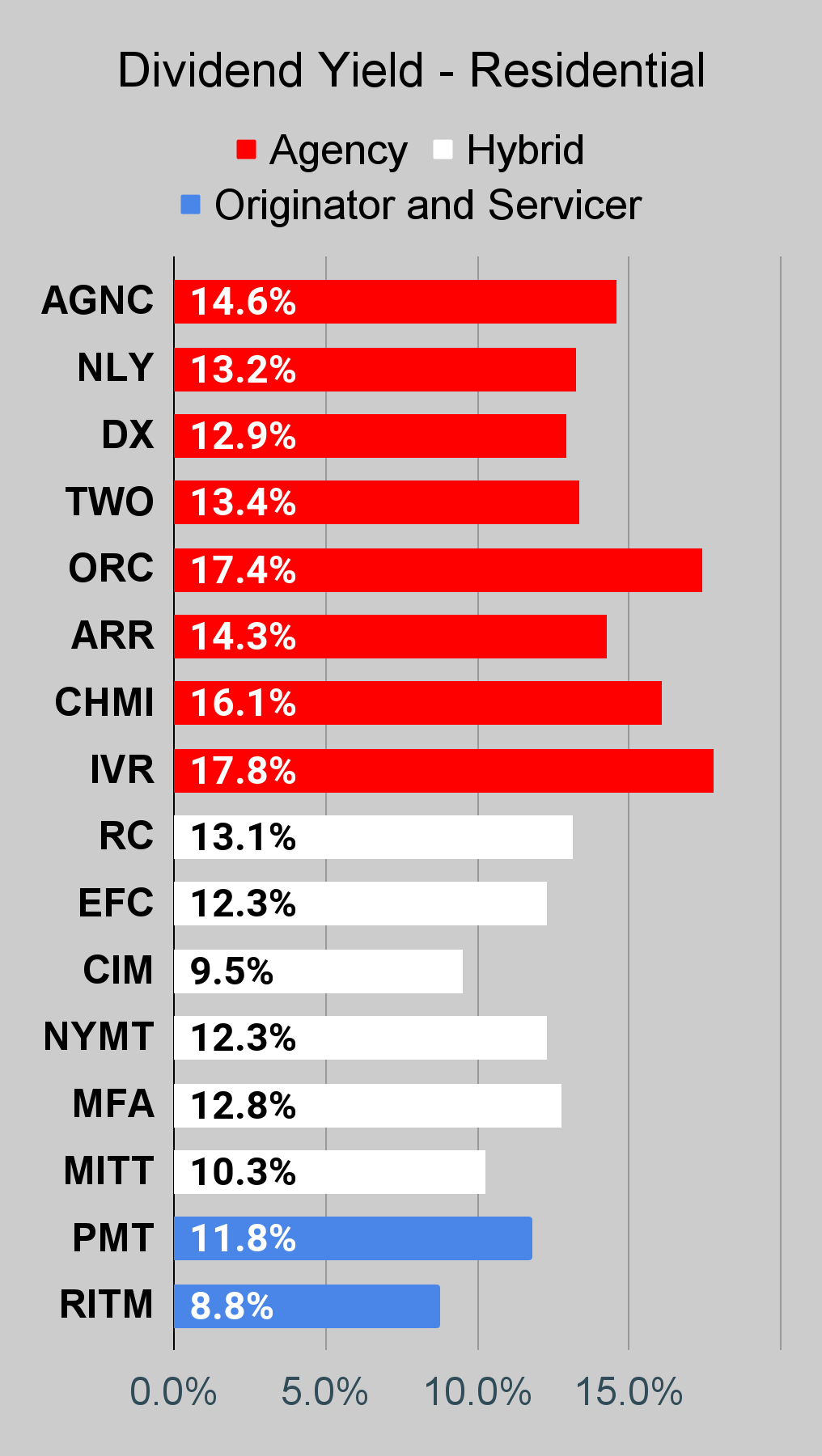

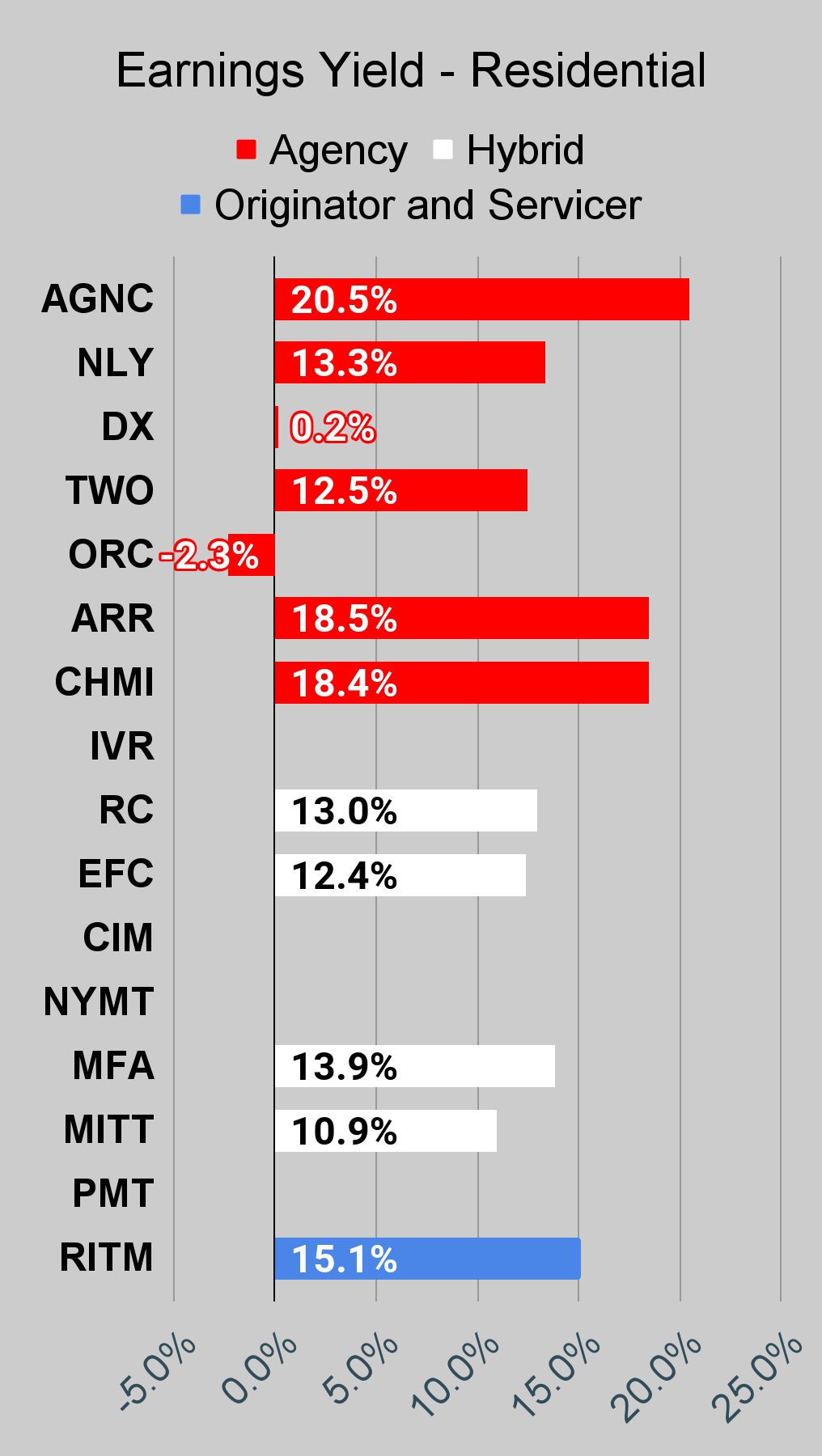

When you’re in search of a inventory that I haven’t talked about but, you’ll nonetheless discover it within the charts under. The charts comprise comparisons primarily based on price-to-book worth, dividend yields, and earnings yield. You received’t discover these tables anyplace else.

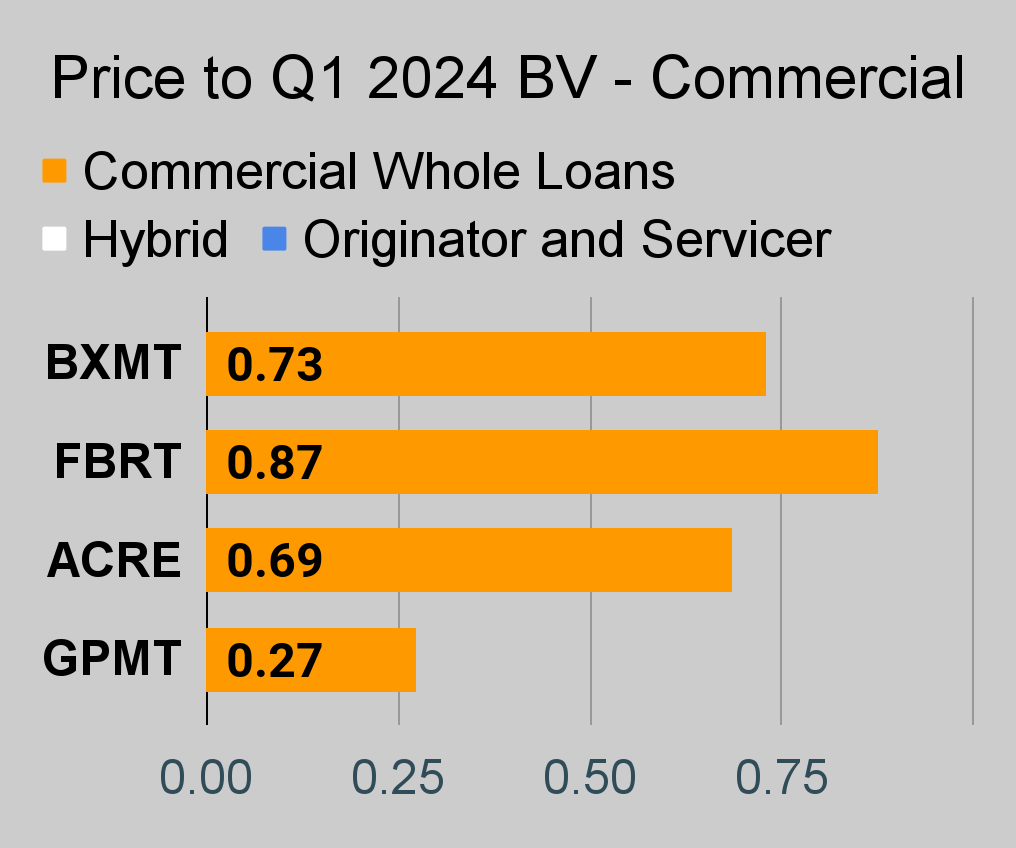

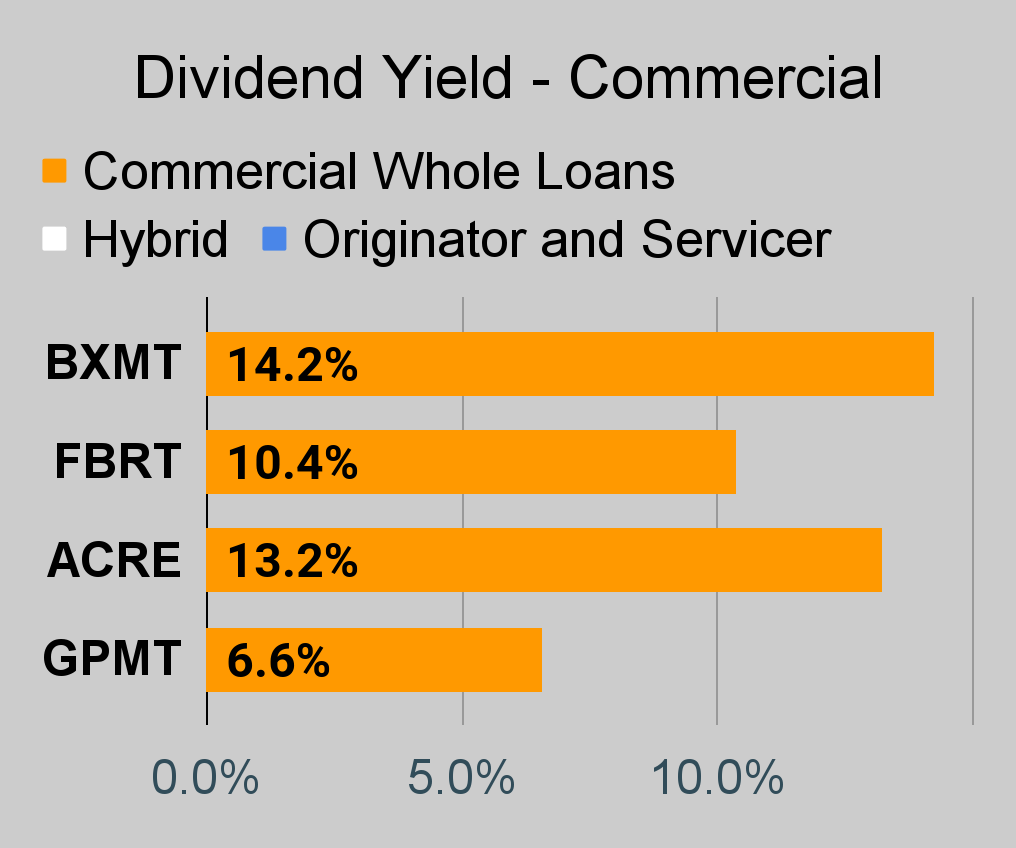

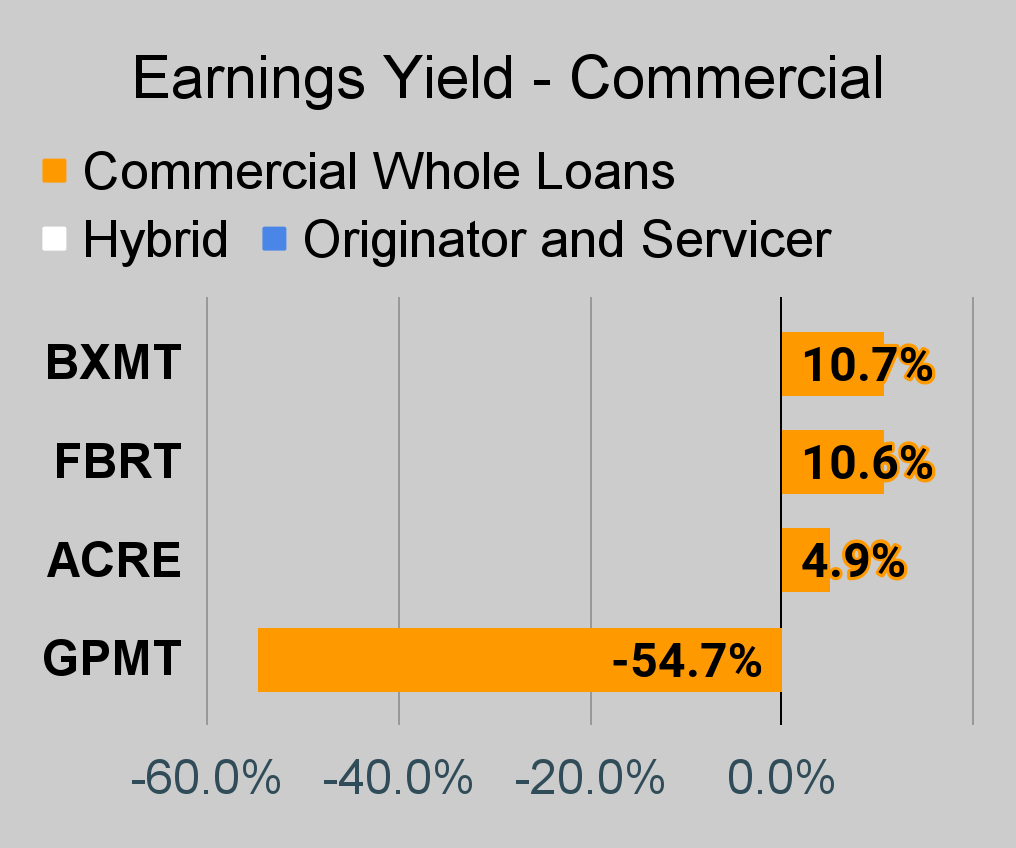

For mortgage REITs, please take a look at the charts for AGNC, NLY, DX, ORC, ARR, CHMI, TWO, IVR, CIM, EFC, NYMT, MFA, MITT, AAIC, PMT, RITM, BXMT, GPMT, WMC, and RC.

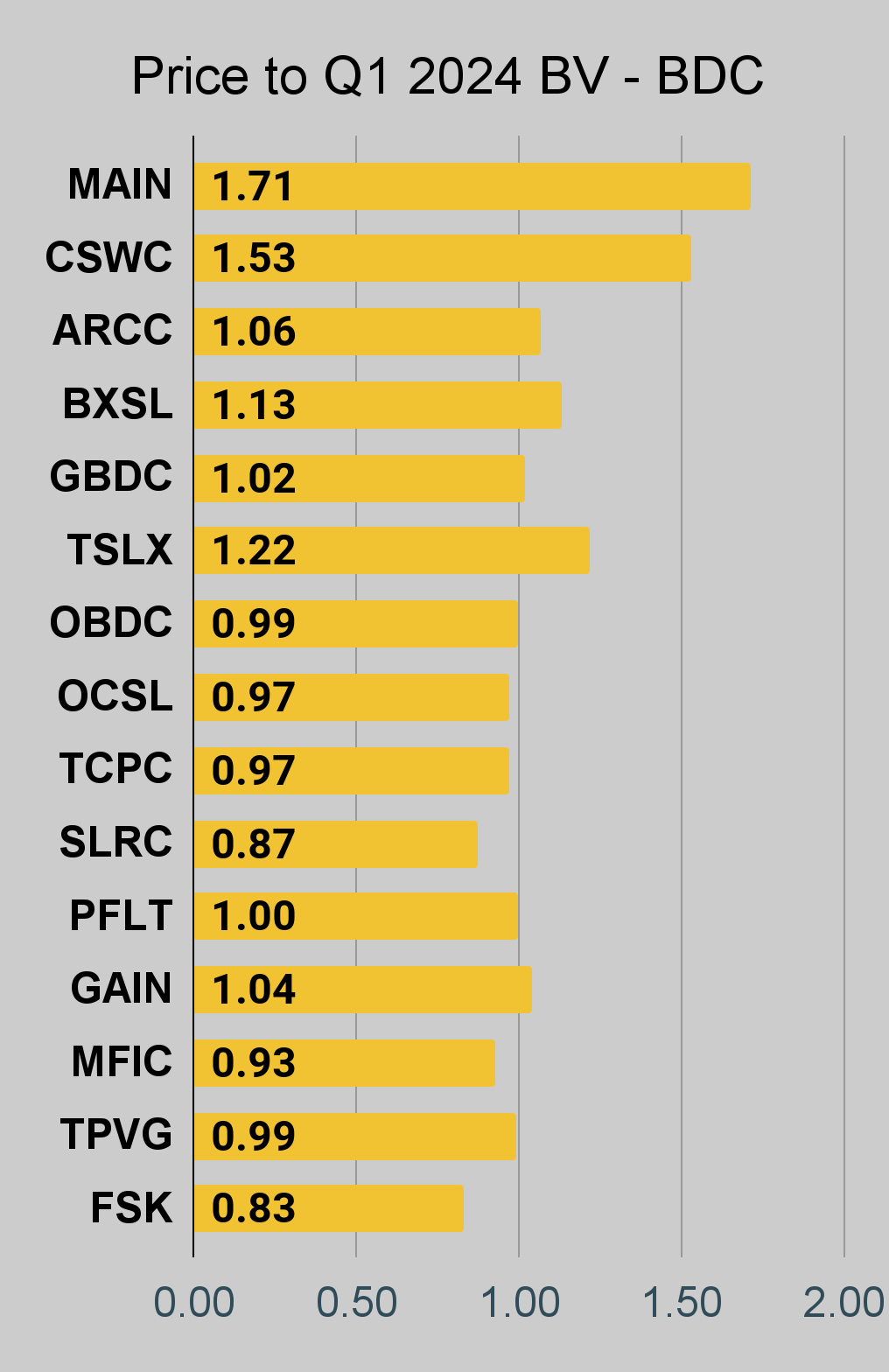

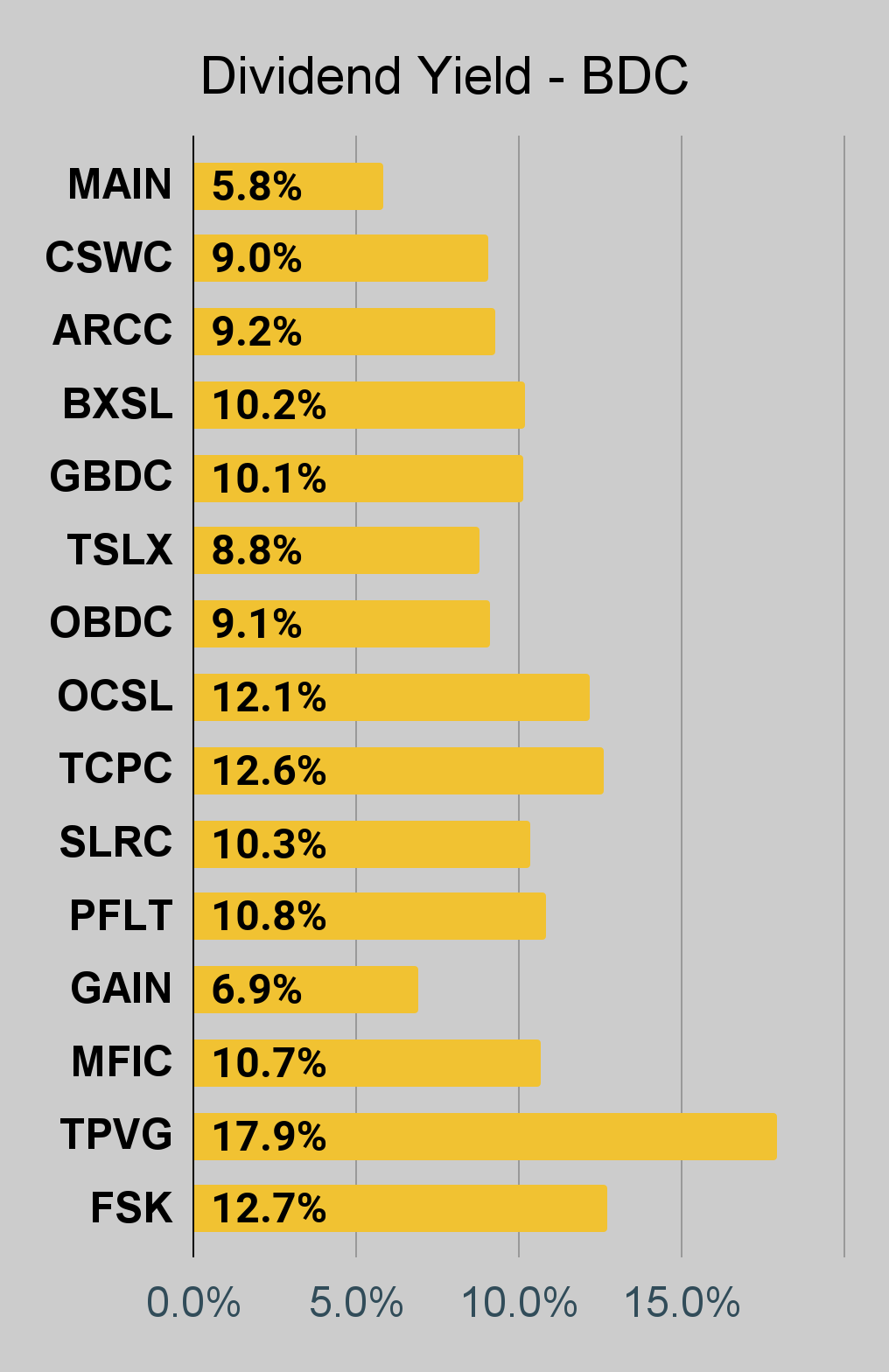

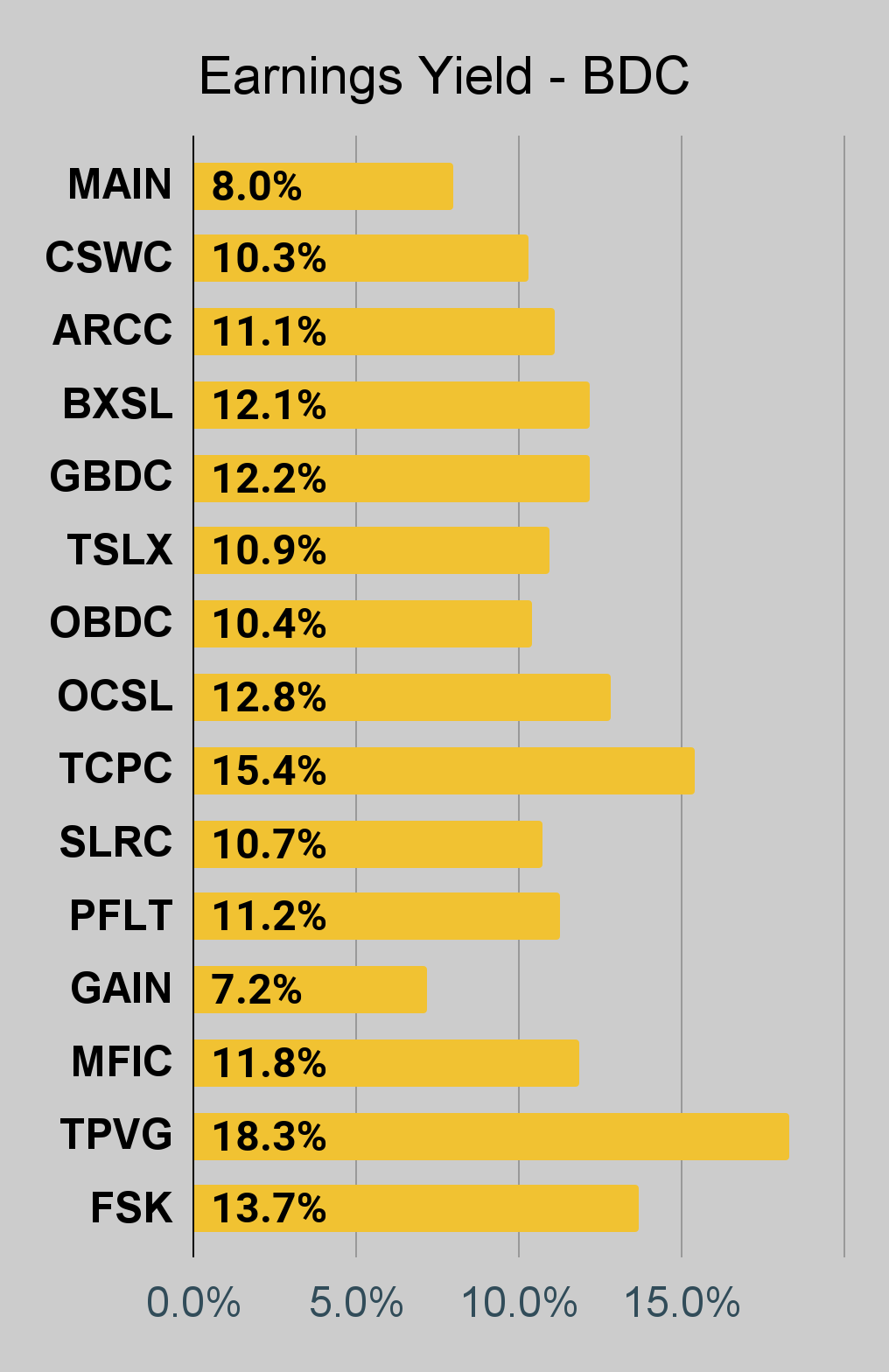

For BDCs, please take a look at the charts for MAIN, CSWC, ARCC, TSLX, TPVG, OCSL, GAIN, GBDC, SLRC, OBDC, PFLT, TCPC, FSK, PSEC, and MFIC.

This sequence is the simplest place to search out charts offering up-to-date comparisons throughout the sector.

Notes on Chart Sorting

Inside every sort of safety, the sorting is often primarily based on danger rankings. Nevertheless, it is fairly widespread to have a number of shares which are tied. When the shares are tied for danger score, the sorting turns into arbitrary. There could sometimes be errors the place a share’s place isn’t up to date shortly following a change within the danger score. That may occur as a result of the charts come from a separate system. Once I replace the system we use for members, it doesn’t change the order within the charts.

Once I say “inside every sort of safety,” I’m referencing classes reminiscent of “company mortgage REITs.” The “hybrid mortgage REITs” are all listed after the “company mortgage REITs.” Nevertheless, that doesn’t imply RC (lowest hybrid) has the next danger score than the best company mortgage REIT. Every batch is offered by themselves.

PMT and RITM are tied for danger score.

This might in all probability be written higher. If somebody feels inclined to take it upon themselves to write down a piece that’s objectively higher at speaking these factors, I’d be all for utilizing it. I’m grateful to have the very best readers on SA. I attribute this to self-selection bias. I embrace sufficient issues to offend the dumb those who I’m left with the very best readers.

Notice: The chart for our public articles makes use of the e book worth per share from the quarter indicated within the chart. We use the present estimated (proprietary estimates) e book worth per share to find out our targets and buying and selling choices. It’s accessible in our service, however these estimates will not be included within the charts under. PMT and NYMT will not be displaying an earnings yield metric as neither REIT supplies a quarterly “Core EPS” metric. Presently, a number of different REITs additionally haven’t any consensus estimate.

Second Notice: Because of the approach historic amortized value and hedging is factored into the earnings metrics, it’s potential for 2 mortgage REITs with comparable portfolios to publish materially completely different metrics for earnings. I’d be very cautious about placing a lot emphasis on the consensus analyst estimate (which is used to find out the earnings yield). Specifically, all through late 2022 the earnings metric grew to become much less comparable for a lot of REITs.

Residential Mortgage REIT Charts

The REIT Discussion board |

The REIT Discussion board |

The REIT Discussion board |

Industrial Mortgage REIT Charts

The REIT Discussion board |

The REIT Discussion board |

The REIT Discussion board |

BDC Charts

The REIT Discussion board |

The REIT Discussion board |

The REIT Discussion board |

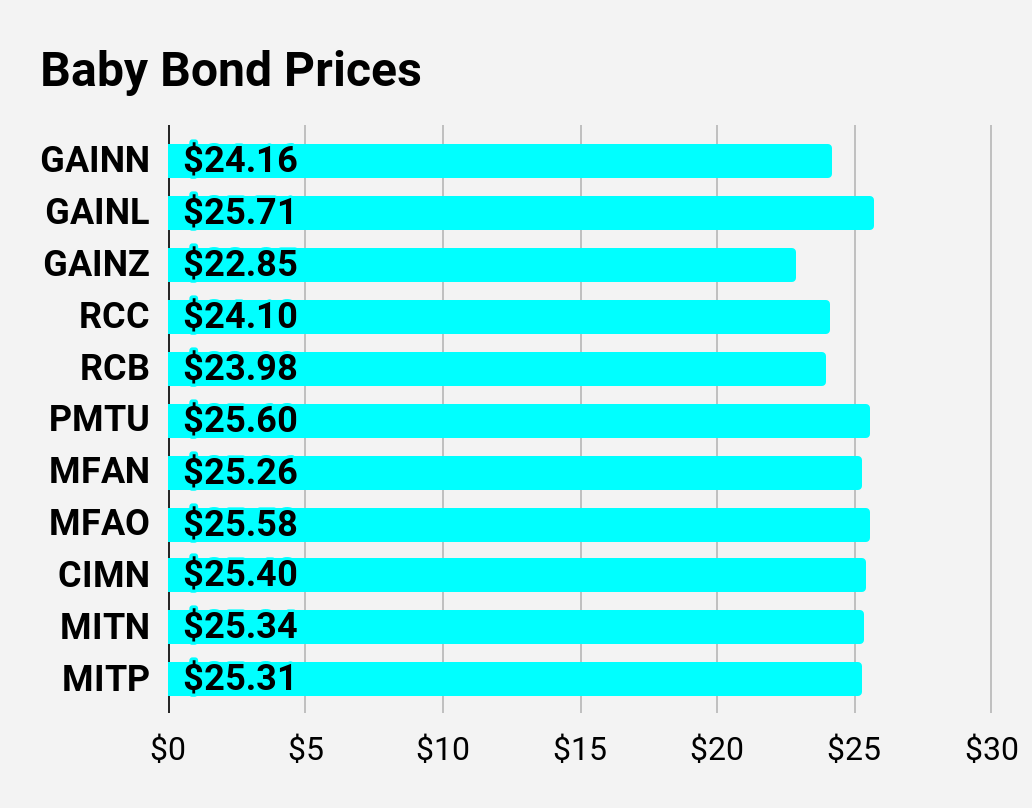

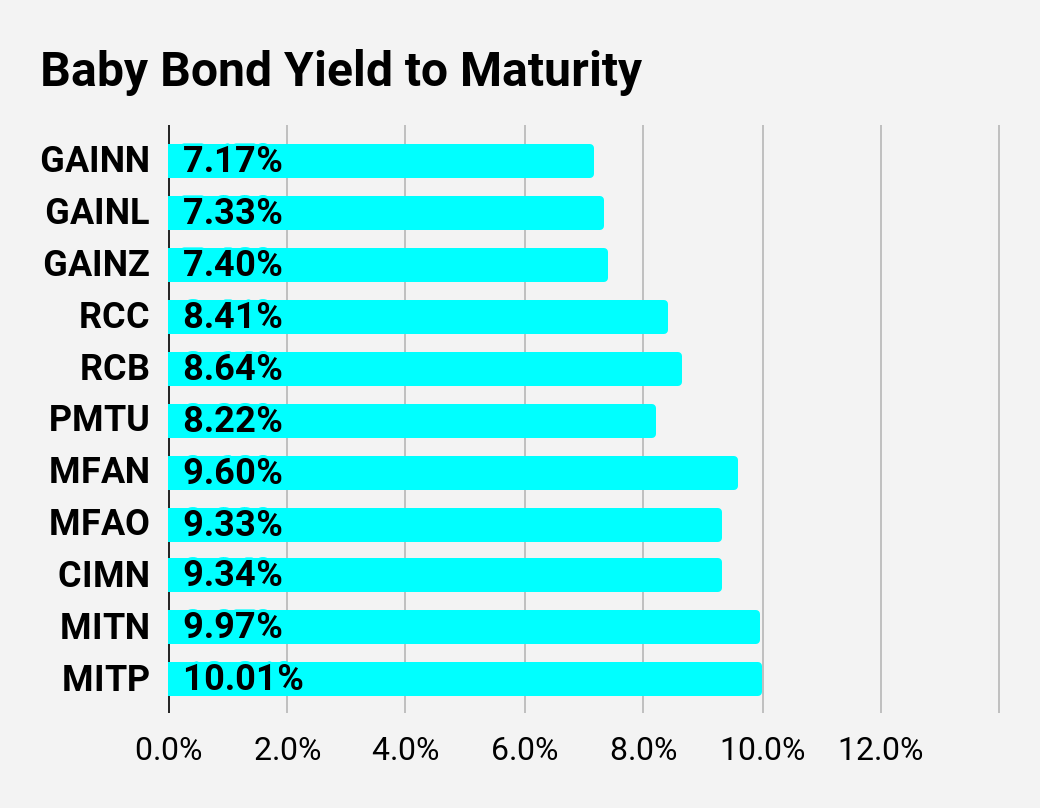

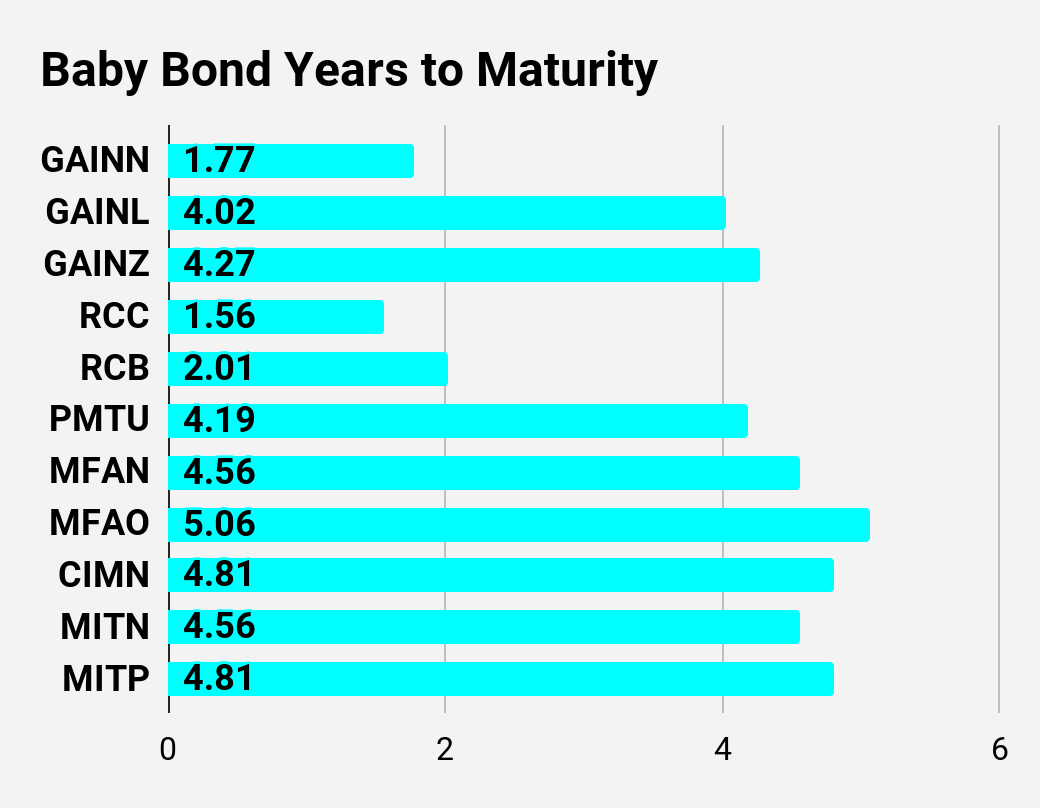

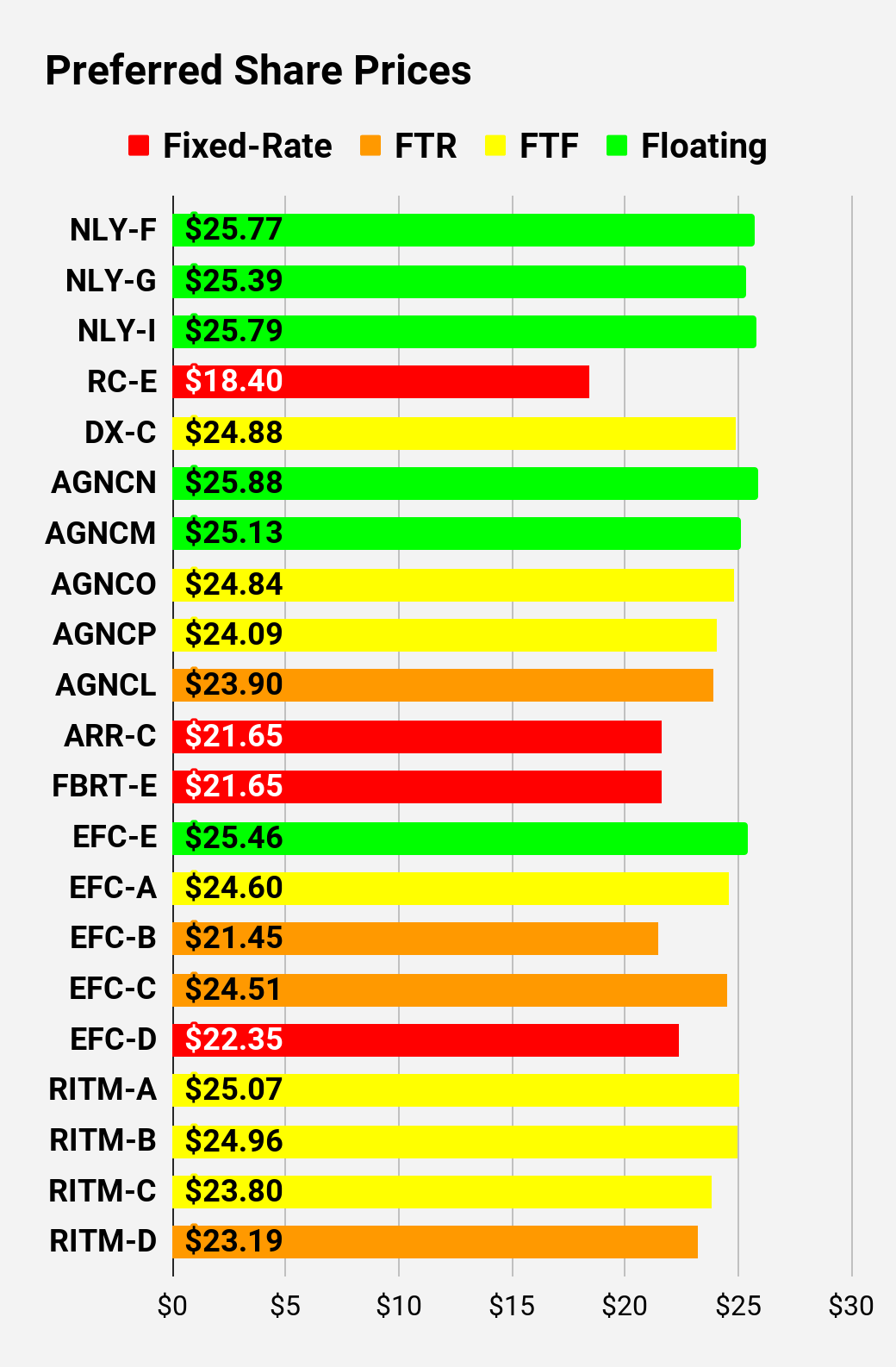

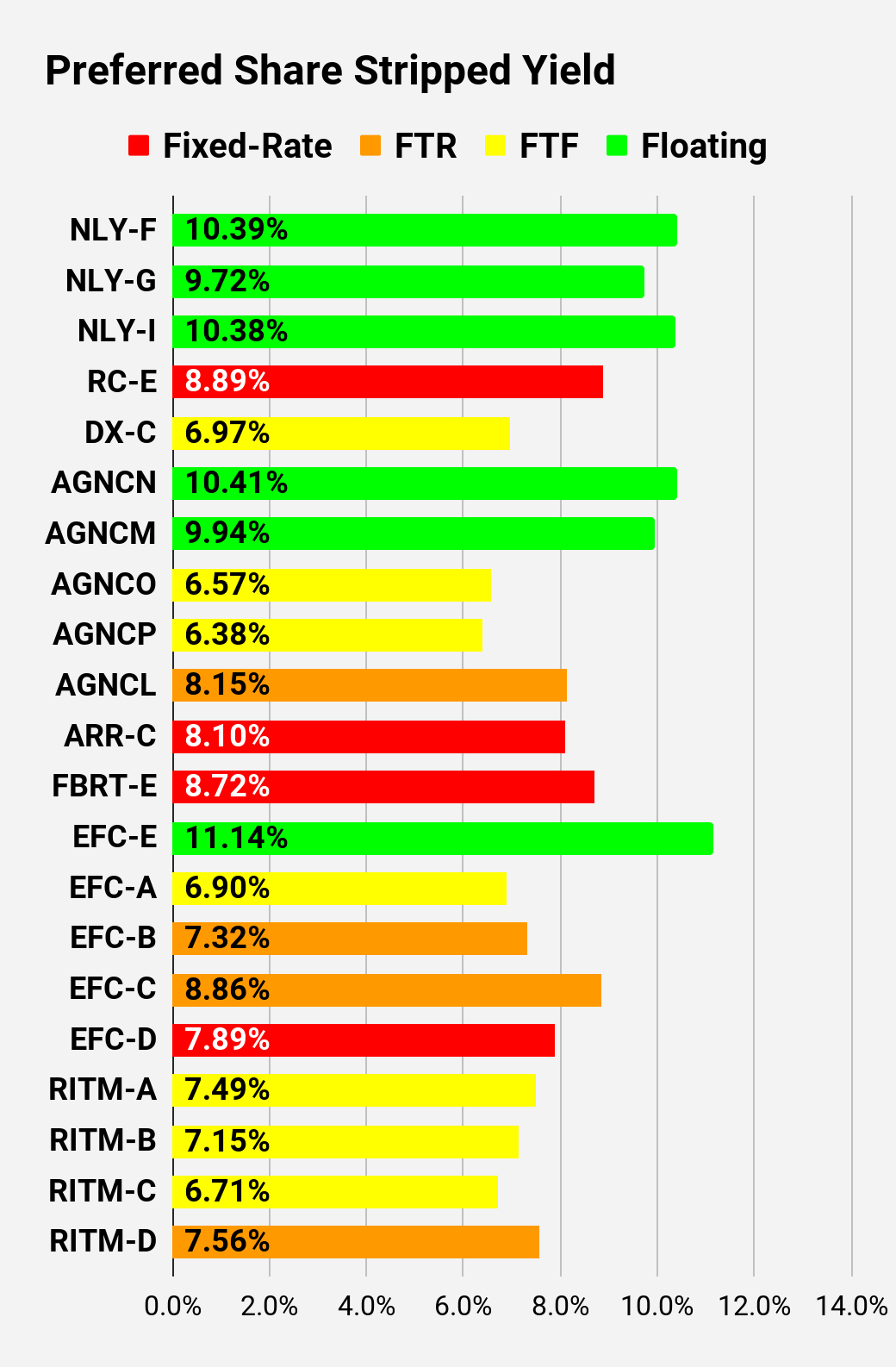

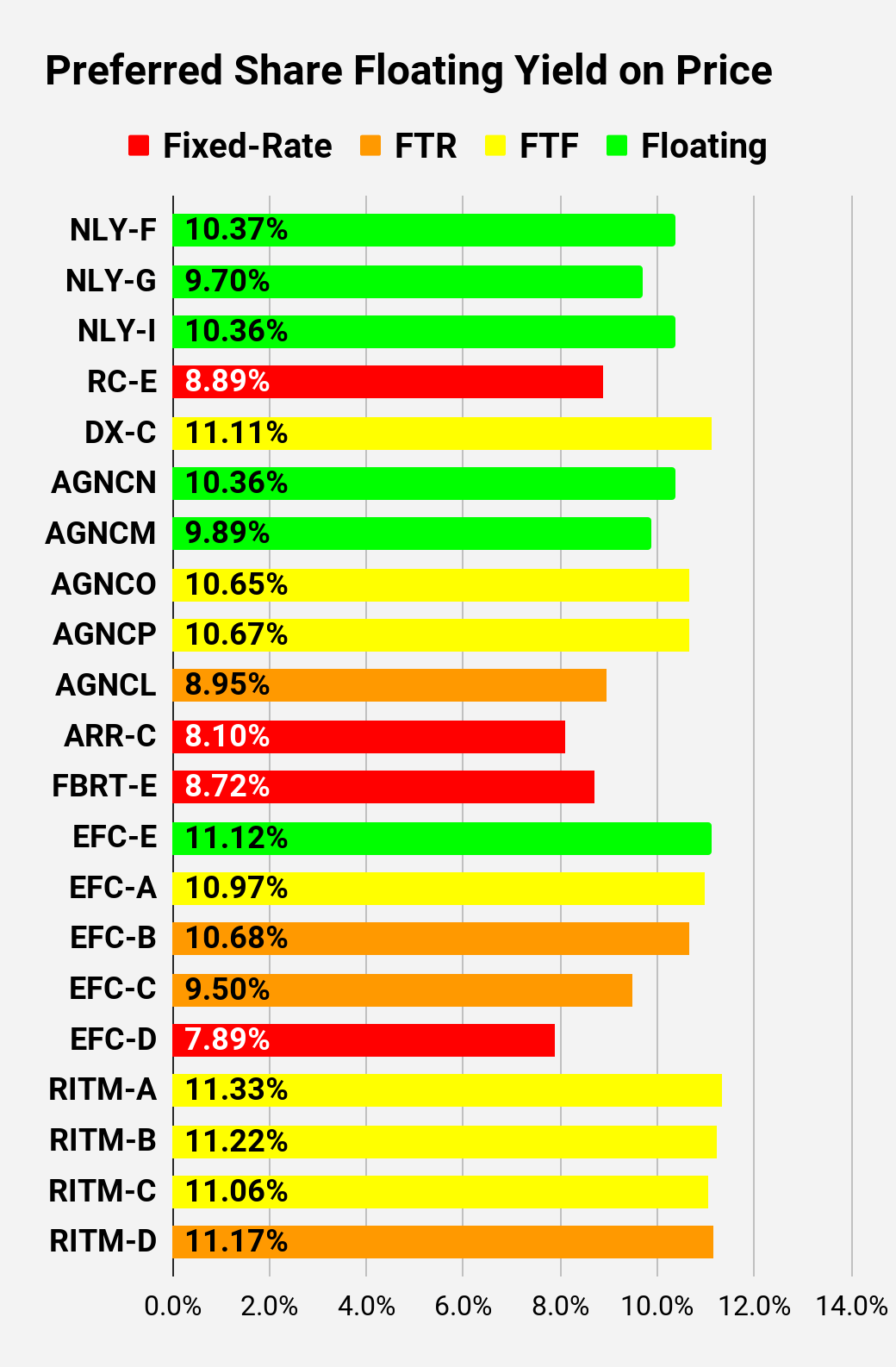

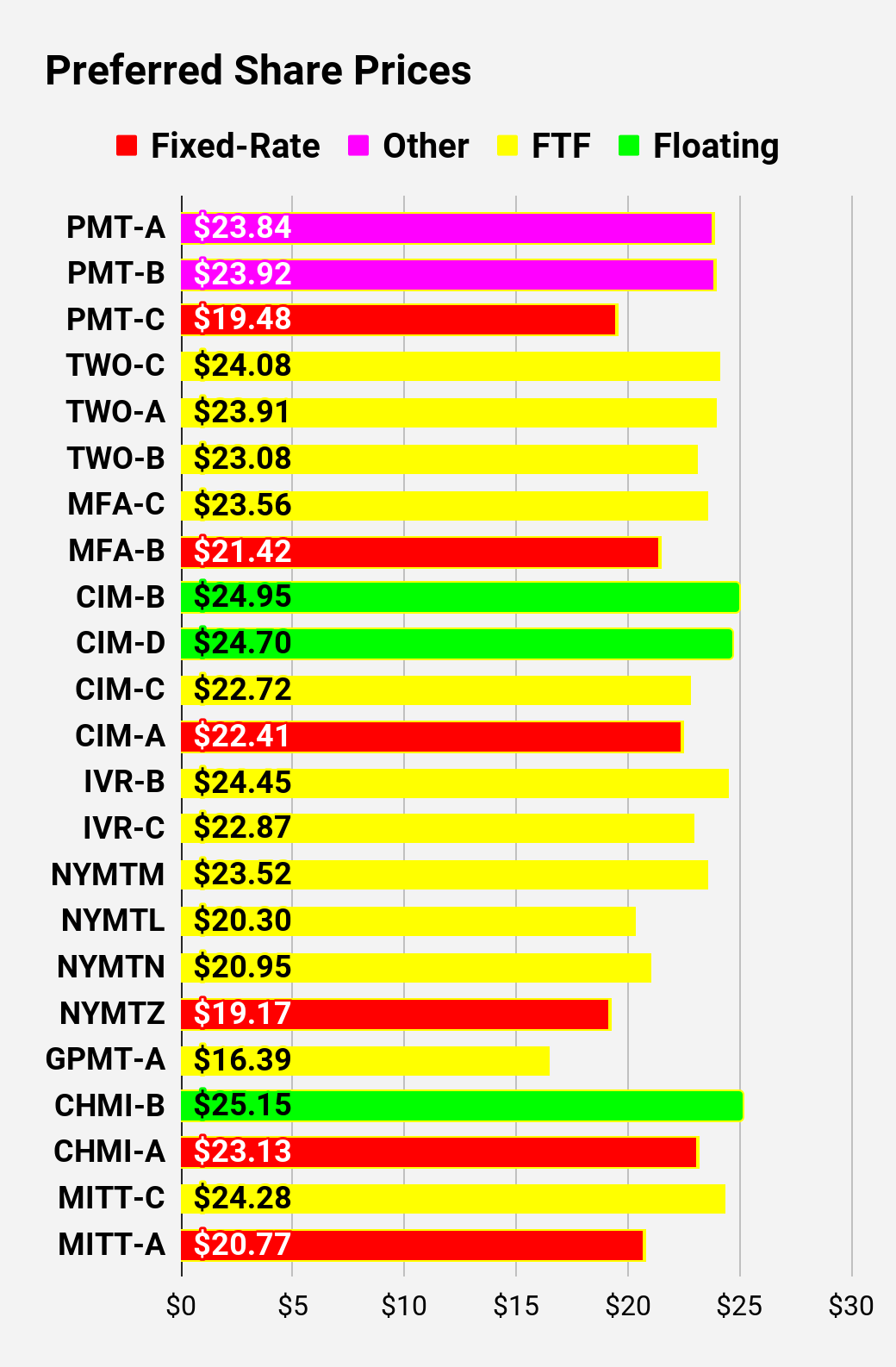

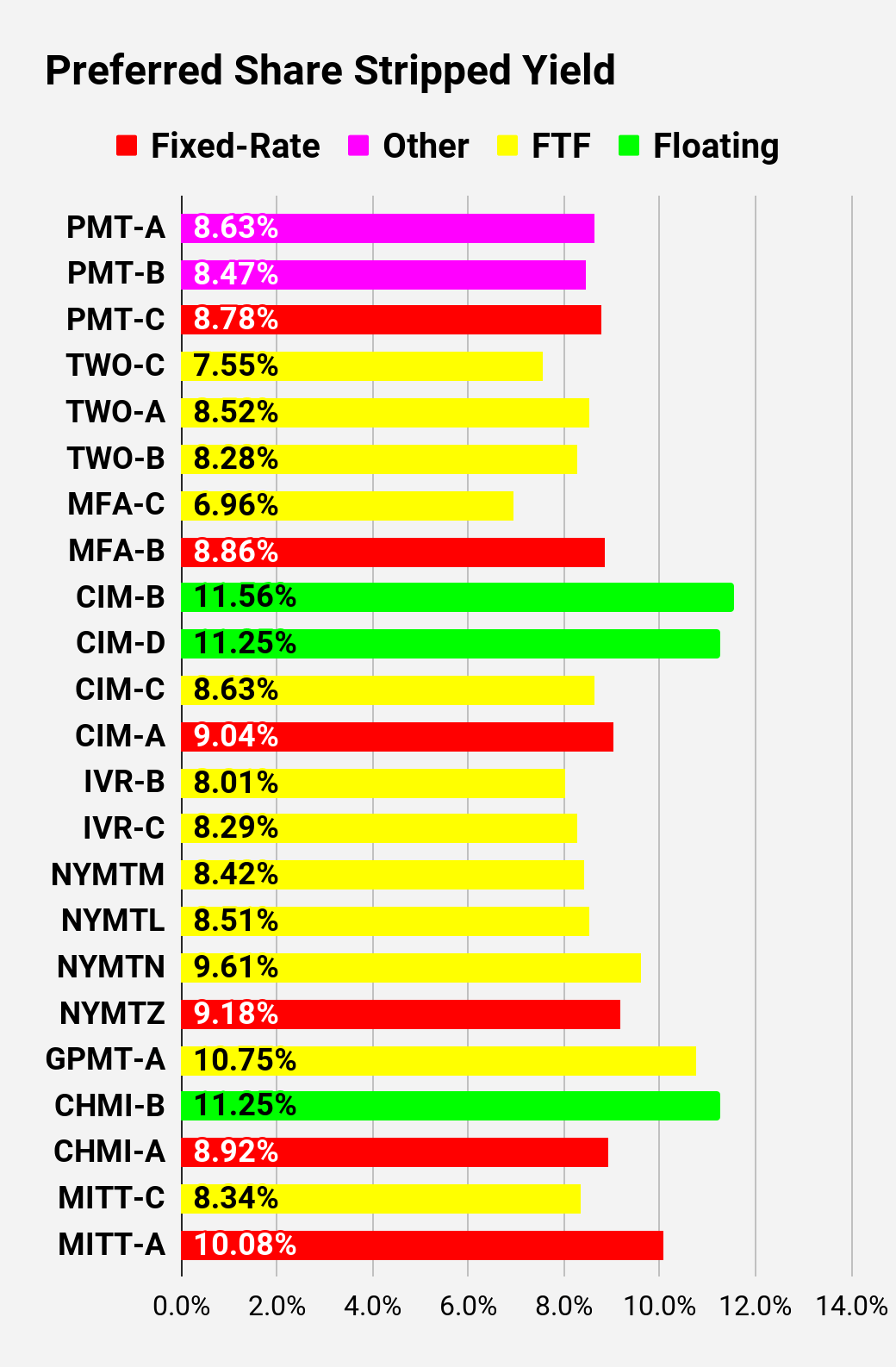

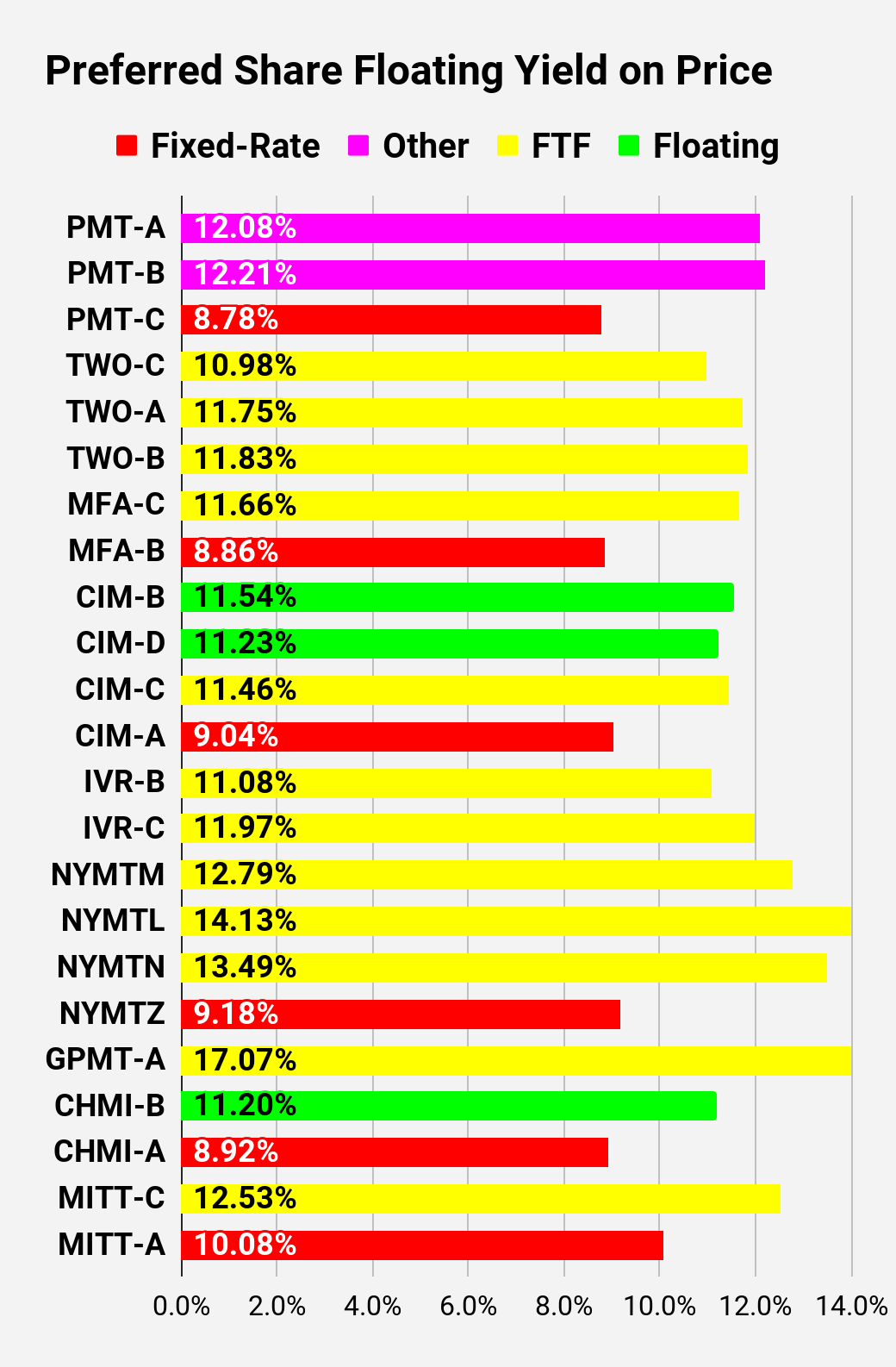

Most well-liked Share and Child Bond Charts

I modified the coloring a bit. We would have liked to regulate to incorporate that the primary fixed-to-floating shares have transitioned over to floating charges. When a share is already floating, the stripped yield could also be completely different from the “Floating Yield on Worth” attributable to adjustments in rates of interest. As an example, NLY-F already has a floating charge. Nevertheless, the speed is barely reset as soon as per three months. The stripped yield is calculated utilizing the upcoming projected dividend fee and the “Floating Yield on Worth” is predicated on the place the dividend can be if the speed reset at this time. In my view, for these shares the “Floating Yield on Worth” is clearly the extra vital metric.

The REIT Discussion board |

The REIT Discussion board |

The REIT Discussion board |

The REIT Discussion board |

The REIT Discussion board |

The REIT Discussion board |

The REIT Discussion board |

The REIT Discussion board |

The REIT Discussion board |

Notice: Shares which are categorized as “Different” will not be essentially the identical. Inside The REIT Discussion board, we offer additional distinction. For the aim of those charts, I lumped all of them collectively as “Different.” Now there are solely two left, PMT-A and PMT-B. These each have the identical problem. Administration claims the shares will probably be fixed-rate, regardless that the prospectus says they need to be fixed-to-floating.

Most well-liked Share Knowledge

Past the charts, we’re additionally offering our readers with entry to a number of different metrics for the popular shares.

After testing out a sequence on most well-liked shares, we determined to attempt merging it into the sequence on widespread shares. In any case, we’re nonetheless speaking about positions in mortgage REITs. We don’t have any want to cowl most well-liked shares with out cumulative dividends, so any most well-liked shares you see in our column can have cumulative dividends. You possibly can confirm that through the use of Quantum On-line. We’ve included the hyperlinks within the desk under.

To raised set up the desk, we wanted to abbreviate column names as follows:

- Worth = Latest Share Worth – Proven in Charts

- S-Yield = Stripped Yield – Proven in Charts

- Coupon = Preliminary Fastened-Charge Coupon

- FYoP = Floating Yield on Worth – Proven in Charts

- NCD = Subsequent Name Date (the soonest shares could possibly be referred to as)

- Notice: For all FTF points, the floating charge would begin on NCD.

- WCC = Worst Money to Name (lowest web money return potential from a name)

- QO Hyperlink = Hyperlink to Quantum On-line Web page

Second batch:

Third batch:

Technique

Our purpose is to maximize complete returns. We obtain these most successfully by together with “buying and selling” methods. We recurrently commerce positions within the mortgage REIT widespread shares and BDCs as a result of:

- Costs are inefficient.

- Long run, share costs usually revolve round e book worth.

- Brief time period, price-to-book ratios can deviate materially.

- Guide worth isn’t the one step in evaluation, however it’s the cornerstone.

We additionally allocate to most well-liked shares and fairness REITs. We encourage buy-and-hold traders to think about using extra most well-liked shares and fairness REITs.

If you need notifications as to when my new articles are printed, please hit the button on the backside of the web page to “Observe” me.

[ad_2]

2024-07-26 02:36:16

Source :https://seekingalpha.com/article/4706955-2-big-dividend-yielders-and-my-rant-about-accounting?source=feed_all_articles

{kind=link}

Discussion about this post